Micron and STMicroelectronics Investor Day

Secular growth opportunities but is it enough to justify a DCF?

Micron Investor Day

Micron’s Investor day talked about the longer-term bull case of memory, Micron’s positioning within memory, and, notably, the financial model and value of Micron. In addition, they gave their first cross cycle model and tried to highlight that Micron has a high replacement value.

Micron and Memory’s Longer Term Opportunities

Micron started the Investor day with a bull case for memory. Primarily driven by HPC and Datacenter, Micron believes that memory will grow to be a larger portion of spend as computing becomes more memory intensive.

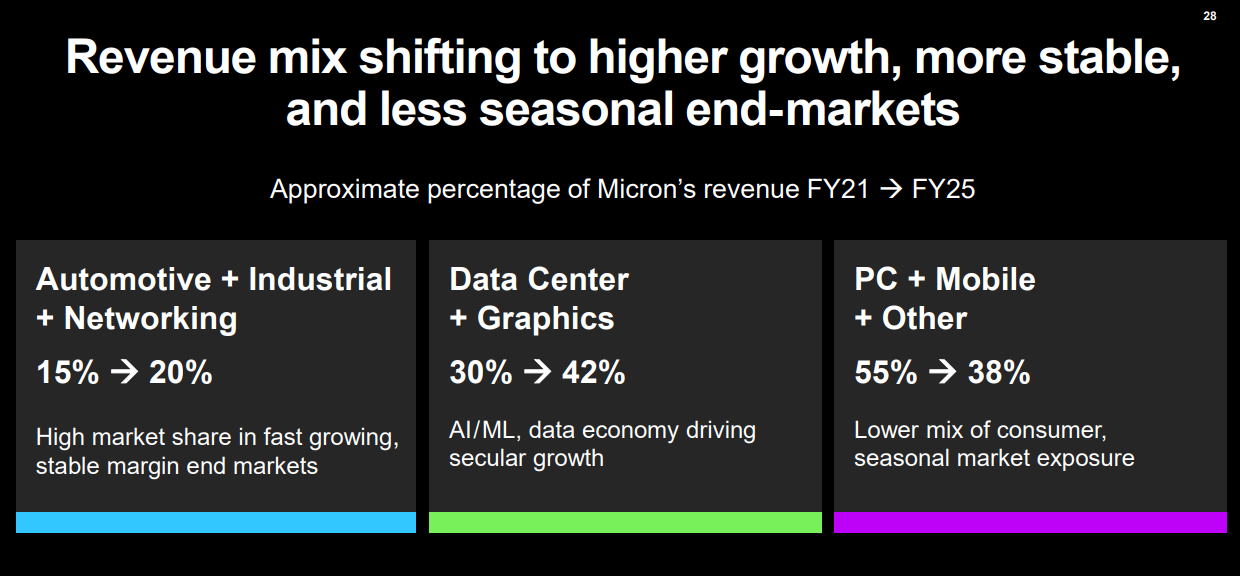

Micron believes they over-index to the faster-growing Automotive, Industrial, Networking, and Datacenter segments, especially compared to their peers. And as those faster-growing segments shift to higher parts of the mix, they believe they will become less cyclical.

Memory in the data center, in particular, is a huge winner, as larger models and DDR5 start to become a more significant portion of the pie.

They believe that they are well-positioned in HBM, DDR5, and importantly CXL memory. I will talk about CXL below.

So amid these growing and addressable markets, Micron believes they are well-positioned in the longer term as they have secular end markets. Importantly Micron also tried its best to highlight that they are improving its competitive positioning within this mix. This is driven by both technology and their margins.

The first technology they are introducing both 232-layer NAND and 1β DRAM well ahead of their competitors, and feel highly confident about the timing of EUV insertion in their DRAM roadmap. Micron has been at leadership nodes at either DRAM or NAND in the past, but this is the first time that both cylinders seem to be firing while their competitors are starting to misstep. Samsung, in particular, looks like the weakest link on the block.

