China's Revenge: The Tower Semiconductor Deal is in a Tough Place

Given the Rogers Deal Break, Tower Semi and Intel seem unlikely to go through.

Paid Subscribers: I’m trying something different. This is going out to everyone and will be unlocked a week later. I think noting Tower Semi’s fragile deal is actionable, but everyone should read about it. Just not today. This post will unlock in a week.

I’ve been on the podcast circuit quite a bit to talk about the US and China export controls. First on ChinaTalk with the Chips avengers, then on Transistor Radio with my good friend Dylan.

But beyond the podcast discussions, the question everyone has been grappling with is how does China respond? I don’t know the broad mechanism they will choose, but I finally found a simple one that impacts public markets. SAMR deal approval.

SAMR stands for State Administration for Market Regulation and is the Chinese anti-trust body that approves mergers similar to the US Federal Trade Commission. But this is China, and every regulatory agency is just an extension of the party’s will, so I think the clear way to hinder the United States and its companies are to block every deal in the approval process.

It’s already happened, as Chinese regulators blocked the Rogers corporation deal. We should expect this to happen to more companies, especially in the semiconductor industry. Check out this traumatic Rogers chart.

Two big semiconductor deals could be blocked for those not keeping track. Silicon Motion and Tower Semi are both in the process of getting SAMR approval, and the spread reflects a low likelihood of approval. I’ll briefly touch on SIMO before going in-depth on Tower because the first is nice to have, and the second is truly strategic and would cripple the United State’s plan for domestic production.

