Nvidia's Crypto Issues, Cisco's Supply Chain issues

Nvidia's results are a tale of two segments, Cisco says Chinese supply chain bumps ahead.

This post will be the last post about earnings this season, given that the earnings season is wrapping up. First let’s talk about everyone’s favorite semiconductor company: Nvidia.

Nvidia

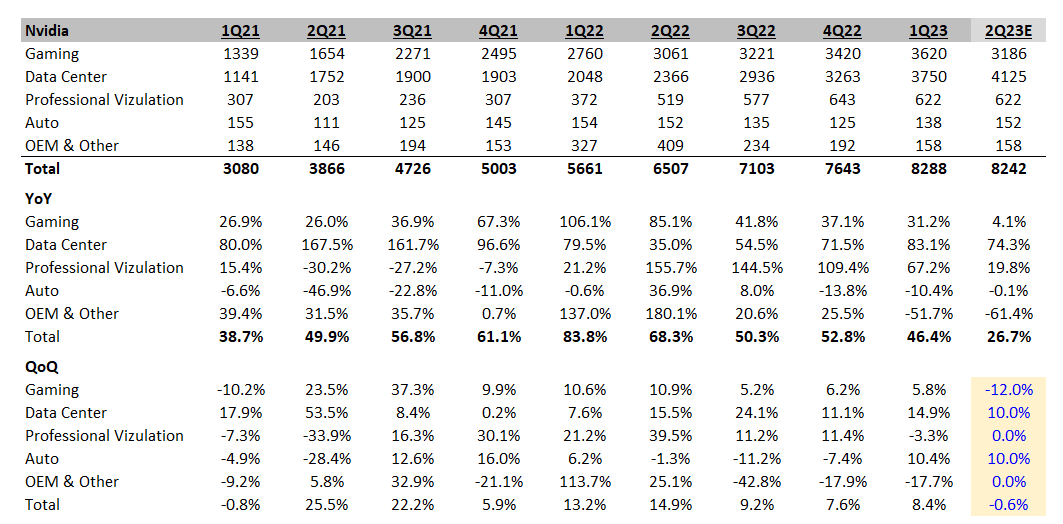

Nvidia was one of the most anticipated reports of the quarter. We knew that they should beat revenue given TSMC’s data center strength, but the real surprise was the guide down. I really like the summary that @ConsensusGurus does, and I’ll be using them from now on.

As you can see, the actual quarter was fine and had a pretty typical Nvidia-like beat. The problem is the guide, and the biggest contributor to the guide down was gaming. They expect revenue to be ~$8.1 billion +/- 2%, which is sequentially down. Nvidia however does tend to be a conservative guider.

While I believe this is likely sandbagging, I tried to back out what I thought was a reasonable revenue range. The numbers led me to 3 conclusions.

Gaming is looking weak with cryptocurrency making it likely even weaker

Datacenter is as strong as ever with a product cycle incoming and easy comps

What is Automotive doing?

Let’s go through each segment and question. First with the all-important gaming segment.

Gaming and Crypto

I wrote about the potential weakness in gaming in March, mostly on the understanding that Ethereum 2.0 will move to proof of stake and thus flood a large inventory of GPUs onto the market. This should fix the supply and demand issues - we have largely seen that come true. One measure of that effect is the pricing of GPUs.

One of the things I have been watching for is if new GPUs get back to MSRP prices with broad availability, and this seems to be the case. Below is a chart of a 3080, MSRP price is $700 dollars, and they are avaliable today on Amazon for $720.

In addition to broad-based availability, Nvidia’s CFO said one of the things that I’ve long believed - that Crypto based demand is almost impossible to forecast for them.

The extent in which cryptocurrency mining contributed to Gaming demand is difficult for us to quantify with any reasonable degree of precision. The reduced pace of increase in Ethereum network hash rate likely reflects lower mining activity on GPUs. We expect a diminishing contribution going forward.