Part of why they are starting to lead is their belief that they are shipping faster and better than their competitors. While competitors are struggling to ramp, they are reducing the cycle time to maturity of their newest nodes.

And in the capital intense and competitive world of memory, this matters a lot. The relentless pursuit of productivity means a real cost advantage over their competitors. This slide about $6 billion in capex reduced was interesting. In particular, they said their data capabilities and working with their suppliers have allowed them to get these kinds of cost reductions.

All of this is leading to Micron’s improving place in the ecosystem, as they have started to become not only cost leaders but believe they can drive their costs down faster than their competitors. But again, high single digits are faster than peers.

One of the best slides was how this translates to gross margins compared to their peers.

This brings us to the financial model. Micron hasn’t had the confidence to introduce a longer-term model, but the recent long-term agreements and improving financial profile lead them to give their first long-term model ever.

I want to translate their long-term guide to a valuation and take a rough stab at a DCF here. The results are not good enough to support the valuation, and I was favorable of their long-term FCF margin.

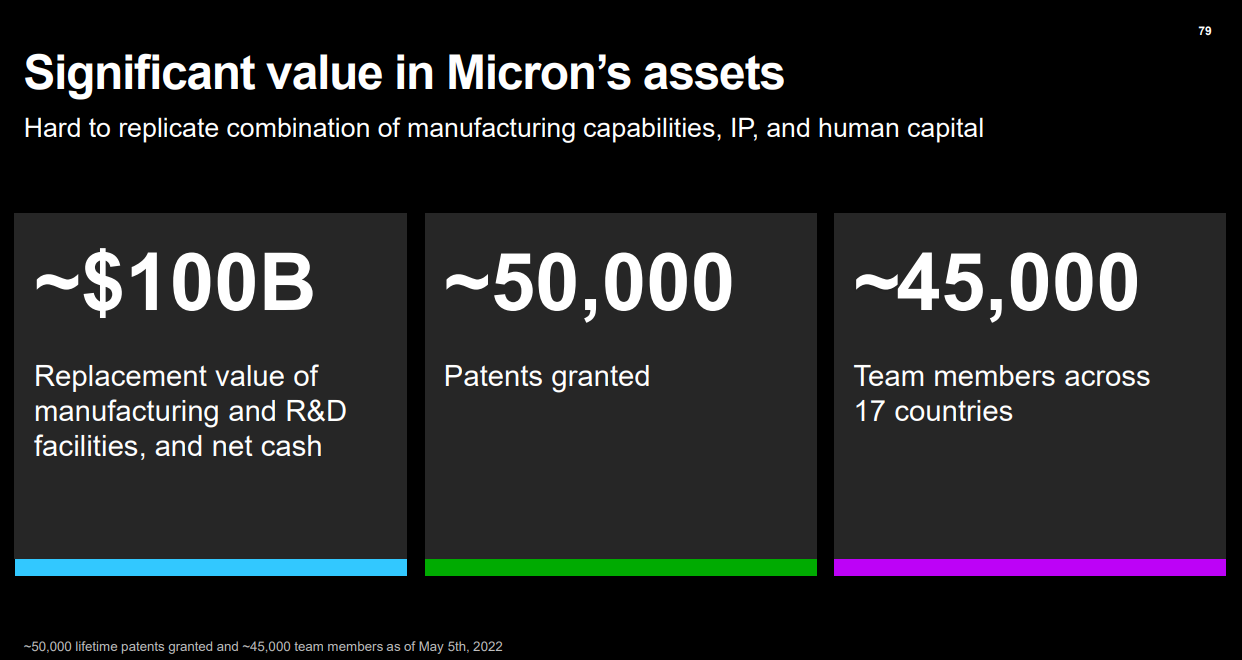

I think Micron still is expensive, and assuming this is their real mid-cycle earnings potential, I cannot get excited. The alternate valuation is something I thought was interesting and probably correct, but a replacement value from Micron’s management team themselves.

I think that the management team is correct; it would take something north of $100 billion to replace Micron, given their technology, processes, and scale. That being said, replacing that cash flow doesn’t mean it is attractive in its own right if it costs that much capital to sustain. At a lower price I’m interested, but stressing the strategic value doesn’t quite make sense to me at this time.