Silicon Motion Deal

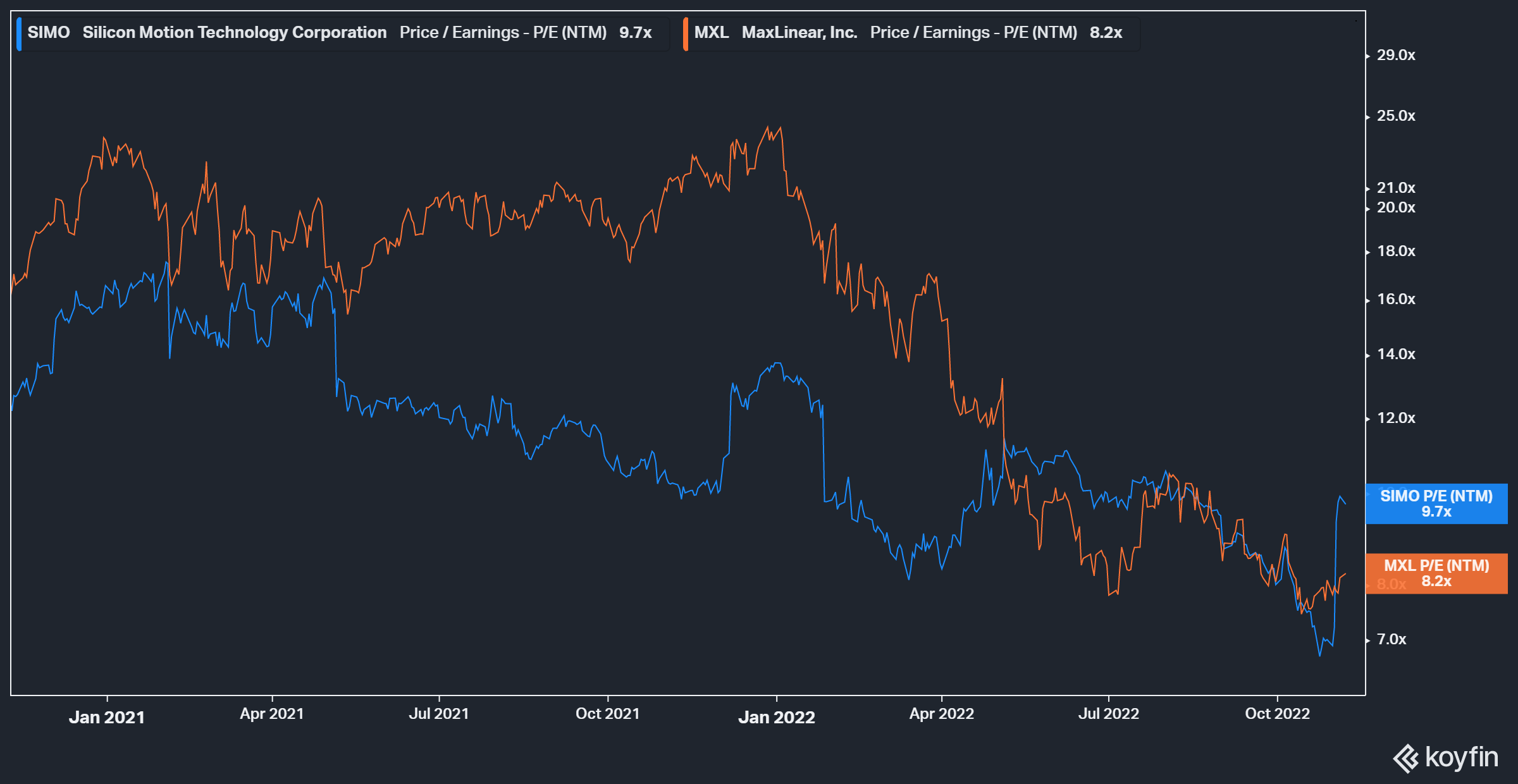

On May 5th, 2022, Maxlinear announced the intention to buy Silicon Motion. I wrote briefly about it at the time, thinking that the deal didn’t make much sense. With a bit more time, I have a bit more perspective. The goal is to create a mini-Marvell, and I can almost understand the logic. Both stocks have taken it poorly, and the semiconductor market is slightly different now than it was then.

Let’s review the offer again.

In the merger, each American Depositary Share (ADS) of Silicon Motion, which represents four ordinary shares of Silicon Motion, will receive $93.54 in cash and 0.388 shares of MaxLinear common stock, for total per ADS consideration of $114.34 (based on MaxLinear’s May 4, 2022 closing price). The strategic business combination is anticipated to drive transformational scale, create a diversified technology portfolio, significantly expand the combined company’s total addressable market, and create a highly profitable cash generating semiconductor leader.

That’s quite the deal premium. Even without the equity consideration, that’s a huge discount. What’s worse is that the actual economics of the deal have meaningfully eroded. During the announcement, the deal was expected to be immediately accretive to Operating Income and EPS, but given Maxlinear’s shares have fallen, the equity consideration is now not accretive, and Maxlinear likely would receive a much better return just repurchasing shares.

MaxLinear’s P/E (earnings yield) is now higher than SIMO's! So they would receive the same return ex-synergies if they just repurchased their stock with cash. The market is a bit of a hater on this deal. Back to SAMR.

One reason the deal premium is so steep is that Silicon Motion is a Hong Kong-domiciled entity and a leader in global NAND flash controllers. This isn’t the most strategic asset on the block, but in a global economic war for semiconductors, you want every arrow in the quiver you can get. I don’t think the CCP would want SIMO to go to an American company, and more so after the United States crippled the Chinese domestic semiconductor industry. The odds of this deal going through feel close to zero, and the market agrees.

Ironically I think that’s a good thing for Maxlinear. The cash consideration at the time was going to a company now expected to make meaningfully lower earnings amid the global memory correction. Now forward EPS estimates are 50% lower! If geopolitics is the way out of the deal, then so be it.

Additionally, in the deal proxy, they mentioned this important date for the SAMR submission, and I have been unable to find the filing on the SAMR website.

The Company and Parent believe they are eligible for a simplified filing in the People’s Republic of China and made such a submission to SAMR on July 6, 2022, which, if accepted by SAMR, could result in a determination in or around 3 months. SAMR may require a longer review under their normal procedures, which would delay a final determination into the second or third quarter of 2023, or even longer.

We are in the “even longer” period already. Silicon Motion shareholders approved the deal (duh, that’s a hefty premium), but I think SAMR will knock it down.

