Intel 18A is in Sight, Does it Matter?

Intel is now in the valley again. Also thoughts on AMD and LSCC and FPGAs.

Intel reported earnings last week. Intel was one of my favorite stocks last year, and I wrote about it here in “Is This the Intel Inflection” (it’s a free post now!), where I successfully called the bottom in the stock. It’s worked pretty well, even against the SOXX index since then.

I’ll summarize my thesis back then, update you now on what I think about Intel, and write about results and read-throughs.

My thesis back then was simple. Intel had hit a cyclical bottom, and EPS guides were low enough to expect big beats into 2024. The market would eventually look out for their 18A inflection as they successfully pulled off the five nodes in four years of process transformation. Meanwhile, AI was a bit of a kicker, and there narratively was a path for the stock forward instead of floundering in a world of hurt and no future.

Remember, Intel was burning cash and paying dividends, and the market feared its prospects.

I think that’s not true anymore, and the market has been rightfully looking out to the 18A inflection and sees hope. Intel, then, had no narrative nor anything to look forward to. Intel has a future, but now the numbers don’t make sense. EPS beats should moderate, and it’s time to acknowledge the CPU business.

Intel’s Valley

I think it’s safe to say that 18A is real. They haven’t done any delays, and everyone I have talked to is excited and hopeful that we not only have another leading-edge process in the West but probably the best HPC-suited process in terms of PPA because of Intel’s crucial Backside Power bet.

I believe it’s valuable, but the problem is I don’t believe it’s quantifiable how valuable it is. Is it worth 10s of billions in strategic value? Probably. Can I ascertain the value of revenue, profit, and cash flow? Probably not for some time. And that’s the rub because the market will now be accessing the value of its current business, and it isn’t good. Especially design.

The only way I can get to Intel being valuable is a very intense sum-of-the-parts (SOTP) thesis, and that’s fine, but SOTP theses have a very mixed track record. I think it’s time to be less positive about Intel’s stock.

I believe there are likely about ~20-30 dollars per share in MBLY and PSG, with a kicker for IFS. The problem is the CCPU business. Intel has to face that they are a legacy x86 CPU maker, and it’s time to deal with that reality instead of hoping for 18A.

The hope is here, but it’s time to value the reality of CPUs. I think it will be multiple years before Intel can help IFS become a $10 billion-a-year business, and in that time, CPUs will be more challenged than ever. 18A will stem market share losses (in CPU), but the market will be much smaller anyway. The handoff from CPUs to IFS is still a few years away, and now it’s hard to value IFS’s results as much more than a strategic put.

Put differently, buy the rumor of 18A and then sell the news. That’s today.

x86 CPUs Look Horrible

Let’s face it, Intel’s core business sucks and will suck for a long time. As AI computing takes share in everything and hyperscalers make ARM-based CPUs, Intel’s role in the semiconductor industry has gone from the center to the side. Intel is just not as relevant anymore.

Nvidia is now adopting a tick-tock product cadence that Intel famously adopted when its CPUs ruled the world. The reality is there isn’t a need for Intel to make CPUs that much faster, and CPUs will be losing share to accelerated computing for the foreseeable future.

And maybe that could be an Intel that investors could understand and handicap if they controlled their market, but the problem is the competition is fierce and not in their favor. Even within x86 CPUs, AMD continues to out-execute Intel. I think that the design team at Intel has clearly slipped, and if AMD and Intel’s teams were to compete head to head on the same process, AMD would come out ahead. Intel’s only shot to gain share is process.

That’s bleak, and I’m not mentioning ARM CPUs gaining a share. Intel is retrenching its core market harder than ever. And this time, they are coping with a bit of a story: the AI PC.

AI PC Hopium

I think hope springs eternal, and the most recent rendition of this for Intel is AI PC. Intel continues to dominate PC despite its declining relevance in the big picture of semiconductors. Now that AI has become a larger part of the pie of computing, there is a belief that PCs need to change to adapt to future workloads. That could be a potential ASP lift in a declining market.

I think AI PCs will be successful, but just not in the way you’d expect. The reality is that the best AI PC today is similar to a gaming PC, with a solid CPU and a great GPU. That isn’t Intel’s opportunity.

But what will happen is that I think in a weird claim to improve AI performance, Intel will try to add HBM to their CPU and increase memory in the name of AI performance. This will make a better user experience and cost a lot more. The entire PC OEM supply chain will jump on this opportunity because a relatively fixed gross margin on higher dollars is more money. The entire ecosystem can make more money, even on a sub-optimal solution. There are many examples of pushing suboptimal solutions so everyone in the ecosystem can make more money (thinking of you, FWA1).

So I think this time next year, laptop and PC OEMs will offer “AI PCs” that are “AI Ready.” This will be nonsense marketing hype, and while consumers won’t need it, HBM will feel like a much faster experience.

But let’s be real. The best AI PC is just an even more expensive GPU attached to a CPU—similar to most gaming PCs and state-of-the-art AI servers today.

Anyways, on to results at Intel.

Earnings Results

Intel reports Q4 EPS $0.54 ex-items vs FactSet $0.45

Reports Q4:

Revenue $15.41B vs FactSet $15.16B

Intel had a meaningfully above guidance quarter, driven by strong gross margin fall through and Client rebounding. The problem was the guide:

Q1 Guidance:

EPS $0.13 ex-items vs FactSet $0.34

Revenue $12.2-13.2B vs FactSet $14.24B

Being 2 billion short is quite the miss for guidance, and it’s hard to explain what happened. Intel has some scapegoats, but it does seem that the channel inventory is filling now, and now is the time to remind investors that the actual end demand isn’t so great.

