Packaging Stocks Follow-up: TER/6857/COHU/FORM & NVMI/CAMT/ONTO

The Turbo Edition of Company Coverage

So this is going to be different from a typical “initiation”. I will be more in-depth with some companies than others, but the key focus is to understand what each company does, what their core drivers are, and what their relative near term setup is. I will augment this over time with discussion of earnings and other company events. Below is a list of the companies mentioned:

Teradyne (TER)

6857:JP (Advantest)

Cohu (COHU)

Formfactor (FORM)

Camtek (CAMT)

Nova Measuring (NVMI)

Onto (ONTO)

This list is not exhaustive and I may add to it in the future. In the end, I will have a “questions I would ask management” section as well for reference for company calls. You’re always free to ping me to discuss and prep before calls with management.

I do want to point out that this universe has some of the best performers amongst all semiconductor stocks in 2020, especially in 2H 2020. In other words, I am worried that this initiation is poorly timed. There are embedded expectations for a better future in advanced packaging related companies, evidenced by multiple expansion. Specifically, note NVMI, CAMT, TER, and FORM in the 1-year returns below:

Teradyne

Disclosure: I own some but have trimmed on its recent run-up.

Teradyne consistently screens relatively cheap in the context of recent revenue growth and other quantitative metrics compared to the semiconductor universe. Despite my expectations for secular OSAT (Outsourced Semiconductor Assembly and Test) end market acceleration, Teradyne has run a bit past expectations given OSAT has historically exhibited intense cyclicality and is overdue for a “bust” in its somewhat predictable boom/bust pattern.

In 2020, Teradyne took massive share relative to competitor Advantest. As such, in the near term, the company looks fundamentally well-positioned with solid revenue guidance and strong broad-based demand for their products. However, I am somewhat worried about 2H2020 comps because of how well they performed in 2020. And guidance can really only be given guidance quarter to quarter.

Longer-term, Teradyne is qualitatively well-positioned and expensive relative to its past trading multiple.

Teradyne is a leader in a duopoly whose business is becoming more important with the rise of advanced packaging. Testing is a key part of the packaging supply chain—the various packages must be tested to figure out if the total system is working. The following quote from semiconductor engineering captures the increasingly important role of testing in semiconductors:

Test, which for years was stuck somewhere in the middle of the pack when it came to hardware engineering, suddenly became much more challenging over the past few years. Test budgets were increased, up from a flat 2% of manufacturing costs, and analytics were added into the mix in order to make sure chips would be able to withstand environmental, electrical and even unplanned events and continue working according to spec.

It seems clear that Teradyne’s testing exposure to advanced packaging is becoming more mission-critical. Other companies like FORM (discussed later) clearly break out their exposure, but Teradyne’s been opaque about numbers around direct exposure. However, we know they’re growing significantly above the market—Teradyne’s 35% revenue growth massively outperformed typical customers in the broader OSAT space (e.g. ASX/AMKR had ~20% revenue growth) and this is likely due to fab demand. Overall, it’s fair to say that testing intensity is likely going up and Teradyne will continue to benefit from its market share position (~45%).

Teradyne Segment Overview

Teradyne operates in 4 key segments. Semiconductor Test Systems, Industrial Automation, Wireless Test, and System Test.

System Test and Semiconductor Test are closely related to each other. The Wireless Test segment is just a modern iteration of telecommunication related testing, an old deprecated segment. Industrial Automation, on the other hand, is a real de-novo business. Here is a graph of the segment by revenue percentage over time.

Semiconductor Test segment is the largest segment but is growing slower than the rest of the company. Still, it dominants ~70% of revenue and is the bread and butter business. The key drivers for Semiconductor Test is the volume of semiconductor output, and the percentage of sales devoted for semiconductor testing, or testing intensity. Volume is very predictable over time, but testing intensity is less so (discussed later).

