Earnings Coverage Part 2 for 2/5

QCOM/KLAC/KLIC/FORM/QRVO/IFX/ONTO/MPWR and a trade idea

More earnings so far. I’ll have a summary document eventually when this is all over trying to pick at themes of what has happened. So far my read is this:

Automotive is really firing on all cylinders and will be for some time

5G Phones are strong while base stations are weak

Sell the news on almost all companies even with extremely strong prints

Trade Idea - Buy KLIC and AMKR

Please read the KLIC portion - I outright am buying on these results. I additionally am buying a speculative position in AMKR (related OSAT) who is reporting earnings on Monday. AMKR has a catalyst in particular - earnings on Monday where they can give their long term guide.

It seems sloppy but estimates are not even close to correct right now - it’s likely trading on ~10x earnings. Even a very modest multiple expansion to their long term ~12-15x gets you upside. I know the results are not sustainable and it will be completely about long-term sustainability, but when a company is up 20% after growing and expecting to grow revenue 75% - you buy it. It’s that simple. This is beyond a shock and I didn’t realize until flipping through the results. KLIC is likely lower quality than most companies but has the lowest expectations of anywhere. Amkor is a similar situation but with earnings as an upcoming catalyst (shorter-term). KLIC will likely be a longer-term story.

Amkor has a very high correlation to KLIC results and AMKR reports Monday. This is very last minute but I do not think that the market is prepared for the guide - similar to KLIC. Read KLIC’s earnings summary then think of AMKR. That is what I’m thinking at least - forward guidance should massively accelerate.

Qualcomm

Results

Qualcomm reports Q1 EPS $2.17 ex-items vs $2.10

Q1 Revenue $8.24B vs $8.26B

Q2 Guidance of EPS $1.55-1.75 ex-items vs $1.58

Q2 Guidance of Revenue $7.2-8.0B vs $7.11B

“Notably, our strong performance and outlook would have been even stronger had we not been supply-constrained.”

5G revenue was astoundingly strong, with design wins and almost every segment materially above estimates. While this is a slight QoQ deceleration, it’s clear that 5G is here and ready to rumble. That being said sell the news is also in effect, and now questions on sustainability get asked on every call.

Quotes from the Call

One of the weirdest and saddest parts was the question on Nuvia - it is all but confirmed that Nuvia will not be making server chips anytime soon.

So Matt, let me just start, and I'll shift to Akash to talk about the TAM. Look, we're very excited about that acquisition. And it's probably very clear. If you look on the announcement we made, one thing that was really incredible is the support we received from the mobile ecosystem. Every single OEM was there with the exception of 2, which -- it doesn't really apply to them. And then you have the entire computing ecosystem there, both across the Windows and Chrome. For us, it basically reflects this view that we had of full conversions between mobile and computing. I think we're in the very beginning of that with our Windows and Snapdragon program. And create opportunities for us to do a step function increase in performance with the power advantage of Qualcomm, both across premium smartphones as well as the computing segment. And that is likely to be a key differentiation for Qualcomm going forward.

And really for the -- if you think about the addressable market for the PC and the Chromebooks market, this is over a couple of hundred million of units, right? So it's a very large market. And what's really important for us is to be able to combine CPU -- leading CPU technology, along with the other assets that we have in mobile and address this market in a differentiated fashion. And so we feel pretty good about our ability to do that.

I'll also say the CPU has a lot of implications outside mobile phones and PC market along with -- into auto and IoT as well. So it's an asset that's going to be broadly relevant to the end markets we pursue.

KLAC

Calendar Year Highlights

By End Market

The Guide

KLA reports Q2 non-GAAP EPS $3.24 vs consensus $3.20

Revenue $1.65B vs consensus $1.60B

Guidance of Non-GAAP EPS $3.23-3.91 vs consensus $3.22

Guidance of Revenue $1.665-1.815B vs consensus $1.61B

They believe that WFE will grow mid-teens off a 2020 baseline of 59-60 billion

They continue to return meaningful amounts of FCF to shareholders and are likely the most stable of all of the semicap companies. In my eyes, KLAC will likely have the best Sharpe ratio out of the oligopoly (ex-ASML of course)

Quotes from the Call

How KLAC is more driven to volume output instead of capital builds, and why their second half will likely mimic their first half. I expect them to underperform peers in the first half and outperform in the second half in terms of revenue growth.

So I think like a lot of things in this industry, KLA's exposure is -- there's less variability in it based on that fact. And so the volume considerations associated with CapEx impact us less than that.

