Marvell Industry Analyst Day

Marvell Industry Analyst Day

Marvell has the right game plan and players for the future: Can they win?

I was pleased to attend Marvell’s Industry analyst day. Unlike a typical investor day, it’s more product-focused than number-focused. But as anyone knows, the products and positioning will determine Marvell’s future. I think they told a compelling story.

Marvell has an interesting history, and that context is essential in appreciating the story today. Unfortunately, Marvell’s history is hurting them today. Still, interestingly their historical business was not what they were focused on during their analyst day, but rather their future business that they are well positioned in. To dive deeper into Marvell's day, you should read Dylan’s piece; he goes in depth. I will not focus on every detail like Dylan but instead, tell you the higher-level story of Marvell and what is incremental to their future.

A Brief History of Marvell

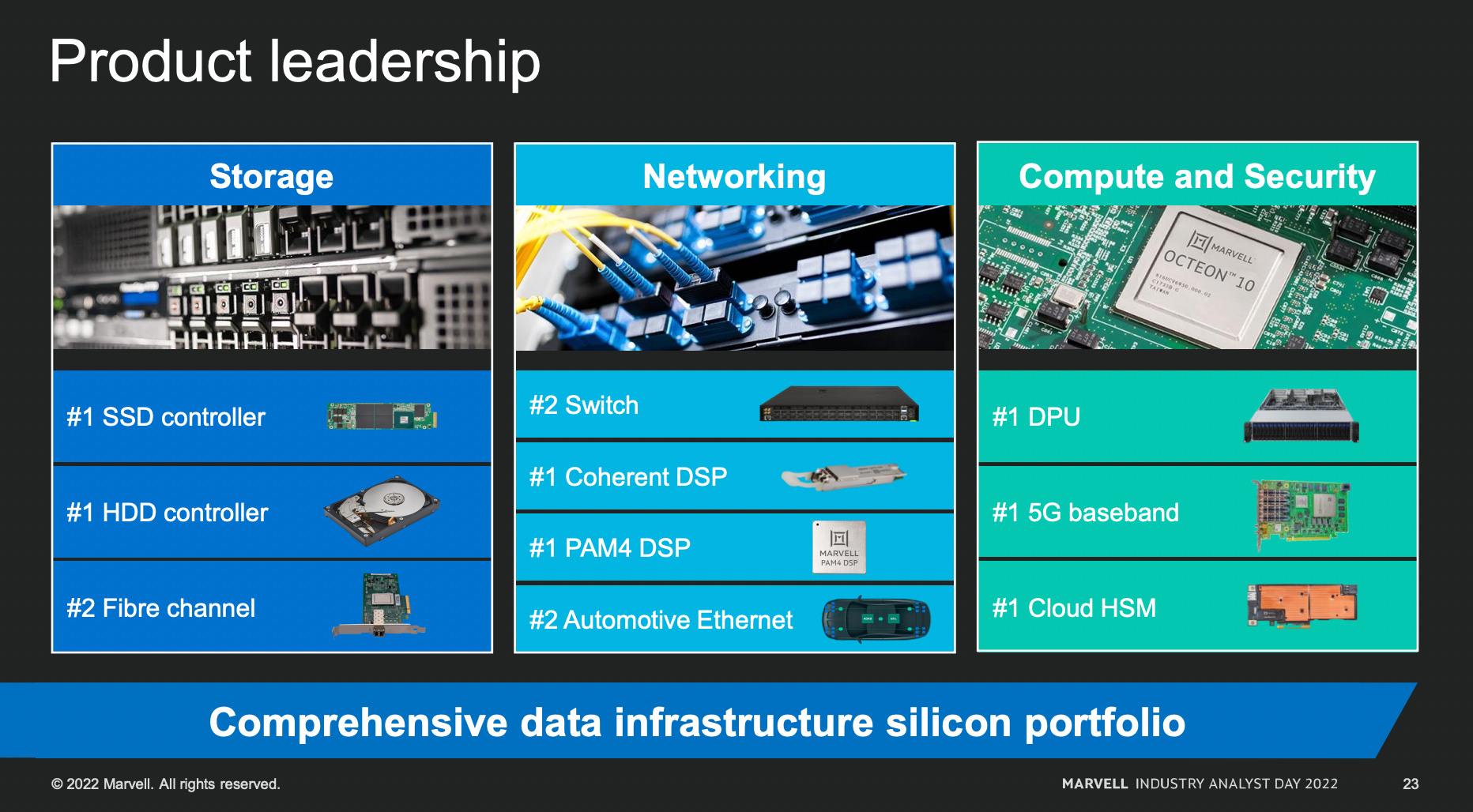

Marvell’s biggest product historically was the memory controller business, specifically in storage controllers in SSDs and HDDs. Their #1 position in SSD controllers and HDD controllers is something they still hold onto today.

Marvell was run by its founders, Sehat Sutardja, Weili Dai (Sutardja’s wife), and Sehat’s brother Pantas Stuardja. Marvell was listed in the 2000 bubble and has always been a networking adjacent company. From day one, it was a tightly controlled company from a governance perspective.

The significant change in Marvell’s trajectory occurred when Starboard took a 6.7% stake and ousted the founders. Sutardja and Weili Dai were ousted in April 2016, and after an executive search, Matt Murphy was appointed CEO.

Murphy is an essential player in this story as he reinvested the meaningful cash stream into a string of acquisitions.

Cavium in July 2018

Cavium was acquired for its DPU products and is the core of the Octeon product family.

Avera Semi May 2019

Avera was the ASICs solution team at Globalfoundries, and their talent is at the core of the ASIC team at Marvell.

Aquantia Corporation September 2019

The Aquantia acquisition kickstarted Marvell’s automotive business. Aqauantia, in particular, was instrumental in the 10G automotive products.

Inphi Corporation April 2021

Inphi’s platform put Marvell at the top of the 400G pluggable market with their coherent DSPs.

Innovium October 2021

Innovium was a venture-backed Switch company, and Marvell purchased them to further cement their positioning as #2 in the switch market.

Marvell, in the past, was focused on dominating the storage controller business. However, through these acquisitions, it has moved up the product stack to the networking business and has acquired its way to an entire portfolio addressing networking. It’s an underrated transformation in the semiconductor business.

In theory, they have a much more compelling strategy for infrastructure, particularly 5g. The business has shifted from consumer to infrastructure.

Today there are three end-markets of note, with a fourth and fast-growing market in automotive.

I will review each segment and then discuss what matters and their major growth vectors. Of course, each segment has a different franchise that matters, but if we refer to their market segment chart above, we can get a good view of the essential products in each segment.

