Intel - They are Who We Thought They Were (Share Donors)

Intel - They are Who We Thought They Were (Share Donors)

I also follow-up the CXL and History posts

What. A. Quarter. Intel is a trainwreck, and I’m used to bad quarters, but this is the worst I’ve seen from Intel.

Pat Gelsinger, Intel's usually upbeat CEO / wonderboy, sounded much less enthused yesterday on Intel’s call. There's a good reason for that. The results were abysmal.

It was hard to come away from the call with any positives. They missed in almost every metric except Mobileye. They completely wound down Optane, they sold their Drone business, and now that’s six businesses that they have exited. Shedding the non-core businesses was supposed to focus Intel on the core, but looking at the core business imploding makes me wonder if the NAND business is doing this poorly. I don’t think so.

One of the funniest things to me is how Pat framed DCAI and admitted that they are losing share in Datacenter.

Turning to DCAI, as we stated at Investor Day, over the next couple of years, as we rebuild our server product portfolio, we expect to grow slower than the overall data center market. It's not a fact we like but the forecast we see. We have a singular focus to regain performance and TCO leadership across all workloads and use cases from enterprise to cloud.

Yet they have a huge incumbency - or the most share to lose.

The advantage of our incumbency position remains underappreciated and provides significant opportunity to drive outsized advantages to our customers

Pat might as well have said, “we are a large and meaningful share donor in the data center.” Because that's what it means to have a significant share and grow slower than the market, but enough about datacenter, PC was also horrific.

I regret not recommending everyone to short Intel, I knew PC would be bad, and PC is 50% of Intel’s revenue. It’s inescapable that Intel would do poorly. The part that worries me is that I don’t think that Intel’s new guide down is particularly that conservative. Let’s talk about that.

Last quarter, Intel talked about PC being down from MSD to HSD, with customers burning inventory and “subsiding in the second half of the year.”

We expect elements of this inventory burn to continue in Q2, subsiding in the second half of the year. Although these headwinds have reduced our CCG revenue forecast, we expect CCG revenue to increase in the second half of the year as a return to normal seasonality boost demand (Q1 2022)

Q3 is in the year's second half, and it looks horrific. Now they expect PCs to be down 10% in volume, which is more in-line with market forecasts, compared to the clearly above market forecast last quarter. The part I don’t buy is that Q4 will magically start to improve inventory. I acknowledge the seasonal impacts, but we aren’t even firmly in a recession. Continuing to push out hopes that things turn around very specifically in Q4 feels contrived to me, especially when the second half of the year’s macro results could be much worse than right now. Intel moved down numbers, but this is not a kitchen sink. That’s the worrying part. Oh, speaking of which, how the hell did they not preannounce this?

They didn’t answer that question (weird), and then they also talked about other execution issues that they have been facing, namely Sapphire Rapids volume delay. Pat mentioned execution issues multiple times, and the proof is in the pudding; they are not executing well.

The infamously broken culture continues to hurt, and Pat saying that employees are engaged via surveys is not exactly assuaging my fears. In fact, given their GAAP net loss (maybe one of the few in the company’s history), the variable bonuses that engineers are receiving are one the lowest, if not the lowest, payouts in the company’s storied history. How will you turn around a culture when you keep losing and everyone’s making less money? Talk about negative momentum.

Capex is another part that I found a bit confusing. Dylan is already out calling Pat for not cutting the dividend - which I agree with, but I understand the struggles of cutting the dividend for index inclusion.

The part I found wonky was that they moved down capex this year by $4 billion, funded by higher smart capital decisions, yet they didn’t model any CHIPs act money in 2022. I understand moving capex lower so they don’t add too much capacity, and I understand shifting of WFE because of tool delays. Yet, I can’t help feeling like their biggest financial lever is being pulled way too early.

I think what’s effectively happened is that their biggest lever to “beat” their financial model was capital offsets, and it’s clear that they sandbagged capital offsets during the Investor Day so that when the business turned around, they could show some stellar results. But they have to pull that lever way too early, and now they might be a bit screwed. The upside is being taken out of the stock to support numbers in an increasingly rough period. A recession hasn’t even happened in earnest, and it’s this bad. Imagine if the economy gets worse.

