ON, NXPI, AlChip, ONTO, and NVMI

The last week of earnings coverage - and an idea

We are almost done with peak earnings. Next week I will not be posting an earnings round-up as I have for the last few weeks. I’m excited to start working on longer-term projects, and earnings season has sparked an idea of my next long piece.

On another note, the SOXX index broke out of a range it’s traded at against the S&P since I left for the hike. I think that the market is starting to believe 2022 is not going to be a contraction year and appreciating the strength and duration of the semiconductor shortage. On to the update.

On Semiconductors Turnaround

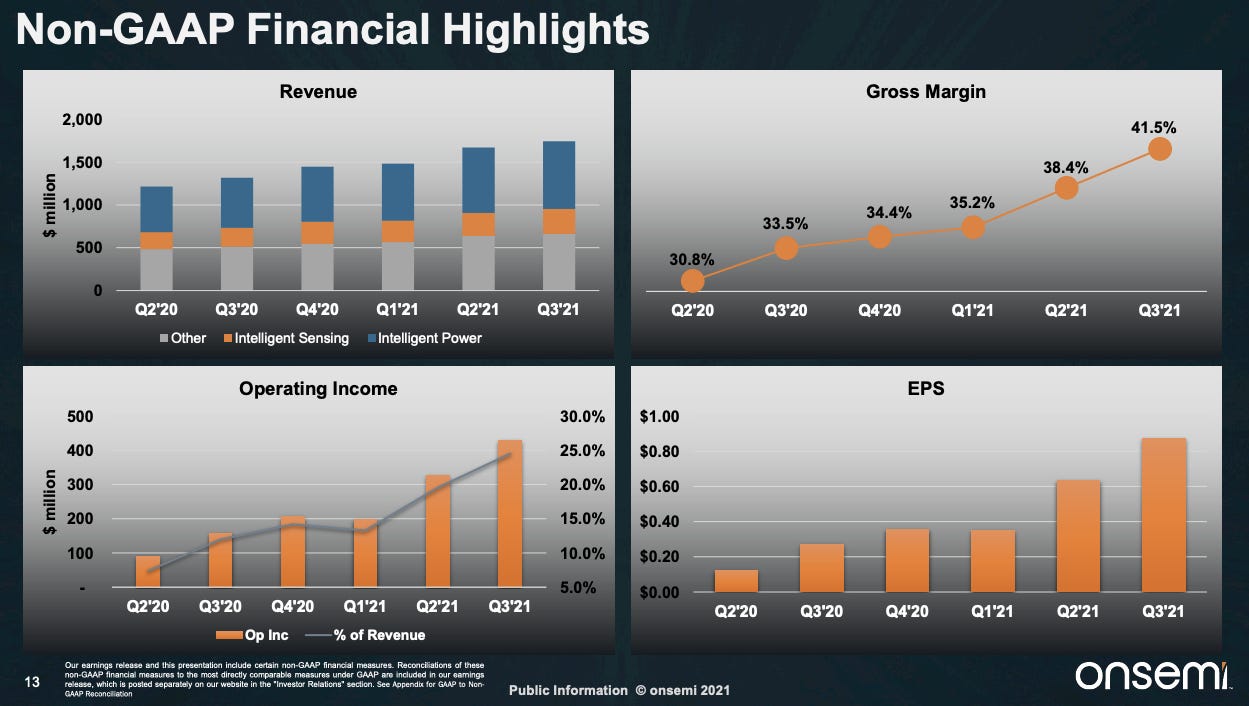

On Semi is firing on all cylinders. On Semiconductor reported EPS of $.87 versus consensus of $.74, and revenue of $1.74b versus consensus of $1.71b. On semi guided for EPS of $.89-1.01 versus consensus of $.75 and revenue of $1.74b-1.84b versus consensus of $1.72b.

For those new to the story, the key player is the new CEO, Hassane El-Khoury. Previously he was CEO at Cyprus Semiconductor before the sale to Infineon. By all accounts, he was an impressive leader there. El-Khoury succeeded Keith Jackson, who lead the company from 2002 until 2020.

Before Hassane, On Semi was sleepy and unfocused and with a leadership team that was not hungry. Meanwhile, Hassane El-Khoury is a dynamic and cheerleader-like CEO. He wanted to make it exciting to work at On Semi, and given the share price performance, I think his employees are likely engaged.

His first steps while joining the company was an ambitious plan to improve margins and refocus the company, and so far, he has done just that. The rapid movement from ~30% gross margins to ~41.5% gross margins this quarter is drastic, and the long-term target of 45% gross margins seems achievable sooner than 2025.