But given the actual results and guide, we are starting to see the impact. The real shoe has yet to drop - Ethereum 2.0 is well on its way to being merged into mainnet likely in August. Meanwhile, we are starting to see pretty interesting anecdotes that the GPU channel has completely cleared and scalpers are now returning their GPUs en masse.

As we expect some ongoing impact as we prepare for a new architectural transition later in the year, we are projecting Gaming revenue to decline sequentially in Q2. Channel inventory has nearly normalized, and we expect it to remain around these levels in Q2.

There is now meaningful channel inventory, and a new product launch this fall. The worst-case setup is likely going to happen for gaming at Nvidia. As they launch their new product, they will be forced to heavily discount their older product at the same time cryptocurrency miners will be dumping their used GPUs. The net effect is that the new generation could have a real problem selling against a heavily discounted secondary market. This is exactly what happened in 2018.

The 3 years long GPU market shortage is likely to become a glut very shortly, especially with this confluence of events. Ethereum 2.0 with proof of stake has already been live and going well, and the full merge is likely to happen in August. All signs point to a weakness that is getting worse.

Looking at past crypto cycles, it’s possible things get very ugly quickly. This is the first sequential decrease and inventory looks bad, it’s possible Nvidia pulls another 2019-like scenario with -40-50% QoQ growth. More on this later.

Datacenter

While I am preaching doom and gloom in gaming, I have to say I am loving the data center results. Judging by absolute dollars added on a trailing 12-month basis, the data center is accelerating on an even larger base.

I have no problem in the near term with data center, and think Nvidia’s results are impressive. They are selling A100s this well before a product cycle which will refresh the 2-year-old chip. The H100 looks like an amazing product chip and yet their customers are still purchasing even more chips into the product cycle.

A further look at their results indicates that the customers that matter are the ones spending even more.

Moving to Data Center. Record revenue of $3.8 billion grew 15% sequentially and accelerated to 83% growth year-on-year. Revenue from hyperscale and cloud computing customers more than doubled year-on-year, driven by strong demand for both external and internal workloads. Customers remain supply constrained in their infrastructure needs and continue to add capacity as they try to keep pace with demand.

Nvidia also feels optimistic about their new Spectrum-4 networking switch and noted that the PCIe 5 launch is actually a new major cycle that will be paired with new product launches like the Grace CPU.

In networking, we're kicking off a major product cycle with the introduction of Spectrum-4, the world's first 400-gigabit per second end-to-end Ethernet networking platform, including the Spectrum-4 switch, ConnectX-7 SmartNIC, BlueField-3 DPU and the DOCA software. Built for AI, NVIDIA's Spectrum-4 arrives as data centers are growing exponentially and demanding extreme performance, advanced security and powerful features to enable high-performance advanced virtualization and simulation at scale. Across our businesses, we are launching multiple new GPU, CPU, DPU and SoC products over the coming quarters, with a ramp in supply to support the customer demand.

Furthermore, the geometric stack is getting easier to comp, so I think the data center will likely continue to be strong.

To take a step back and be bearish on the data center, my biggest concern is we are a lot closer to the peak than the trough, and that results could decelerate just as gaming implodes.

However, on closer inspection, it seems a lot harder to call data center weakness than in the past. Part of this problem is the new product launch, another part is that AI really has started to decouple from the larger data center spending cycle. Mix-shift could bail out Nvidia. Let’s talk about the last cycle and this upcoming cycle, first refer to the YoY capex numbers of the big 4 below.

The thing I’m watching for is the digestion period that happened last time during the capex splurge, with 2019 being a rather tepid year that the hyperscalers focused on buying and building boxes instead of filling them with servers.

The problem is that unlike last time Nvidia really seems to be decoupling from hyperscale capex numbers. Here is the best match I could do calendarized of total Big 4 spending compared to Nvidia capex. Nvidia accelerated before hyperscalers, and despite some deceleration in aggregate capex they are still accelerating. Last time there was a meaningful digestion period in 2018 - this time I’m not as sure.