And maybe Bren can give some color on how that looks for the -- as we go out through the year.

On whether if Services could grow to be even larger than systems over a longer period of time. It seems the answer is clearly yes.

Well, Krish, it will. It's 2 separate questions. It will because it's growing faster than the underlying Systems business. If you look at our service model, it's a 9% to 11% growth rate, which is what we articulated at Investor Day. And I'd argue that, certainly, the increase in demand we've seen on the Systems side gives us a tailwind to that growth rate moving forward.

There's -- clearly, customers are valuing the service offerings, particularly as you're seeing more and more demand at the trailing edge and the need for those customers to keep those tools up. A lot of those customers, particularly around automotive, are facing increasing reliability requirements, and that's driving more investment in process control and the information that comes off the tools.

So those have all been good drivers for us. So I keep thinking, look, 80%, 85% (attach rates), I think that's probably reasonable to think that we could aspire to get there. There's always dynamics for certain customers that prefer a billable model. And so we'll have to deal with that resistance to try to move to a contract structure. At the end of the day, contract structures allow us to optimize the cost structure underneath, and we can serve to an entitlement level that drives higher through-cycle profitability. So that's what we aspire to.

Just to add to it, I mean, the one other factor is the tools that are being shipped today, the complexity is such that if you think about a car analogy, it's pretty hard to service a car today. 15 years ago, it might have been different. And so you think about, over time, the complexity and the associated, more and more of our systems end up having more and more custom design parts throughout the system, and it just becomes more economical to rely on us.

And then there's no question that in service model, customer benefits from having a contract over the long term. They take the risk out of episodic events and they have more reliability of uptime.

On their ability to return cash to shareholders

And so when you look at what we're doing going forward, we expect that at a minimum, we'd be able to return 70% and investors can model that as they think about the returns profile over time. We're right around that this year, but this was a little bit of a unique year with some of the COVID dynamics at the beginning of the year. We did build our cash balance a little bit. But you're right, given the growth of the business, I would expect that we can deploy more. We do an exhaustive exercise here to understand the liquidity of the company and how much cash we need to run it, and we're operating at that level today.

And so we have to juxtapose those alternatives against opportunities for growth in the company, and I think we've done a pretty good job of that. But generally, I think the 70% tends to be a floor. And given the uptick in the business that we're describing, I would expect our quarter-to-quarter share repurchasing to increase as we go forward here.

On Margins and what their incremental margins have been and how they already are ahead of their long term target model

Well, there's always quarter-to-quarter fluctuations. But when you look at our long-term plan of growing our top line at least in the 7% to 9% range and dropping 1.5x that revenue growth rate in terms of EPS growth. But that drives effectively an incremental operating margin that's between 40% and 50%. And that's how we're going to run the company over time. So you always have the drivers that influence margin -- gross margin, whether it's a product mix. Obviously, service has a dilutive element at the gross margin line. But we factor that into how we think about the model when we put out there.

So yes, we're outperforming the public model. I think the strength and the speed of the growth that we've seen over the last couple of years has helped drive a fair amount of leverage in the business.

