Intel is the Antithesis of "Smart Capital"

Intel defends the dividend. The balance sheet is in shambles. Additional thoughts on positioning.

Let’s start with the results before I get a bit more granular. Below is a great graphic from Consensus Gurus on Twitter.

Client missed, datacenter slightly beat, network and edge missed, and importantly we are seeing the result of de-leverage in a high fixed cost business. Intel didn’t want to guide for the full year, just for Q1, and the margins will erode.

Gross Profit Margins are Worse than Stated

But it’s much worse than the first blush, as there were meaningful accounting adjustments and an insurance adjustment to prop up the current quarter’s profit margin. There was a ~170 bps improvement to gross margins from insurance, meaning their core gross margin was closer to ~37% this quarter.

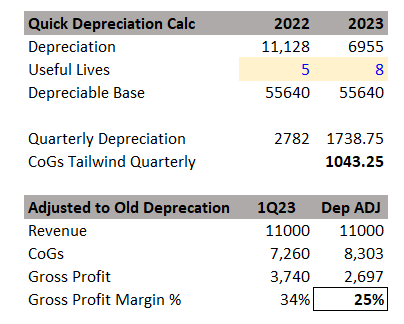

Next, the accounting change to improve depreciation was moving the useful life of equipment from five to eight years. That reflects the change of business model to IDM 2.0, and while tools do last a long time, this is a pretty egregious accounting lever to pull to improve gross margins.

Taking their annual depreciation of ~11,128 million, assuming that is for five years to get the approximate total asset base, and then dividing that number by eight, gets us to annual depreciation of ~6,900 million a year. They said it would reduce total depreciation by ~4,200 million in 2023, and this calculation gets us to ~25% gross margin for 1Q 2023. This implies a 25% Q1 2023 gross profit margin.

This is an approximation, but if I used the old accounting treatment for Q1 2023, the underlying story is much worse than the headlines. Gross margins are not comparable; if they were, it would be the worst in Intel’s storied history. I believe this is an all-time low for Intel’s gross margin.

This is frankly out of the realm of imagination for Intel. I would never have thought this could be possible, yet here we are. They ramp up a huge amount of capital for future projects while losing massive market share during an intense drawdown. This is the worst case. So let’s step through a few other things on the call.

On Inventory

They think Q1 is the “most significant inventory decline at our customers we’ve seen in recent history,” but the bottom of inventory will likely be pushed out another quarter. Refer to my piece on inventory for more details. I believe in a broad inventory bottom in Q1-Q2, but likely, Intel will be later than the industry. Memory as well will trail the industry.

We should be led out by consumer GPUs and smartphones in China. While the data center begins its digestion, the price cuts at Tesla potentially imply EV deceleration.

Does that mean that the channel is cleared at Intel in Q1? We won’t know, and Intel has no visibility into their business. I remain optimistic that inventory should improve. The biggest swing factor is the strength of the Chinese reopening, yet I doubt Chinese people will buy more PCs after the rolling lockdowns are done. Like the rest of the world, China had a cyclical bump in 2021 and has moderated.

When asked about the biggest gross margin driver, they answered that it’s all about revenue. The problem is that they don’t have any meaningful competitive products for the rest of the year. In the client, they are playing pricing wars; in the data center, they have an objectively worse product.

So while there should be a cyclical recovery in the second half, we are talking maybe ~40s gross margin on the other side of the cycle. Getting back to cycle-high margins takes leading products, and Intel doesn’t seem to have that in store for a few years, if ever.

PC TAM Delusions

The most confusing part of the entire story is the PC TAM. Dylan did a great job discussing the unreasonable TAM expectation of ~300 million units. I think that is the part that is terrifying about Intel. They still believe in the 300 million unit estimate, while everyone disagrees. It’s Intel in the wrong here.

Intel is clinging to 300 million units, similar to how it’s clinging to its dividend. Why? I have no idea.