Deceleration has already started to happen while Nvidia is still growing at a much faster rate. I think the biggest reason (other than me having bad AWS numbers) is that it’s as simple as a secular budget shift towards AI spending. AI is the fastest-growing portion of the pie and becoming a larger part of the capex budget. It’s not as clear-cut as datacenter spending being a proxy for Nvidia datacenter. Especially with a new product launch on the way.

I’m amazed at the results, I can see how the data center could accelerate slightly higher, but think that Nvidia likely won’t have a hard landing in Datacenter. It’s completely possible that a new product cycle in the data center could offset horrific gaming results. The data center will just become a larger and larger part of the pie and soften what would have been a mortal blow in 2018.

Automotive

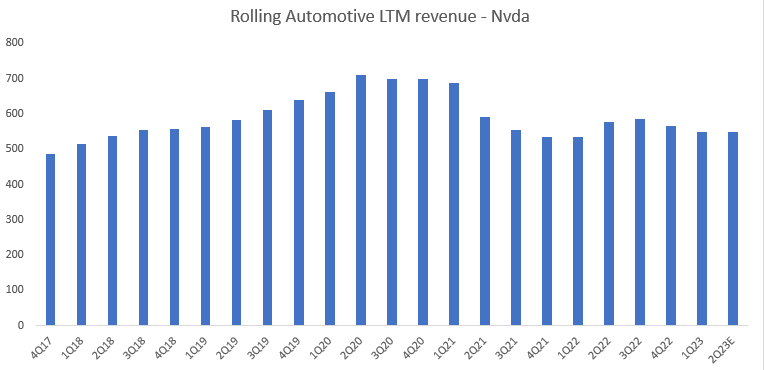

This is a weird segue, but for a company that has been touting its design wins for years and talking about how material the automotive segment is going to be, Automotive revenue has gone nowhere.

Compare this automotive commentary on the call to the actual rolling last twelve months of revenue.

Moving to Automotive. Q1 revenue of $138 million increased 10% sequentially and declined 10% from the year ago quarter. Our DRIVE Orin SoC is now in production and kicks off a major product cycle with auto customers ramping in Q2 and beyond. Orin has great traction in the marketplace with over 35 customer wins from automakers, truck makers and robo taxi companies.

In Q1, BYD, China's largest EV maker, and Lucid, an award winning EV pioneer were the latest to announce that they are building their next-generation fleets on DRIVE Orin. Our Automotive design win pipeline now exceeds $11 billion over the next 6 years, up from $8 billion just a year ago.

This doesn’t look like billions in revenue, this looks like a business that is just treading along. I really want to see some of these design wins flow through because I am absolutely shocked that there was more revenue in April 2019 than revenue in April 2022.

Compare this to the STM investor day presentation, Nvidia is a secular share donor from this perspective. Give me more reason to believe in your Automotive story Nvidia.

Nvidia Thoughts

I want to summarize my entire thoughts on Nvidia. It’s pretty complicated. First and foremost I think Gaming is imploding at a rate that should be concerning for investors. They just guided down teens sequentially with a stuffed channel into a new product launch and a crypto clearing event. I want to kind of test a worst-case at Nvidia.

First I have some assumptions of what could happen, and I am going to assume the worst happens at Nvidia - a 30% sequential decline on top of this mid-teens sequential guide down. Meanwhile, I am going to continue to assume 10% QoQ growth in Datacenter, driven mostly by new product launches. I’ll assume flat visualization and OEM QoQ. Let’s roll it up to results and see what we get.

Unlike last time, I think Datacenter will completely bail them out. Even with a 30% sequential QoQ drop (less than 2018 but stacked worse), revenue could be positive at worst, and then begin to grow again. This is not the same Nvidia of 2018, and the accelerating and larger data center segment are making sure of that. In my view, this is a pretty reasonable base case.

The problem is that the valuation of Nvidia really does not make this bearable and street estimates really are not willing to take the bitter pill of a gaming implosion. Hell, I am not sure gaming will quite implode like last time!