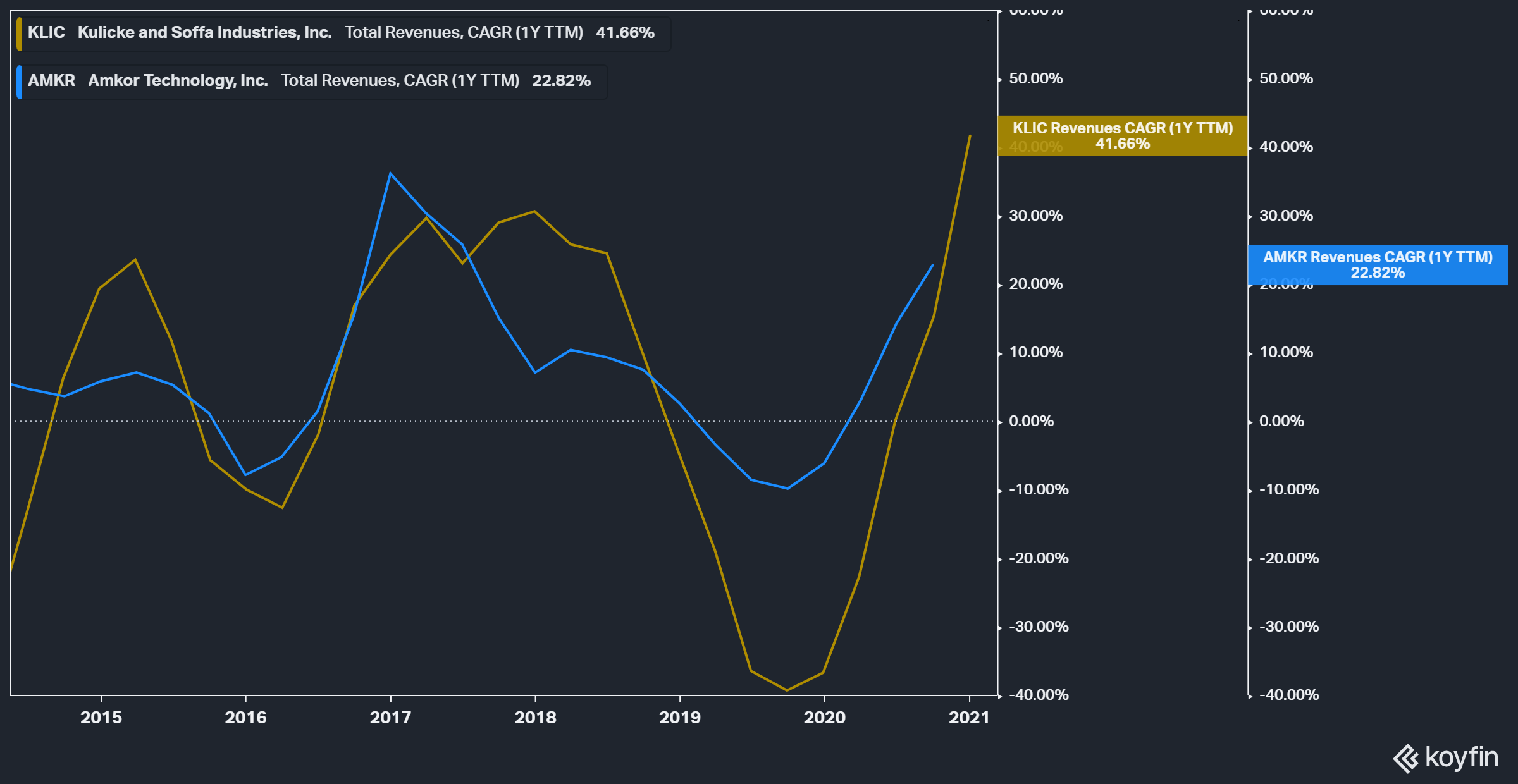

KLIC

Kulicke & Soffa was a real surprise to me. Increasingly it seems like the tide is lifting all boats, and the boats that are not often thought about are the ones that are truly surprising. I wrote briefly about KLIC in my packaging primer. They are the explicit leader in flip-chip, wirebond, and various other packaging technologies. I didn’t put the important part that actually the lagging edge is the tighter supply chain currently, and that disproportionally affects KLIC over wafer-level packaging plays.