Concluding Thoughts

I could go on and on and on about Intel. DCAI, in particular, is terrifying, and either all of the hyperscaler capex plans are about to fall off a cliff (they haven’t), or AMD is about to murder earnings on relative share gains (which makes sense given TSMC’s results). The entire ~2 billion revenue miss could probably accrue to AMD this quarter. The valuation is also starting to become concerning to me - because I don’t know how to price it, and my gut says lower.

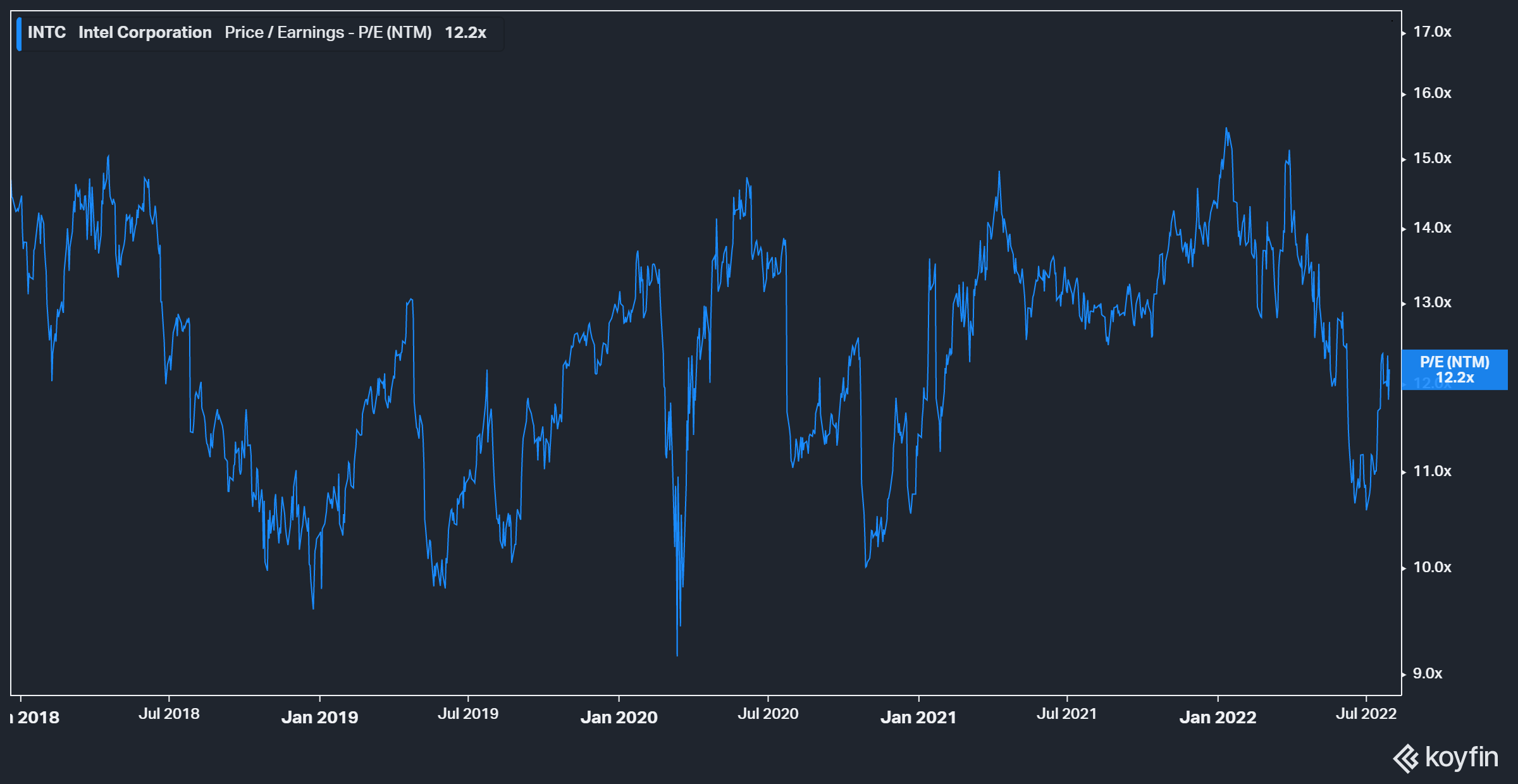

Let’s start with the $2.30 earnings for the year as our base. I first expect next year’s earnings to be lower than the entire industry, but for the sake of this analysis, I’m going to say 2023 earnings are flat to be conservative. Intel’s been trading at ~12x earnings on average for a while now, getting as low as 10x.

