From Draw Down to Bounce Back: A Guide to the Q1 Inventory Bottom

Certain parts of the semiconductor industry look better positioned than others

Psst. If you want to listen to this episode via podcast, listen to it on Transistor Radio. You can listen to it on Spotify or the uploaded podcast in this email.

If you enjoyed the episode, please share it or subscribe. I talk more this round, as I went deep on the inventory cycle this time.

In my latest earnings overview post - I noted that the Q1 bottom and incremental Chinese demand the critical question for investors this cycle. I have watched a meaningful divergence between some companies, with Microchip guided to sequential revenue while NXPI guided to meaningful QoQ declines.

Some companies even provided the target days of inventory by the end of the quarter, so what follows is a very detailed analysis and attempt at figuring out where the bottom is and what sell-through is looking like versus sell-in at this point. From that starting point, let’s talk about a semiconductor inventory cycle and then dive into where we are in this cycle.

The Difference Between Sell-in and Sell Through

The terms "sell in" and "sell through" refer to different stages in the distribution channel of semiconductor inventory. "Sell in" represents when the manufacturer sells the product to the distributor or retailer, while "sell through" refers to the point at which the end consumer purchases the product.

In other words, "sell in" is the initial sale to the channel partner, while "sell through" represents the final sale to the end user. Understanding these two terms' differences is critical for semiconductor companies to manage their inventory levels effectively. It helps them evaluate their distribution channels' performance and identify potential issues such as overstocking or understocking.

A high "sell-in" volume without a corresponding "sell-through" could signal a problem with the product's marketability. In contrast, a low "sell-in" volume with a high "sell-through" could suggest a supply chain bottleneck that needs to be addressed.

Right now, we are in the cycle of high stocks at the distributors and retailers, so semiconductor companies are pulling back sales to the channel to focus on clearing the inventory and thus stopping further pricing pressure.

The lagged response to demand, creating an over-inventory effect, is often called the bullwhip effect. The bullwhip effect is a phenomenon that occurs in supply chain management when small changes in customer demand at the retail level lead to progressively more significant changes in demand at the distributor, wholesaler, and manufacturer levels of the supply chain.

The bullwhip effect is often caused by communication and coordination problems between different levels of the supply chain, which lead to overreaction and overcorrection to changes in demand. Some factors contributing to the bullwhip effect include delayed and distorted information, order batching price fluctuations, and gaming behaviors. A good graphic shows how a slight variance in customers can lead to significant supplier changes.

The 2020 semiconductor shortage made the bullwhip effect go nuts. Distributors and OEMs have been asking for more and more inventory, but as macroeconomics has weakened, so have demand signals. And so the desperate need for more inventory has turned into too much inventory. Customers are not buying now.

During the shortage, end demand was high, and every aspect of the supply chain was trying to replenish depleted inventory. So besides having to sell into strong demand, the industry was trying to replenish the channel.

Now that demand has weakened, the channel is entirely full, and every company is trying to reduce its stuffed channels. This is how a small demand change can lead to massive over-inventory effects.

This is where we are now. We are at the clear peak of the inventory cycle, and many companies have been expecting that Q4 and Q1 would be quarters where semiconductor companies shipped less to deplete the channel. I wrote a little bit about this when I examined inventory bottoms.

So that’s the cycle. We are clearly at a glut in inventory. Does this get worse forever, or is there an end in sight? I walk through some of the company’s commentary that was recently reported to see if we can look at some patterns and then see what parts of the industry look better and worse position.

Comments on Inventory

First, I want to start with a smattering of company inventory comments. I will then piece together what that looks like at a higher level.

Analog Devices

We ended the quarter with approximately $1.7 billion of cash and a net leverage ratio below 1. Days of inventory increased to 155 while channel inventory remains below our target level. Recall that last quarter, we outlined our strategy to rebuild strategic die bank and hold more finished goods inventory on our balance sheet as we moderate shipment into the channel during this time of inflection.

Renesas

On the right-hand side, the company total DOI declined Q-on-Q. And it is 98 days. Looking at each segment, for both of the segments, DOI declined. As of the end of fourth quarter, the yen strengthened, so that was a positive element. And excluding FX impact, it was Q-o-Q increase to 111 days. This is sales channel inventory in WOI. And the WOI Q-on-Q declined and both -- in both segments, it is 7 weeks or so. This is inventory analysis and the outlook. From in-house inventory to the left, from third quarter to fourth quarter, the actual amount declined and that was due to FX impact.

FX helped the decrease in days inventory outstanding, which is a weird dynamic for the ex-US companies. It looks like they are planning to build inventory. This bodes well for Renesas and is why their shares are up so much.

As I have said, as of the end of fourth quarter, DOI was 98 days, out of which die banks are actual for in-house and foundry combined, 18 days. The target is 22 days to 23 days. So, we needed to build up some more. Out of 18 days, roughly 4 days is the in-house production part. Legacy product category, we completed almost entirely the expansion for die bank, but we still need to expand the inventory level of die bank for our growth products. Therefore, finished goods in fourth quarter, mostly for automotive application, we shipped the production done in the previous quarter.

