Inphi Follow-up: The Game's On

The exciting second paid post of this substack!

Wow. What an exciting second piece. It’s hard to imagine that my piece I posted publically last Friday would have a follow-up discussing a buyout with a premium the very next week. It is as @MinionCapital’s tweet mentioned, my single largest position.

The feeling is bittersweet. If you read the piece, Inphi is so attractive not because of a quick price bump, but because it had a chance to grow into a sizeable strategic market with an incredible management team and growth opportunity. I wanted to be invested alongside Ford Tamer as he continued to make intelligent deals, attack adjacent markets, and become a much larger company pursuing data center interconnect. That ship might be sailing. But I don’t think it’s for certain. Let’s discuss.

The Deal Rationale

At first it seemed to just be a rumor, but this morning the press releases confirm that the deal is real. Let’s first look at the deal slides.

It’s approximately 56% stock / 44% cash and they expect ~$125 million in run-rate synergies. On a ~2.7 billion dollar combined total OPEX + CoGs basis (last quarter annualized), this is just 5% of costs. I think this is conservative, and if they are ripping out costs for both companies, they are likely doing it wrong. My guess is most of the synergies are going to be driven by CoGs scaling at foundries, some overhead costs, and pooling resources to push lower geometry.

Let’s move onto rationale - which at first blush looks really compelling.

