Intel's Troubles and Lam Research's Cautious Optimism

Another week of earnings! Never a dull moment.

Before anything else - this meme needs to be seen.

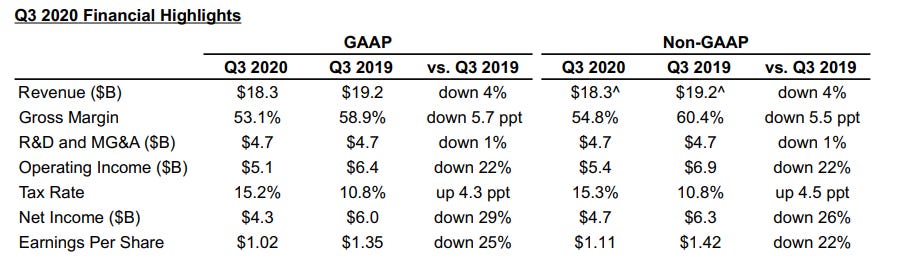

Intel’s results were not pretty. It’s like a murder, and while many are looking around and wondering what happened, it’s pretty clear to me. Intel is in trouble. Nothing new, but just a lot more dismal than you’d think possible, and it’s starting to make the bear case the most likely one.

I have not been bullish on Intel for a while. It’s pretty easy to see why, other than valuation, Intel is a grim investment choice. If the technology is good, customers will adopt it and the profits that are expected will come. If the technology is bad, your customers will abandon you, and your expected profits will likely miss. But this was below any kind of expectations I had going into the quarter.

Intel’s Results

There is no way to put this other than “this is ugly”. Most other companies had wonderful quarters in the industry, and Intel did not. Intel’s results are likely a function of competition (AMD), digestion of Q2 revenue pull forward, and customer weakness.

The operational deleverage was staggering. In a fixed cost business, every incremental bit of revenue tends to highly margin accretive, but that same logic applies on the way down. EBIT down 22% is just the beginning, with the fourth-quarter outlook another 150 bps of deleveraging. Watch out below.

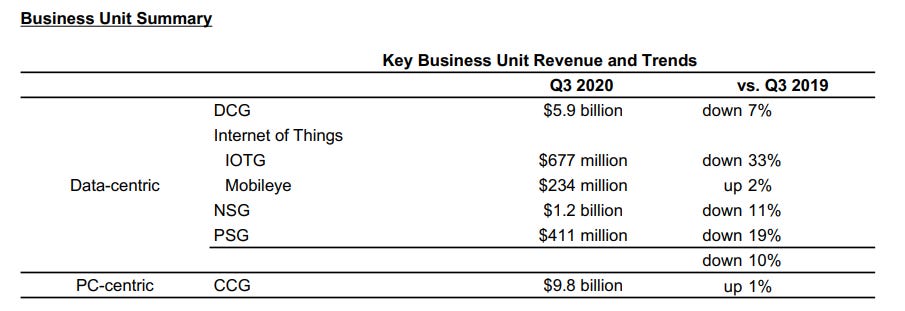

The really ugly part comes next, DCG, or “Data Center Group” is not that much data center after all, and is mostly an on-prem enterprise business. I knew it skewed Enterprise, but this result really shows how ugly it is.

“Cloud revenue” grew 15%, but the entire DCG segment shrunk -7%. Enterprise was the delta for this, at a staggering -47% YoY comp.

*Edit - I was wrong, Cloud is still the majority of revenue. I didn’t see the part about the Government / Enterprise -47%. This puts Cloud at ~2/3 of revenue, and Enterprise at ~1/3 revenue.

This is also the single strongest read through to corporate IT spending budgets in my opinion. The recent CIO surveys about JNPR/ANET/etc falling off a cliff because of enterprise spending seems all but confirmed from Intel’s earnings. I’m curious to see CDW’s results.

Another tidbit is that Intel is seriously considering going to TSMC. Some of these quotes feel like TSMC/MediaTek is all but assured.

So the criteria are relatively simple, and we're evaluating each one of those kind of as we exit 2020 and really early 2021 because that's the time that we'll have to make the determination as to whether we're buying more 7-nanometer equipment or whether a third-party foundry would be adding that capacity. So we're going through this process, really looking at our capabilities, others' capabilities around those 3 fundamental criteria. I would say since the last time we spoke, our 7-nanometer process is doing very well. I mean last time we spoke, we had identified an excursion. We had root caused it. We thought we knew the fix. Now we've deployed the fix and made wonderful progress. But nonetheless, we're still going to evaluate third-party foundry versus our foundry across those 3 criteria. And the call will be towards the end of this year, early next year.

The thought of the Intel of old even considering this is nuts. And what does that mean for the actual fabs they own right now? How “valuable” is the accumulated IP and assets of Intel if they cannot move to 7nm? Compared to the “money good” comment I made about TSMC, the value of any Capex spent at Intel seems dubious.

I want to see Intel succeed, for the sake of America and for the sake of our semiconductor independence. But each and every call seems to be slipping into Taiwan’s continued dominance. Taiwan is already the single most geopolitical asset globally, and will likely to continue to rise in that regard.

