After the Fallout: Yields Spiral

Yields, Tariffs, and Semiconductors

This week’s will have a bit of macroeconomics and semiconductors.

Tariff Relief

If you haven’t heard, Trump is pausing additional reciprocal tariffs on anyone not named China. Here’s the potential impact of the new higher China tariffs, sourced from Bloomberg. Additionally, China is pursuing an origin of semiconductor tariff, which is sending Texas Instruments down today.

As you may have heard, there’s a loophole for servers, specifically GPUs and others. SemiAnalysis did a great job on it here. Now that we are done with the worst-case scenario, pricing is not as bad, and how that is going is a bit mixed. Yesterday’s price action in stocks was among a handful of the best days ever in stocks. You must return to the 1920s and 30s during the Great Depression to get more enormous relief rallies.

But that’s the thing. You have to go back to the 1920s for a relief rally that large. Given how oversold we were, I am positing that Wednesday’s was a bear market rally, which was long overdue. Stocks had almost the worst three-day return since, you guessed it, the Great Depression. It makes sense a rally would happen as well.

Since tariffs are not the worst case, the whole world is breathing a sigh of relief. But I ask you—how is a 145% (likely some deal lower) tariff on China and a global 10% tariff a good thing? This is what the market is pricing in today! We will chop and likely be in a confusing market for some time.

But it’s time to shift your attention from stocks to bonds and currency because that’s the real action.