Datacenter

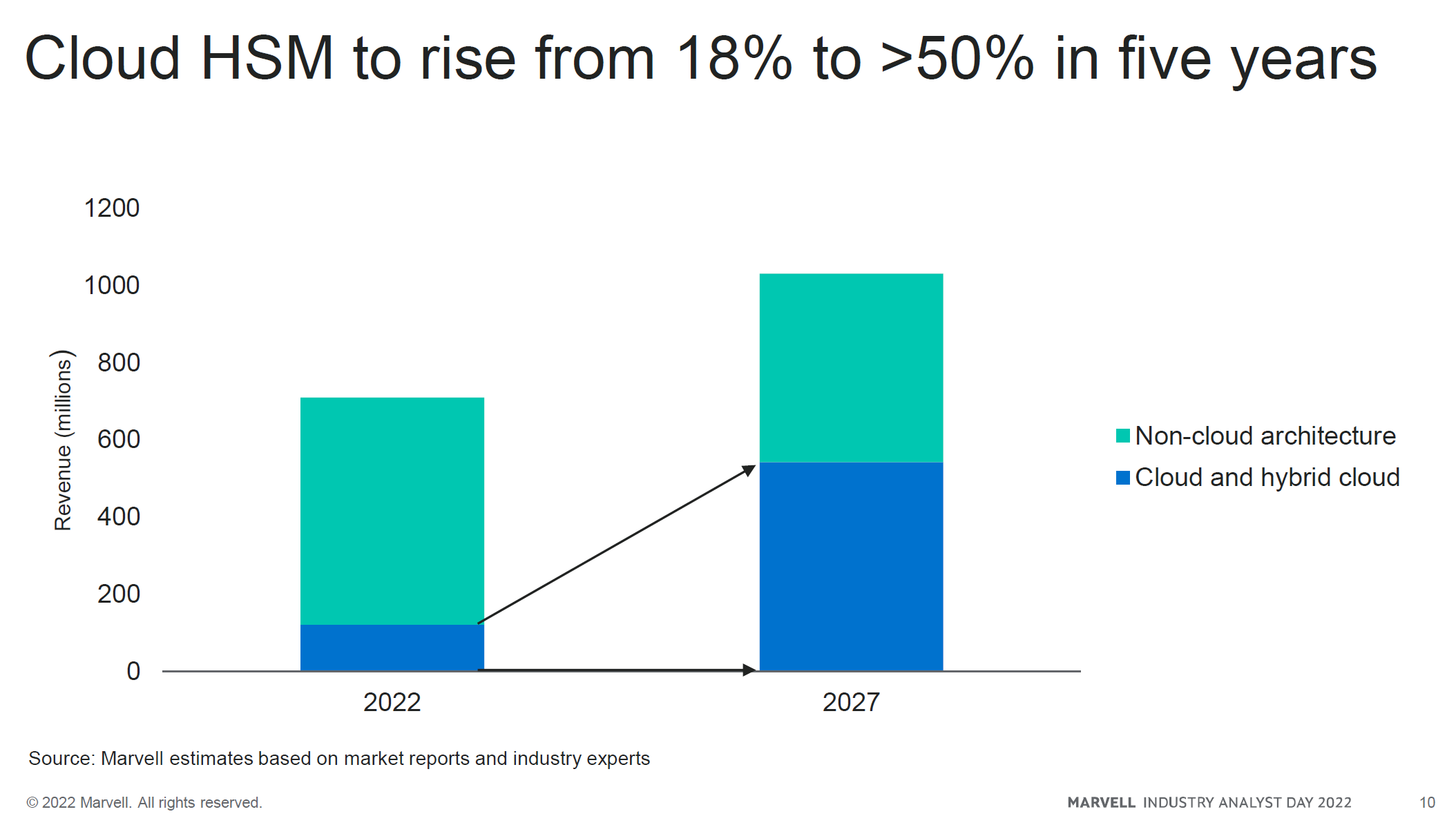

This business primarily consists of the optoelectronics from Inphi, network-attached storage and controllers, and their switch business. Incrementally they will grow their new cloud HSM (Hardware Security Module), continue to dominate in transceivers, and be a second source for switches. Their storage controller business will remain dominant, but it isn’t a quickly growing market.

In particular, their HSM looks like one of the larger new incremental markets they have identified, and they are the leaders there in a market that is poised to grow meaningfully in the next few years. From this graphic, we can assume that the HSM market will be ~4x in 5 years, which could be an incremental ~300 million+ revenue to Marvell.

The other clear driver is their continued dominance in the 400G PAM4/ZR markets and the eventual drive to 800G. This is from the Inphi acquisition, the clear leader to coherent DSPs. There is explicit talk that some share losses will happen, as it’s rarely sustainable to have ~90%+ share in a market, but they will continue to grow in this critical market for a long time. The insertion of content into the transceiver is one of the highest incremental additions of content on the networking side in years, and that trend is likely to continue.

Their switch business was recently jump-started with the Innovium acquisition, which lost a significant customer when they were private and joined the Marvell family. Innovium is a clear competitive product, but competing with the Broadcom behemoth is a tough battle. I believe, at best, Innovium could make this market closer to a 60/40 share over time. Today it’s less than that.

The storage market is where I don’t think there are meaningful share gains or losses to be had, and it’s a very mature business with lower volumes and now experiencing a cyclical drawdown. As the HDD market collapses from Chinese demand and the SSD market collapses from memory market woes, Marvell is caught in the crossfire.

Carrier Infrastructure

It took me a while to appreciate this segment. However, I think that in the future, this is the segment that Marvell dominates the hardest, and that’s because of their Samsung and Nokia partnership and Intel’s waning competitiveness in this market.

Marvell’s business is tied to the continued 5G capex rollout:

Marvell had design wins with Nokia and Samsung, who pivoted harder to vRAN and ORAN ecosystems, which telecom operators adopted over incumbents. Realistically, the ORAN alliance's true flexibility will likely not be realized, but VRAN will take a massive share. And Marvell is partnered with the share gainers.