Lam Research’s Cautious Optimism

If the tone of Intel’s earnings were of dismay, Lam’s was of cautious optimism. Lam Research’s entire call was about China (of course) and is all of this pull forward or not. If you remember in Cadence’s China quarter piece, I talk about how there is a bubble in China. We are seeing this flow through to the numbers.

Lam’s Results

It’s a great quarter - but it almost always is for these guys. But is this some kind of stocking event or pull forward? The answer from Lam seems to be no.

Yes, Tim, it's hard to know, to be perfectly honest. One thing I looked at, in anticipation of this question coming up, is from the beginning of the quarter to the end of the quarter, did any customer meaningfully increase their spares orders with us in China. And the answer to that was no, not really. That doesn't mean that maybe they weren't planning to stock a little bit ahead. It would be pretty hard at times to know. But I don't see a big stocking going on in China for spares as maybe the way I'd summarize that. I don't know, Tim, if you think any differently about that.

A reminder that Lam not only sells their semiconductor equipment, services the equipment but also provides spare parts for the equipment. They would know what kind of stocking would go on for a broad pull-forward, and I don’t think this is it. This is really alarming because this was the highest quarter of China's revenue in the history of the company. If this isn’t a stocking event, is this the run-rate kind of demand from China going forward?

I think it is. I have expressed concern about NAND in the past, especially the notable entry of YMTC into the NAND space. I think that DRAM for now looks good, and many choose to participate in the memory recovery via the optically cheap Micron.

But I think the better bet is with the better business model. Lam has a better return on capital, a better FCF conversion, and a better share repurchase yield. And the outlook for next year is pretty good. They are trying not to ramp expectations, but clearly, an extremely strong outlook for next year is coming.

In my view, NAND is pretty decent right now. And I think it will be pretty decent next year. Again, based on our view of the industry, inventory, investment plans, I think it will be a pretty decent year for '21 next year. We're not going to give you numbers on '21 yet. We'll do that in next quarter's earnings. But I think it sets up pretty well.

-Douglas R. Bettinger

And while there are always concerns about Lam’s ability to sell to China, there is no concern about who going to be making the equipment. I like these two quotes in conjunction

Well, hard to know. That's a pretty recent announcement, and it would be a little bit speculation. I mean, Sidney, long term, the way I think about this is, at the end of the day, demand is what matters, right? Our customers are putting wafer capacity in place to supply demand. And things can get pulled in, pushed out a little bit on the margin. But at the end of the day, when I think about where I think the industry heads, supply and demand have to be in relative equilibrium over the medium or longer term. And whether that means we have 5 customers in NAND or 3, it largely doesn't matter. They're going to invest to satisfy demand in my mind.

But even in the long run, that -- we've seen that play out over every region. And what ends up happening is that turns in, ultimately, to business for our installed base business where we go back years later, and we're making that installed base productive. And so this industry is so efficient, but I don't think there's ever really anything that gets lost, quite honestly. And that's -- but I mean there's a lot of -- there are probably a lot of pieces to your question that require assumptions. But I think that it would cause some disruption, as we've said, in the short term. But in the long term, demand drivers and the need to supply semiconductors and semiconductors' equipment to meet them doesn't fundamentally change in our view.

And even if all of the Chinese manufacturing were to go to zero, it’s likely a meaningful percentage of the multinational customers would be able to move Fab equipment outside, say to the likes of Vietnam, Thailand, or Malaysia.

Yes. And maybe, John, I'd just add a couple of things, the way I think about it. When I look at the revenue in China for us, it's split fairly evenly between the multinational customer base and the local Chinese customer base. So to help you frame it a little bit, that multinational stuff, obviously, was a decision to put in a country that could have gone anywhere, quite honestly. And then as Tim alluded to, a lot of the Chinese customers are relatively new in their process ramps, so maybe they're a little bit inefficient or somewhat inefficient. But at the end of the day, they're building capacity to support long-term demand that somebody else will step into over a period of time. So anyway, hopefully, that's helpful.

The memory chips must be made, and Lam is going to be the one making them. Whether if it’s in China or not, Lam will be selling the service, spares, and equipment for the memory demand of the world. Lam is irreplaceable. No matter the industry structure, Lam will likely benefit from memory in an outsized way. While not as optically cheap as the like of Micron, you are trading up on the quality scale in a big way. I think Lam is well-positioned.

Let’s not forget how cheap this company is currently.

I’m not aware of many other companies trading at mid-teens capable of growing 20%+ EPS through a full cycle.

Some Other Updates

For the sanity of your inboxes, I’ll be doing weekly earnings coverage once a week. So I’ll try to consolidate it all into a single post. I also think I’m going to lower the quantity up the quality. Follow-ups with more actionable and direct read-throughs will be likely behind the paid Substack going forward.

Additionally, there is now a paid Substack! The first high conviction name is out - and I think if you’re looking for a way to participate in datacenter spending, it’s particularly compelling.