Semiconductor Test and Products (Segment Overview)

Teradyne is mostly focused on “Automated Test Equipment”. Teradyne of course invented this field in the 1960s, and if you want to read about their history, “Teradyne the first 40 years” is a good place to start.

A brief explanation of automated testing can be found below. It’s a classic 2000s era business hype video.

Digitaltest itself is a competitor to Teradyne, but the core products are essentially the same. In most examples of testing within the video, you are witnessing “package level” testing. These are testing systems that usually occur after silicon has been packaged into its final form but before integration into a PCB.

Package level testing is probably the largest category of test but is a relatively mature market. The growing incremental testing market is “wafer-level test” which is often done by probe test (more on that in the FORM section below). Teradyne serves both needs.

There is also a large category of testing primarily associated with ramping products during the manufacturing process, akin to the step before volume manufacturing. This is “design for test” and is closer to EDA and verification than to OSATs. This is where the foundries buy testing equipment. The below video clarifies this (starting 2:21).

I hope this offers a better understanding of how important testing is for manufacturing. It’s quite neat how engineers have to “design for testing” after the EDA tools step. The whole process requires very tight feedback loops between the simulation of EDA and result confirmation.

In any case, it seems to me that there actually are two schools of test demand, the initial ramp to volume manufacturing, and then the maintenance volume manufacturing that comes after volume production. The second category is a much larger dollar amount.

Pre Volume Testing Process

DFT / Sim stands for the design for test and simulation, a process that is completely almost completely in EDA tools.

Simulation to Test

So something that I want to highlight here is that testing and EDA go hand in hand for ramping volume production. This is because there is a simulation of ‘what should happen in a semiconductor’ during EDA, and then testing occurs post-manufacture to confirm the simulation.

The first part is where the fabs buy testing equipment, while OSATs buy testing equipment for post volume manufacturing yield checks, especially at the package level. I put this in here to make this point: testing isn’t exactly tied to “commodity-like” OSATs, but is an integral part of improving semiconductor yield overall.

Drivers of Test

Instead of writing about testing intensity, I think that the following video’s very specific 4 minutes (starting 16:19) is helpful to find what the drivers of testing intensity are. The segment ends at around 20 minutes - this is a “must watch” because this explains the entire industry drivers in a very succinct way. If you choose to skip the whole article but watch this - you’ll be fine.

A little later on in the presentation, the speaker mentions how testing intensity has actually gone down quite a bit but could rise again:

You might think that we've failed over the last 15 years, but over the last 15 years we've been able to reduce the cost of test from 2.5 percent of IC revenue to 1 percent of IC revenue.

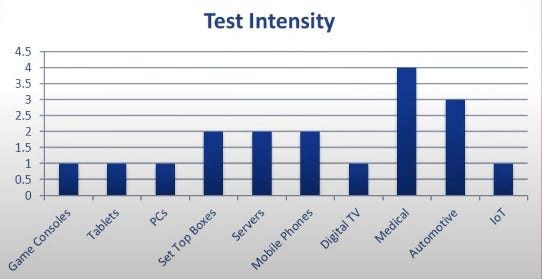

So the key drivers are mostly around a variety of form factors more so than the volume of semiconductors, as well as the criticality of the type of device. Medical and Automotive have much stricter testing requirements than PC and mobile. Recently each quarter, the testing intensity seems to be bucking its 2012 - 2018 trend and has been rising significantly. A great example is below and is likely the single most important driver for Teradyne:

The principal driver of mobility test demand continues to be increases in complexity of cell phone silicon. This is especially notable in 2020 when smartphone unit shipments are expected to decline about 10% to 1.2 billion, yet the collective test intensity of each unit continues to grow at a rate in excess of this unit decline. Within smartphones, the mid-to-high tier is the place to be in test, and that's where Teradyne is solidly positioned. These phones are seeing disproportionate growth and complexity related to multiple high-density camera arrays, and the associated processing power and storage to manage this data.

