Oracle and Animal Spirits

Oracle's result is the second most impactful earnings result this cycle. And I think it's a critical turning point.

Oracle just posted the single most astonishing quarter I have seen since Nvidia’s blowout in May 2023. A reminder is that it was the quarter where Nvidia guided to 100% Y/Y growth and shocked markets after the ChatGPT moment. It has been almost a straight line to becoming the world’s most valuable company since then. Oracle’s guidance is staggering for a different reason: its sheer magnitude.

This was the largest one-day move in any stock’s history by absolute value. Larry Ellison also became the wealthiest person alive in the span of a trading day. The opening line of Oracle’s guidance explains why:

Q1 Remaining Performance Obligations reached $455 billion, up 359% in both USD and constant currency.

Pause and digest that number. Denmark’s GDP is about $450 billion. It’s a number so big I first thought it was a typo. It is almost unbelievable for a company to disclose hundreds of billions in future revenue; it is even rarer to offer four-year guidance. But Oracle just did:

We now expect Oracle Cloud Infrastructure will grow 77% to $18 billion this fiscal year and then increase to $32 billion, $73 billion, $114 billion and $144 billion over the following 4 years. Much of this revenue is already booked in our $455 billion RPO number, and we are off to a fantastic start this year.

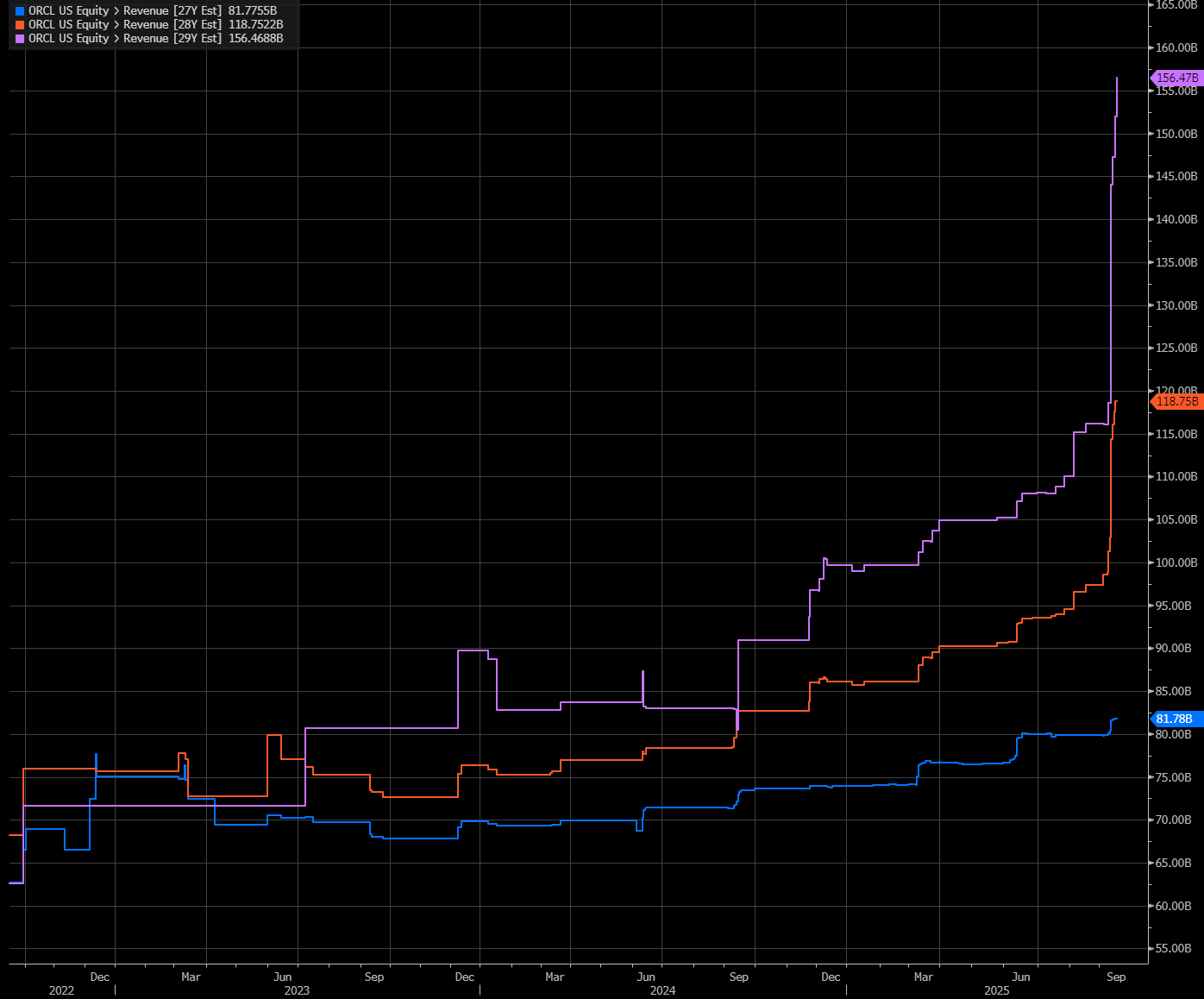

For context, Microsoft’s Azure is forecast to generate approximately $75 billion this year, while AWS is expected to generate around $126 billion, and Google Cloud is projected to generate about $56 billion. Oracle was not even considered a top-tier option until recently. If its trajectory holds, it could surpass Google and perhaps even Azure within a few years. Look what it did to our year-end estimates. The street consensus shifted from approximately $95 billion to approximately $118 billion after the guide.