Results

Q1 Outlook - or 100% YoY growth and it’s trading ~12-15x earnings

Kulicke & Soffa Industries reports Q1 EPS $0.86 ex-items vs consensus $0.75

Revenue $267.9M vs consensus $264.9M

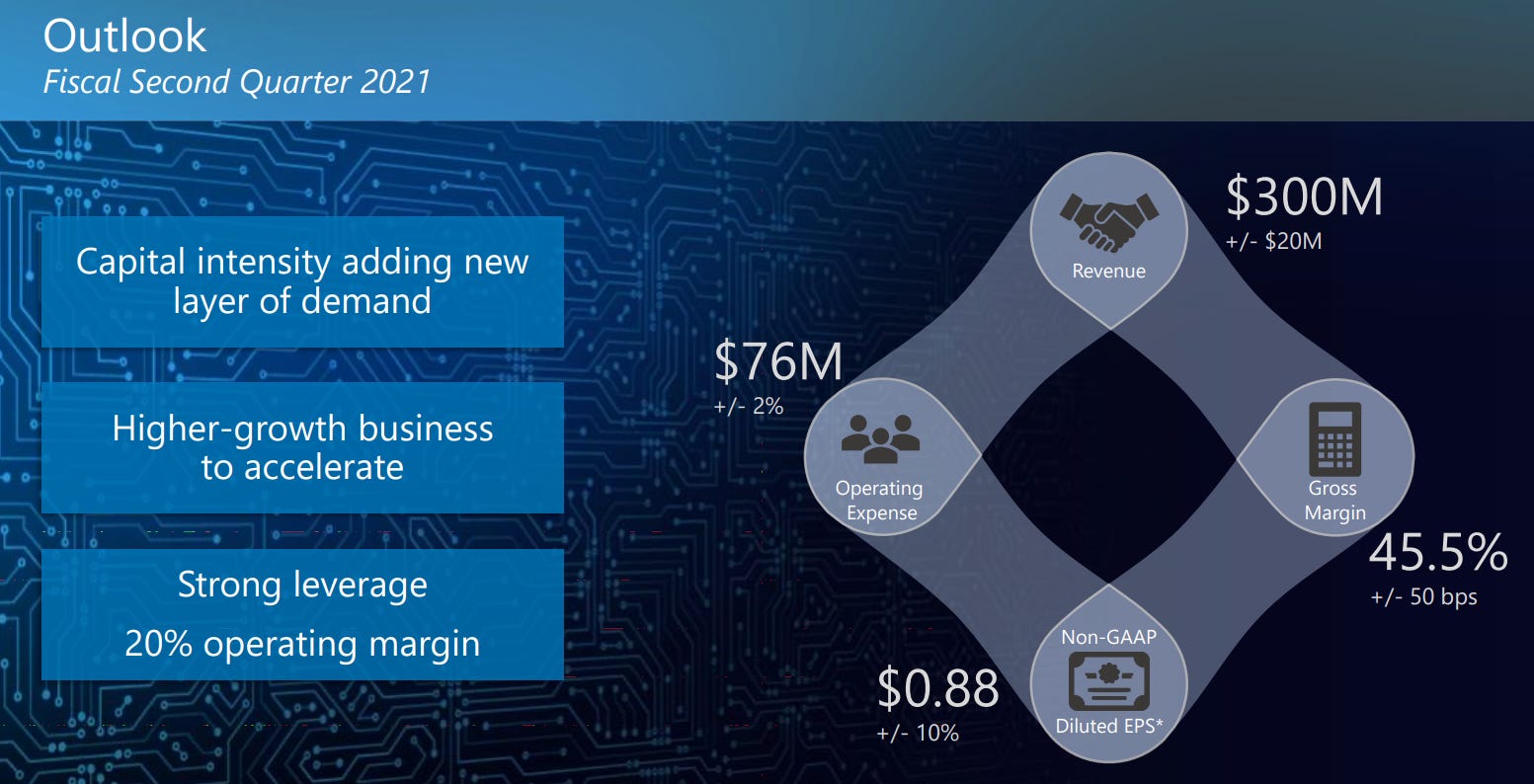

Guidance of EPS $0.88 +/- 10% ex-items vs consensus $0.59

Guidance of Revenue $300M +/- $20M vs consensus $239.5M

Frankly, the most obvious advanced packaging player was the right play - and it seems like this will persist for all of 2021

I know this seems insane - but I am chasing these results. They ended up being the advanced packaging play that actually wins (my mistake truly!) and while cyclical their new base of revenue should be sustainable. Just annualizing their 1Q puts them at 12x earnings - and yes I know this isn’t sustainable but chase this - they should not trade at this multiple.

For context, their average multiple is ~12x earnings - and they just accelerated revenue meaningfully and have more visibility than they have ever had before

I am firmly buying a 5% position on these results. I know it sounds drastic but when the facts change my mind changes - and these results are the best this company has ever seen. This is a bit of a trade and I will preface that.

Quotes from the Call

Broad-based demand for multi-die packaging

in the past 2 years, '19 and '20, because of semi downturn and underinvestment from customer and right now go another way, right? So we expect this year will be slightly higher than 6% to 6.5%. So number one is really the unit growth coming back.

The number two, I think, is very significant. I think we are seeing a different phenomenon. For example, the transition from 4G to 5G, we are seeing the demand for the multi-die package, big example is RF module. So this module actually typically have a 4 die to 40 dies. Actually, demand increased significantly due to transition to 5G. And not only [ that among -- ] or the multi-die package increase, the die is much more complicated. So the time to process this package also increased dramatically. So therefore, capital intensity increased, right?

So originally, I think we gave a guidance in normal year, our base should be around $750 million right? We take our 3-year's average, I think 2017 is normal year, '18 very strong year and '19 is a very bad year. So if you take the average, it's about $750 million . So this should be a representable number of our base in a normal good year. And we estimate this complex additional multi-die package actually increase our capital intensity, we estimate, another $100 million to base line, right?

