Mobileye S-1 Teardown

I can't help ask: Why now? It does look priced to pop.

The Mobileye S-1 just dropped, and I want to write a short overview of Mobileye, their opportunity, and some thoughts about Intel in relationship with Mobileye. I wrote about Mobileye briefly when they were rumored to go public with a ~50 billion dollar market cap in December of 2021. The math is very different now. Mobileye is a much smaller offering and at a much smaller valuation, but there’s probably a good reason for that.

I’m first going to discuss Mobileye, the company, talk about their links to 2 very important companies (STMicro and Intel) and then discuss what I think about the overall offering. Strap in.

A Brief Overview of Mobileye

Mobileye is the leader in hardware solutions for ADAS systems in cars. They have a few potential products, but EyeQ (95%+ of revenue) is the big one. I must mention the other parts of the business that could be large tomorrow but are small today. Those are Road Experience Management (REM), RSS (not going to be a business but important), and Moovit.

EyeQ - The Leader in ADAS SoCs

Mobileye today is this single business. 95% of revenue is from a single product, the EyeQ system on chip (SoC). While this might make some investors nervous, I think the number of design wins across many OEMs should give some respite. Mobileye is the incumbent in all ADAS technology today and has likely shipped the most ADAS SoCs to date. Every car with a front-facing sensor, auto-breaking, or lane assist likely uses an EyeQ module by Mobileye.

Their OEM list is essentially every car company. And the net number of SoCs shipped over the years is impressive. That number is starting to accelerate meaningfully as the adoption curve of L3-L4 continues. A friendly reminder below what each level of ADAS means.

The increasing levels of automation require more silicon content per level, and ADAS is still only a small part of the total cars shipped annually. So, of course, Mobileye is shipping a lot of EyeQ chips. Below are their annual units sold.

That’s a lot of EyeQ SoCs. That is now more EyeQ SoCs sold annually than cars sold, and that’s because the higher levels of ADAS vehicles require more EyeQ modules per car. For example, the Mobileye Chauffeur, their level 4 solution, requires EyeQ 5 High SoCs.

Mobileye Chauffeur’s™ first generation solution will be based on six EyeQ®5 High SoCs, and the next generation will be powered by one EyeQ Ultra™, our AV-on-Chip. It will combine our leading computer vision camera-based perception subsystem with a radar-lidar subsystem.

But notice the different SKUs of EyeQ, from EyeQ 3 to EyeQ Ultra. This brings me to the part I want to talk about, Mobileye, and that’s its comprehensive roadmap from L2 to L5.

Mobileye has a very opinionated and defined forward and backward-compatible solution for ADAS. When they are designed for L2 products, the step-up to L3 and L4 is just more EyeQ SoCs and a few more sensors. As far as I know, I don’t think any other company has enunciated such a well-defined roadmap.

This is great for a car OEM. If they want to offer an ADAS-lite product, with only smart braking, lane control, and highway L3, they can sell the same model with a much cheaper chip. Meanwhile, they could likely upgrade that exact same model to a full L4 solution with just a higher level of semiconductor content. The car OEMs are free to choose what differentiation they want to offer.

Additionally, Mobileye is positioned for both a consumer autonomous vehicle (AV) and autonomous mobility as a service (AMaaS) future. In part, they can sell full consumer AV to the car OEMs or eventually sell AMaaS through Moovit, their internally owned platform.

It’s unsure what the actual outcome of AV looks like, but Mobileye likely will be some part of it, given their current incumbency and positioning. I want to move on to their other products and significant services more than the hardware. First REM.

Road Experience Management (REM)

This is an interesting segment. REM is a bottoms-up mapping initiative by Mobileye. Given Mobileye’s large installed base of computer vision sensors already, they can collect snippets of data from the installed base and create a bottoms-up “ground truth” map similar to Waymo. The difference is that Mobileye is passively collecting this data.

Additionally, we have created a separate dataset of 8.6 billion miles of roads driven as of July 2, 2022 from, based on our estimates, approximately 1.5 million REM™-enabled vehicles worldwide. We then apply a series of on-cloud algorithms to build this crowd-sourced data into a high-definition, rapidly updating map that contains a rich variety of information, including road geometry, drivable paths, common speeds, right-of-way, and traffic light-to-lane associations. We estimate that the data we have accumulated covers over 90% and 80% of the approximately 0.8 million miles of motorway, trunk, and primary road types in each of the United States and Europe, respectively.