-Mark Jagiela, Teradyne Q3 2020 Earnings Call Transcript

Wireless Test

Wireless Test traces its lineage back to the wired test product that Teradyne invented but differs in that it’s targeted towards the most important semiconductor product in the world: the mobile phone. Wireless Test is focused on making sure RF and other packages work together in a phone form factor. A good example of the type of product is below:

RF (radio frequency) can be very hard to work, especially in small and bundled packages where (despite engineers’ best efforts) the output can be messed up. This causes issues like the iPhone 4 signal malfunction and is the area of Wireless Test that is relevant to Teradyne.

Wireless Test likely becomes more important as UWB (ultra-wideband) and Wi-Fi become larger and more varied parts of IoT devices. Every package with RF has to make sure the signals work together, and thus the results must be tested. This is good for semiconductor testing intensity.

Industrial Automation

Last but not least is one of the weirdest categories within Teradyne, Industrial Automation. In some ways, Teradyne’s testers have always been semi-automatic. After all, it’s called “Automatic Testing Equipment” (ATE) for a reason. In fact, a core value-add of the first Teradyne tester was that it didn’t need manual probing or humans to align the semiconductors.

Over time, Teradyne has slowly added more and more robotic features to their automated testing, especially in wafer and package handling. Paired with a few acquisitions, Industrial Automation has become a larger part of Teradyne while remaining distinct from the rest of the business. Here’s an interesting YouTube video about cobots (collaborative robots) from one of Teradyne’s competitors, Universal Robots:

Universal competes against the likes of Fanuc and other famous robot arm companies (as well as Teradyne). Incidentally, unlike Fanuc, Universal Robots trades at a huge discount, exacerbated by the last 3 years of sluggish industrial automation. In any case, I think this could turn very shortly.

Take a look at Fanuc’s Financials (from Sentieo):

I think Fanuc’s relatively sluggish results are better put into the context of a broad backdrop of poor results from global industrial automation in this area. Additionally, what’s more, surprising is that Teradyne’s Industrial Automation managed to grow when the largest company was shrinking revenue.

I am no expert in this segment, but assuming Fanuc’s forward estimates hold true, it seems a cyclical rebound could make this historically sluggish segment shine for Teradyne. Note that below all of the results are non-organic, and FY19 is likely more in-line with a modest tuck-in instead of large transformational deals.

What’s cool is that they get to leverage this segment directly to put into their semiconductor test equipment, which adds to their existing market offerings. To sum: this segment is a strong performer in an end-market that seems to be at a cyclical trough. Think of it as a “free option” embedded within Teradyne.

Financial Overview

Finally, a quick overview of financials and valuation.

