Chinese EV's and the Lagging Edge Price War

Prices cuts imply price wars, Western chip subsidies are against strategy spending in China. Full stack margin at Chinese Automotive makers means China should win.

Are you an avid reader of this Substack and will be in Taiwan during Semicon? You should come to this free meetup that is cohosted by me, Jon, from The Asianometry Newsletter and Dylan from SemiAnalysis.

Get your tickets here!

Now for this week’s note and probably what I’ll talk about at the meetup. I think there’s a potential for a price war at the lagging edge. Let’s discuss.

This earnings season has highlighted the robust performance of older-generation ("trailing edge") companies. Their inventories have also been rising. At the same time, there's a noticeable demand slump in China. Surprisingly, Chinese semiconductor firms are increasing their investments in older technology, known as the "lagging edge" capacity. Put the pieces together, and there’s a big story here.

This story complements another major development: China's upcoming electric vehicle (EV) export surge. For a detailed overview, check out the Asianometry video below. The goal for China is to increase its footprint in the EV market substantially. Their market share may be modest, but as they introduce a diverse range of models, this will likely shift.

China's strategy for the EV market involves ramping up its production capacities. Vertical integration is the goal exemplified by companies like BYD. There's also emerging competition in China's lower-tier semiconductor market, highlighted by NXPI's observation on low-end microcontrollers:

I mean we -- I can only report here what we are witnessing -- the only 1 place where we see more extended pricing pressure is low-end micro controllers in China.

Connecting the dots, price competition seems imminent. For example, Texas Instruments has already reduced prices to expand its market share in China. With China increasing its investments in the semiconductor market, especially the lagging edge, there's potential for a price war. Aggressive capacity expansion into high inventory sounds like a bad outcome.

East vs. West Dynamics

On one side, we have Western semiconductor giants, such as Texas Instruments (TXN), Microchip (MCHP), and Analog Devices (ADI). They have historically high inventories and are building new factories on the back of CHIPS Act subsidies. Texas Instruments now has over 200 days of inventory, banking on the longevity of its products. Microchip and Analog Devices will likely tread similar paths. The CHIPS act further motivates these Western firms to invest heavily now for the future.

In contrast, after facing restrictions on accessing cutting-edge chips, Chinese semiconductor players are doubling down on older-generation semiconductors. Their objective is to capitalize on the worldwide EV export surge. With many of these companies being state-owned and vertically integrated, they are not required to have high returns on capital. However, a concern is China's tendency to disrupt markets by oversupplying. This was evident in the solar market, with a looming possibility of history repeating.

While manufacturing semiconductors is complex, entering the older "lagging edge" market is more accessible. This segment once faced a massive supply gap, but now there's a growing risk of an oversupply. Let’s talk about lagging edge capacity shortages, and how much capacity we need.

How Did We Get Here? And How Much Capacity Do We Need?

I have written quite a bit about the lagging edge supply problems. In “The Rising Tide of Semiconductor Cost,” I talked about how old depreciated fabs are being run for profit and how the increase in Automotive content creates demand for these fully depreciated products. Adding capacity means capitalizing a new fab’s cost again, and that means higher costs.

The lagging edge refers to technologies older than 7nm. A significant number of existing fabs manufacture these chips. According to ASML's slide from their recent investor day, over half of all produced wafers fall into this category. Excluding memory chips, the volume of lagging edge wafers overshadows the leading edge by a 5 to 1 ratio. Moreover, the lagging edge is now expected to grow, bucking the trend of recent history.

The supply-demand dynamics of the lagging edge are odd. The 2020 chip shortage hit the lagging edge the hardest, unable to match the responsiveness of the leading edge. Leading-edge capacity responds to customer demand tightly with new capacity, while the lagging edge revolves around managing the depreciated historical manufacturing base.

The current demand for older chips has reshaped lagging edge pricing and value dynamics. Despite transitioning from shortage to surplus, long-term agreements have raised pricing in the entire market for now. I see potential price wars in select markets where China’s aggressive investments in the lagging edge can ruin good markets.

For instance, BYD, a major player, internally sources around 34% of its Power Management Integrated Circuits (PMIC). Their capacity has surged by 140%, while the entire market has grown by 43%. Chinese companies, in general, are expanding faster than their Western suppliers.

Although the Chinese demand has been below expectations, there’s a clear distinction between companies focused solely on semiconductors, like STMicro and OnSemi, and those like BYD, which sell cars. BYD aims to maximize car sales profits by producing chips tailored for their vehicles. This vertical integration threatens the profitability of standalone semiconductor companies. Most of those standalone companies happen to be Western Semiconductor companies.

Projecting Capacity Additions

The situation might stabilize if capacity additions match market requirements and if Chinese stakeholders act rationally. Data from ASML paired with my estimates (large range, not precise) has Chinese investment this year meeting between 40 to 100% of demand! I think the assumption that it’s only 5 billion per 100K WSPM is conservative, and in reality, Chinese capacity is meeting around 50%+ of capacity.

To put it plainly, China's expansion in the lagging edge might suffice for the majority of growth, not even considering the investments made by Western firms. The large capacity additions at Western Analog giants could end up with poor investments.

Future Industry Outlook: A Potential Decline in Profits

Western semiconductor manufacturers specializing in automotive products will struggle against car companies opting for vertical integration, like BYD. Vertical integration seems poised to prevail.

This scenario is problematic for Western semiconductor producers. While the market won’t solely consist of Chinese EVs, their growing share implies slower growth for companies that aren’t vertically integrated. As pricing decisions are influenced by marginal costs and returns, the automotive sector's profitability might be nearing its peak. This situation is exacerbated by the influx of capacity additions.

