Micron's Guide and Global Foundries Investor Day and other Earnings (AOSL, ICHR, ONTO, POWI, 8035, HIMX)

HIMX is another victim of NCNRs, GFS talks about LTAs and their positioning, and what does Micron's negative FCF imply for Earnings?

Micron guided down revenue and earnings 40 days after reporting last quarter's results. This guide down is a big deal, as Memory is used in every end market within semiconductors. The Memory market so far looked like it was holding up, but the sudden weakening of Memory is the ultimate tell that we will be entering an inventory cycle quickly.

There are a few important things they said

Broadening of customer inventory adjustments

FQ4 revenue is below the low end of the guidance

The sequential decline in revenue and gross margin

Negative FCF in FQ1

Reducing WFE spending for 2023. “Down meaningfully versus FY22.”

In particular, some of the specific things they said on the call were telling. End market weakness is now spreading.

But actually, in the quarter here that we're in, the August quarter, it's broadened and actually weakened more. We're seeing inventory adjustments across most end markets. That includes the cloud.

Now the cloud is a bit of a unique case because we still see strong end market demand. So cloud adjustments are likely just customers taking stock of the macro uncertainty, maybe the market conditions, and thus adjusting their inventory levels down. We do see some isolated supply chain disruptions affecting cloud as well, but it's principally macro and market conditions, inventory adjustment.

We're also beginning to see some inventory adjustments occurring in automotive and industrial markets. And so that's beginning, and we'd expect that to continue through this quarter and into our first quarter. And then, of course, we see PC and smartphone and enterprise continue to be weak.

PC and smartphones are getting worse.

We see even more weakening in smartphone and PC. I can't say it's the most intense weakening we've seen, but we are seeing weakening. And we're certainly seeing broader weakening.

They also talked about the nature of the LTAs. They are not take-or-pays akin to the NCNRs rocking Qorvo, Himax, and Nvidia. They are, however, formal arrangements with their customers. Lastly, they talked about inventory. They will be going through 150 days of inventory.

Well, just one comment on inventory I'd like to make. So we had talked about 150 days as kind of a point that would be a sort of a high level for a down cycle period, and I think we're going to be through that in the first quarter. I mean I -- we modeled to be through it at the moment given this -- what you saw in the 8-K this morning. So you can expect our inventory levels to be up. But again, for -- because it's advanced technology, inventories, for the reasons Farhan mentioned on cost downs, we believe it's a prudent decision given circumstances.