I don’t believe their primary goal is to sell this as a service to customers but rather to give themselves the dataset to continue to improve their models and training to hit full level 5 autonomous driving. While they are likely not the leader, they will be able to be competitive each year as they collect more data.

Also, as their installed base grows with more EyeQ SoCs, their data collection grows. There’s a huge benefit from this kind of incumbency.

RSS (Responsibility-Sensitive Safety)

This is not exactly a product but rather an interesting regulation standard and mathematical AV model to prevent crashes. Think of it like a formalized logic system that AV cars will adhere to. It considers driving with AVs and humans together and creates a formal car-to-car rule system. By contemplating the problems of what that future will be like today, Mobileye further encourages incumbency.

Imagine a world where a standard for AV car-to-car logic is regulated, and let’s say its spearheaded by the EU in turn, chooses something akin to RSS. That would be a huge incumbency advantage that would confer incumbency in the AV space. I think that’s the play here.

There are competing products, most notably Nvidia’s SFF standard. But in my opinion, Mobileye’s logic system seems a bit more complete and thought out.

Moovit

Moovit is an interesting piece. Moovit is similar to Waze, which is a non-Google Maps transportation app. Put in where you’re going and where you are, and it’ll link a route based on public transport or driving. It, of course, is popular primarily in Israel.

In some South American countries, it’s similarly sized to Waze but much smaller than the behemoth Google Maps.

The interesting part is that Moovit likely makes zero revenue today. Still, if Mobileye was first to AMaaS as a service, they would already have a UI to roll out their service that likely is at scale to support the service. Moovit is their call option to offer AMaaS as a service. It’s long-dated and seems unlikely today, so that’s all I’ll mention for now. Time to discuss financials.

Financials

Let’s now turn to the financials. I think the simple way to look at Mobileye is price and quantity. First, let’s talk about units increasing as a percentage of global SAAR. We should expect this number to outpace SAAR as they move from 1 to multiple EyeQ SoCs per car.

The total number of units ramping is interesting to me. And if you look closer at their disclosures, I found this interesting.

We estimate, based on our existing design wins through July 2, 2022, that our ADAS solutions will be deployed in more than an additional 266 million vehicles by 2030, including approximately 37 million vehicles based on our first half 2022 design wins and approximately 50 million vehicles based on our 2021 design wins

That implies ~31 million cars a year and likely more than one EyeQ SoC in the out-years. Assuming 3 EyeQ SoCs on average, ~35 million peak cars (it ramps to that number) in 2027, and an ASP of $30 (assume ASP erosion) puts a ~3 billion+ revenue target as a potential. Comparing that to $1.7 billion in revenue in 2022, that’s only a 12% revenue CAGR. So either there needs to be more units (probable), higher ASP (also possible), or more cars (possible).

My rough range of outcomes based on the current design win trajectory and the implied revenue CAGR is below. The assumptions are at the high-end Mobileye wins it all, and on the low-end, Mobileye loses a lot of share but relies on design wins.

It’s likely the ride is a bit bumpier, the SoC ASP is a bit lower, and many other things that are harder to make happen in reality come to fruition. Competition is really heating up, and there are zero long-term agreements, so reality could happen anywhere between those very wide CAGRs. However, that’s a compelling revenue CAGR based on their current design win cadence (double digits). The next thing I want to talk about is ASP.

ASP in 2022 increased but fell in 2021 from 2020. This doesn’t make any sense to me - given the broad-based price increases the entire industry saw during this time period. I think what is happening here is that the higher-end SoCs are starting to ship in higher volumes and thus bring ASPs up on average.

Meanwhile, the company talks about having a full L5 autonomous solution for “less than 6,000 dollars”. At today’s ASP and an average of 1-2 SoCs, that seems like a 60x content increase. That math doesn’t make sense to me. I don’t know what the difference is, but given the language in the filing, it seems that they will be selling a lot more than just EyeQ SoCs in the future.

Our solutions have different margin profiles. As we develop, bundle, and sell full systems that include third-party hardware beyond EyeQ®, we expect that our gross margin will decrease on a percentage basis because of the greater third-party hardware content.

Anyways I want to move to the actual financials. For a company as dominant as Mobileye, I am not that impressed with the profitability of its revenue base. I think a big part of the equation is that Mobileye has been spending massively in growth opex under the Intel umbrella. Check out the simplified income statement below.

A ~50% gross profit margin, yet 0% operating margins. Talk about heavy reinvestment! But it looks like the days of operating losses are over. They are starting to scale profitably, and I expect them to hit positive GAAP operating income and likely much more profitable Non-GAAP operating profit. Let’s now move to the cash flow statement.

