MARKETS AND SEMICONDUCTORS

All caps for the circuit break in Korea. What is happening in markets, and how does that impact Semiconductors?

Hello! I went on a short hike this weekend, which always seems to cause something to change. What changed was that we are seeing a very large leveraged unwind in the market, driven by the BOJ's hike in interest rates.

Let me write out the series of events. First and foremost, last week, we saw some of the first macro jitters. The CPI came to light, which was viewed as positive. But then NFP showed a bit of weakness.

Now, unemployment has started to rise, and historically, once unemployment increases by 50 basis points, a recession comes after. Some aspect of this is noticing that it’s a bit of a logistical flow and not a predictor, but something that always happens during that period.

Anyway, this sets the scene. We know that the macro has gotten worse, markets have ripped year to date, and we have reached a fragile moment. Macro fears were the tinder; now we are just looking for a spark.

The spark came in the form of a rate hike from the BOJ. Part of this was to defend the Yen’s catastrophic fall, but this was the proverbial spark for the tinder box set by macro concerns.

The rate hike was slight, but Japan has been the most accommodating geography globally for borrowing.

The yen, which hovered around 157 to the dollar at the time of the June meeting, hit a 38-year low below 161 in July - a move that likely affected the BOJ's decision to hike short-term rates to 0.25% from 0-0.1% at the July 30-31 meeting.

The knock-on impact was unwinding one of the most significant carry trades globally. It’s simple to understand: borrow Japanese Yen at an effective 0% interest rate, invest it in almost any other currency, or even worse, borrow on margin and buy shares of global stocks unaffected by the Yen’s fall.

If you borrowed at 0%, and now you have a funding cost, and the asset you invested in from invested in is going down, it’s time for a margin call. And that is precisely what happened in Japan, leading to a messy result in Asia. Below is the total buying margin in Japan. That’s ~4.9 trillion Yen.

Notice the magnitude of the total borrowings: 34 billion dollars of purchases on margin. That number won’t go to zero, but it should revert, and there are many flows to account for. We saw it most acutely within Asia, with Taiwan, Korea, and eventually, TOPIX all-seeing circuit breakers or historic down days.

Where does this leave us now? Two or three very credible market themes are swirling simultaneously, and the concern is that any of them could broadly wreck semiconductors and stocks.

The Fed Could Be Too Late (US Recession)

The first thing that freaks out investors is that we see quickly deteriorating fundamentals in the US consumers. NFP means that jobs are becoming more scarce, and the slight uptick in unemployment means that the impacts of higher rates are finally flowing through to the real economy. The consensus

In just one month, the consensus was about two cuts by the end of the year to over 4. Market-implied cuts are interesting because this measure is incredibly jumpy. But the market seems to be pricing in that we are currently in a recession, and cuts are coming, so it might be too late.

And these cuts are not the good kind, but rather the type that subsequently happens during a downturn - aka bad news is now bad news. The kind of cuts correlated with recessions - look at the timing for the first cut last cycle - shares crumbled after (in conjunction with COVID).

But the question of whether we are in a recession is a difficult one. As you’ve seen in the earnings posts, industrial production worldwide has decelerated meaningfully. So, while I won’t call it a recession, I think the jury is still quite out.

Nvidia Delays Creating an Airpockets

The other big thing is that Nvidia is seeing some delays in the B100 generation in favor of the GB200 generation and that the complexity of the GB200 could be causing accurate supply chain-driven slowdowns. Ming-Chi Kuo and The Information have written all about it. I liked SemiAnalysis’s piece the most.

The problem is that AI is the Semiconductor trade, and what is bad for Nvidia is horrible for semiconductors. While this could create air pockets in the spending done by the hyperscalers, the odds are that the spending is still higher.

Almost every major hyperscaler has already committed to more capex; we know it goes to Nvidia. Yes, it might have some revenue shifting from the B100 later back to the GB200, but I think it's a mistake to assume it isn’t Nvidia’s. A 25% drawdown should be more than enough to account for the revenue shift. Unless we go into a drastic recession starting today, I think that the odds are that next year's revenue will still be higher than this year. This is a shift, not a collapse. We got the confirmation that spending will continue from last week’s hyperscaler capex numbers.