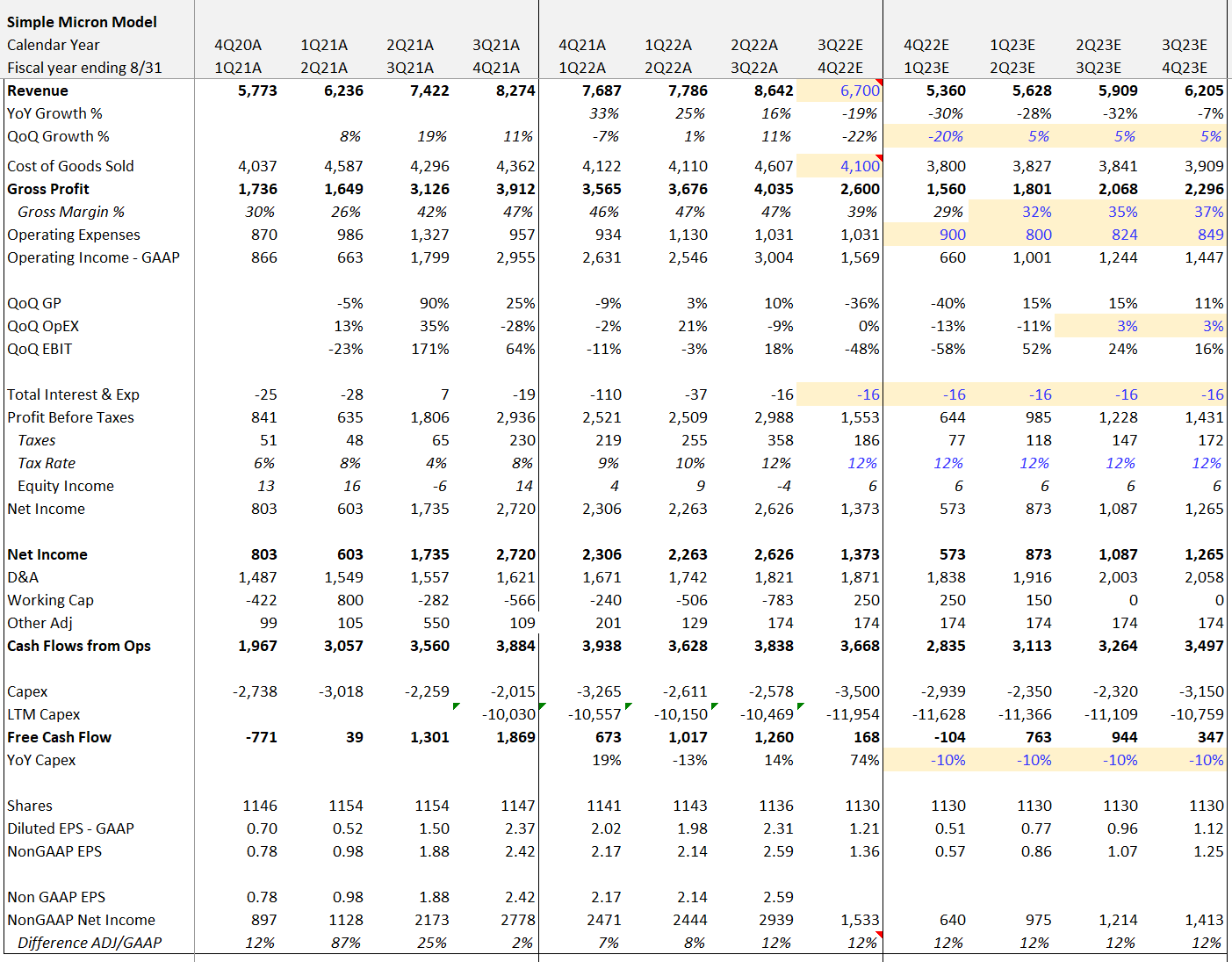

I’m going to take a quick stab at modeling what this means. But, first, let’s try to get to a negative FCF in 1Q2023.

For me to get to a negative FCF in 1Q23, revenue growth has to go down 20% sequentially twice, and gross profit gets cut by over half. I took a stab at modeling, and the numbers don’t look great. It’s tough to know what Micron gets out of the trough-like, but I felt that I was conservative on the gross margin improvement out of a 1Q23 trough. So here’s my simple model.

The model result is ~$3.75 in Non-GAAP EPS or ~17x earnings. Before you go screaming that it must be the end of times, I want readers to think that maybe it’s an excellent time to buy the stock. Usually, when the earnings contract and Micron becomes a high P/E stock, it’s probably time to start buying.

Semiconductor stocks tend to bottom 2-3 quarters before the actual bottom, and if we mark their next quarter as the beginning of a QoQ decline, Micron rarely has more than three-quarters of contraction, especially if there’s a -20% QoQ result. That means the best time to buy is right now. I highly advise you to look at the history of QoQ declines in the attached spreadsheet.

Below is my model, and I recommend you adjust it yourself. Maybe also flip through to the QoQ tab and look at the historical results of Micron. I highlighted in grey recessionary periods so you can look for yourself to see what a typical contraction looks like.

The world is not ending, the trough is likely in sight if this is the first quarter-on-quarter contraction, and the bottom for the fundamentals is within a year, and the bottom of the stock could be right now. It’s hard to know - but the worst for the stock is likely behind us.