Datacenter Hopium

Additionally, the discussion of the data center seems to be very delusional. Intel talks about its incumbency, an incumbency they are actively losing. A pessimistic reading is that Intel has a 95% share to cede.

There's an enormous on some -- many of the cloud customers, 95-plus percent of their installed base is Intel. That gives us a very strong incumbency that we get to renew as we rebuild our customers' confidence. So as you put all of those things together, yes, we realize that we stumble, right? We lost share. We lost momentum. We think that stabilizes this year, and we're going to be building a road map that allows us to regain leadership for the long term in this critical market.

I would feel good about that if the AMD products didn’t look so compelling, not to mention the hyper scaler’s internal products. The only hope for Intel is that Chinese hyperscalers come back online in a big way. Seagate recently expressed optimism in this segment, but Intel needs this desperately.

Intel is “Dumb Capital” with the Dividend and Capital Structure

Intel got asked why they are paying a dividend this quarter, which is the first time they have ever been asked that question, and what’s worse is their answer. A complete stonewall.

Yes. Well, obviously, we announced a $0.365 dividend for the first quarter. That was consistent with the last quarter's dividend. I'd just say the Board, management, we take a very disciplined approach to the capital allocation strategy, and we're going to remain committed to being very prudent around how we allocate capital for the owners. And we are committed to maintaining a competitive dividend.

How can they use the words smart capital when they are paying a ~5%+ annualized dividend while burning cash into the foreseeable future? It feels downright delusional. If they cut the dividend, I think the stock would go up, yet they continue to cling to the dividend.

Intel had negative ~$9.4 billion in free cash flow in 2022. They are paying ~$6 billion in dividends a year. They have ~$11 billion in cash at year's end, which will quickly be burnt this coming year. Remember, their original aspiration was burning ~$1.5 billion this year and being FCF breakeven for 2023 and 2024. They will burn through their cash balance at an accelerated rate with the dividend.

The 2029 tenor of bonds is yielding 4.5%, yet the equity is yielding 5.5%. I don’t understand why they would let this happen to the capital structure; frankly, the debt looks absurdly priced. I think the debt is an interesting short if you can do that.

Right now, Intel’s capital structure is almost a ponzi scheme. They are borrowing debt to pay out equity to investors. I understand the fear of dividend funds being forced to sell Intel stock, but this is not sustainable, and as Intel gets more levered, they are screwing over their future even worse.

Intel still has an A+ debt rating, but this will have to drop at some point. This a reminder that they are burning cash and will have meaningfully negative EPS for the coming future. How do you feel comfortable issuing debt against a capital-intense business in turmoil with no visibility to profit for at least two quarters?

We have seen this story play out in equity markets over and over. The unsustainable dividend always breaks. I’m reminded of this amazing quote.

“More money has been lost reaching for yield than at the point of a gun.”

– Raymond DeVoe Jr.

When you are forced to issue debt or equity to pay out an unsustainable dividend, it always breaks. A more recent example is the MLP craze, which would issue equity to pay out the unsustainable dividend. Issuance ponzis always break, and this one will too.

Intel’s credit rating, balance sheet, and capital structure make no sense to me. Cut the dividend cowards, or at least never use the phrase “smart capital” ever again.

A Murky Horizon, A Bit of Hope

I do want to leave you with a bit of hope. I am at the point where I am just tired of writing mean things about Intel. In an effort to be balanced, I think there is still a chance the channel could reach some equilibrium in the middle of 2023, and Intel could grow again. It will sadly be tepid, not the traditional V-shaped bounce from the bottom.

The biggest and continued important factor in semiconductors and global markets continues to be China. China’s Q4 COVID fiasco hurt near-term results, but as they continue to reopen, China’s incremental demand could bail out the entire semiconductor cycle and, hopefully, Intel in the process. China is 30% of the global demand for semiconductors and has been effectively asleep for a few years. Intel is uniquely levered to PCs, which will not benefit, so it’s up to the Chinese hyperscalers. Good luck.

Additional thoughts on positioning and AMD are behind the paywall.