Ball Bonders being here to stay and part of the SIP process

Okay. So Krish, let me put it this way: I think the estimate from the market this year is about a trillion die -- semiconductor die will be produced, roughly 1 trillion die. And the estimate of market shares of the ball bonder, I think about 65% of these die are processed by ball bonder, between 65% to 70%. So ball bonder is here to stay. And ball bonder also went through a lot of technology improvement, although we did not provide very detailed information. Actually, ball bonder, a lot of technology associated with that, right? For example, currently, all the segment, majority, actually is a user of the ball bonder and many, many days orders taking. And also, multi-die package I mentioned, including SiP and also including multi-die module, actually is a very complicated ball bonder process, right?

So to answer your question, I think this year, the revenue for ball bonder is very strong. Maybe it's a little bit strong than needed because of 2 year underinvestment. But we are quite optimistic. The ball bonder is here to stay. And the level actually the industry needed to support the overall industry growth, I think ball bonder will continue to grow.

This isn’t a 1H heavy story

So, Craig, the first quarter, I think, we delivered to $267.9 million, right, Lester? So the second quarter, I think we guided $300 million. so if you add this together, it's a little bit more than $550 million, I think $567 million, right? So we are looking at -- if you have a mirror image -- so Q2 -- the second half can be the mirror image over the first half. That means we expect Q4 probably will have a seasonality, as usual, but it's not going to be very significant, right? So if we model, Q1 is comparable to Q4 and Q2 and Q3 comparable, actually, we get about $1.1 billion. So does that help?

They have more visibility than ever - 40 weeks

So Dave, our visibility has extended. As you put in the backlog, customers are putting in PO at a tremendous rate, not just for the next quarter but for the remaining rest of the fiscal year, given the very tight demand for our product as well as for all products as well as lead time. Lead time now has gone up significantly. I would say it's almost up to about 40 weeks or so -- 30, 40 weeks. So I think we do have much better visibility, which is why I think we were comfortable in terms of giving guidance of $1.1 billion for the year.

It seems very easy to me that they could earn ~$3-3.5 or 12.5x-14x earnings this year. Now I know this growth isn’t sustainable but looking at consensus right now revenue for their FY is still slightly under by 2% and there is no way in hell the management team over-guided that would be like asking to get fired. It takes guts to put up a 75% revenue expectation for an FY - there is clearly going to be an upside from that. This is a shock and awe story.

FORM

Results

Customer Exposure (Intel)

FormFactor reports Q4 EPS $0.44 ex-items vs consensus $0.39

Revenue $197.0M vs consensus $184.0M

Guidance of EPS $0.34-0.42 ex-items vs consensus $0.36

Guidance of Revenue $176-188M vs consensus $176.6M

Non-GAAP gross margin 44-47% vs 43.4% in Q4

No strong feelings here. I would say that FORM has to put up this kind of beat to justify its premium valuation, especially right now. I know they are growing and expanding their customer base, but still given the price I would expect at least double-digit revenue growth.

Quotes from the Call

On VLSI and how fast the probe card market can and will grow

I think you've seen some of it already. If you look at the probe card market in 2020, it almost certainly grew faster. I mean, we'll find out in a couple of months when VLSI rolls up their survey. But almost certainly grew faster than the historical correlation to the semiconductor industry that we've observed. That also was the case in 2019. And so I think you're seeing the leading edge of some of these things. But each of the projects you talked about, still pretty early innings. If you look at those as a fraction of wafer starts for any of our customers, they're still relatively small. Having said that, they consume a good fraction of the test capacity because of the need for high test intensity and high test complexity to make sure you've got something close to known good die, as we talked about in various -- well, most recently, the Analyst Day we did last year.

So I think you're already seeing the leading edge of this. If you look at our results and the probe card market results over the past couple of years, obviously, as semiconductor industries continues to accelerate adoption of these I think various customers have made pretty firm comments that for 7-nanometer and 5-nanometer, they view advanced packaging with these various architectures as being a big part of their innovation road map I think you'll see that probe card intensity continue to increase.

QRVO

Qorvo was another sell the news event. Very strong revenue compared to actual and after SWKS surprise print, Qrovo rallied to reflect an expected beat.

Qorvo reports Q3 EPS $3.08 ex-items vs consensus $2.68

Revenue $1.09B vs consensus $1.07B

EPS $2.42 at the midpoint ex-items vs consensus $2.01

Revenue $1.025-1.055 vs consensus $944.9M

No real read-throughs here that I think you couldn’t get in QCOM/SWKS.