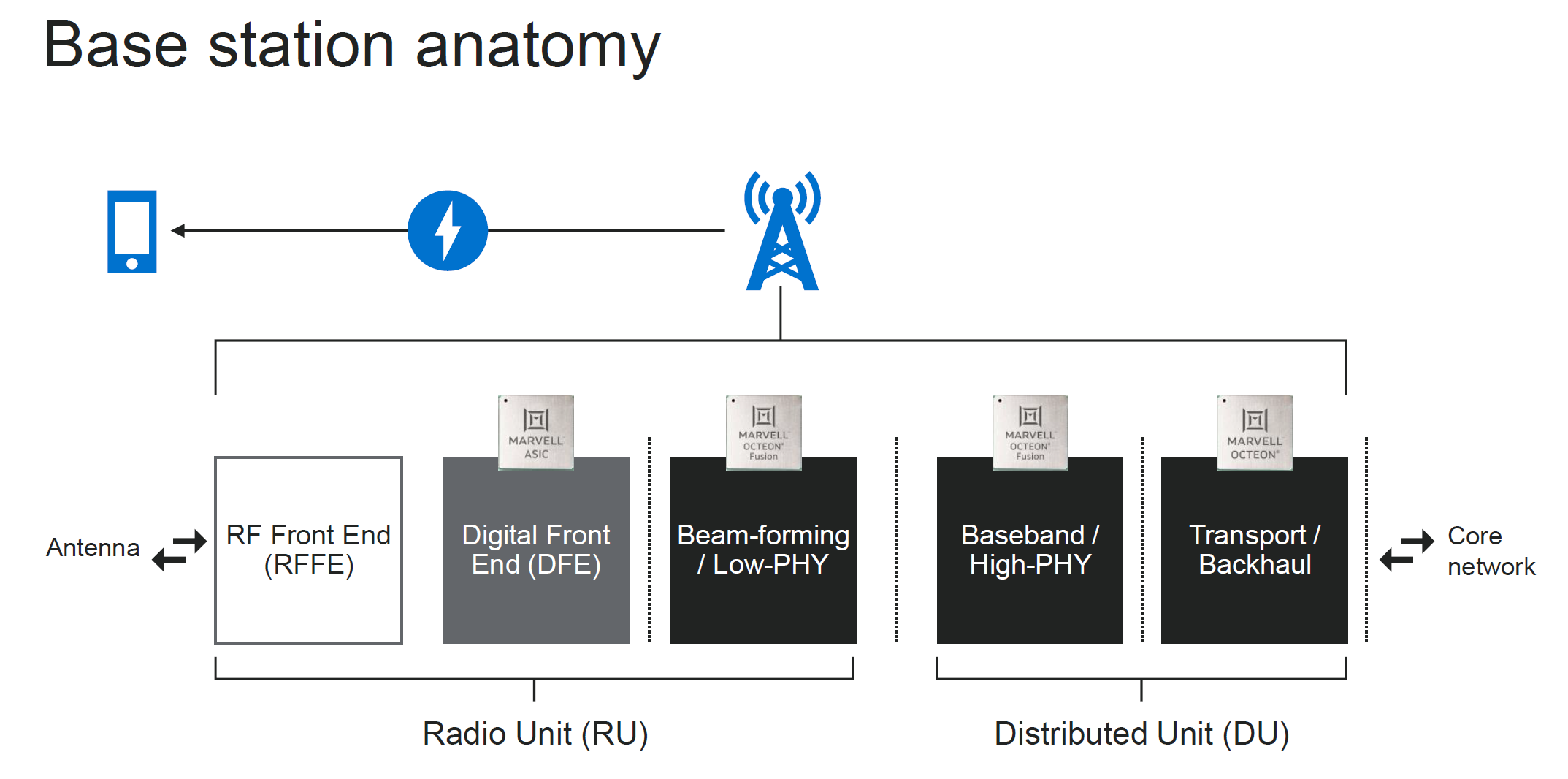

Here’s an overview of their products here:

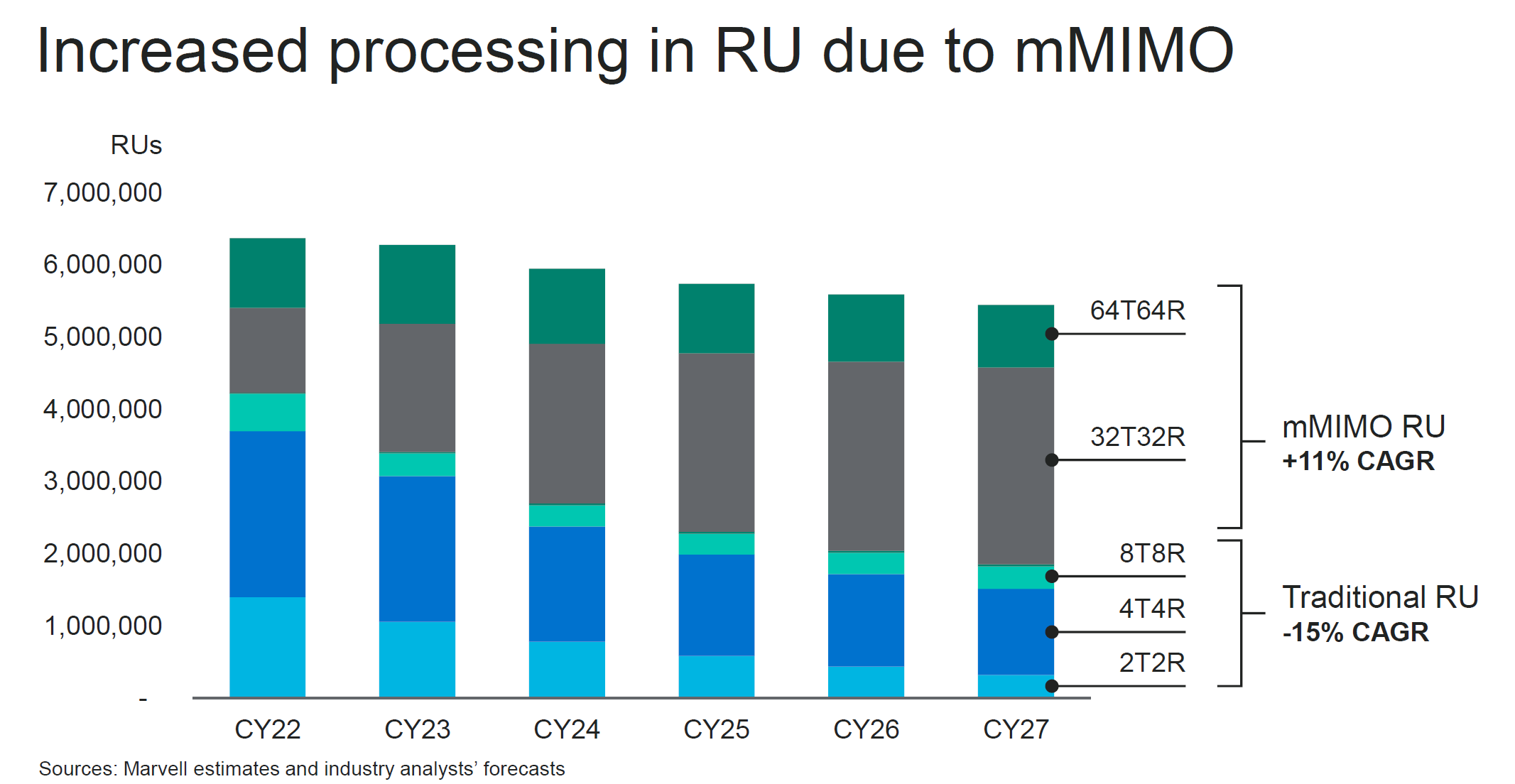

What’s happening is that the Radio Unit is starting to take a more significant part of the computing needs to get closer to the massive MIMO unit. So traditional Radio Units are losing share compared to higher-end RUs to save space.

The OCTEON Fusion (DPU) takes up less space and has better power consumption and energy footprint than FPGAs. As a result, FPGAs and CPUs are losing at the expense of Marvell’s semi-custom solution.

Between the baseband and the DPU segments, it seems like Marvell is becoming the defacto leader in 5G baseband and RU deployments. The momentum here is meaningful, and Marvell’s share and market dominance compared to competitors are palpable. This is the strongest end-market franchise within the Marvell portfolio and should do well in the coming years.

Enterprise Networking

While a slower-growing business than the other two segments, enterprise networking is still an important market. In particular, this is small campus routers, switches, and network appliances like firewalls.

This is where the Innovium switch comes into play, and the Octeon DPUs come into play. Octeon was originally a firewall product, and they are levered to firewalls and campus routers. They are a perfect use case for a firewall, a product that historically relied on a CPU and FPGAs. DPUs encompass computing, storage, acceleration, and fast data plane movement and are an excellent fit for the long tail of niche firewalls and other campus-level router products. Additionally, transceivers are still a meaningful part of spend for campus-to-data center networking. And lastly, we cannot ignore the storage and network-attached storage business.