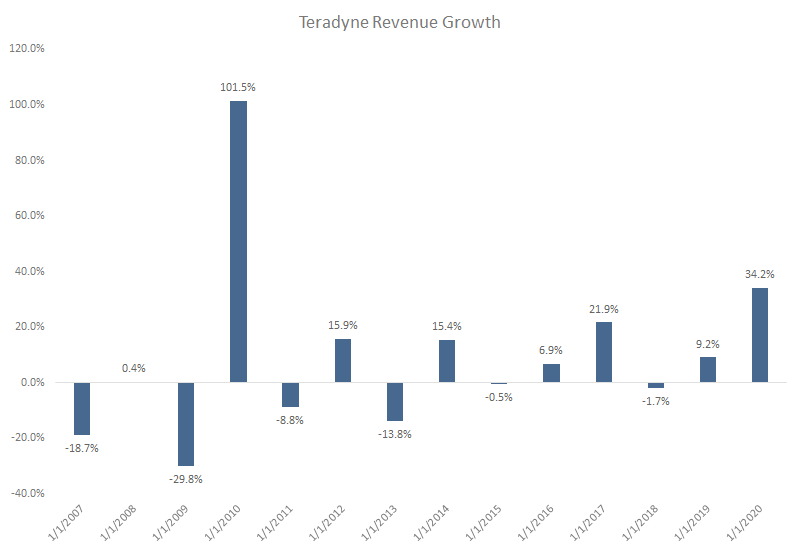

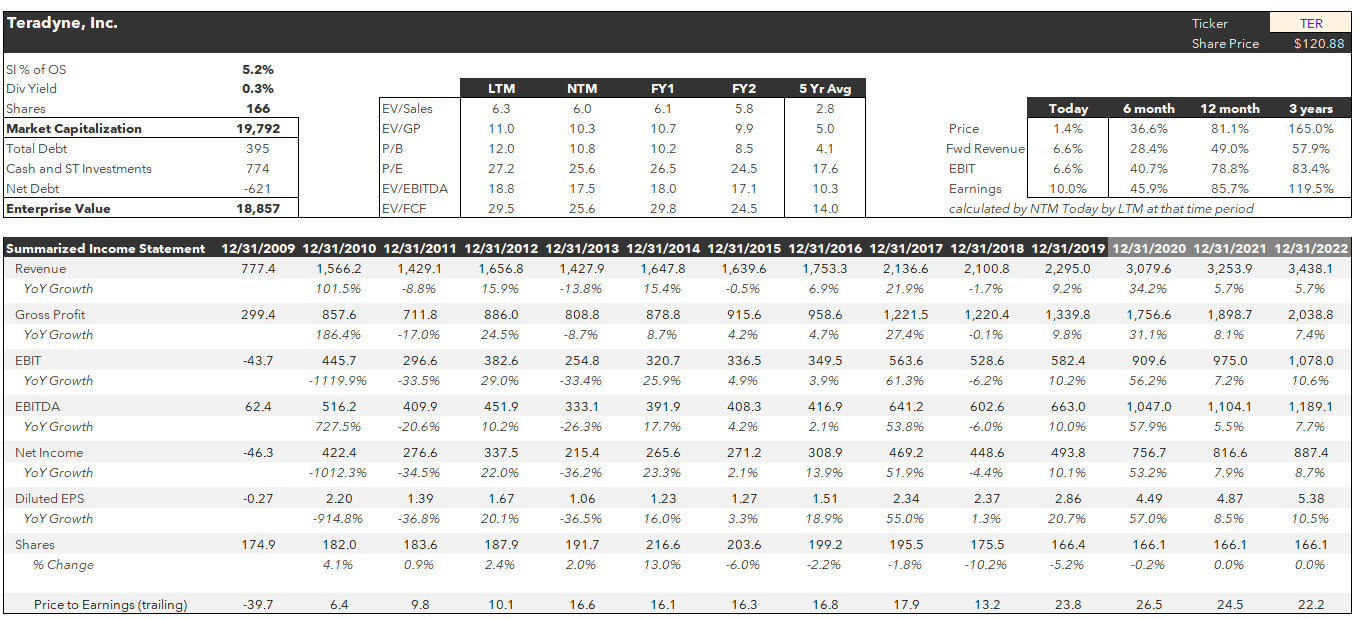

Summarized Income Statement

Note the cyclicality of their results, Teradyne tends to have large growth years followed by sluggish results. 2020 was one of those boom years, and the question is whether or not if that forward number is going to continue or end the trend. It’s unlikely that they grow as fast into 2021 or even grow, and it’s important to watch for hard comps in 2021, especially in the second half. But if testing intensity really is secularly increasing in excess of volume, then the downcycle won’t be as bad as expected.

Margins and Profitability

This is where the business shines. The mixed business has been generating incremental EBIT at a ~40%+ rate, and their incremental ROIC is much higher than the peer average.