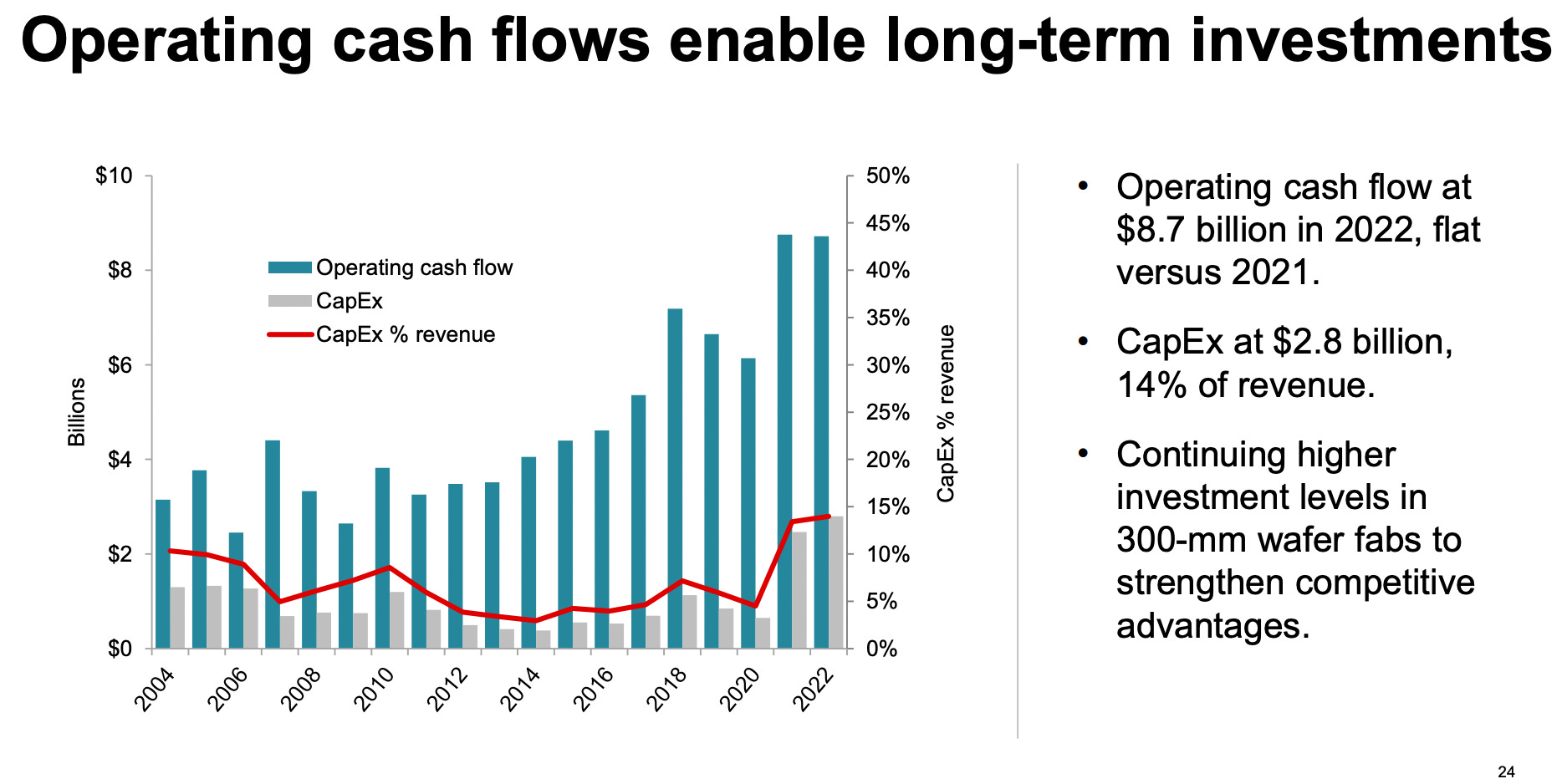

Take Texas Instruments as a case study, their historical success, measured by strong cash flow margins, was due to low capital expenditure (capex). From 2006 to 2020, they allocated only 5 to 10% of their revenue for capex. Their new projections assume 15% of revenue dedicated to capex, a meaningful escalation in spending.

Investing in more capacity while facing vertically integrated competitors hints at a decrease in future returns. Texas Instruments’ strategy might be optimistic, referring to the stable supply conditions of the 2000s instead of the future vertically integrated customers. The future might not look like the past.

Broadening the lens beyond Texas Instruments, these observations apply to various semiconductor components, from PMICs to IGBTs to Automotive MOSFETs. Wherever a vertically integrated Chinese fab intervenes, profit margins are likely to plummet. A transition from supply shortages to excesses is inevitable, and with the automotive pivot, parts of the semiconductor industry may face shrinking profits. Brace for a price war.

Post Script: Okay guys, I write big industry pieces like this, and I promise this will not happen in the next few quarters. Things take time, but if you are not concerned about BYD becoming a semiconductor producer to drive lower-cost EVs, I don’t know what else to tell you. There are going to be problems to come. I’ll keep you updated. But if you enjoyed this - consider subscribing or sharing this piece!

Hi Doug! When referring to BYD's vertical integration & PMIC, does BYD design its PMIC or does it both design & fabricate its PMIC chips. In the latter case it will have its own semiconductor fabs.

Have you noticed similar vertical integration outside of BYD, both in auto & non-auto sector?

Thanks in advance.

Interesting. But does TXN, ON, NXPI, etc sell to Chinese OEMs?