Marvell’s enterprise business is fine on the net, but it’s not exactly the crown jewel of carrier infrastructure or data centers.

Automotive - The Call Option

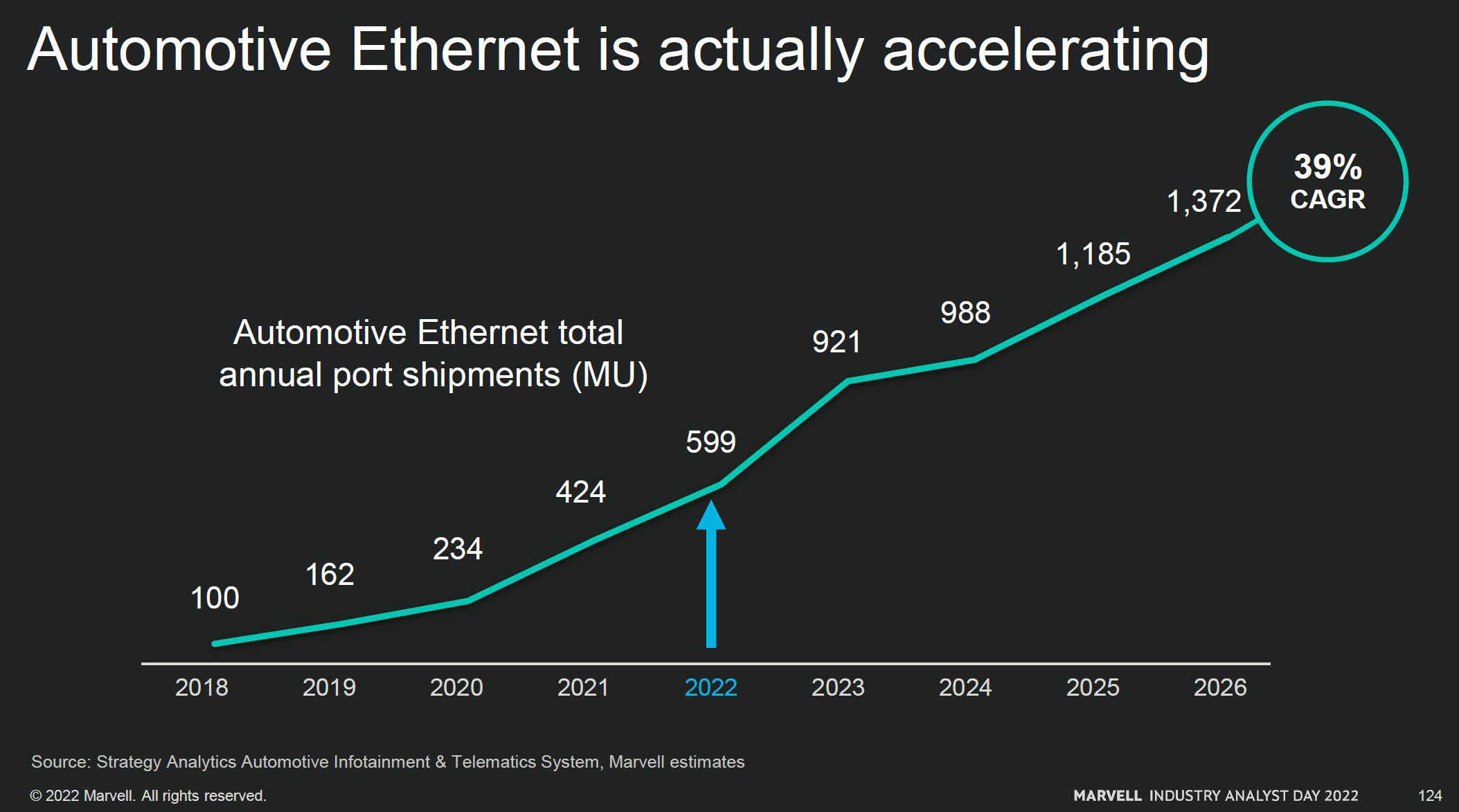

Automotive is the smallest end market but the biggest call option within Marvell. Automotive Ethernet is accelerating, and the positioning from Inphi and Aquantia makes them well-equipped to address this growing market.

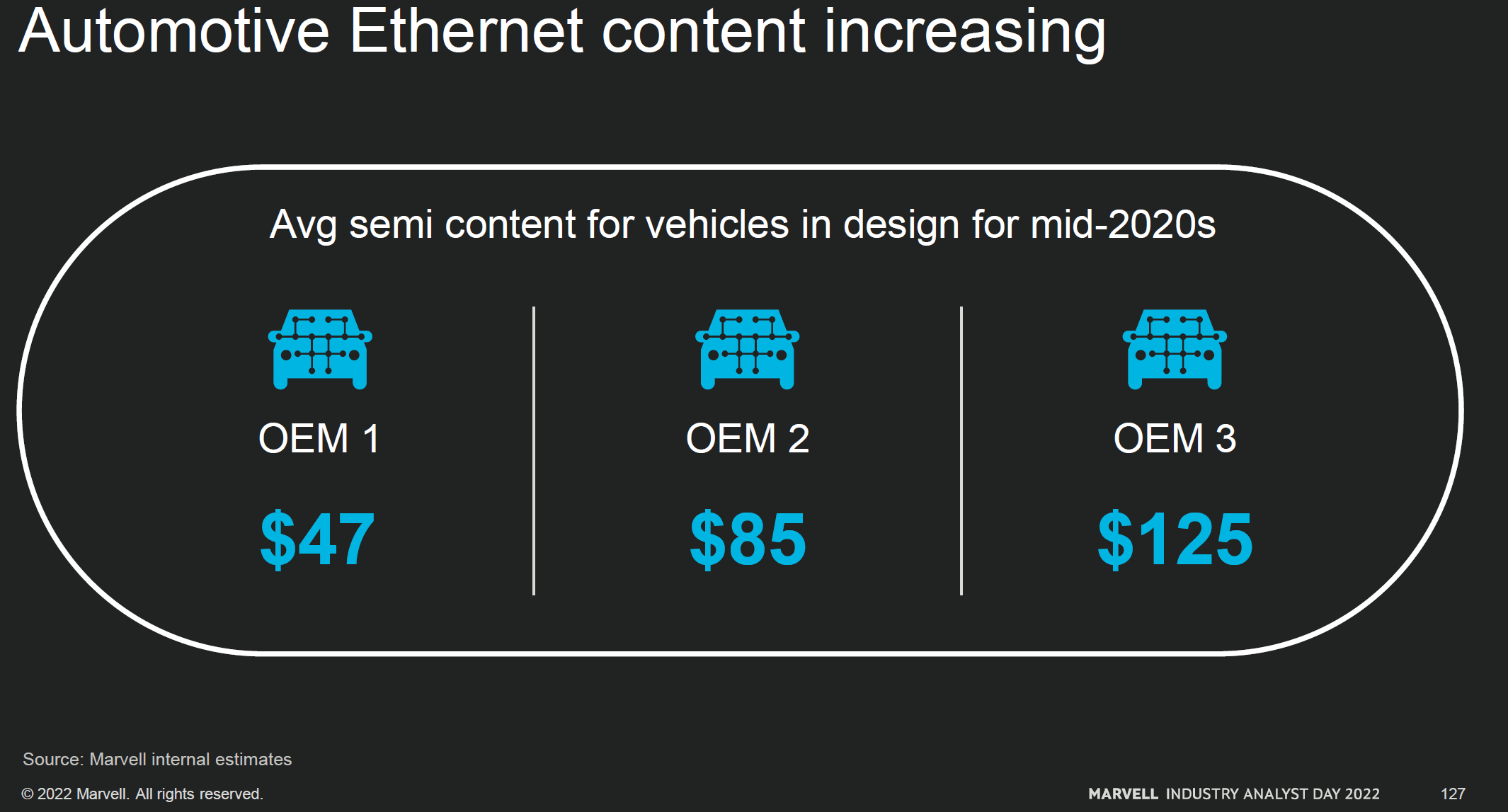

While most of the content story is focused on ADAS or EVs, something has to connect the ADAS systems, which will be ethernet. They give examples of between 47-125 dollars per car of content in design for a few OEMs.

