AMD's MI300 Disappointment, Hyperscalers Capex, and FPGAs

This is my earnings overview for the Hyperscalers, AMD, and thoughts specifically on FPGAs.

I will start with a free AMD section, and then the rest of this post is behind a paywall. Shares are down ~6-7% on last week’s result. Let’s talk about the result and why it was so disappointing.

AMD exactly matched EPS, was slightly light on revenue, and guided essentially in line with Q2 guidance.

Advanced Micro Devices reports Q1 EPS $0.62 ex-items vs FactSet $0.62

Reports Q1:

Revenue $5.47B vs FactSet $5.48B

Q2 Guidance:

Revenue $5.7B +/- $300M vs FactSet $5.73B

This also was one of the slightest EPS and revenue beats in recent years. The last time this happened, the PC segment was imploding. This time it’s embedded revenue.

However, the real thesis point here hinges on MI300, and that was where the disappointment came from. I want to remind you that last quarter, they guided to $3.5 billion in MI300 revenue, and at one point, the buy-side expectation was $5-6 billion for the year. Instead, they were guided to $4 billion for the rest of the year. That was disappointing, but maybe AMD is sandbagging for the rest of the year.

MI300 demand continues to strengthen. And based on our expanding customer engagements, we now expect data center GPU revenue to exceed $4 billion in 2024, up from the $3.5 billion we guided in January.

Remember that AMD has a window of competitive strength from Q1 to Q3 to the middle of Q4 for AMD’s MI300X. B100/200 ramps will happen in Q4 and have a much better TCO, and then the R100 product launch will occur by Q1 2025.

Put differently, this is the only moment for AMD’s silicon to shine, and if they can only put up these numbers, it’s questionable what the future is here. What’s worse, the supply and demand questions created real confusion. Let’s walk through some of that.

One of the first lines of questioning was if a partner (implied to be Samsung) was creating a delay in supply, and thus that was leading to sluggish MI300 revenue. Lisa shot that down and said that their supply ramp is going very well, and it’s the fastest they’ve ever done a product ramp. They also said they would do better with more supply in 1Q and 2Q.

I think Q2 will be another significant ramp. And we're going to ramp supply every quarter this year. So I think the supply chain is going well. We are tight on supply. So there's no question in the near term that if we had more supply, we have demand for that product, and we're going to continue to work on those elements as we go through the year. But I think both on the demand side and the supply side, I'm very pleased with how the ramp is going.

But Vivek Arya (best question on the call) pretty much asked what your exit rate is, and given you are halfway through the year, you should have more visibility. Lisa’s answer was a bit disappointing and confusing. The implication is that they have a supply capacity in the second half above $4 billion, and the guide is, in fact, demand, demand-driven.

Yes. Vivek, let me try to make sure that we answered this question clearly. From a full year standpoint, our $4 billion number is not supply capped -- I'm sorry, yes, it's not supply capped. It is -- we do have supply capability above that. It is more back half weighted. So if you're looking at sort of the near term, I would say, for example, in the second quarter, we do have more demand than we have supply right now, and we're continuing to work on pulling in some of that supply.

That means that in the second half, they are not supply-capped; they might just not have orders. That also aligns with the timing of Nvidia’s product ramp. The reality is that MI300 might be dead in the water. Share gains are not happening, and Broadcom is winning second place much quicker than AMD.

But that isn’t the only part of this story that makes this result disappointing. Looking at every other segment, you will see that AMD had a pretty mediocre quarter. Even if MI300 ramps quickly, there is the rest of the business to contend with, and there are weaknesses in every segment. Gaming, Embedded, and even the datacenter CPU business was not as strong as hoped.

The data center implied MI300 revenue is about ~600 million for the quarter, which means about ~34% revenue growth YoY for DC CPU. That’s a strong result, given the cannibalization of server share, but much below the original Genoa share gain thesis.

However, the real issues began with the client, who took a bit of a share from Intel. It’s just not that profitable at this point, and Intel and AMD are fighting in price in this segment. I think share gains from here will start decelerating, especially if Intel launches a resurging 18A process in 2025. This segment is a mature business now and shouldn’t be worth much. Now, let’s turn to gaming.

Revenue was down sequentially 33% and almost 50% YoY. Consoles are clearly in the off cycle, and they expect next quarter to be no better. They expect a “significant double-digit percentage” decline in embedded and gaming, and I think the cycle there is now just starting in earnest. This is not a great result.