I’m kind of impressed they are free cash flow positive! The big driver of that cash profitability is the amortization of intangibles, particularly the Moovit transaction and other IP. They are fabless, so they have very little net capex needs.

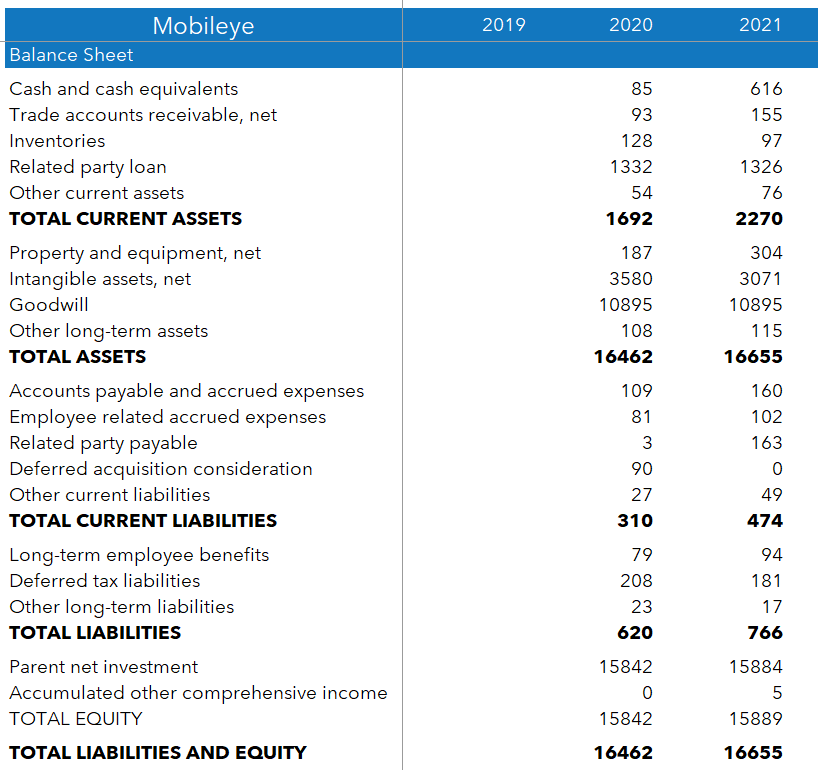

Now it’s time for the balance sheet. It’s vanilla.

The balance sheet has no debt (except the potential dividend note). I think post-offering the dividend note will be the only debt on the capital structure. And that should be paid down with follow-on offerings. Last I want to do some valuation work.

I made a simple comp sheet, including Wolfspeed, which almost always breaks every comp sheet with their negative EPS and 100x EBITDA multiples. That being said, Mobileye looks fairly valued from this perspective.

Here’s a comp sheet not including Wolfspeed, and I think this makes Mobileye look overvalued. That said, next year's biggest what-if is revenue growth, which I think will be a bit more agnostic to market growth than other automotive companies. Mobileye likely deserves a premium to Automotive semiconductor companies, but a 100% premium on EV/EBITDA and P/E seems steep.

Mobileye is a larger participant in ramping legislative safety protocols and penetration than total SAAR, and I think that even in a bad year, the company should be able to grow. How much? Who knows - they haven’t put out any kind of guidance yet.

I still think the shares will pop regardless, and that’s mostly on the float dynamics. Refer below to the IPO statistics.

Notice that only ~7% of the float will be available, and it’s widely known that most of the offering is locked in with large institutions (Ballie Gifford) and Amnon (40 million) himself. Put differently, there’s very little supply, and there should be some demand. The result is a very obvious day-one pop.

Important Relationships (STMicro and Intel)

I would be remiss to talk about two very important companies to Mobileye. I have to mention STMicroelectronics first because I find this relationship so interesting.

STMicro does part of the design, packaging, and testing for Mobileye. STMicro uses TSMC as the fab but effectively does the entire backend packaging for Mobileye. I don’t understand why and I have to imagine that this business is margin decretive for STMicro, but they continue to be an important part of the company’s roadmap.

STMicro also seems like it will not be designed anytime soon. I don’t understand the nature of this relationship, but given that Mobileye was owned by one of the largest potential foundries in the world, I think if STMicro could have been designed out, they would have been already.