The potential ramifications are this is a multi-billion dollar market for them someday, but that’s likely to be at the end of this decade.

Product Overview

Because this was an industry analyst day, not an investor day, they mainly walked through some of the technologies that make Marvell interesting. The significant few were PHY, CXL, the DPU platform, and HSM. I will address PHYs, and CXL briefly, but, importantly, the DPU.

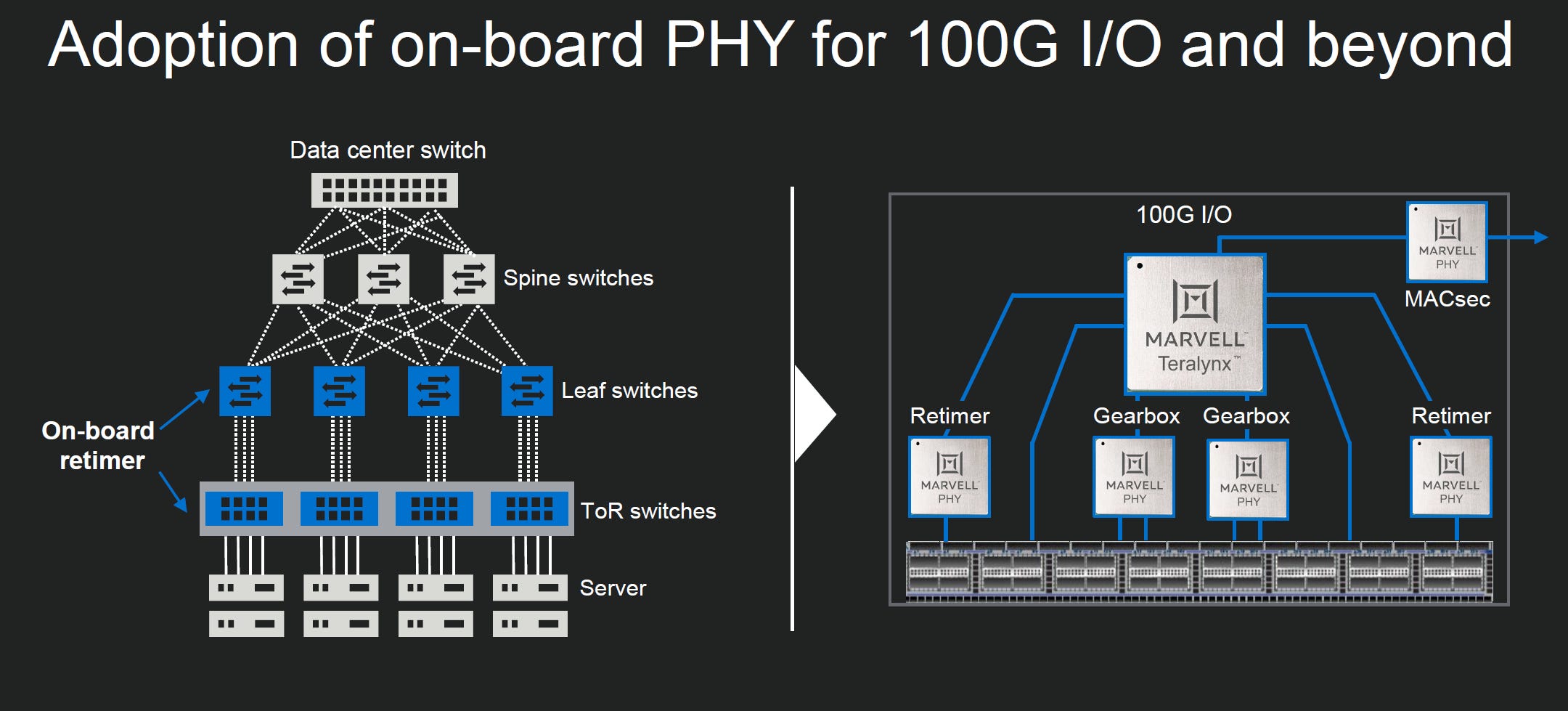

PHY and why it Matters

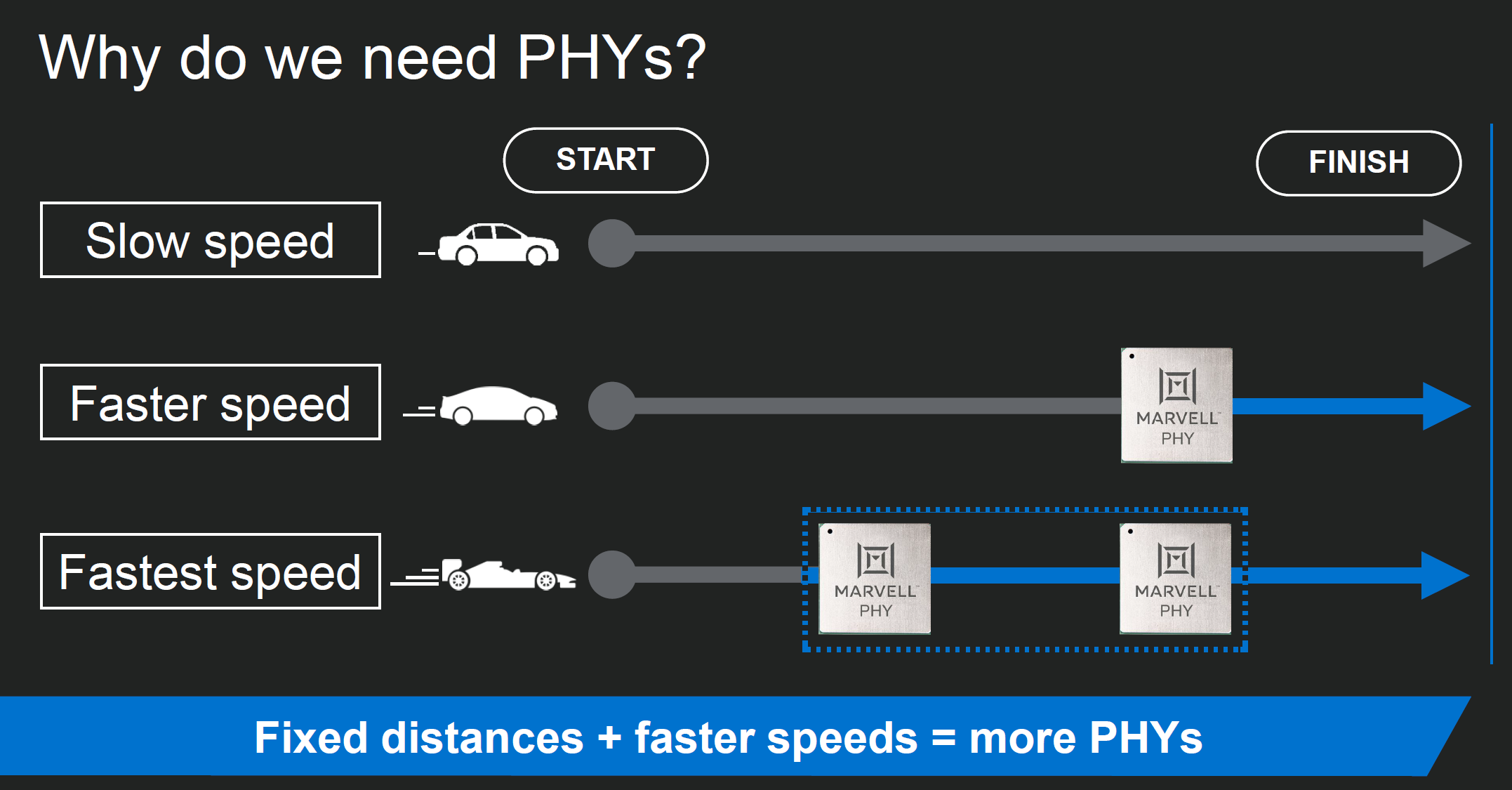

A PHY chip is a type of hardware device that is used in computer networking. It is short for "PHYsical layer chip," a device that communicates with other devices on a network at the physical layer. The physical layer is the first layer of the OSI model and is responsible for transmitting raw data over a physical medium, such as a copper or fiber optic cable. A PHY chip is used to convert digital data into a form that can be transmitted over the physical medium. It also performs other functions, such as error correction and data synchronization.

The analogy they gave is that if you want to go fast, you’re going to burn through tires quicker, and that means you need more PHY. So the faster data is transferred, the more PHYs are required.

PHY is one of those foundational technologies that go into many aspects of Marvell’s products and is a foundational part of why Marvell wins. Their PHY and SerDes are important for custom ASICs, automotive ethernet, coherent modules, switches, and DPUs. It’s at the core of what they do - they believe they are leaders, and it will continue to entrench them in the networking markets.