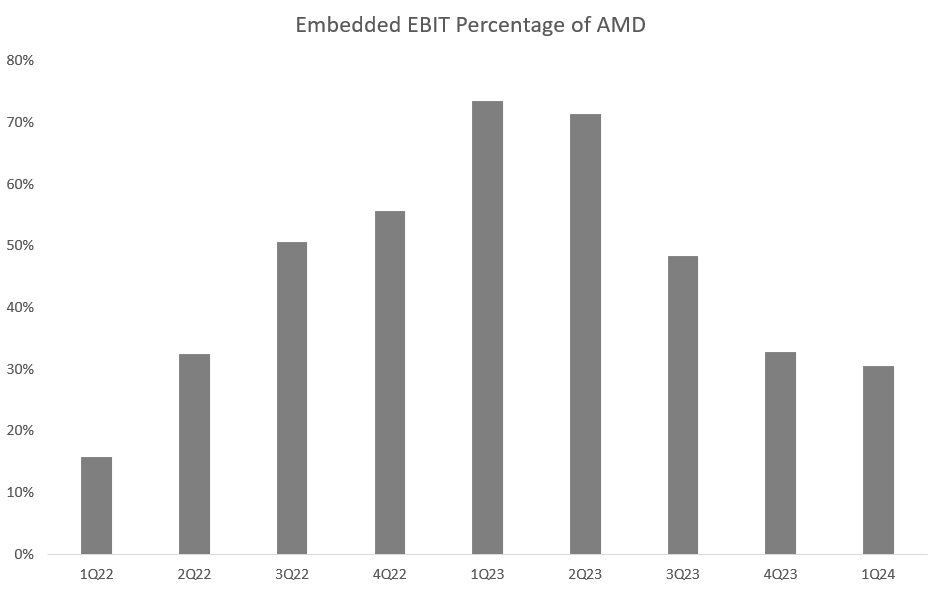

That brings me to Embedded. One of last year's sneaky aspects is that AMD’s EBIT and profitability have been driven mainly by embedded. Xilnix and FPGAs were a bellwether last year when the PC business went through the cycle. However, as the CPU business has improved, FPGAs are starting to decelerate. Historically it was a meaningful amount of the total profit at AMD.

In 1Q23, it was 70% of EBIT, and now, as a data center, EBIT is finally growing, and embedded is decelerating. In the very near term, I think this is just another point of frustration for AMD. Still, I will point out that embedded will likely start to grow again in conjunction with data center revenue in the second half of this year. When that happens, the financial model will finally start to work again.

But when this happens, I believe the forward-looking data will have to contend with Intel's real competition in Client and Nvidia’s R100 product, making the MI400 product a complete dud. Looking to the future, AMD's competitive positioning is about to get a lot worse before it gets better.

The real bit of hope is that a new console cycle eventually happens and that FPGAs finally come through. I am much more bullish FPGAs than MI300 and have some extended thoughts behind the paywall. The clear driver out of the AMD rut is embedded, not MI400.

I remain concerned about AMD. I think their competitive positioning is the very best it will be for the next two years, and they are not able to pull forward the revenue they need to be doing to make a competitive install base in the hyperscalers. Google Cloud is not even planning to offer AMD’s chips, so let me ask you, what is the future plan at AMD? Because it’s current accelerator product looks like it will not be remotely competitive to Broadcom’s custom solutions or Nvidia’s merchant. So we have to face the fact that AMD’s future is an x86 CPU maker, which is not a great place to be, and even then, they face increasing competition from Intel.

I am very negative about AMD's competitive positioning. The multiple has ripped on the hope that they will be a number two to Nvidia when in reality, the hyper scaler’s own custom chips will serve that function. Somehow, it trades a premium to both and is going through a particularly nasty FPGA cycle. MI300 couldn’t move estimates up for the year meaningfully after almost every cloud company raised capex meaningfully. That implies that it is, in fact, a demand issue.

To me, AMD’s future value seems much lower than the multiple the market currently values it at. It’s time to wake up from the Client story and face reality.

Speaking of which, I dive more into the capex results for the significant clouds behind the paywall and some thoughts on FPGA companies.

Hyperscaler Capex

Let’s talk about hyperscaler capex. Because of this earnings season's takeaways, every hyperscaler raised their 2024 capex numbers, and most did so meaningfully. Every major company is guiding to acceleration.