That’s a share price of $23-28 or 25% lower. I can appreciate that maybe that’s trough earnings, but I want to point out there’s no FCF underneath it to support it. I don’t think there is valuation support at this current price because multiple peers are executing, growing, and making FCF trading at 3-8 turns higher.

What is the valuation support? Book Value is at ~100b, or 40% lower. I don’t know how you’d value this one, and I think the direction in the near term is lower. This report has a lot to digest, but almost nothing is positive. Post Earnings Announcement Drift takes a few days to digest, and this one, in my opinion, is lower. And that’s just the financials; let’s talk about our confidence in Intel’s culture!

Intel clearly cannot execute on anything. Sapphire Rapids got massively delayed, and how are we supposed to believe in Pat’s five nodes in 4 years if they can’t even get the first one to work? Oh, and that huge and aggressive bet for BSPDN? Kiss 20A’s dominance goodbye because by the time it’s ramped, TSMC will be inserting PowerVia into their process at the rate Intel is executing.

Pat’s Intel was supposed to be a recovery in their Grovian culture of execution. I can’t help but see the same Intel that missed 10nm multiple times, misstepping over and over. Intel is who we thought they were - a broken culture dying a slow and ugly death. The turnaround was supposed to be not that same Intel as before, yet they keep acting like who we thought they were. This turnaround was always going to be slow, but this isn’t looking good. Something needs to change, but I couldn’t tell you what that is.

CXL Follow Up

When I was on my recent hike, Dylan of Semianalysis passed along a paper about how CXL impacts data center costs. We inadvertently published about CXL on the same day, but I wanted to do my quick take on the paper because it puts numbers to the crux of the CXL bullishness. Here’s a list of some stats:

In Azure, up to 25% of memory is stranded

Google reports that 40% of DRAM is used in production clusters

50% of all VMs never touch 50% of their rented memory

Disaggregation can achieve a 9-10% reduction in overall DRAM

CXL can result in an overall decrease of 4-5% in cloud server costs

The most shocking part is that this is just by adding a single block of disaggregated memory. This isn’t even an advanced implementation of CXL, just a simple one. I don’t think this is considering more complicated structures like a larger ML cluster, just production clusters for rent. There’s going to be more in time - CXL is going to be a huge deal. This is just the beginning.

Lessons from History Follow Up

The post is long, but the thing I didn’t talk about is where I think we are in the cycle. If it wasn’t abundantly clear, I tried to highlight the 96/97 downcycle because we are now in a downcycle! Gluts follow all shortages, and a soft landing seems impossible.

The double ordering of this cycle is expressed through longer backlogs, but unlike in the past when there were 10s of memory fabs, things are a bit tamer. I believe that this will be a “typical” semiconductor pullback, more akin to the 2013 and 2018 cycles than the traumatic 2008 and 2001 cycles. But time will tell how bad the macro situation is.

In times of distress, it’s time to move up the quality curve until high-growth names become extremely bombed. Right now, that’s EDA - which refuses to go down. I am increasingly worried about MSI (million square inches) and volume names; FORM is an excellent example of a name that was supposed to benefit but is hurting.

We are still in the first round of earnings cuts, and I think it isn’t quite time to start buying the dip. Instead, I believe it’s time to do some work on names with longer-term potential, and some that come to mind are SITM and MRVL. Those high-quality product stories will eventually work, but it will take stones to step in. Time to work on conviction now.

I’ll have a more typical earnings post next week - I was writing it, but Intel was too good not to have a standalone. I usually put posts like this behind a paywall, but Intel’s story is too good to not tell. So if you found this write-up helpful - please consider subscribing or sharing. Both would immensely help me. Thank you!

We were all somewhat wrong about Gelsinger. We thought he's shrewd, bold, yet humble. Reality is that he's not much different from his predecessors, Wall Street puppets. Yet the irony is that even Wall Street does not like puppets, not for long.

Intel will keep losing share in data centre until it can make EUV work at volume and compete on power/performance. Metrics beats marketing every time, eventually.