Yields Up, Dollar Down

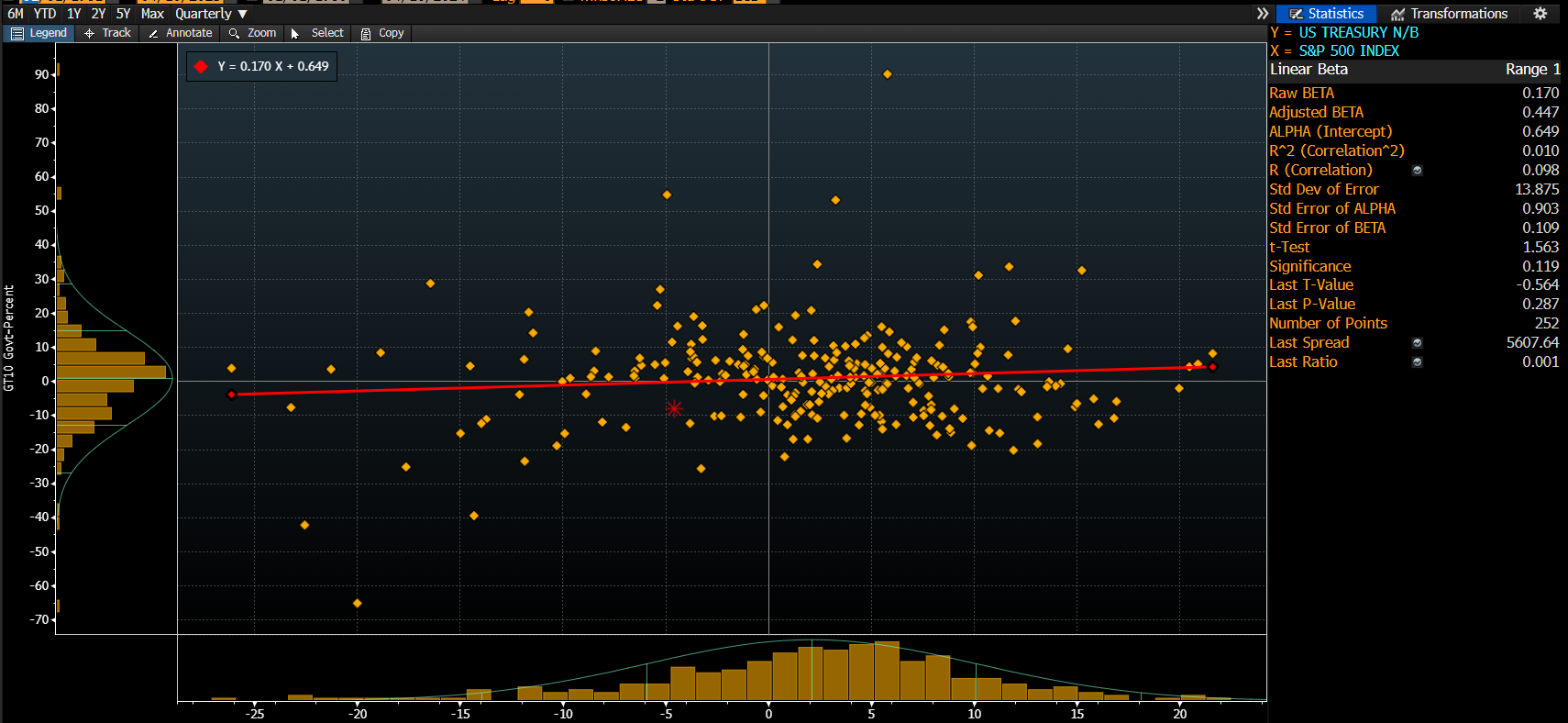

Historically, there is a simple but fundamental relationship between bonds and stocks. This effectively becomes a strong, diversified portfolio with a slightly positive beta over time. There is one issue—and this is the issue during all recessions. All betas are headed to 1.

This is the real “scary” leg of this entire story today. Treasuries are starting to scream something is wrong, not the short end but the long end. A primer on the 10-year if you know nothing. The 10-year treasury rate is considered the “risk-free” rate. This is the safest possible asset in the global universe of securities over the long run, and the entirety of international finance is graded as a curve against that baseline of risk.

That “risk-free rate” is supposed to reflect long-term GDP growth and an inflation premium to reflect longer-term inflation. Now, this is, of course, assuming the risk is zero.

There’s also another part of the story that is extremely important to consider. US treasuries, especially paper, are the plumbing of the world’s financial complex. Longer-term debt is present as well, but foreign nations heavily own it. The major holders are the Federal Reserve, Japan, China, the UK, and the rest of the world.

Now here’s why I think people are freaking out about the treasury rate right now. Inflation expectations (I guess a bit stale) are going down. This estimate uses a derived index of inflation-adjusted bonds and the actual treasury yield.

So either you have to believe real growth is about to accelerate, or there’s something much more scary. Contracts based on recession probabilities signal that some betters believe in a coming recession. So inflation expectations are flat-ish while recession belief is higher, and yields are higher, which means bonds are pricing in risk.

Let’s discuss another confusing aspect: the “basis trade” and China owning so much of our treasuries. Because there is feasibly a world where a run on treasuries can begin, and that, my friends, really sucks if we live in a post-Bretton Woods world.

The basis trade is the arbitrage between futures and cash treasuries. This popular trade picks up a few bps of returns and uses heavy leverage, but when the underlying (UST) moves heavily, it disrupts the trade. Typically, the trade has short futures and long underlying, creating liquidity during good times but increasing fragility during duress. We are starting to see the duress become a self-inflicting margin call.

Even worse, there is a bit of a reflexive loop here. The more selling that happens, the worse the price gets, and if you’re smart, you can panic early. There is a problem because if we look at the above holders of US Treasuries, China, Japan, and the UK are the biggest foreign holders. These are the countries the US is antagonizing with the tariff trade war. What happens if they sell bonds out of spite? This could create a self-reflexive run on treasuries. And as losses become worse, selling becomes frenzied.

This is a real risk, which is why markets continue to freak out. We don’t see what I would call true panic, but since everyone knows that someone could call fire and the theatre only has one door, people are walking to the door.

Higher interest rates also have the reflexive property of making the United States inherently a worse lender. Remember, we are raising interest rates in a country with a massive deficit. If a true run on treasuries were to begin, the logical response would be to pursue austerity as soon as possible, throwing the United States into a recession. The state of fiscal and monetary policy in the United States is between a rock and a hard place.

I don’t think we are at the point of economic brinksmanship, but if we were, the Fed would step in with its infinite balance sheet. They could print money to buy long bonds and create an orderly market. Ironically, the history of QE announcements almost always increases long bond rates. So, interest rates in the United States are probably going up, whether if it’s inflation, a risk premium, or forced selling.

I am unsure what inning we are in - but another observation I must make on top of the treasury concerns is the dollar. The dollar is now quickly exploding in a way that is screaming that assets are fleeing the United States asap. There are legitimate conversations about the United States seizing Norway’s assets as a move to negotiate for Greenland. If I were a foreign US asset owner, I would panic early.

It’s ironic that the consensus macro trades going into the election were a stronger dollar and lower rates, which is the opposite of what we are seeing today. Markets are always fun, huh? Anyway, for some updated thoughts on investments and macro takes (hopefully, my last one; I’m tired), please refer to behind the paywall.