On the other hand, in the industry infrastructure and IoT, we suppressed the shipment to the sales channel by looking at the demand. So it is flat. In the first quarter and onwards, according to the demand, we will conduct shipment. So the inventory level of finished goods Q-on-Q will likely be flat

Monolithic Power

And as you can see on the webinar video, days of inventory rose to 212 days at the end of Q4 2022 from the 167 days at the end of the third quarter of 2022. Historically, we have calculated days of inventory on hand as a function of the current quarter revenue. We believe comparing current inventory levels with the following quarters revenue provides a better economic match. On this basis, again, you can see days of inventory increased to 214 days at the end of the fourth quarter of 2022 from 188 days at the end of the third quarter of 2022. I would now like to turn to our Q1 2023 outlook.

On Semiconductor

Accounts receivable of $842 million declined by $15 million and DSO of 37 days increased by 1 day. Inventory increased by $41 million sequentially and days of inventory increased by 7 days to 136 days. This includes approximately 26 days of bridge inventory to support fab transition and the impending silicon carbide ramp.

We continue to proactively manage distribution inventory decrease in inventory in the channel by $10 million sequentially and at historically low levels with weeks of inventory at 7.3 weeks compared to 6.9 weeks in Q3. Total debt was $3.2 billion and net leverage is approaching 0.

Mediatek

It's a long question. I think, our understanding and maybe our observation is that the smartphone inventory, including our customers and channels in China probably at about 3-3.5 months level. We believe it will go down to probably 2 to 2.5 months this quarter. I think that's what we are expecting to see. I think Chinese New Year time -- during the Chinese New Year time, the sellout in China as far as we understand, it's better fairly good, but definitely better than our customers' expectation.

As to the outside of China inventory, what I can say, I don't have specific numbers. What I can say is some of our customers had a little better fourth quarter business than they expected. So I expect -- but they still have inventory at hand, so they're burning their inventory probably at a faster clip than expected. Our own inventory days is still high. However, the inventory of quotas, the inventory volumes continues to go down quite substantially. We have really carefully managed our wafer start for our business.

China Inventory coming down next quarter is good and means that the cycle will probably be over sooner than we expected.

Cirrus Logic

Inventory was $152.4 million, down from $164.6 million sequentially, and days of inventory was 47 days in Q3, down 8 days sequentially as we shipped product to support our customers' new product ramps. Looking ahead to Q4 fiscal '23, we expect inventory to increase from the prior quarter as we fulfill ongoing demand and manage inventory ahead of product ramps later in the calendar year.

This one was odd, but given their VR headset and synaptic business, it seems that they are either channel blind or this is the inventory impact of the new AR headset from Apple. I believe that CRUS seems to be the clear “winner” of the upcoming headset.

Microchip

Our inventory balance at December 31, 2022, was $1.165 billion. We had 152 days of inventory at the end of the December quarter, which was up 13 days from the prior quarter's level. We have increased our raw materials inventory to help protect our internal manufacturing supply lines. We are carrying higher work in progress to help maximize the utilization of constrained equipment as well as to position ourselves to take advantage of new equipment installations, which should relieve bottlenecks.

So we specifically guided in our release today for inventory days ending March to be between 157 and 164 days. Beyond that, we really haven't given any color, but we'll continue to manage our manufacturing operations and our purchases from our suppliers to be in the right spot to support our customers.

Inventory will slightly sequentially increase, but an increase of ~5-12 days, compared to 13 days last quarter.

Silicon Labs

The absolute amount of channel inventory declined in Q4, and we held GSI flat at 59 days versus Q3, which is an excellent outcome.

Their actual inventory increased, but their channel inventory is decreasing—a good bill of health for Silicon Labs.

NXPI

Turning to working capital metrics. Days of inventory was 116 days, an increase of 17 days sequentially and distribution channel inventory was 1.6 months. As we mentioned on our last quarter's call, given the uncertain demand environment, we made the intentional choice to limit the months of inventory in the channel, while keeping inventory on our balance sheet to enable greater flexibility to redirect product as needed. Furthermore, given our manufacturing cycle times, combined with the uncertain demand environment in the first half of 2023, we will continue with this approach in Q1, and we expect DIO to increase in the quarter

Ross. Yes, you are correct in a way that when we look at inventory, we look at both the internal and the channel together. So as you can imagine, right, the channel inventory today at 1.6 months, basically, we can move that up by about another 25 days if we wanted to, to our target of 2.5 months of sale.

Their channel inventory is starting to look very lean. Inventory on hand is increasing, but 2.5 months of channel inventory is their target. The Chinese recovery particularly impacts them, so I think their channel will respond well when the reopening happens. I think NXPI is in a good place with inventory days and channels.