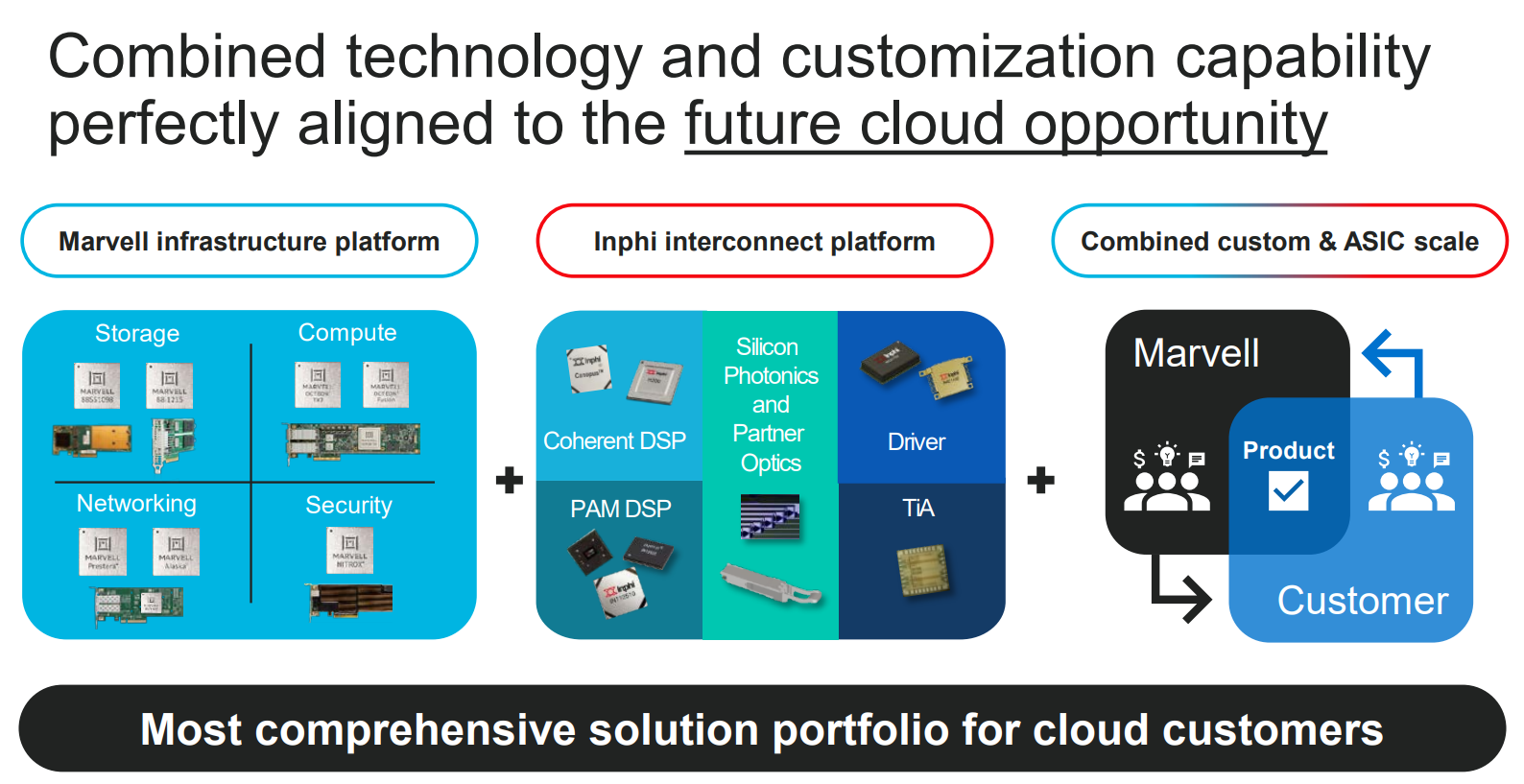

This slide while pretty basic - explains the rationale in a decent way. Inside the data center, Marvell has a large portfolio of compute, storage, and networking, and Inphi is usually how each of those products is connected together. Next, let’s turn to growth and TAM slides.

That previous TAM I talked about in red was essentially the crux of the Inphi long pitch. It’s going to be growing fast, and it’s going to be growing for a while. Inphi clearly is growth accretive, but I do think the combined enterprise has a really interesting go to market and cross over and rationale.

This slide highlights their IP. On Inphi’s side, it’s mostly their best in class DSP + TiA that makes them stand out. On Marvell’s side, it’s their networking, serDes, and NiC businesses that stand out. Now it’s likely that Marvell + Inphi has products that likely address or touch every segment of the datacenter. From custom ARM servers to networking ASICs, to transceiver DSPs. It’s end to end.

Additionally, the second graph is pretty illuminating for anyone who follows semis closely. Tape-outs for 5nm and onwards are just going to get harder, and the scale does matter. This is a core principle in all semiconductors, and I’m going to highlight this not with a quote from the current companies, but from a deal that just recently got announced, AMD and Xilinx. Here’s Lisa Su.

So the majority of those cost savings are really on just the scale of bringing the 2 companies together, so if you think about our opportunities on the COGS side as well as some of the public company functions and those kinds of things

COGs is an interesting call out because both Xilinx and AMD are fabless, and so are Inphi and Marvell. The key here is 1) new nodes are really hard and expensive so scale matters and 2) grabbing your share of fab space at TSMC/Samsung is partially dependent on scale.

Portfolio Overlap

This is where it gets really interesting. Let’s just look at their 5G network base station. Notice the amount of compute units in basebands or central units, but Inphi’s portfolio will interconnect each piece.

Additionally, in the cloud segment, there are a lot of complimentary products that Marvell can offer to customers. Not the storage controllers you traditionally associate Marvell with, but rather DPUs, networking switches, and NICs. From where Marvell’s portfolio ends, Inphi’s begins, and then vice versa.

The customer overlap is great too. Microsoft for example has Thunderx2 servers in Azure and is the largest customer for Inphi. But there are also negative overlaps, such as Marvell’s significant Cisco customer. Acacia - Inphi’s largest competitor in many markets - just got bought by Cisco and would be unlikely to use Inphi’s DSP over Acacia’s. However, for anyone else other than Cisco, it’s likely that Marvell + Inphi combined can likely become a one-stop-shop, with meaningful customer wins with large businesses with Marvell. If this sounds familiar, this sounds a lot like the Broadcom portfolio across networking. But instead of leading with Broadcom’s Jericho / Tomahawk portfolio, but with Inphi’s transceiver DSPs. I am surprisingly bullish by the platform that could come from this. They should be able to offer merchant silicon solutions to anyone who's looking for it, and importantly it won’t be Broadcom. I’m excited to see what comes of it.

Simple Takeaways

This is the skim part - this hopefully makes it all easier.