Long Term Agreements and CXL

Before we move on from Micron, I wanted to touch on two crucial areas in their investor day. First is the long-term agreement that felt like a watershed moment for the notoriously cyclical and commodity-like memory. If there ever was an argument to make about memory not being a commodity, the largest customers lining up for a direct long-term agreement is one of them.

While memory is technically a commodity like oil, with entirely interchangeable products, it isn’t relatively easy as spending money and then drilling on land you own. Moreover, a considerable engineering element only exists globally at the most significant 3-5 players. And given the recent shortages, the realization that not having access to this commodity would be dire. Hence the long-term agreements (LTA).

This is like airlines directly reaching out to Exxon for oil instead of purchasing it on the open market. This is a sea change and unlike what we’ve seen so far. The first largest customer is heavily implied to be a hyperscaler spending $500 million a year, and given their predictable end economics; it makes sense why they would do this deal.

The point is that the forward pricing agreements should help stabilize their cross-cycle margin.

I cannot express how pivotal this LTA is, and if Micron can establish more LTAs, I think this would be the ultimate feather in the cap of the new memory paradigm thesis.

The other thing I wanted to mention is CXL. CXL is very top of mind for this newsletter and is a nascent market that should become much larger in the coming years. I knew it was an opportunity, but this slide by Micron was eye-opening to me. That’s a ~60%+ CAGR from 2025 to 2030!

Refer to their whitepaper for a better technical primer on what exactly CXL is. But the gist is that CXL is decomposing compute into interoperable units with infinite plug-and-play scalability. In particular, this is compelling for hyperscalers, who have to scale large memory, compute, and accelerators into almost unlimited sizes.

CXL would let them skip the problems of “match sets” of GPUs, CPUs, and memory together. Instead, they could customize the need based on what is available, as truly elastic pools of each that can be composed for the task. This is heterogeneous computing at its finest.

Marvell, Micron, and many other players are highly interested in this quickly growing space. The problem is it’s pretty hard to get a pure bet on this trend. However, I think I found one - I think it’s worth reading these two pieces on Rambus in particular. The opportunity is massive, and while Rambus isn’t the best horse, it’s the purest play on this decade-long opportunity and trades at a discount to the entire semiconductor universe.

STMicro Investor Day

STMicro started their investor day with a highly bold long-term vision - and that’s a $20+ billion-dollar revenue target by 2026 (midpoint). The investor day was an exercise of showing how they will get there, driven by their automotive, analog, and microcontroller businesses. Their revenue guide is believable, but their FCF guide is doubtful.

First and foremost, STMicro’s greatest opportunity is likely the automotive segment. Additionally, they are one of the leaders of wideband gap semiconductor materials, such as GaN and SiC, that are sold into EVs.

