NVIDIA: Waiting on Blackwell, and the Networking Question

A brief update on Fabricated Knowledge, and then an update on Nvidia.

For those who haven't heard, I am officially joining the SemiAnalysis team! I announced the change on the Stratechery Podcast. My role, in particular, is to help drive high-level strategy and launch the Core Research Product for financial customers. Think of it as a higher tier of SemiAnalysis (and Fabricated Knowledge) content that marries the technical content with an economic lens. If you’re curious (this is for institutions only), reach out to sales@semianalysis.com.

Now, what that means for Fabricated Knowledge is… pretty much nothing. There might be more help if I post more information from better sources, but I think there will be some limits. I’ll try to retain my independent voice on my beliefs and focus on where I do best: higher-level stories and market analysis. It’s helpful that I now have the handy world-class expertise of SemiAnalysis to guide me.

If you can’t beat them, join them. And SemiAnalysis / Dylan has always been close to me. I cannot express how excited I am to uplevel my understanding of the space.

Anyways, on to Nvidia.

Nvidia posted earnings yesterday, and guidance was light of buy-side bogeys. I’m not going to step into the mind game of bogeys here, but there are some finer points to focus on.

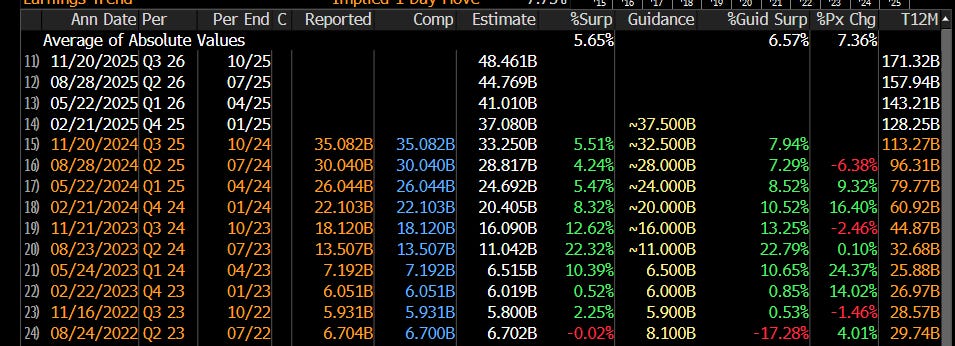

NVIDIA reports Q3 EPS $0.81 ex-items vs FactSet $0.75

Reports Q3:

Revenue $35.08B vs FactSet $33.17B (2 billion beat like clockwork)

Q4 Guidance:

Revenue $37.5B +/- 2% vs FactSet $37.09B (a bit light)

GAAP and non-GAAP gross margins are expected to be 73.0% and 73.5%, respectively, +/- 50 bps. (also light)

This is the lightest guidance this year since the beginning of the massive beats. The guide of $37.5 versus estimates at $37.09 pretty much means a 1% guidance beat. That alone is “disappointing,” but it makes sense given that we are approaching the crossroads of Blackwell and Hopper.

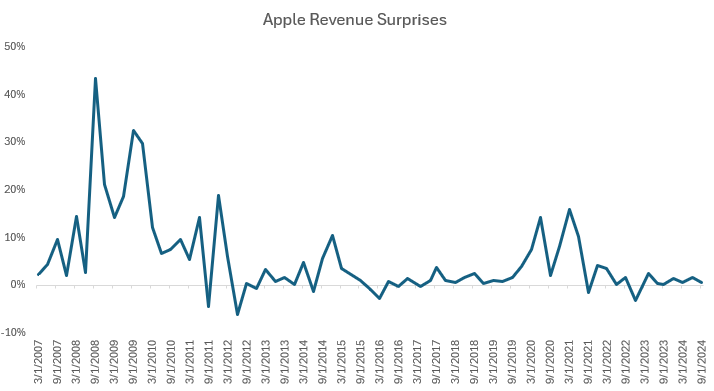

Lower-than-expected beats mean the street is finally catching up to Nvidia, which is good thing. It’s the largest company in the world, and it shouldn’t be possible to see 20% revenue beats without the whole world knowing. The reality is the bigger you are, the less volatile your results. The bigger you are, the more flows it takes to move your stock, and as you become a larger company, the +/- 20% moves usually start to simmer down.