This is what disruption looks like. I have argued before that the hyperscalers’ old moats, balance sheets, and CPU-centric distribution were less impregnable than they appeared. SemiAnalysis’s ClusterMAX benchmarks confirmed this, and it is now a genuine contender from Oracle. Capital as a moat is not a lasting one.

History suggests that incumbents rarely dominate tangential markets. A focused challenger emerges, captures share, and reshapes the landscape. AWS played that role a decade ago; Oracle may be playing a similar role now. Amazon’s in-house Trainium effort increasingly resembles an “Amazon Basics” strategy, viable but not leading, while Oracle doubles down on the largest GPU-first cloud in the world.

The driver of this sudden leap is clear: OpenAI. Microsoft has slowed its spending; Oracle has filled the gap, becoming OpenAI’s primary infrastructure partner. That single customer dominates Oracle’s RPO. And if Oracle leverages its entrenched database franchise, it could become enterprises’ default inference partner as well. In one fell swoop, they are now the addressable inference partner for the majority of enterprises globally.

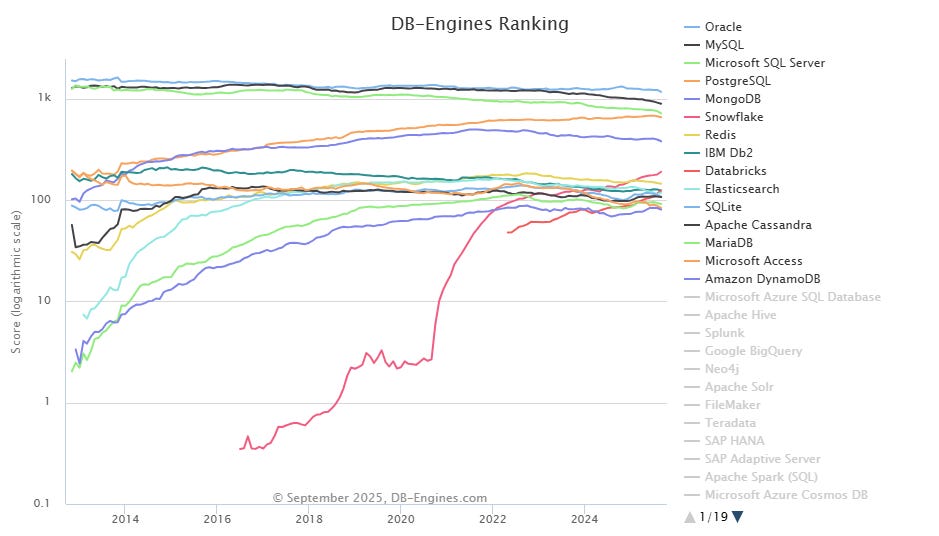

It is worth recalling that Oracle’s database remains the most widely used globally—still the gold standard for ERP, CRM, and data warehousing. PostgreSQL and MongoDB may be fashionable, but feature parity remains elusive. On DB-rankings.com, Oracle remains in first place. A reminder is that this chart is logarithmic, so the gap between competitors appears wider than it actually is. Oracle actually is the most dominant database in the world.

Now Oracle is pushing vectorized databases, paired with inference capacity, directly into enterprises. It is a compelling combination: entrenched incumbency in data, plus the most significant player in GPU infrastructure. To Larry Ellison, this is how you win the future's biggest enterprise in the world (OpenAI) while servicing decades of data from your historical dominance. However, all this spending is going to be quite costly. Which brings me to my next point: The Capital Cycle. Because this must be funded with something, and Oracle cannot pay for this with cash flow alone.

Capital Cycles and Debt

There is no way for Oracle to pay for this with cash flow. They must raise equity or debt to fund their ambitions. Until now, the AI infrastructure boom has been almost entirely self-funded by the cash flows of a select few hyperscalers. Oracle has broken the pattern. It is willing to leverage up to hundreds of billions to seize a share. The stable oligopoly is cracking. I wrote about this earlier, and I think that we are starting to see the markers of a classical bubble.

The implications are profound. Amazon, Microsoft, and Google can no longer treat AI infrastructure as a discretionary investment. They must defend their turf. What had been a disciplined, cash-flow-funded race may now turn into a debt-fuelled arms race. That’s a vibe-shift if I’ve ever seen one.

Welcome to the next and newest phase of the capital cycle. I believe the Oracle quarter achieved something more elusive than just revenue. I believe Oracle has just sparked the elusive animal spirit to life.

For more thoughts, please subscribe.