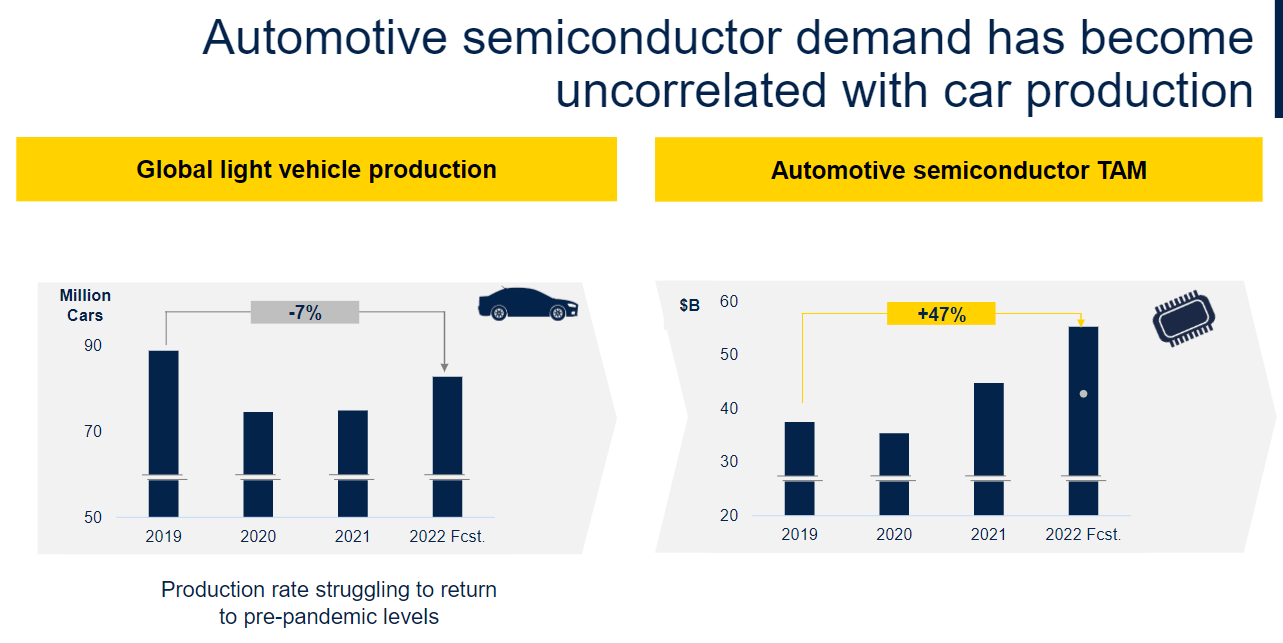

Something they mentioned that I now believe is that automotive content is far outpacing initial expectations, partially driven by the increasing cost of Semiconductors. Additionally, despite SAAR being down for over two years, automotive semiconductor sales have been up! This is primarily driven by higher content in newer cars, and I found this graph an elegant expression of this trend.

One of the biggest debates in automotive semiconductors right now is inventory builds. Is the above graph overstating the relationship between end demand and inventory build? While parts of the industry are likely building inventory, I still point to 2023-25 EU requirements for even more car content; this trend isn’t stopping anytime soon.

Even if there was a significant amount of inventory build, this is a massive confirmation of the content story that every investor should be expecting. The primary driver is content increases, not inventory building.

Compare this to my original expectation that EV would be an approximate double in content, looking more like 130% more dollar content. One could argue that the real difference is based on price increases, but I am starting to believe that, like most long-term TAM graphs for a genuinely secular market, they are underestimating the real end-market growth.