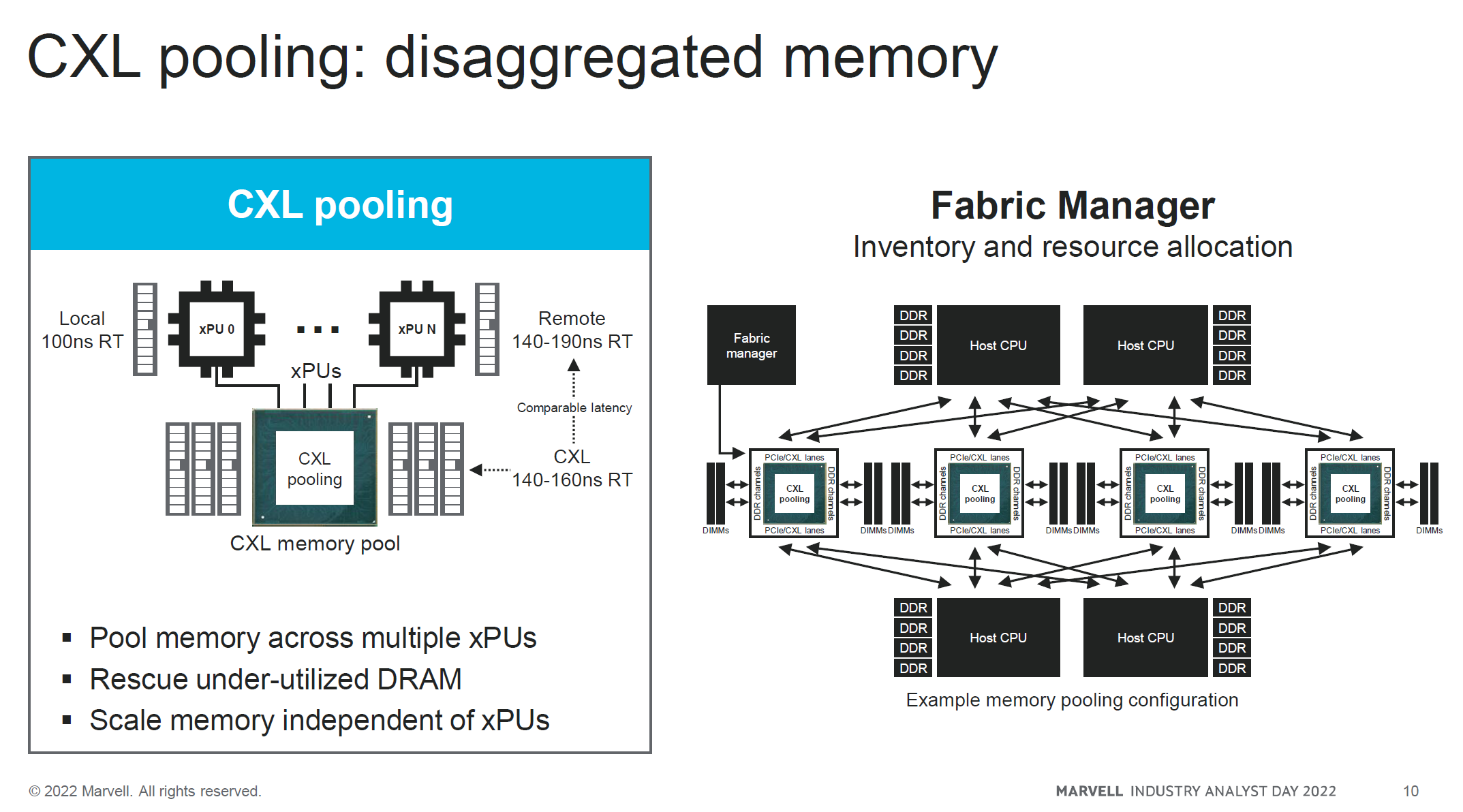

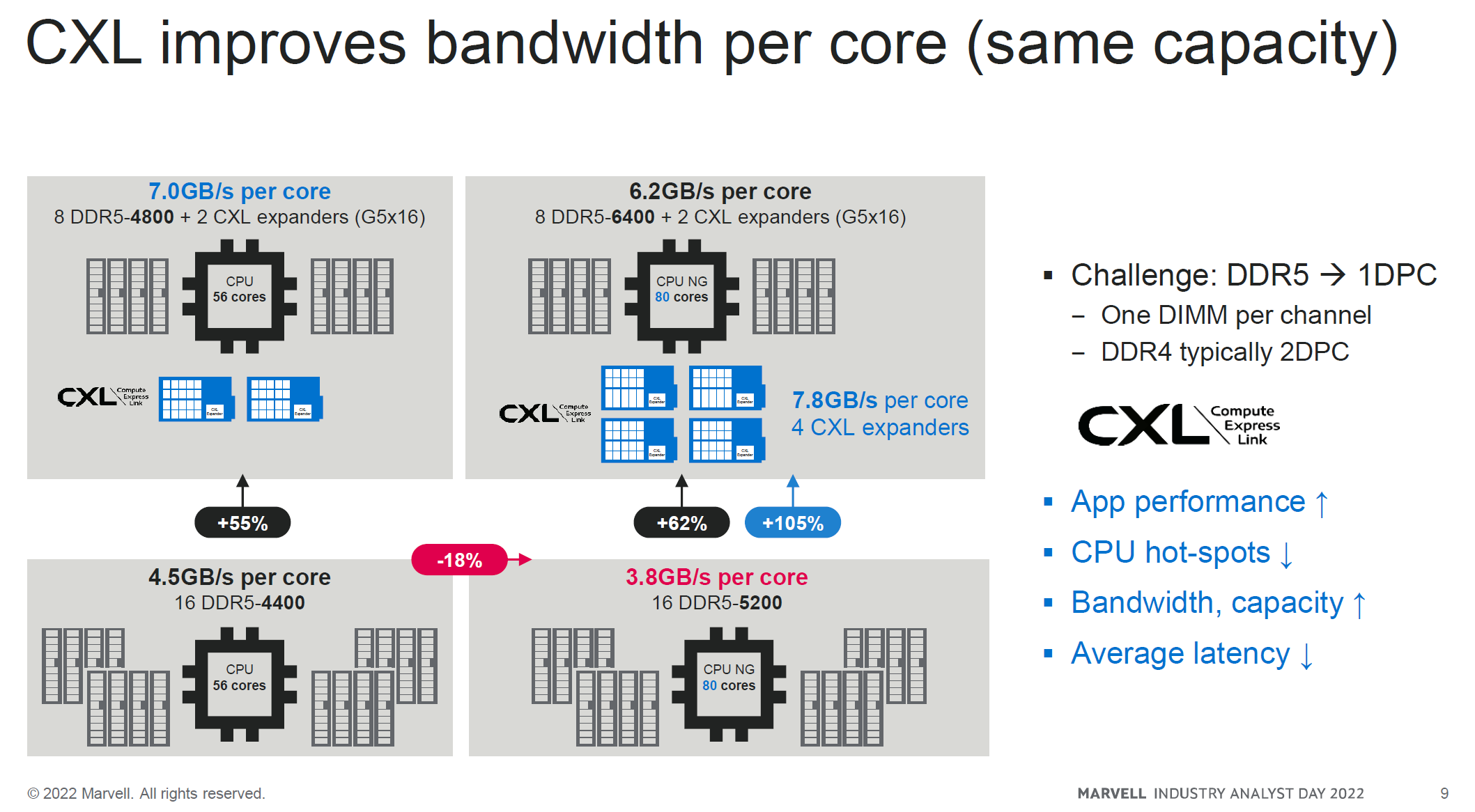

CXL and Storage Controllers

Marvell has an interesting play in CXL as well. I wrote a great primer about CXL here.

Marvell’s positioning in storage controllers gives them an interesting perspective to get into CXL. In particular, they want to make a memory pooling device that sits between CPUs for dynamic memory scaling.

The actual numbers are impressive, meaning there is more memory per core, better utilization, and average latency goes down despite the latency challenges of CXL.