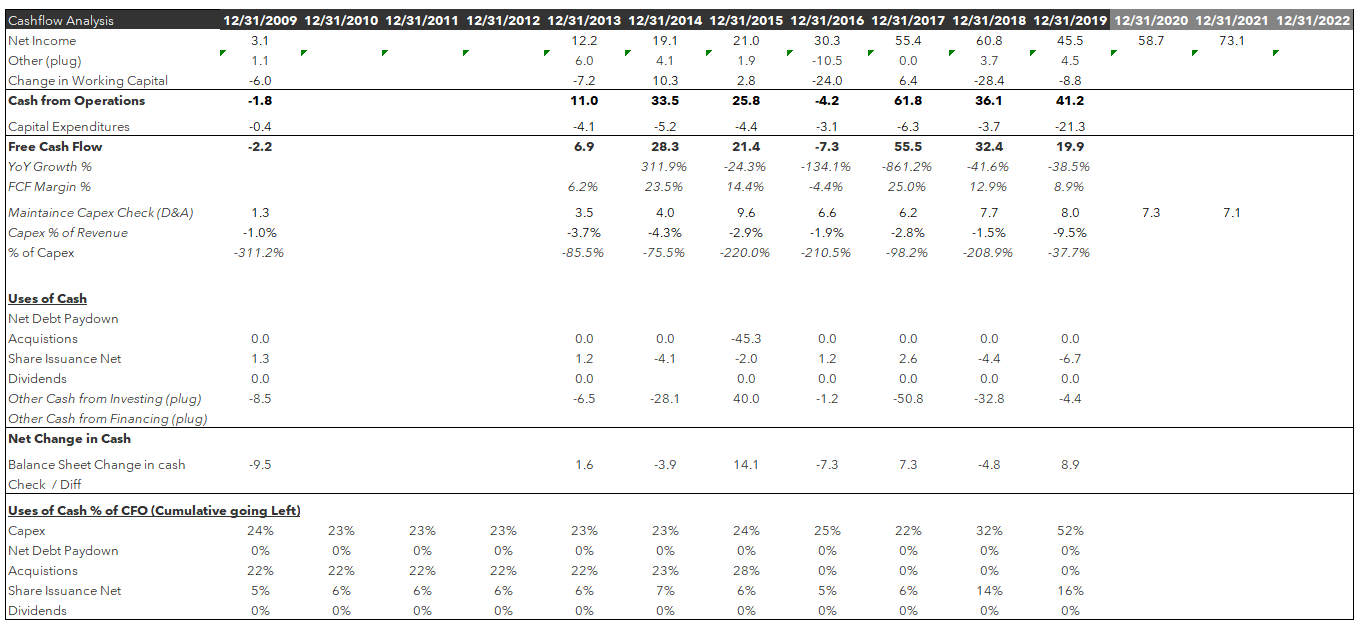

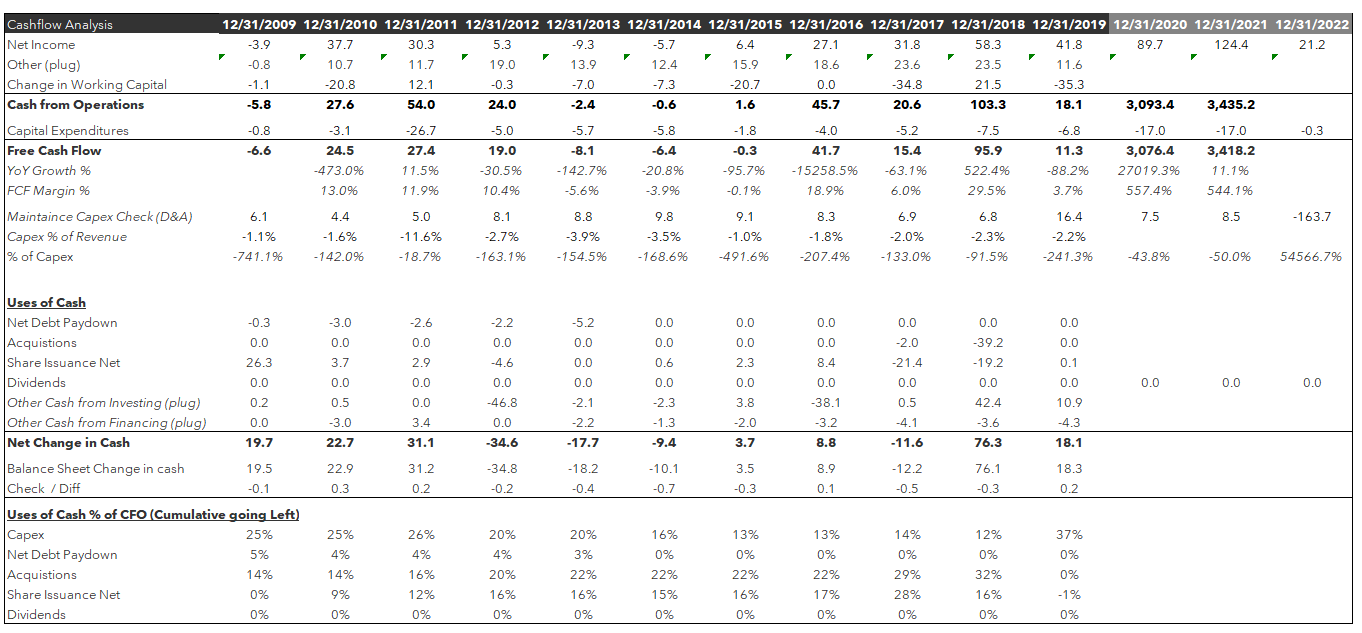

Cashflow and Uses of Cash

Let’s focus on their uses of cash. Reading it right to left, note that for the last 10 years, they have spent approximately ~24% on capex, ~24% on Acquisitions and ~36% buying back shares. This is partially funded by adding ~6% a year in debt. From this perspective, Teradyne is one of the most compounder-like in its uses of cash as it is a very consistent share repurchase yield and has high free cash flow generation relative to most peers.