First, the Client segment rebound continues, and the sell-through of reserved inventory moved the operating margin meaningfully positive while growing revenue meaningfully. This means that we are through the cycle in PCs. Turning to data center and AI.

Intel might be the only company worldwide with a declining AI segment. Most of this revenue is server CPUs that AMD is crushing them with their much more competitive product. Intel doesn’t have much of an AI solution, but their pipeline (note, not revenue) of Gaudi is growing to “over 2 billion”. This pales in comparison to AMD’s multi-billion and Nvidia’s 10s of billions of revenue.

Our accelerated pipeline for 2024 grew double digits sequentially in Q4 and is now well above $2 billion and growing. We recently increased our supply for both Gaudi2 and Gaudi3 to support the growing customer demand and we expect meaningful revenue acceleration throughout the year.

They acknowledged that the CPU in the data center is getting cannibalized by AI but expressed optimism it would improve throughout the year. This seems reasonable given the commentary of increasing capex spend ex-AI.

Networking and Edge is the final group in this equation, and while not a perfect comparison, I believe this is what has most of the PSG and FPGA business. Results are bad, and now NEX is in the negative operating margins territory.

They believe that markets will remain weak for the rest of the year. They do believe the bottom is in Q1.

Within NEX, telco markets are likely to remain weak through the year, though we expect solid growth from our network, NIC and edge products. These signals give us confidence that consolidated revenue will grow beyond typical seasonality after a soft Q1. And that we can deliver sequential and year-over-year growth in both revenue and EPS each quarter of 2024.

Note that they believe it will just be in Q1. Mobileye will probably be the trough quarter, but I’m doubtful about the network. The conclusion is that FPGA is pretty bad.

While we expect a slightly subseasonal first quarter from our core product businesses, we see material inventory corrections in Mobileye and PSG.

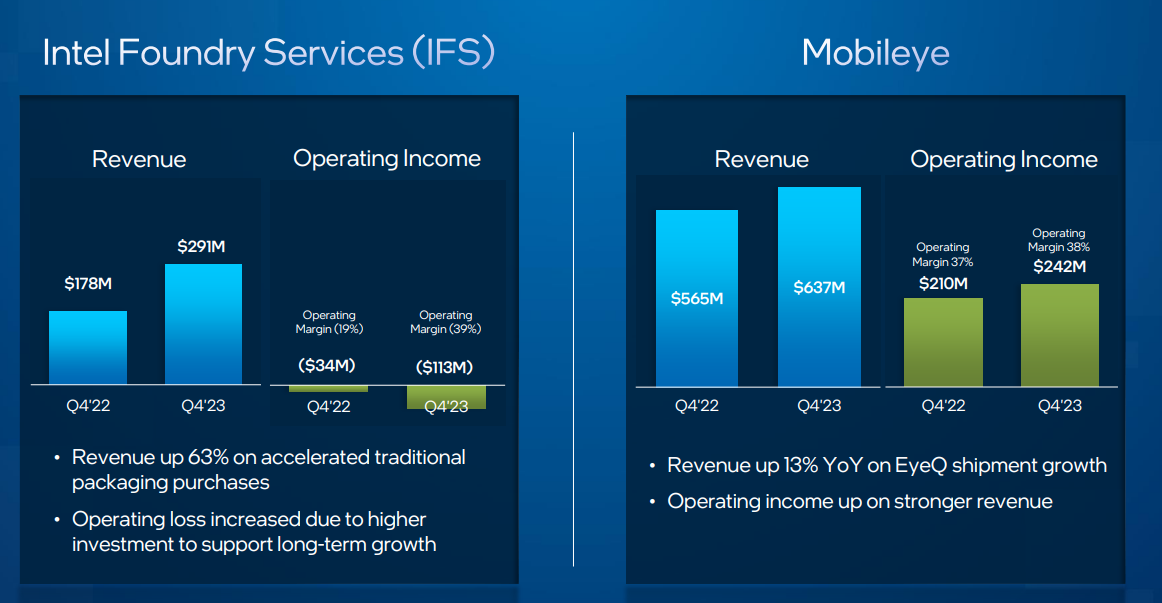

Last but not least is IFS. IFS announced new customers, but the quarter's revenue bump was for traditional packaging. This is far from being large enough to matter compared to the billion-dollar shortfall in DCAI and the weakness in PSG.

Additionally, we expect a significant drop in IFS revenue after seeing accelerated purchasing in our traditional packaging business and cyclical weakness in wafer equipment buying in the first half of the year, impacting the IMS business.

They did announce a new 18A customer, but we don’t know who it is. The hope is that it’s Nvidia.

In addition to the 3 intel 18A customers we disclosed in Q3, we won a key design win with a significant high-performance computing customer. This customer was particularly motivated by our unique leading-edge manufacturing capabilities and U.S. capacity. We came into 2023 committing to one 18A foundry customer. We executed on 4 inclusive of a meaningful prepay and our momentum continues to grow.

Doing some math, we can probably attribute ~400 million in the guide to Mobileye, a billion to PSG, and likely the remainder to DCAI. Meanwhile, the Client segment will continue to improve off cyclical lows. That’s probably good for AMD. For further knock-on impacts for AMD, please consider subscribing.