December Semiconductor Quarterly Roundup

Plus a high-beta semicap idea!

Welcome to the second month of the monthly review of semiconductor stocks. This time it will be more quarterly focused, as it’s much less noisy. Please don’t take this too seriously, this is just a quick overview of price action and a recap for you non-generalists out there. I hope you can just refer to this and figure out what happened this quarter or what you might have missed. I’ll call out interesting things I see as well.

Domestic Universe Price Action

From a SOXX point of view, December was not quite the ripper that November was, but the 3 month period has been a very good one for semiconductor stocks in aggregate.

Let’s break it down under the surface, because there obviously is always more than meets the eye.

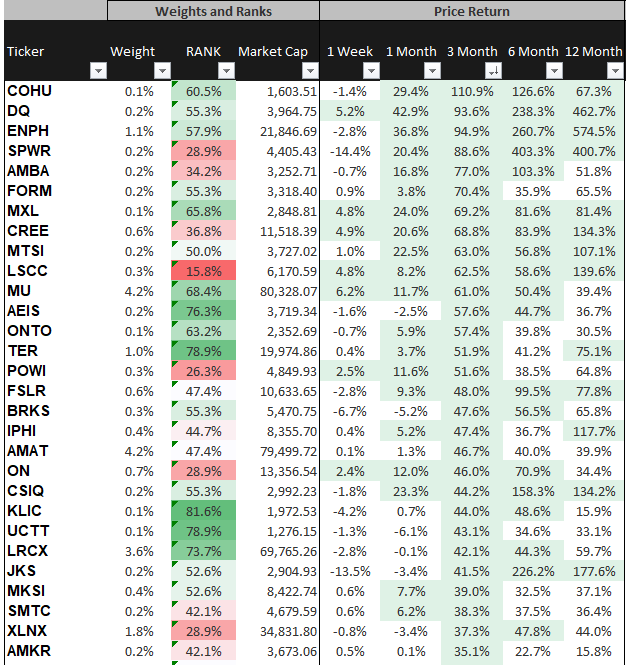

US Listed Domestic Winners

Takeaway #1 Testing stocks lead the way

COHU - Cohu got way too cheap during the March sell-off, and was pricing in some pretty terrible outcomes. A reminder that Cohu is the 3rd player in the test oligopoly, behind Teradyne and Advantest. All of those companies of course have done well, but Cohu has the most juice. They also very recently guided up during their analyst day.

I believe that this is yet another heat check on the demand-pull that is being shown on the semiconductor side. Between this and Micron, things are looking up.

FORM - I’ll have a little bit more on this one in a packaging stocks follow-up, but testing clearly is running the leaderboard recently. They are the global leader in probe card testing units, and this is something that will take share as advanced packaging continues.

Takeaway Number #2 - Solar and EV Names Continue Higher

DQ / ENPH / SPWR - It looks like post-election the market is seriously considering a green new deal. This has impacted DQ/ENPH/SPWR, all companies that primarily deal with solar. I am partially skeptical, as the industry has been prone to boom busts. However, it does seem that unlike the last time, solar’s cost advantage is likely permanent. This could still be the early stages of a secular shift, but it’s priced like it.

AMBA -Ambarella clearly got the EV bid this quarter. Financially the company doesn’t look very promising from trailing numbers, but clearly, the market is thinking their future is extremely bright. They are ~60-65% a security camera company focused on embedded and integrated SoCs that are put into cameras. The excitement around this company is their Automotive camera systems, which is ~15-20% and they expect the SAM could grow meaningfully from 2019 to 2025.

I got asked if this is safe to short and I truly don’t know. In my view, it is likely in the EV / Autonomous basket and probably trades with those companies. But let’s not kid ourselves, it’s a competitive space, with the likes of Nvidia, Renesas, TI, XLNX, and many other companies focused on automotive visual cores. At 12x sales and ~100x EBITDA with maybe a 30-40%+ revenue growth in their future, it seems egregiously expensive relative to hardware, but cheap compared to software. If you think of this as an “AI vision company” (their tagline) maybe you can justify it. I could be missing something here.

Meanwhile our Domestic Quarterly Losers

Takeaway #3 - Large Cap Semis were Left Behind

It’s amazing to see the size effect here, this is likely in conjunction with the IWM outperformance over the last 3 months. Intel, Nvidia, AMD, TXN, AVGO are literally the top companies in terms of size, and they all in aggregate brought down the market cap weighted return.

NVDA - I actually called this one out last month as being a company that seems well-positioned in the near term, but has lagged in recent months. I think this company continues to “take a break” and eat down their multiple as investors digest the stellar YTD results here. Nvidia was quite an impressive story in the first 6 months and has chilled out.

Intel - I don’t think I need to speak to this one here - I have and many others have written about it time and time again.

SWKS - I am not familiar with this company as much, but my understanding is they are a key Radio Frequency supplier to apple that is slowly getting designed out.

ACMR is one of my favorite names that I follow (not from a business but purely entertainment) - It is a US-listed Chinese Semicap specializing mostly in cleaning, but it’s most important customer of course is SMIC. There has been a reasonable short report on this company, but I believe that China’s willingness to back national champs will trump this.