There’s an excellent historical analogy to this: the iPhone. Once upon a time, Apple had massive revenue beats similar (but nowhere near as big!) to what you’re seeing today when they launched the iPhone. That surprise has gotten smaller over time.

It’s also easier to get wind of your supply chain. I think that today’s earnings result was quite dull, and the reality is that’s a good thing. Boring execution is alright, and Nvidia is doing that with 90% revenue growth year over year.

The reality is that being number one carries some heft. Part of that should be lower surprises and volatility in the future. Nvidia’s surprise moment has come, and the market, in its wisdom, has come to anticipate it. That’s a good thing about growing up, but expecting the same volatility beats doesn’t make sense.

On Gross Margins

Ironically, the concerns I had last quarter showed up this quarter in full force. The guide was a bit light, and I think that almost all I had feared in the previous quarter has come to pass, but the market is okay with it.

As Blackwell ramps, we expect gross margins to moderate to the low 70s. When fully ramped, we expect Blackwell margins to be in the mid-70s.

We will start growing into our gross margins but we do believe those will be in the low 70s in that first program. So you're correct, as you look at the quarters following after that, we will start increasing our gross margins, and we hope to get to the mid-70s quite quickly as part of that round.

So first, starting on your first question there, Stacy, regarding our gross margin and define low. Low, of course, is below the mids and let's say, we might be at 71%, maybe about 72%, 72.5%. We're going to be in that range. We could be higher than that as well. We're just going to have to see how it comes through

The reality is, does it even matter? When margins are asked about a product that has peaked, you’re looking at the past, and stocks are forward-looking. The only thing that matters is Blackwell, and the reality is that Nvidia’s stock is waiting on Blackwell.

Waiting on Blackwell

This is not Blackwell's first quarter. The next quarter will be the first with meaningful revenue. Nvidia raised its previous guidance from several billion dollars in Q4 to exceed that number with supply increases.

While demand greatly exceed supply, we are on track to exceed our previous Blackwell revenue estimate of several billion dollars as our visibility into supply continues to increase.

This also flies in the face of the new chips overheating rumor that The Information is flying around again. This is the B200 cancelation that flew around a few months ago and was just dragged back from the dead. Nvidia's increasing supply directly contradicts this, and the swirling rumors have become hard to keep up with (and wrong!).

We continue to wait on Blackwell. The crossover is much more critical this time, and we are starting to see the secondary market's in H100 pricing decrease, as first reported by SemiAnalysis. Hopper's revenue additionally looks weaker than last quarter, which many thought meant growth from Q3 to Q4. It seems now it will be flat.

Q4. But yes, is it possible for Hopper to grow between Q3 and Q4? It's possible but we'll just have to see.

Weak Hopper matters on the margin, but if you’re forward-looking, it’s, once again, eyes on Blackwell. Considering they just put up 90%+ revenue growth, Nvidia shares are cheap (~34x CY-ish 25x earnings). Blackwell’s success is what will make this EPS real or not. And while slightly disappointing, this isn’t a shocking quarter.

Nothing can shake how much all debates don’t really matter compared to Blackwell. Shares are cheap, Blackwell's demand exceeds supply, and we are waiting on Blackwell. I don’t think estimates will meaningfully move higher or lower until we see the ramp in earnest. From this perspective, this was a bit of a snoozer earnings result.

But What about Networking?

I think that’s all fine, but the actual open question from this earnings result was about networking—specifically, what is happening with the networking attachment rate? Its a drastic decline as a percentage of datacenter revenue.

How could this go from ~30% of revenue to 15% this quickly? Networking revenue shrank sequentially while the rest of the business grew. What gives?

Networking revenue increased 20% year-on-year. Areas of sequential revenue growth include InfiniBand and Ethernet switches, SmartNICs and BlueField DPUs. Though networking revenue was sequentially down, networking demand is strong and growing, and we anticipate sequential growth in Q4

I have some informed speculation behind the paywall.