We have co-developed seven generations of our automotive grade SoC, EyeQ®, with STMicroelectronics including EyeQ®5, EyeQ®6 and EyeQ Ultra™. We design the front-end and STMicroelectronics designs the back-end package and also includes testing, quality assurance, customer care, failure analysis and manufacturing standards. All of our EyeQ® integrated circuits are manufactured by or outsourced to a partner foundry by STMicroelectronics.

STMicro’s relationship will likely continue until at least 2025, given they helped design the EyeQ ultra.

Intel

Intel’s relationship with Mobileye is pretty odd. Despite the close coupling of the two businesses for the past five years, there doesn’t seem like much interlinkage beyond some IP, photonics packaging, and FMCW lidar. These are important, but I feel like they are secondary to STMicro’s deep involvement.

There are plans to integrate EyeQ with Intel and use Intel Foundry services in the future for advanced packaging. However, this is yet to be seen. From a financial perspective, I want to focus on the specifics of the Intel and Mobileye listing, starting with the dividend note.

I think most of Twitter has mischaracterized the note. Most people have read the S-1 and view the note as a 1-way debt of Mobileye to Intel for $3.5 billion dollars over the next three years, meaningfully ruining the firm's Free Cash Flow to equity. I understand how at first glance, it reads like this.

In connection with the Reorganization, on April 21, 2022, we distributed to Intel the Dividend Note, a promissory note pursuant to which Cyclops Holdings Corporation, which will be one of our consolidated subsidiaries following the completion of the Reorganization, agreed to pay Intel an aggregate principal amount of $3.5 billion. The Dividend Note is scheduled to mature on April 21, 2025 and accrues interest at a rate equal to 1.26% per annum, such interest to accrue quarterly.

However, if I’m reading this correctly, it looks like this is just an amount that Intel wants to recapture from the listing over the next few years.

Intel informed us that it intends to contribute to Mobileye Global Inc. any remaining portion of the Dividend Note in excess of such repayment prior to the completion of this offering, so that no amounts under the Dividend Note would remain owed by us to Intel after the completion of this offering and such repayment. Under the terms of the Master Transaction Agreement we will enter into with Intel in connection with this offering, immediately after completion of this offering and on a pro forma basis after all expenses of this offering have been paid

I’m reading this because Intel wants to get $3.5 billion in cash from Mobileye over the following years, and once they hit this amount, the proceeds will start to accrue to Mobileye. Think of the dividend note as an “I owe you.” The dollar amount is the planned amount of equity follow-ons. Given the implied ~$15-20 billion dollar valuation, this is another ~17.5% of the company.

Something else I found kind of odd is that Mobileye is getting its independence unless the amount is over $250 million. Any capital allocation decision (equity issuance, debt, capital expenditures) over $250 million has to be approved by the board, aka Intel. I thought this number was arbitrary, but given their absolute capital size, this seems like a hurdle Mobileye is unlikely to hit.

Last but not least, I mentioned above that the low float dynamics seem to make this offering priced to pop. I think that’s primarily for some good news for Intel, and that way, Intel can continue with follow-ons until it hits the 80.1% ownership number stated in the Master Transaction Agreement. Intel is trying to reserve its optionality by floating Mobileye today and then doing follow-ons later. That makes sense to me.

Offering Thoughts

I cannot help but think that this offering feels very desperate in timing. This has to be one of the worst windows for Intel to list Mobileye. We are days from the year's low, so why would they do this offering right now? I understand that five years is when the spinoff becomes more tax efficient, but they could wait until markets rebound slightly. So why now?

Two things come to mind. First, the IPO is extremely rigged to pop with low float dynamics. Similar to Global Foundries but with even more extreme float dynamics. This clearly would be some “good news” for Intel, something Intel could desperately need.

The second thing that makes me wonder is the timing. The price date is October 25th, and Intel’s earnings will be on October 27th. I have written some massively negative things about Intel as of late, given PC shipments. Are they trying to get some good news before very dismal earnings? I think so.

I think that Intel feels desperate about this raise. Why do they need $900 million this desperately right now? I understand giving the Mobileye employees their own stock incentivizes them, but if Intel had any kind of leash, they could wait for a better window. I think the cash burn of a weakening economy and massive Capex needs to catch up are coming to a head, and Intel feels desperate.

That being said - I think Mobileye itself is awesomely positioned. The company has been on my radar for a long time as a potentially great stock, and when they initially announced a $50 billion dollar valuation, I was very disappointed. $15-20 billion looks much more reasonable, but the stock will pop on a very small float, likely inflating the valuation to higher.

This allows intel to have follow-on offerings, and I think the optionality here is very smart. Low float pop, followed by offerings as the shares do well. Meanwhile, they will eventually get $3.5 billion in cash proceeds from Mobileye, all while maintaining effective control. The only problem is the timing feels desperate.

