Earnings: Wolfspeed Analyst day, INTC, SITM, RMBS, QCOM, QRVO, ENTG, AMD, LSCC, CRUS, and More

You either miss and guide down, or beat and raise. Worlds apart in semiconductor land.

Housekeeping: Substack launched the new Meetings feature, essentially an ala-carte expert call. It’s a brand-spanking-new product, and if you want to make history as the first Substack meeting ever, schedule a meeting, and we can chat about semiconductors. Want to know more about Rambus, SiTime, or any of the names I’ve gone in-depth on? Grab a slot - let’s make history!

Anyways - it’s earnings season. Before I get even more behind, I will put out some quick takes. I first want to talk about Wolfspeed and their recent Investor day and then move to the rest of the update.

Wolfspeed Analyst Day and Earnings

The results were good, with a slight beat. Wolfspeed highlighted that demand continues to outpace supply, and as they ramp Mohawk valley, they now need a much bigger fab! Meet Siler City.

During the quarter, we also announced plans to construct the world's largest materials factory, Siler City, North Carolina, and we are also evaluating further expansion of our device capacity. The construction of this new North Carolina facility will require significant investment from our end. We believe that it's prudent at this time to increase our CapEx guidance from $550 million last quarter to approximately $1 billion for the fiscal year 2023 to reflect the increased investments and support the higher revenue growth we outlined on last quarter's earnings call.

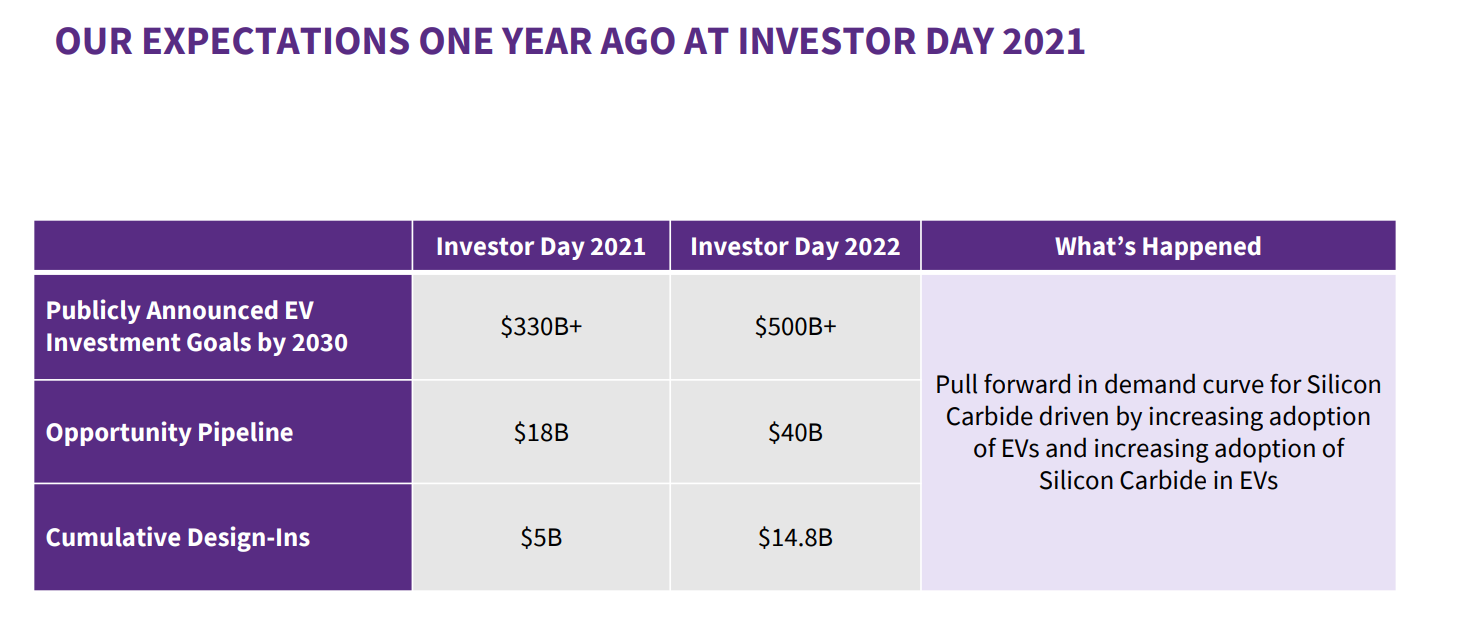

The reasoning for the even larger fab was laid out during investor day. Wolfspeed says SiC adoption has been much faster in the last year than expected. Demand has been pulled forward, meaning they will need another fab. Below is the change in the pipeline in just one year.

The problem for Wolfspeed the stock is that it ruins the FCF profile they originally highlighted in the past. Below is the 2021 Investor day and then the 2022 Investor day. Peak investment was supposed to be behind them, but now it’s looking like the FCF is kicked even further out, and there’s more capital needed to get there.

Now Wolfspeed is not FCF positive until 2026. Wolfspeed is a tomorrow story that worries me, given the current environment. It feels a bit tone-deaf, as every company is being punished for not being profitable, and Wolfspeed says, “we will be even more profitable… in the future.”

So now Wolfspeed has another huge tranche of funding they must raise, akin to 2-3 billion dollars of cash they will need. I truly believe this wouldn't be possible if Wolfspeed wasn’t such a great ESG bet. ESG mandates likely free up a cheaper cost of capital that would only be available to them, and if they weren’t as green as they are, this investment would be completely impossible. Wolfspeed also gave details on how they hope to raise the capital.

The goal here is to not be dilutive and to first pursue Government incentives (duh), then upfront payments from customers, then private or project financing, and lastly, public markets. Since the passage of the chips act, I believe the first bucket is larger, and the second bucket is likely as large as last year, but the stock went down, given investors think that they will be diluted. That makes sense to me.

I continue to like Wolfspeed’s pure play to one of the most secular trends in the market. I bought and then sold a bit of the dip during the initial sell-off, but now it’s becoming harder than ever to underwrite the story. Below is my simplified financial model from their IR day.

12x 2025 EBITDA? I guess that would have flown in the 2021 market, but with rising interest rates, Wolfspeed continues to be hard to underwrite despite its amazing long-term growth story.

I'll post about that behind the paywall for more earnings coverage, like Intel, AMD, Qualcomm, Rambus, SiTime, and others.