MaxLinear’s shares should eventually rise on the deal break, and Silicon Motion should fall, albeit how much further than a price that reflects an 80% premium to the deal, I don’t know.

From that perspective, I think it’s an insane risk-reward in the unlikely case it gets approved to be a SIMO shareholder. The downside should be lower, but it’s incorporated partially. But I don’t recommend doing that or touching SIMO at all. MaxLinear, maybe it’s time to be constructive on. Tower, however, is another story.

Tower Semiconductor and Intel

This is the deal that I have been thinking quite a bit about. I wrote about this deal much more extensively when it got announced, but I am now worried about the possible closure.

Unlike SIMO and MaxLinear, the deal is pure cash. Tower Semi trades at ~40 dollars today, and the cash offer is $53, or 30% higher than today’s price. I love the strategic rationale here, as Tower is the largest independent fab that Intel could likely swallow (sorry about missing GlobalFoundries Intel). That would kickstart a foundry culture and team with industry-standard workflows and customer-facing. This is the Petri dish to grow IFS from, and I think Tower is key for long-term foundry success. China wouldn’t want that.

Meanwhile, China just got kneecapped by the Bureau of Industry and Security (BIS). Almost all leading-edge efforts by China have been thwarted. The United States is directly trying to stop China’s semiconductor independence and pulled out all the stops with its recent export controls. Meanwhile, Intel is trying to bolster domestic production and reduce the United State’s reliance on Taiwan. Why would China let Intel, and by extension, the United States government, do this? They will almost certainly block the deal. But let’s first examine China’s legal case.

Why does an Israeli company without Fabs in China need deal approval? Well, that’s because any company that hits a revenue threshold of ~55 million dollars in China is subject to SAMR review. It’s possible to merge without Chinese approval, but then China could restrict Intel’s right to sell products in China. That’s 30% of sales!

Maybe that would be impossible, given China’s reliance on global semiconductors. Still, they could be unilaterally punitive to Intel if they merged without SAMR approval to “restore competition to the market.” So I think the more likely option is a deal delay and eventual break. That would not be good for Tower.

I think Tower Semi would go much lower in a deal break, at least to the mid-30s, possibly high 20s per share. Given Rogers moved much lower than the pre-deal price, $25 seems possible. That seems asymmetric.

But I acknowledge that in this environment, that’s a frustrating short. Stocks seem to be going down every day, and I would guess that it will take at least until 2023 to get your catalyst of the deal falling through. The deal spread already has reacted to the Rogers break by going down 6% last Wednesday, but the spread should intuitively widen. If this is the bottom of the semiconductor cycle (possible), this is a good short as all stocks rip higher.

Meanwhile, I am saddened by Intel. I understand the competitive dynamics at AMD and the layoffs, but not getting Tower Semi to kickstart IFS feels like a national security travesty. Intel has a lot of unwinding for its fab and foundry, as they mentioned on their last call. I highlighted this in my last post.

But there's been many of these areas that I described that there hasn't been this intense accountability. Steppings were done too easily and without the quality A stepping. And some of that came through or stumbles as you went with 14 and 10 nanometers, but we lost the discipline of the understanding of what steppings cost and not just in the fab but also in the validation cycle.

Also, we expedited all the time. While expedites are a good thing when you're bringing a new product to marketplace, but they also create fab inefficiencies, and the results of that are we're not being accountable for the fab efficiencies. Otherwise, our margins will be markedly higher than they are today

Tower Semi is a quick way to make the IFS dream a reality and has to be at the top of Intel’s strategic priorities. But this is how China can strike back. The market is not pricing the deal break risk well because it’s a logical next step to block. And allegedly, SAMR hasn’t even reviewed the Tower Semi deal yet.

If you enjoyed this post - consider sharing or subscribing! Until next time.

What are your thoughts today about the deal?

Thanks for this Doug. On the SIMO transaction, the stock has moved up about 20% since you wrote this (I think the Semi index is flat or down slightly). What do you think the market is seeing here ? More positive on SIMOs business or greater likelihood the deal is approved?