Finding the Sweet Spot: Nvidia's Goldilocks Quarter

Not too hot, not too cold: Nvidia is threading the needle with a clean result

Nvidia’s earnings are akin to my Super Bowl. There is no more significant event in semiconductors and AI, and each quarter, we tune into Nvidia’s results to see precisely what quarter we are in the AI hype cycle (and potentially bubble). There is no better signpost for the entire AI ecosystem than the company making the most of the revenue so far: Nvidia.

Anyways, let’s flip the results.

NVIDIA reports Q4 EPS $5.16 ex-items vs FactSet $4.59

Reports Q4:

Revenue $22.10B vs FactSet $20.40B

Q1 Guidance:

Revenue $24.0B +/- 2% vs FactSet $22.21B

Non-GAAP gross margin 77.0%, +/- 50bp vs consensus 75.5%

This was an almost perfect quarter. Nvidia came in with a revenue beat meaningfully ahead of consensus and right around buy-side bogeys. There was a surprising amount of negativity in the print and the belief that if Nvidia cracked, so would the market.

Well, I’m here to say that Nvidia saved capitalism (joking). Nvidia’s print was an extremely clean result that defied almost all critics, and shares are up 15% today. They beat revenue despite China being nearly zero in the quarter, expanded gross margins, and, importantly, said that they are supply-constrained and expect to remain that way for their new product coming next month. Let’s evaluate each statement.

Revenue grew meaningfully, driven by the continued outperformance of the Datacenter. The chart below puts the magnitude of the growth into perspective, but the actual numbers are staggering. Year-over-year growth is ~400% in the data center segment, growing 26% sequentially. They expect to grow again sequentially, implying ~21-22 billion of data center revenue next quarter. That’s almost at a run-rate of 100 billion for the year if they continue to post double-digit sequential revenue growth in just data center revenue.

The impressive part of this result is that this is happening even while China's revenue has effectively gone to 0 in the quarter. Mid single digits in revenue is de-minimus and a far cry from the previous 20 to 25 percent of revenue China used to contribute.

Shifting to our Data Center revenue by geography. Growth was strong across all regions except for China, where our Data Center revenue declined significantly following the U.S. government export control regulations imposed in October. Although we have not received licenses from the U.S. government to ship restricted products to China, we have started shipping alternatives that don't require a license for the China market. China represented a mid-single-digit percentage of our Data Center revenue in Q4, and we expect it to stay in a similar range in the first quarter.

For context, that means that while there was an approximately 3 billion dollar absolute dollar headwind quarter to quarter, Nvidia managed to shrug that off completely. We would discuss a 25 billion dollar quarter if China were not banned. That’s an incredible result and shows the strength and demand of hyperscalers. CPU cannibalization must be happening at an insane rate, and I am starting to doubt that data center CPUs will have a meaningful year of growth, given this mix shift.

Now, let’s talk about gross margins.

Nvidia just posted its highest quarterly GAAP gross margin ever and expects next quarter to be approximately the same. Now, I thought it interesting that throughout the rest of the fiscal year, they said that gross margins should subside.

Similar to Q4, Q1 gross margins are benefiting from favorable component costs. Beyond Q1, for the remainder of the year, we expect gross margins to return to the mid-70s percent range. GAAP and non-GAAP operating expenses are expected to be approximately $3.5 billion and $2.5 billion, respectively.

Now, there are multiple ways to look at this, but I think it is so interesting that they are comfortable sticking to the 75% gross margin despite the fact that, at some point, B100 will start to ramp in the latter half of the year. We should expect higher HBM costs and chipset costs, so this implies that they have either figured out a way to costs in a way we can’t understand or they will raise the price massively with the implication that performance should be much better than the H100. I think that the answer is the latter.

The power of this cannot be understated. B100 is almost here and will be announced at the GTC conference later this March. While pricing will be meaningfully higher than the H100, I can’t imagine a world where they increase prices 50% on 100% better performance. There’s a real chance that B100 has design choices that could shock us, and the pricing commentary leads me to believe B100 will be a hit. Time will tell.

Last but not least, I need to talk about the real takeaway for the call: supply constraints. It started with this comment in the prepared remarks.

We are delighted that supply of Hopper architecture products is improving. Demand for Hopper remains very strong. We expect our next generation products to be supply constrained as demand far exceeds supply.