It’s hard to size this opportunity for Marvell alone, as everyone wants a piece of this market. But clearly, their legacy positioning puts them on a front-row seat in this market.

DPUs - I’m Impressed

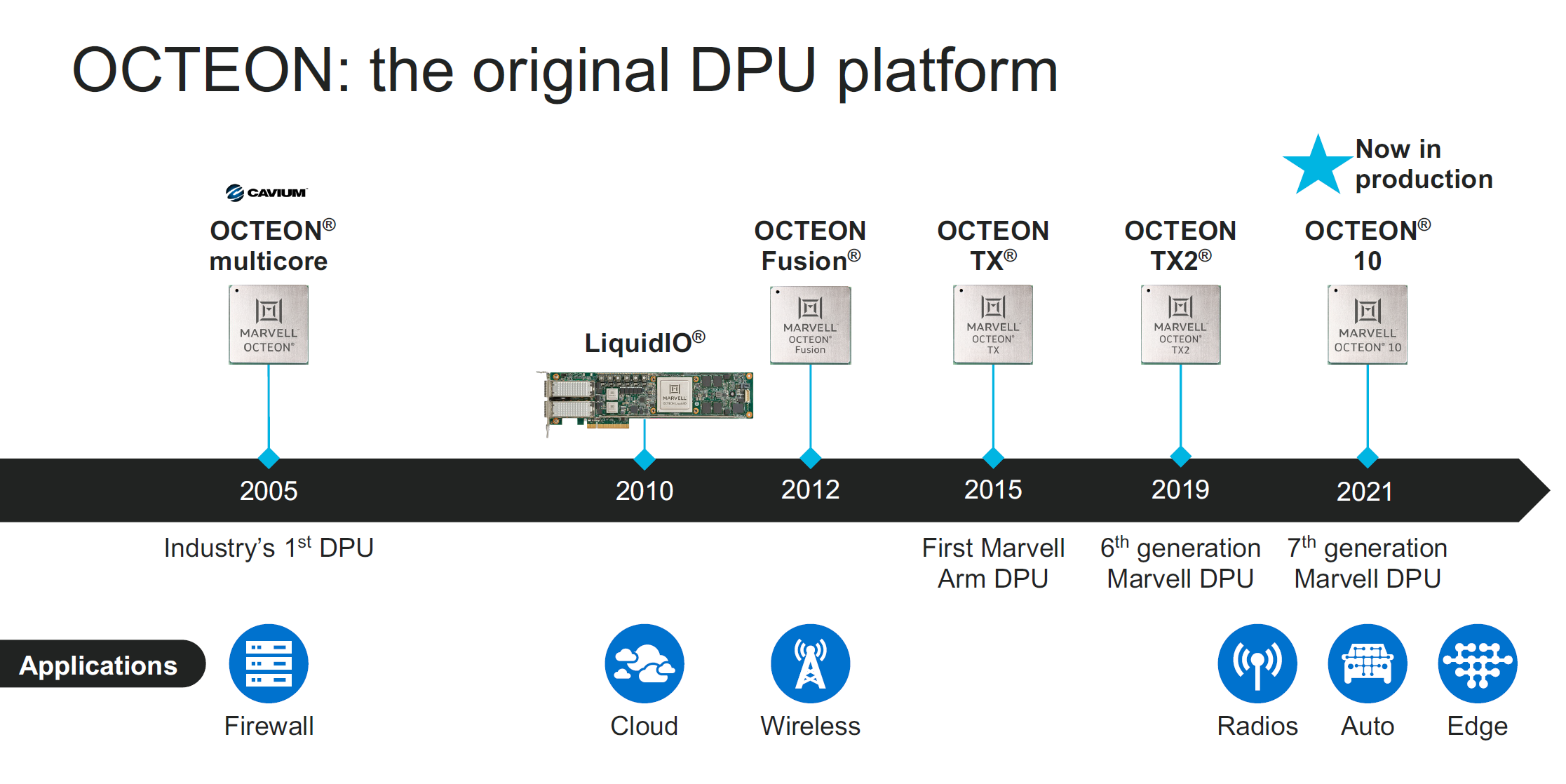

I think the most impressive product demo that logically seems to fit many parts of their portfolio was the DPU. A simplified overview of a DPU is as follows: its compute, accelerators, and high-speed interfaces into a single system on a chip.