But in a market with rising interest rates, the longest duration stocks are getting crushed. A company like Nvidia cannot have that kind of revenue growth at their valuation, and if this time ends up worse than last time (50%+ sequential decline) then revenue growth will go negative.

If they really do implode in the gaming segment, forward earnings are way too high and the multiple should shrink. The 20x forward P/E on depressed earnings is the number that feels right if we are taking history as a guide.

It’s a hard short to be fair because even underwriting the worst case you can squint and see that Nvidia would be trading at a very average multiple and the forward numbers would look pretty appealing for one of the best secular stories in semis. I think you should tinker around with the numbers yourself! The spreadsheet I used is attached at the end of this post.

Cisco and Supply Chains

Cisco had one of the weakest guides, especially relative to peers. They continued to iterate that it was not demand-driven weakness but completely supply-driven weakness that caused the entirety of the guide down in the coming quarter. In particular, they had two events against them, exiting Russia completely and the partial shutdown in China.

On that second note, I liked Cisco’s commentary on China. They had one of the most forward-looking perspectives on the Chinese lockdowns ending. Counter-intuitively China's reopening will likely create even more supply chain chaos.

We don't know what open up means. Does it mean that they're going to slowly open grocery stores and salons and things of that nature and that the logistics side of it -- or do they open up their logistics on day 1? What does it mean about the capacity of resources they have for the logistics side? But our concern is that every company there is going to be trying to ship out. In some cases, many of the factories have been approved to keep working, and their workers have been working in dormitories. So they have components or ready-to-ship product that is sitting on the floor, and it's all going to race for the ports. It's all going to compete for the airports.

And we know there's lower air traffic capacity right now for us to leverage. So we're concerned about how long it takes to clear that up, which is reflected in the guide. We also think that once it gets into their ports and it starts coming to the U.S., we have the risk of seeing what we saw in L.A. several months ago. So those are all just the unknowns about what does opening up look like and what's the time frame for recovery that led us to the cautious guide that we put out there.

And I would just remind you that it's not just Shanghai. I think as of the last article I read, there were like 45 cities that were in lockdown, and it was over 1/4 of the population of China. So it's broader. But that's how we're thinking about it, and we just have to wait and see how it unwinds.

They continue to say that they don’t see demand issues and that their following quarter guide (bad) was utterly supply-driven. Their backlog is at a record $15 billion, but something I can’t help but wonder about is the flow-through of backlog and revenue for the rest of the year.

So first thing I'll say is that I think any seasonality right now is out the window with the current situation and with what we've seen with the order demand. We're doing 18-month planning with certain customers. And if they placed 18 months' worth of orders last quarter and now they're going to pause and we may be doing it with 3 fewer customers this quarter. So I mean it's just a -- it's a very difficult thing to get your head around.

So they are taking multiple years of orders right now, and the order book may grow into the next quarter, but it’s hard to see orders growing from there. Revenue growth should catch up to order growth, but I can’t help but ask is this the cyclical peak of order intake?

There's kind of 2 angles to that, David, that I'll try to touch on. One is the -- when does the backlog itself peak. And while we don't forecast that, it would not surprise me to see it grow again in Q4.

I hope that makes sense to you. We're sitting on both a record backlog and record inventory, which seems like it's in contrast with one another, but it's not, right? We're holding on to the parts that we've got, and we just have to get the remainder to square the sets and get those building out the door.

Regardless of how you feel about Cisco (I don’t have a strong opinion), I thought the Chinese commentary alone was worth highlighting. The global supply chain continues to be stretched and broken over and over, and despite the disruptions from Shanghai, it’s looking like it will counterintuitively make things worse in the near term after the eventual Chinese reopening. Big if.

Have a good day! If you enjoyed this analysis - consider subscribing or sharing! Both free and paid subscribers help me immensely. If you want to play with the assumptions yourself, feel free to download the models I used behind the paywall.