Now, there’s some interesting context on this; as they said at the same time, the supply of H100 and H200 has been improving, yet they still expect B100 demand to far outstrip supply.

The first thing is overall, our supply is improving. Overall, our supply chain is just doing an incredible job for us.

Our InfiniBand business grew 5x year-over-year. The supply chain is really doing fantastic supporting us. And so overall, the supply is improving. We expect the demand will continue to be stronger than our supply provides, and through the year and we'll do our best. The cycle times are improving and we're going to continue to do our best.

Given that B100 should start to ramp in the second half, and demand outstrips supply, I think it’s hard to view this as anything less than favorable. If B100 demand is so strong out the gate, there’s a real chance that sequential revenue growth into the new product launch is possible, even as B100 improves effective capacity for the hyperscalers.

Also, if you noticed, InfiniBand revenue grew 5x year over year, even with Fabrinet missing results. I think that’s interesting because as fast as Nvidia’s GPU revenue has grown, the networking aspect is growing faster! Interconnect remains a bottleneck, which likely bodes well for Marvell and Arista. Interconnect has a chance to grow as fast as GPUs, but today, Nvidia has the InfiniBand ecosystem locked down. In the future, as products shift to ethernet, this could be an opportunity for other players not named Nvidia.

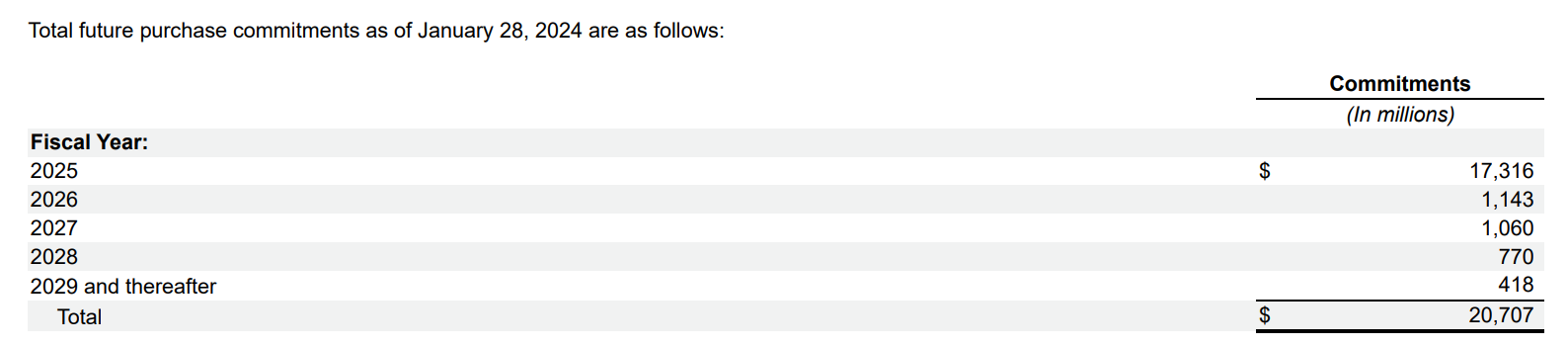

There was a little quibble on the call that I thought was interesting. One of the analysts pointed out that the absolute value of purchase commitments went down, but I believe if you opened up the 10-K, it’s mainly about the timing of the purchase commitments. The absolute dollar value of the fiscal year 2025 purchase commitments is up, and it’s up 54% quarter over quarter.

Compare the above fiscal 2024 commitments to the Q3 2024 commitments. 2025 has grown 54% quarter over quarter. That’s an impressive increase.

And if you compare it to the 2023 fiscal year commitments, it’s a 3x increase over the prospective amount Nvidia had for 2023. That might also be because they didn’t foresee revenue increasing that fast, but purchase agreements are massively bullish to me.

Anyways, wrapping it all up, Nvidia did have the Goldilocks quarter. They grew through the China headwind, are about to launch B100, and are crushing gross margins despite the headwinds of a new product launch. What’s more, they believe they are supply-constrained for the time being. It’s hard to beat expectations in the hottest stock on the planet, but somehow Jensen did it. This was an amazing quarter.

Now, I’ll turn to valuation and a bit more on thoughts about the upcoming B100 launch behind the paywall, including my estimates for FY25 / CY24 EPS and upcoming catalysts.

For free subscribers, I’ll talk to you soon during GTC, as I’ll be covering the event closely.