As for what I’m doing - I want to stay on for the Marvell and Inphi combined company. It’s an interesting idea, and the revenue synergies alone can make this deal work. There is a lot of upside here from a strategic perspective. I’ll likely sell some down for portfolio weighting reasons, but other than that I think it’s great.

Also, the deal premium as of this morning is confusing to me. At a share price of ~$36 - Inphi’s take out value is ~$149. It’s trading at $132 currently or a 12% gap.

The Good

Scale - semiconductors are a fixed cost scale business. Marvell + Inphi together can stay at the leading edge geometry with less burden. They have the same fabrication partners as well and have common suppliers. Clearly, the rationale is good there.

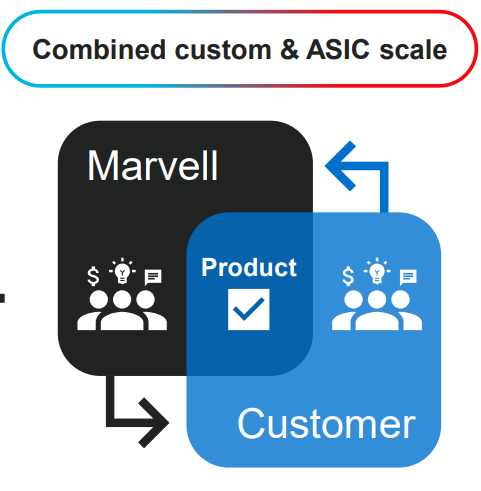

Similar Business Model - Inphi and Marvell both do intense scale projects, that are often for a single customer and often the cost is for millions of dollars. Having a single company to go to pursue these large ASIC and custom products is likely a good idea.

They are the best serDes team in existence currently. This really matters and is a very subtle. SerDes is going to increasingly become an important part of all interconnect strategies. I have long looked at Marvell’s product, and together it’s clear they are a leader here.

No revenue synergies mentioned - and the revenue synergy opportunities are obvious. They said they wouldn’t model or talk about the potential revenue synergies, but Ford Tamer had a great example of why revenue synergies are possible. Inphi in the past has actually bid on some of the ASICs that Marvell has, but got turned away based on their size. Customers want a mature partner that they can bet on, and now Marvell and Inphi is the largest partner that can bring these products to market.

Antitrust is not a concern - very little direct revenue overlap. They have products that sit next to each other in the datacenter, but not quite

The Bad / Questionable

Customer concentration could swing negative. Cisco for example at Marvell is going to be awkward. Cisco is going merchant silicon, and that is important, but Acacia is Inphi’s mortal enemy.

Culture - Part of my obsession with Inphi is their culture. Go read the glassdoor reviews and its very jarring. I know there is positive bias, but the summary is “We are disrupting the world, and getting paid to do so. The only downside is the work/life balance, because of the speed we execute.” This is dilutive to the culture and execution they’ve done so far.

Growth Dilutive to Inphi Shareholders - I am kind of weirdly disappointed here. Something I think about a lot and noticed in the first write up, was that Inphi has been investing like mad for years, and finally they are starting to reap the benefit of their growth. The incremental operating margins should be really impressive from here.

The Financials and Some Proforma’s

This is their financial summary slide.

This is a pretty aggressive target model, but also note that this is last quarter annualized and this is likely a bit ahead of themselves.

I started making something super in-depth and then I realized there really is no need. It’s slightly accretive in FY22 (assuming the deal closes in FY21). I’m pretty excited for Marvell to issue debt. Inphi has a large amount of convertible debt, and that so far has been one of the most expensive financing sources ever.

I could run you through the interest expense schedule but I think it really isn’t worth it. Inphi has expensive debt, trades more, and should grow faster. Together it’s going to move the numbers in the out years. Additionally, Inphi should ramp back to its 70% gross margin by FY22 as well.

The financial logic here is pretty lackluster, but if you believe there are revenue synergies it’s a home run. The evidence seems kind of compelling to me for two reasons.

First - some great quotes on the call.