How they did this was primarily a divestment of lower-margin products. CFO Thad Trent explained this well on the call:

Ross, this is Thad. I'll take that. In my prepared remarks, I talked about we've exited approximately $100 million over the last 2 quarters, 60% of it being in the third quarter. And the average margin for that business was roughly 15%. We plan on continuing to exit that business over the next 2 years. As we've talked about, it will be about being fairly linear for the next 2 years as we continue to execute and we shift that capacity into higher-value products and higher-value capacity.

Analysts had some concerns about the durability of these gains, and if this was a cyclical and not structural change. Given that their fab utilization went down this quarter and margins improved, it seems like this is sustainable. On Semi thinks it is:

The other thing -- over the last year, the other thing that worked in our favor is the utilization. And that's sustainable, as you mentioned, as we wind down some of our fabs and we restructure and do the fab manufacturing optimization. That utilization is going to be and remain at that higher level, even with that 10% to 15% reduction in the noncore business. So all of these, I would say, are self-help.

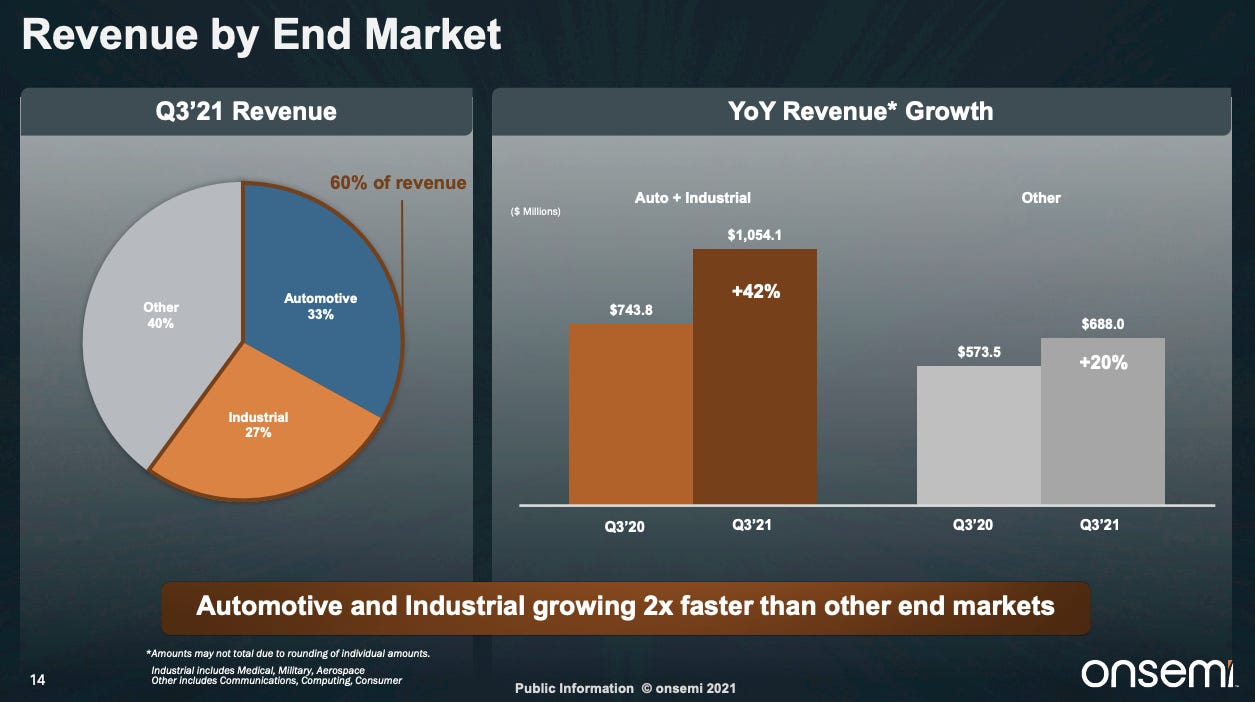

Besides the gross margin, ON posted strong revenue growth, especially in its automotive and industrial segments.

I still think On Semi looks “cheap”, and the self-help story is only half-finished. I’m waiting for a pullback, but I want to highlight that despite the impressive performance year to date, the multiple is cheaper than at the beginning of the year. Part of this was expected, and why On Semi trade at such a “premium” multiple when in reality the market was expecting meaningful margin improvement. I still am impressed by El-Khoury’s quick margin expansion and what’s to come.

If you believe in the continued strength of the automotive market, I believe On semi’s stock will continue to work. So that brings me to NXPI.