Cavium was the maker of one the first DPUs, and today their Octeon and Fusion platforms are from the Cavium heritage.

Today's big DPU adoption is the Nokia Open RAN product ReefShark, which is taking share from the incumbents of 5G infrastructure. Additionally, one of the compelling parts of the Octeon platform is its multi-product offerings, with faster or slower SKUs depending on the energy and computing needs.

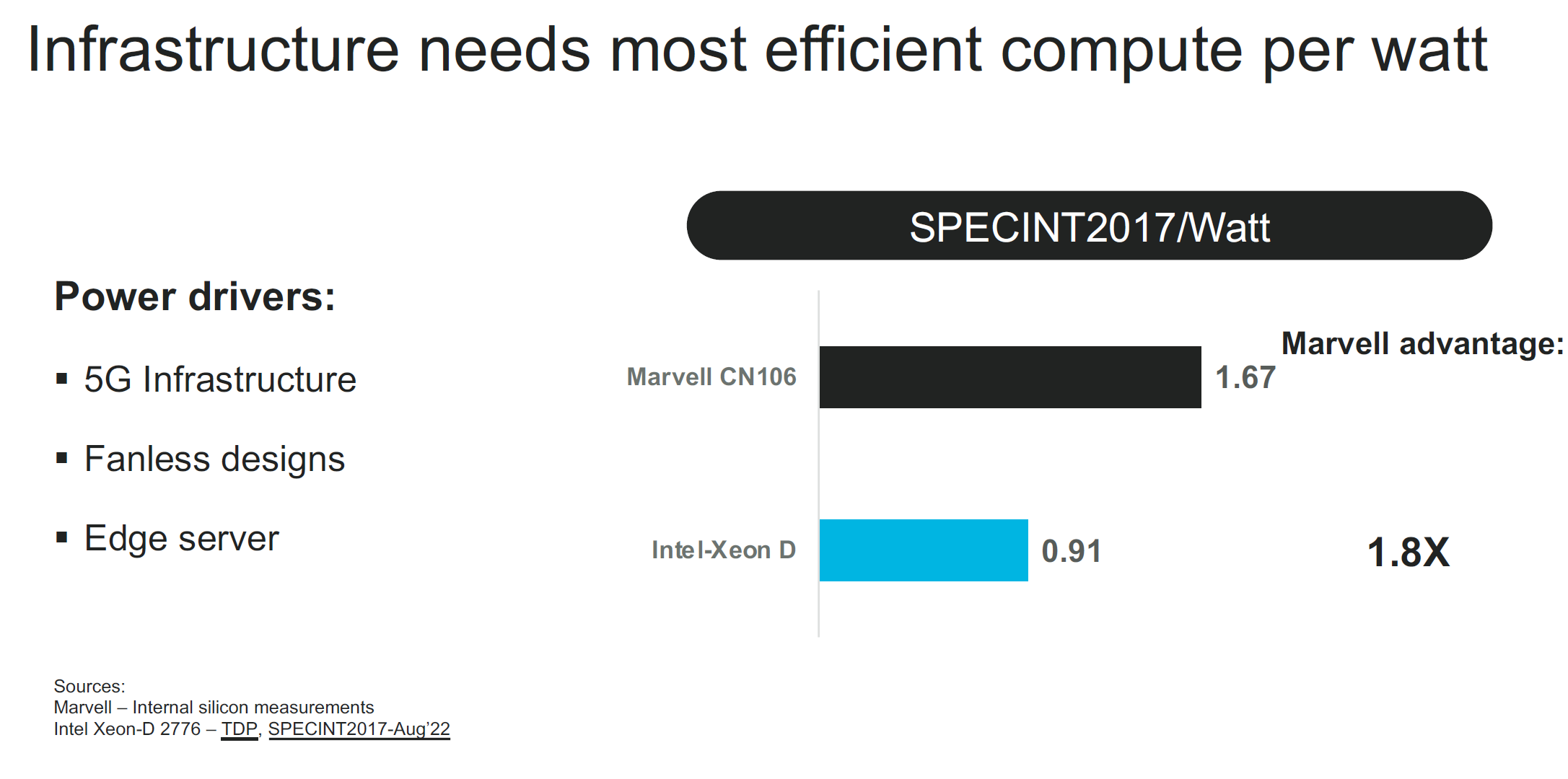

The Octeon is a high-speed chip well suited for networking edge, servers like PoPs, and firewalls. This solution crushes the competition, as Intel Xeons cannot keep up with the semi-custom solution that fits networking applications with a lower power envelope. They were putting up impressive SPECINT numbers in small energy envelopes of ~50 watts. The use cases scream edge computing.

The share gain stories here are still developing; for example, the huge need for content delivery networks to put servers near the edge in a small and energy-efficient platform seems almost ideally suited to Marvell’s Octeon family. And that product is only being considered today. Octeon’s lower power DPUs make them a perfect company to enable edge computing in all forms, from the radio unit in the cell towers to PoPs at CDNs, to firewalls at campuses. The Octeon DPU family is an absolute beast with a bright future ahead of it.

Concluding Thoughts

Marvell is an interesting company. I found the cohesive culture interesting and exciting when talking with the employees there. An analogy was a football team where a group of players who specialized in their markets could come together and be a much better cohesive team, and the misfits that each company would have been alone being more than the sum of its parts.

In theory, I agree. Cavium’s DPU, Aquantia’s ethernet, Inphi’s DSP, Innovium’s switch, and Marvell’s storage controller all come together to offer a compelling end-to-end networking platform. But something that is also hard to reconcile is that despite this, it’s hard to upset franchises in semiconductors. It’s a competitive market, and while I think all of these products are better together in the Marvell family, I can’t help but wonder if Marvell has acquired #2 in multiple markets. Of course, the #2 businesses will be on a firmer footing, but they are still #2.

Besides Inphi (my favorite), the legacy memory controllers (an okay business), and the DPU and HSM business, Marvell self-admittedly says they are #2 in many of the markets they compete in. That’s okay, but it feels different than the story they are trying to tell. And what matters then is the markets of tomorrow because that’s often how leadership is created, winning a big market early and then fighting for incumbency.

For Marvell, those markets are CXL, 5G infrastructure, and Automotive. They have acquired and have the technology to win these markets, but we will see if they end up the ultimate winners while defending their current #1 positions. I think they have a chance, and I’m excited to see if they are up to the task.

Additionally, at some point, I hope to do a model and a bit of a deeper dive into the financials. My high-level view is that compared to fabless peers (not AMD), they are “cheap” to Nvidia and expensive to Broadcom. They will do fine, but it’s not screaming a deal unless they meaningfully accelerate revenue.

That’s it for this week! Next, I will have a year-ahead outlook that is behind the paywall but will expire sometime in January for free readers who are interested.

Happy holidays if you don’t hear back from me; I wish you and your families an excellent end of the year!

Really good stuff. Thanks again for all you do