International Universe Price Action

Call me absolutely surprised that GCL-Poly Energy, a Chinese solar company with very little financial disclosure is up 100% and tops the quarterly winners. Yet another repeat of theme #2.

Takeaway Number #4 - The Market Likes the Wafer Consolidation

Now, what is not really surprising is the Globalwafers price move, a reminder that a month ago the merger of the #2/#3 largest in the world looked really favorable, and it seems like the deal logic is being appreciated. I think this counts as a miss for me in my book, as I talked to a few people and seemed really enthused but didn’t really follow up on the lead. There are almost no small players in wafers globally anymore, and the intensely cyclical industry could improve as fewer players consolidate, a well-known playbook for the industry. All companies are cheap but maybe rightfully so, as it historically has been a deeply cyclical industry.

Takeaway Number #1 Repeated Internationally - Testing

Advantest / ASE Technology - This is interesting to see the testing share price at work internationally as well. FORM, Teradyne, and Cohu top the list of domestic, and clearly this is replicated internationally. Something interesting to me is that Teradyne’s results at least seem backed by fundamental momentum, with 40-50% revenue growth compared to Advantest’s -2% growth last quarter. Something is amiss.

The International Losers List

The one I have to talk about and have a take here is 981 - or SMIC. SMIC has been hit by a deluge of bad news. I wrote about this in the last update - check it out!

STMicroelectronics is currently undergoing a union protest in France but is well-positioned in Automotive regardless. If you believe this is transitory, this could be an opportunity.

Some Great Articles / Reads / News

I found this Advanced IC Packaging: Fundamentals For the ‘More Than Moore’ Era series on EETimes very helpful.

I really love everything that Erik Engram writes - and this RISC-V article helps put their positioning into a much better perspective. ARM will be the new x86, and eventually, RISC-V will succeed especially as their positioning for coprocessors is better.

Graphcore’s recent benchmarks and subsequent raise has created a lot of hype. Additionally, the AWS announcement means that of all the AI chip startups, it seems that the company firmly in the lead is now Graphcore.

“Graphcore has said previously that the IPU-M2000 has a recommended retail price of $32,450, though this does not include a CPU server also needed to run the system (Graphcore says this enables freedom of server choice). By comparison, the 8-GPU DGX-A100 starts at $199,000. An Nvidia A100-accelerated server with 4x A100 GPUs (Supermicro A+ Server 2124GQ-NART) including CPU starts in the region of $57,000.”

I’m excited about shake-ups at Intel, and Third Point’s letter to Intel seems to be a call to action. Intel was and continues to be funding short for me. The problem I foresee is that Intel’s fab doesn’t have an exciting customer base, and the x86 business is lackluster. Even with a shakeup, this is a hard road ahead. If you told me Intel was spun into fab and fabless, I wouldn’t buy either business.

I thought this very brief overview of GPU APIs was useful by https://threedots.ovh/.

Quick UCTT Idea

Last but not least I want to put out a quick UCTT idea. I want to stress that this isn’t exactly a wonderful company at a great price, but rather a fair company at a cheap price with a strong backdrop of revenue acceleration. If I had to characterize this investment, you are long small-cap growth with operational and financial leverage on WFE at a very cheap price.

ICHR and UCTT tend to trade at least somewhat in tandem over longer periods of time, or at least a 2-4x multiple discounts. The discount currently is much wider than it’s historically been.

The reasoning for the close multiple pair is that if you combine LRCX / AMAT as a percentage of sales for both ICHR/UCTT, it is practically 100%. ASM, another semicap player is the delta along with a mid-teens percentage of revenue service business. They are all very sensitive to WFE spending.

The result is that you end up with a staggeringly high beta company that tends to really swing whenever AMAT and LRCX move. Meanwhile, I believe that we just began the multi-quarter earnings surprise cycle. More can be found about that in my 2021 outlook piece.

Additionally, UCTT just did an interesting acquisition of Ham-Let that might actually be the mysterious acquisition candidate that NVMI meant to buy. Who knows - but what is more interesting to me is the absolutely lackluster synergies estimates in an industry that tends to have massive economies of scale. 20 million in EBIT synergies on this cost structure seems like a layup.

Between that and a strong fundamental setup for AMAT / LRCX - UCTT looks staggeringly cheap. I want to stress that this is levered beta exposure, and is not for the long term. You are getting long the end of the bullwhip just as the cycle gets moving fundamentally. I view it as leverage on AMAT / LRCX and you should too - and it’s sized accordingly as well.

In the long term, you want to set it and forget it with the likes of Monopoly-like Lam Research. But for now, this is just an interesting idea I thought I’d mention given my fundamental bullishness on the cycle.

That’s it for now - Happy New Years everyone! Here’s to an exciting and hopefully better 2021.

Thank you to all my new subscribers! Please give me any feedback on what you like to read about either via email or directly to me on Twitter @foolallthetime.

This may be the best $20/month I've spent.

did not know how to message you here, so commenting here :).

Would love to hear your take on the MU earnings and the impact to Lahm Research. Also, if you think Lahm is more exposed to NAND and less to DRAM?

Another one, which you have talked about but is there a piece you can reference too which gives overview of the "custom silicon" trend and who are the major players and your projected winners in that?