IFX (Infineon)

Infineon Market Share

Total Exposure by Segment

This might be new to you - but this is the EV waterfall of power content

Infineon Technologies reports Q1 EPS €0.19 vs consensus €0.16

Revenue €2.63B vs consensus €2.57B

Guidance of Revenue €10.8B (+/- 5%) vs consensus €10.69B

I can’t help but finish this feeling like NXPI is the better of the two in terms of valuation

Infineon is the most well known and credible company in the Automotive space, and they are really starting to swing into high gear

Quotes from the Call

On EV’s and expected growth in 2021

Sandeep, yes, the EV market is growing extremely strongly. In 2020 alone, it has grown 36% versus 2019. And people are expecting that to accelerate significantly into '21, so more like double actually, but strongly coming from plug-in hybrids but also from battery electric vehicles.

So we, in our case, are expecting something like a 40% growth in fiscal year '20 as compared to previous year coming from electric vehicles. So about, I'd say, 2/3 of the surplus growth that we at Infineon expect to the market value is driven by ADAS and EV again. So very strong momentum as expected.

On European legislation helping microcontrollers in Cars

We are in strong, I would say, a close discussion with the politics. There is a European scheme on supporting the digitization, which is also benefiting the microelectronics.

That had been a first scheme called important project of common European interest one where we are benefiting with in Villach, in Austria as well in Germany.

There, we are at the dispute on the next one where we see that further financing will come from the European Commission. The R&D are a part of that.

Regarding our manufacturing strategy, we will not return to deep submicron manufacturing because that is a large-scale business and we are much better off to cooperate with the foundries.

And of course, if there is an opportunity in Europe, we will be supporting this. Now very sorry. And please go on.

ONTO

Onto was very good and stood out quite a bit to me. The read-through to KLAC, CAMT, and NVMI is pretty strong and I think metrology is in for a very good year. Onto in particular seems like they will grow faster than WFE and trades at a below-average price. I really like Onto and I highlighted it during my packaging stocks write-up. Things are good for them, and they are really leveraging their scale to become more than the two companies that they merged into.

Results

Onto Innovation reports Q4 EPS $0.72 vs $0.60

Revenue $155.1M vs $150.5M

Guidance of EPS $0.62-0.76 vs $0.61

Guidance of Revenue $155-169M vs $154.5M

Onto was pretty strong, and it looks like now they will be growing faster than WFE and probably crushing synergy targets going forward. Additionally, the thing I liked that they talked about the most is how they are leveraging their large footprint to now get purchase agreements with their customers. This creates more visibility and more important a co-invested roadmap with their customers. This is how you “win” in semicap, and I’m frankly impressed. Onto is now one to watch and objectively cheap.

Quotes from the Call

Getting purchase agreements and total spending plans with customers, and thus integrating into their roadmaps. This is how you go from a B-Tier supplier into an A-Tier supplier.

So as we've grown, as we merged and brought together the 2 companies, both companies were serving these large IDMs, and we had back end a lot of strength from the Rudolph side from the back end, from the Nanometrics side, some front end. When our customers are looking at the total spend together, they're looking at putting together a more comprehensive plan, so giving us more visibility, letting us understand where their expansion plans are coming across both the front end and back end and making sure that we have the visibility to ramp along with them.

So the volume purchase agreements are meant to give that indication. In some cases, they're more formal than others. All of it is meant to define a year. So this isn't over multiple years. I think that was part of your question. It's all for this year. So it's an indication of what they see -- what they expect to spend this year across our products.

I think we would see this as we continue to grow our position and integrate more deeply into customers' road maps, I think this would be a more common occurrence.

On first half versus second half dynamics, and when the supply that is being added in the ecosystem will come online.

I think some of our customers in the front end will be more front end first half weighted, although when I look through the list, there was a mix and a number of them are balanced. So I think there'll be maybe a slight bias to the first half. But remember, half our business is volume-driven business, which really sees the pickup in the Q2 and Q3 time frame. So -- and in addition to that, we see the new products that we've announced and gotten acceptance on, we would expect more of impact from that revenue in the second half.

So all things considered, I would say that we would expect first half, second half to be relatively -- on the conservative basis, relatively the same for us. Even if there's a slight bias towards the first half spending from some of our customers, I think with the new products and the traction we're gaining in some other areas that we would offset that.

Wow a lot work here. Thank you.

Did you intend to put the MPWR analysis in this report? I see it in the header, but not the body of the report.