Risks and Concerns, Other Tid-Bits

The big risk is in-housing by automotive OEMs and competition. Mobileye is already such a large incumbent for ADAS solutions, any incremental in-housing will negatively impact them. This risk item is the big one.

OEMs who have or are pursuing their own in-house solutions are also indirect competitors, with Tesla and Mercedes-Benz being examples of automakers taking that approach today, with others such as General Motors, NIO, Volvo Cars, and Xpeng Motors also pursuing in-house solutions for portions of the ADAS software stack. In the future, our indirect competitors could become direct competitors.

The thing that is more worrying is that Mobileye is the incumbent, and almost any incremental “design win” you hear from Nvidia’s Orin or Qualcomm’s Snapdragon has to come partially at the expense of Mobileye.

Amazon Web Services Bill

I thought their absolute spending at Amazon Web Services was curious. Most of the spending was for REM and Moovit, but the number seems large for a business with substantially zero revenue today. In 2021 and 2022, the company incurred increased R&D costs of 20 and 21 million dollars, mostly in Cloud computing expenses. That’s a hefty AWS bill. 👀

No Long Term Price Agreements with STMicro, Reliance on Third Parties

In addition, our contractual relationship with STMicroelectronics does not provide us with long-term pricing or quantity guarantees, and both we and STMicroelectronics are free to terminate the arrangement at any time. Further, we are vulnerable to the risk that STMicroelectronics may be unable to meet demand for our EyeQ® SoCs or cease operations altogether.

Kind of crazy for a company that manufactures all your products. Additionally, they rely on Quanta to make ECUs for the larger hardware ecosystem they are trying to provide. Mobileye has a curious partnership pattern, in my opinion.

We have also established a relationship with Quanta Computer to develop and assemble our ECUs including our reference design for our Mobileye SuperVision™ solution, which includes our EyeQ®5 SoCs from STMicroelectronics.

Significant Concentration of Suppliers and Customers with no long term agreements

In 2021, our three largest Tier 1 customers, who were ZF, Valeo, and Aptiv, accounted for 35%, 19%, and 17%, respectively, of our revenue. For the six months ended July 2, 2022, our three largest Tier 1 customers, who were ZF, Valeo, and Aptiv, accounted for 43%, 15%, and 15%, respectively, of our revenue. Moreover, in 2021, 14%, 12%, 12%, and 12% of our revenue was derived from the incorporation of our solutions into the vehicle models of four OEMs and a total of 78% of our revenue was derived from the incorporation of our solutions into the vehicle models of eight OEMs (including those four) through our Tier 1 customers. We have not executed written agreements with these Tier 1 customers but rather provide our solutions to such customers pursuant to standard purchase orders under our general terms and conditions, pursuant to which they are generally not obligated to purchase our solutions in any certain quantity or at any certain price

Amnon Shashua Seems Unfocused - and He has a nice purchase option

Amnon is very talented. Check out this bio.

We are highly dependent on Professor Shashua, our President and Chief Executive Officer. While Professor Shashua is highly active in our management and allocates a significant amount of time to our company, he does not devote his full time and attention to our company. For example, Professor Shashua is also the Chairman and co-founder of AI21 Labs, which works to use AI to understand and create natural language, the Co-Chairman and co-founder of OrCam, which harnesses computer vision and AI to assist the visually and hearing impaired, the Founder of One Zero Digital Bank, an entirely digital independent bank being developed in Israel, the Chairman and co-founder of Mentee Robotics, which aims to build humanoid robots, and the Sachs Chair in Computer Science at the Hebrew University of Jerusalem, where he teaches and supervises graduate students.

He’s actively a professor at the University of Jerusalem? That seems like a heavy burden. Oh, but this is my favorite part of the entire registration filing.

Additionally, Prof. Shashua has the option to invest up to $10,000,000 of his own capital in Mobileye, and such investment may be made, if Prof. Shashua so elects, by purchasing shares of our Class A common stock in this offering. Furthermore, if such investment is made, it will be matched on a three-to-one basis through grants of additional awards of our equity, vesting 50% in the fourth year following the completion of this offering and 50% in the fifth year following the completion of this offering, with specific terms of the grant to be determined.

Links

I’m putting up the simple model I made behind the paywall. It’s pretty much just the S-1 filings put into excel. If you found this entire post helpful, I would appreciate it if you shared or subscribed! Any bit counts. Thank you!