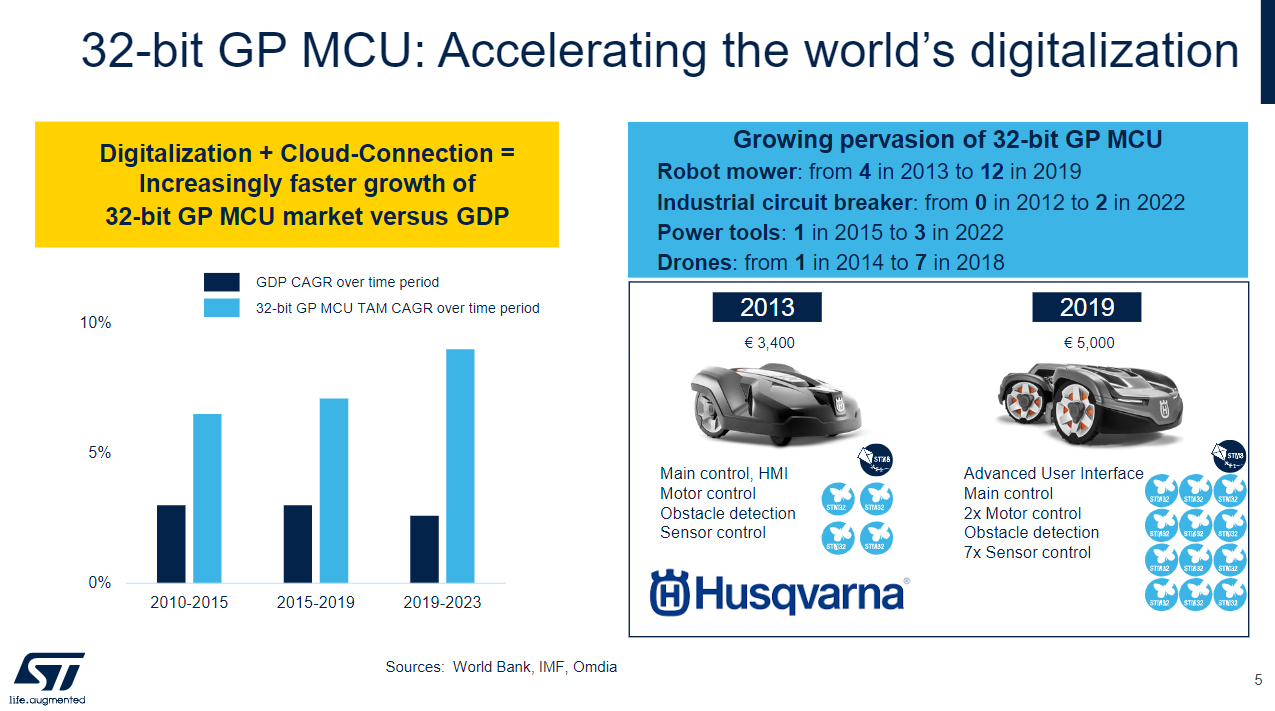

Outside of automotive, the business I found most compelling was the 32-bit MCU. One of the harder-to-qualify content gain stories is industrial and why the rest of the IoT space is growing so fast.

I think STM gave concrete examples of how MCUs are starting to become larger and larger portions of the pie. Products are just becoming smarter, and the increase of a power tool starting with just a motor controller to a battery controller and connectivity MCU is a perfect example of how content is tripling in the long tail of consumer products and other connected devices. The blue box shows some examples of content growth stories.

STMicro now brags that they are #1 in general-purpose MCUs, a historically competitive market, and a relatively undifferentiated market. Of course, part of this has to be the ability to get capacity in the shortage, but another aspect that I found compelling is their ecosystem support.

They talked quite a bit about STM32Cube, their developer-first strategy to give customers an accessible and programmable toolkit. I did a bit of sleuthing on GitHub and was pretty impressed. They have one complete developer kit, and the reviews don’t lie, with more stars than NXP, MCHP, and TXN combined. For an indicative comment, refer to this post in r/embedded, where one of the most upvoted comments about the most popular MCU family was STM32.

They are doing something right, and I think their concept that they will be selling higher-level products such as security, AI accelerators at the edge, and other add-ons starting from the MCU is correct.

It’s not Nvidia’s CUDA, but STM is making the right moves and has an ecosystem that helped them win their #1 share in MCUs. Of course, I don't expect them to start charging for the ecosystem, but this is yet another example of where software support is leading to hardware gains. Additionally, if STMCube can easily program wireless and other security functions, the land and expand strategy could work meaningfully in the coming years.

Last but not least I wanted to talk about wide-bandgap semiconductors, aka GaN and Silicon Carbide. STM was the first to this market famously with the Tesla SiC inverter win. And while they are not the leading the raw material additions like Wolfspeed, they have a significant internal source and are one of the leaders in the space.

I found these comments on Silicon Carbide interesting. They believe they can do ~$2 billion in SiC in 2026. Given that ON is expecting $1 billion run-rate revenue exiting 2023, this seems conservative, or they have lost a lot of market share.

I guess our charts are very explicit on that. Well, then Orio showed a chart to say between 2022 and 2025, we will multiply by 2.5 our capacity on silicon carbide. And I say that we plan to saturate this capacity. So the baseline is USD 700 million this year multiplied by 2.5. So you make your computation. So I don't want to hide ourself. I put the pressure on myself. But yes, $2 billion is clearly the target, the mission we have.

Despite all the hype about silicon carbide, they still believe that the absolute volume has not begun yet. Additionally, like most large growing markets, everyone is likely to undershoot the potential market size.