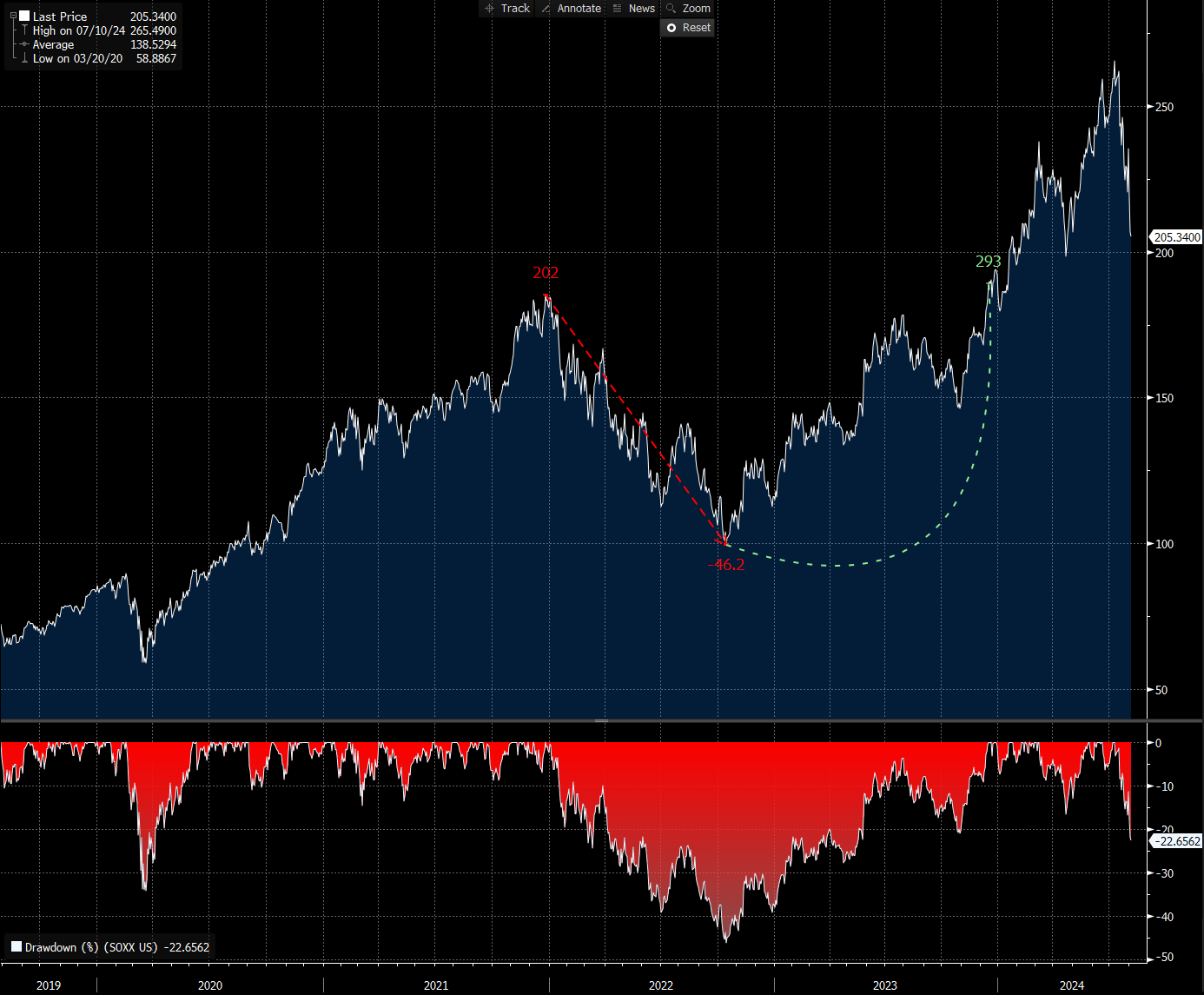

But Share Prices Have Reflected A Recession Halfway (In Semi)

But let’s talk about that because the thing is, even if there is a recession, drawdowns of this magnitude are attractive because we are ap[approaching halfway of a typical recession-like a drawdown of, say, ~25-30%. COVID only had a 27% drawdown in the Nasdaq; as of today, we are 45% of the way there.

Of course, I also look at Semiconductors. They have always been much more cyclical than the market, and the 2-year beta has been around ~1.5 times SPY. The drawdown there is already halfway to a COVID-style correction, and even if there’s another 25% leg lower, share prices going down do de-risk some of the correction.

So where does that leave us? I understand things are pretty bad right now, and I am unwilling to stick my neck out and call a recession. But man, do I like the risk-reward here. Maybe we are about to hit a global recession, and the Fed is too late. But as far as I see it, there’s a chance there’s a soft landing, and the market has just overreacted to the downside.

I see risk reward is much more balanced now, and I want to explicitly say that my bearish call on semiconductors and Semicap is over. Another 25% leg down would likely be a screaming buy territory, and I do not think this setup looks worse than the previous ones. Next year, WFE still looks like it will be meaningfully up. Nvidia will sell more accelerators, and we are just beginning to see green shoots in Mobile.

To keep the record straight, I wrote about being bearish semiconductors in early July and late June. I did it twice, and so far, so good on that call.

I wrote about that on July 2nd.

I can’t help but think that if this is my idea set, we are doomed for a market pullback. I continue to like Nvidia, but it’s very full price, and the rest of the AI trade is very long in the tooth. We are just starting to see some of the profit taking in AI for software, and I think that normalization can take sometime. Nvidia at under $110 is probably a screaming buy, personally.

And again on June 28th.

Not to mention that the SOXX / SMH index itself is extremely overstretched, and the relative performance versus software has been the best it’s ever been. After the recent software blowup, WCLD and IGV were barely positive for the year at one point. I think Software continues to have profitable margins and growth issues, but profit-taking in the AI trade and rotation into “losers” like SaaS create an outflow within TMT.

Putting it all together, I’m pretty cautious about semiconductors. This is a multi-month view but not a view for the year. If Gary’s insider sales are an indication, it’ll be a quarter of relative underperformance.

While I think there are real risks in the market, the risk is favorable to the upside when everyone panics. Now is the time to step in slowly to companies of higher quality unlikely to have meaningful headwinds.

I can name a few, but they are behind the paywall.