Micron

It's really a function of how the market is recovering, but we expect days to peak in second quarter. So we were at 214 in the second quarter. So we'll be above that. And then we expect to remain at elevated levels, but down in days in the third quarter and then down days in the fourth quarter, closer to 150 obviously we are today.

Micron is among the worst for Inventory, with the third largest quarter-over-quarter increase behind SiTime and Nvidia. But their preliminary belief that inventory will peak in Q2 is healthy. But they will likely tag an all-time high for inventory days at Micron. It’s going to get better, but it’s terrible.

Broadcom

Days sales outstanding were 30 days in the fourth quarter compared to 29 days in the third quarter. We ended the fourth quarter with inventory of $1.9 billion, up 5% from the end of the prior quarter because we expect the mix of revenue in Q1 to have a higher cost of materials. We ended the fourth quarter with $12.4 billion of cash and $39.5 billion of gross debt, of which $440 million is short term.

Broadcom is astounding. Their actual inventory was only up 5% from the prior quarter, and they had days of inventory flat QoQ. I think Broadcom gets the cleanest bill of health for an inventory of the semiconductor companies.

Wrapping it all up

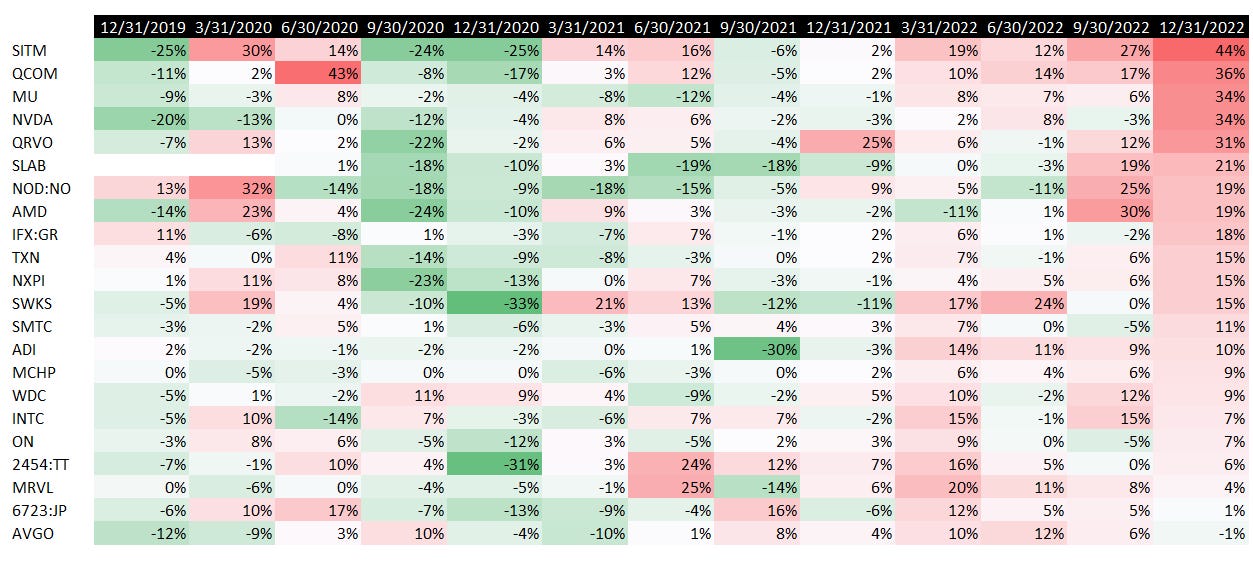

I think where we are at the semiconductor cycle is at the absolute peak of inventory, with a clear view into cleaner channels in the coming quarters. The fact that SLAB, AVGO, and Renesas lowered inventory leads me to believe it’s not as bad as feared.

Here’s a graphic of QoQ inventory day increases. I think it’s interesting how you can visualize the cycle, as you see the clear inventory drawdown in 3Q 2020 and the continued lack of inventory build. Then the rapid inventory builds in 3Q 2022. We are in the midst of the depths of the inventory cycle.

I will take a moment to call out my friend and peer, Dylan Patel, at SemiAnalysis . He wrote this piece about semiconductor inventory, and I think he’s wrong.

Pointing to inventory being above historical averages and this being a historically strong inventory cycle is akin to looking in the rearview mirror and driving. Meanwhile, companies are guiding to decelerating inventory day increases, historically associated with the quarter before an inventory correction is over. That jives with history, giving me faith that Q1 will be the bottom for most companies ex-Memory.

If you look at history - cycles usually last 2-3 quarters of increasing inventory, and swiftly recover. We are well into our second quarter of inventory correction, and a Q3 recovery would be a historic 4+ quarter adjustment. I don’t think that will happen - and looking at a very simple analysis of inventory days’ rate of change shows that we are much closer to the end than the beginning for most companies.

For more analysis, which companies are best positioned, and a full data sheet of DOI and Inventory from history, refer to the rest of my piece behind a paywall.