I think in some way, you are right in the sense that the silicon carbide in automotive in terms of volumes has not yet started. So all the car the Europeans will put in the market with silicon carbide are not yet in production today. So this will come in the next, let's say, 5 to 10 years. So for sure, the ambition to grow on silicon carbide is there. You see we are preparing ourselves in capacity for MOSFET in substrates to fulfill the need. We don't want to give unrealistic targets also because we have to say material is still a bottleneck today. But for sure, we are a strong believer of silicon carbide.

We think silicon carbide will evolve much more than what we think today. I think we will go more on top of the automotive, also in industrial, even on consumer. I think the next one will be GaN because part of GaN, when we'll be solid in production, will take also part of silicon carbide. But again, we don't want to be, let's say, unrealistic in giving numbers. We'll not go in numbers over the $1 billion that we are telling you today. But I am with you. The expectation for silicon carbide is probably much bigger than what we think today. And frankly, we are prepared to fulfill these volumes.

I believe the revenue goal looks highly attainable between Silicon Carbide, a growing MCU business, and continued strength in MEMs and other products. So let’s translate that into financials.

Valuation

Last but not least, let’s try to get a handle on their long-term guidance and what that implies for STMicro’s stock. Let’s try to back out of the long-term guidance posted below.

If we take their IR day at face value, this company is screamingly cheap. The discount rate to make $2.5 billion exit PV work is a 20%+ CAGR. The problem is I don’t believe that FCF Margin. Let me explain.

The problem here, in my opinion, is that they have never, and probably will never, achieve that FCF margin of 25%. I would like to see it, but it would be multiples higher than their peak margin in 2021.

Luckily I think you can make the stock work in a DCF with a much less heroic 17% FCF margin, and given how much their margins have expanded recently it’s a stretch but it’s possible.

The entire story hinges on this singular point. I believe that they likely can put up the revenue growth, and they probably can maintain and improve gross margins, but I want to see it convert into FCF, and then I’m a believer. But at a price and for what it is, I think STMicro put out a compelling vision of the future that you can underwrite, unlike Micron. A 17% end-state FCF margin would align with the likes of ON, IFX (~14% ‘21), and the analog companies.

It’s possible, and a 15-17% FCF margin guide feels doable, and the stock would be undervalued from this perspective. However, it’s worth looking into the story more at this price. If you found this helpful, consider subscribing. I put a lot of work into my posts, and I hope you enjoy them.

That’s it for this week, folks. I’m going to try to get to Cisco and Applied Materials soon, and then a discussion of data center lapping in the second half of 2022 later. Ciao!

I work in electronics design and manufacturing. STM32 MCUs are impossible to buy at the moment, have been for the last year, and probably will be for the next too (unless you are a Tier 1 like Apple). This has caused an interesting effect; everyone is designing out STM32 parts as fast as possible, and not even considering them for new builds. Instead, they are being replaced by Chinese grown MCUs that are “clones” of STM32s like the gigadevice GD32 or Geehy APM32, as well as the more well known Espressif ESP32 which seems to be relatively available on the market.

And truthfully, the reason STM32s are the number 1 MCU is not the software libraries, which were awful and buggy for the first 5-10 years - they actually made development slower than programming on a register level. The real reason is that they were cheap with lots of peripherals and relatively abundant; ST also pioneered the low cost evaluation kit where you could buy an MCU dev kit for $20 instead of $2000 which was unheard of at the time. This caused the low end of the market to standardise on them. Since hobbyists, universities and engineers playing with their first ARM MCU were all using STM32, you could basically assume that anyone who applied for a job in embedded systems had some experience with them. And because it is what everyone had experience with, that is what they chose for their designs. Other vendors later followed with cheap dev kits, but it was too late.

Unless ST can solve its supply problems soon, I think they will begin to see their market shrink from the low cost end. They probably won’t care about this initially as it would hardly register in their profits, but in the long term the general knowledge base of everyone will be moving away from their devices (and to some extent, already is), giving mindshare and revenue to their competitors like Gigadevice, Nordic and Espressif and allowing them to grow.