And they think about these choices in the same way to think about their GPU, their AI, how they think about supporting their applications for their future user growth and the optical connectivity is a key part of it. And so the what's changed a lot in the optical business, and then I'll let Ford take the second piece, from what I was involved with it in my prior company was in the past, optical is really selling the module vendors who then sold into a variety of applications. With the advent of the cloud and the need for very significant customization and going deep technically, the cloud OEMs have really become the customers that define the requirements. And of course, you need to work with the whole ecosystem as well to make it happen, but that's created a unique change, which allows, I think, a lot more value to be delivered and to be a bigger part of the solution. Ford, maybe you want to comment on some of the product synergies and some of the other things we've discussed.

You'll see what's first generation called onboard optics and then eventually co-packaged optics and with a combination of Marvell switching and Inphi optics, we'll be able to get closer to customers around that first level of integration. Second, on the processing side, if you look at the optics to the endpoints, being a processor, being a net card, being a special ASIC that customers are doing for acceleration. That's going to be another area of synergy where, again, bringing the Marvell nick the Marvell processor, the Marvell ASIC next to our optics would make a lot of sense. Customers are redreaming storage. So memory disaggregation is happening in a big way to get these data center storage more efficient. And again, we'll be able to be together dreaming up how we could enable better memory disaggregation with our interconnects. And then finally, as you look at Slide #15, from that's presentation, you can see there are opportunities for custom offering in on our own, have bid on these sort of custom devices. However, we didn't have the scale and we didn't have the whole infrastructure needed. To go after these billions of devices -- billions of gate devices, very complex. The cloud customers would like a larger company to do this. And the 2 companies combined together with able to bid after these ASIC opportunities or customer opportunities. So together, I think we see a tremendous amount of revenue synergy over the next few years in the cloud, number one. Number two, as you go into 5G, Inphi has been focused on only mid-haul and backhaul, and we're doing very well in those markets. We haven't gone after front haul just because we didn't have the bandwidth or the presence, but with Marvell leadership in front haul, we'll be able to, again, expand our markets and grow our revenue together in the front has opportunity #2. And number 3, that's a bit more long-term as you go to automotive. And you look at things like LIDAR, as an example, that with combined silicon photonics was better coherent type of receiver to increase the reach of these units. This a very large opportunity for us to go and grow our markets together. So I think you're going to see over the next few years, tremendous revenue synergies between us. We've been growing our company, a 30% CAGR for the past few years and really look forward to combining with another high-growth company like Marvell and growing this together and finding plenty of revenue synergies.

Second the past conversation about during the Cavium acquisition - they managed to win a lot more business with Samsung in particular by approaching them with a much more aggressive slew of products.

4G is really where the breakthrough came, which is Cavium was and still is, combined with Marvell, the only, call it, merchant baseband supplier for base stations, right? And that's where we were able to break into Samsung, supplying them their 4G baseband. And the content went up from, call it, $200, almost 3.5x, right? Call it in the high $700, $800 range, essentially.

And that's where you saw, in fact, if you were tracking Cavium, you saw a pretty meaningful shift upwards in their revenue trajectory. It's been a very successful rollout in 4G. The world's most populous country, India, basically uses -- essentially the biggest network is run by Reliance. It's called the Jio network. It's all run on Samsung base stations, which is all running essentially on our silicon, right? So the world's most populous country, most of the traffic, which goes on a 4G network runs on Cavium-based silicon.

-Ashish Saran, Marvell Technology Group - Citi Global TMT 2020

Concluding Thoughts

But I want to wrap up that the irony is not lost on me that Inphi’s actual quarter results were pretty disappointing in my books. Essentially in-line with consensus. If it was not for the merger announcement, I believe the stock would have acted negatively.

I still don’t think it really matters from the long term perspective of the company. They have a huge growth opportunity ahead of them and they flexed meaningful operating leverage this quarter.

But anyway, I think that ship has sailed. Marvell looks like a really solid deal from a financial perspective, and while the upside is probably more capped than Inphi standalone, I believe so too is the downside.

Also interesting to note is if someone wants to interlope. The deal spread is still wide, and I think the likes of Intel or Broadcom would still be a happy buyer of this company.