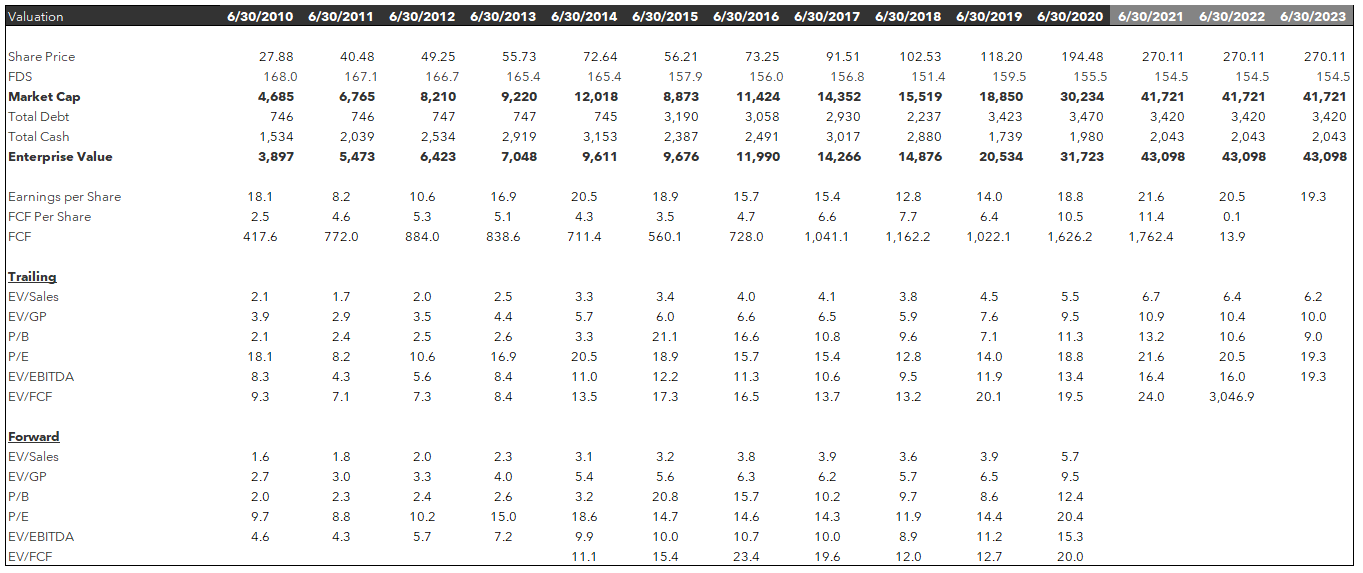

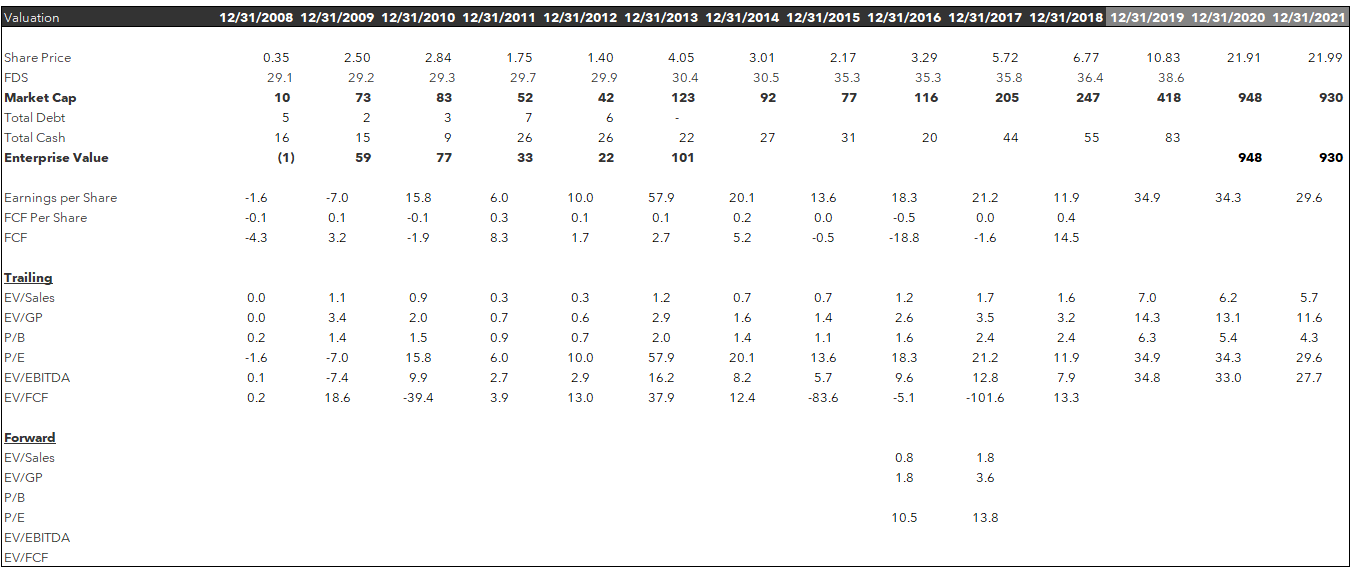

And Last - Valuation

Teradyne is currently more expensive than during most of its history, even on a forward basis. The firm used to trade at a high teens forward earnings multiple and is now trading at ~25x. Something to be cautious about given the likely rough comps given their huge recent wins. You have to believe they defy the historical odds at a higher valuation.

This could happen if the test intensity story plays out over a longer-term time frame, but as it stands, the valuation is running a little hot. I still like Teradyne over a longer period of time, so I would call this “market weight” as an opinion. If there ever is a revenue guide down and the business de-rates on a digestion period, I would gladly be a larger Teradyne owner.

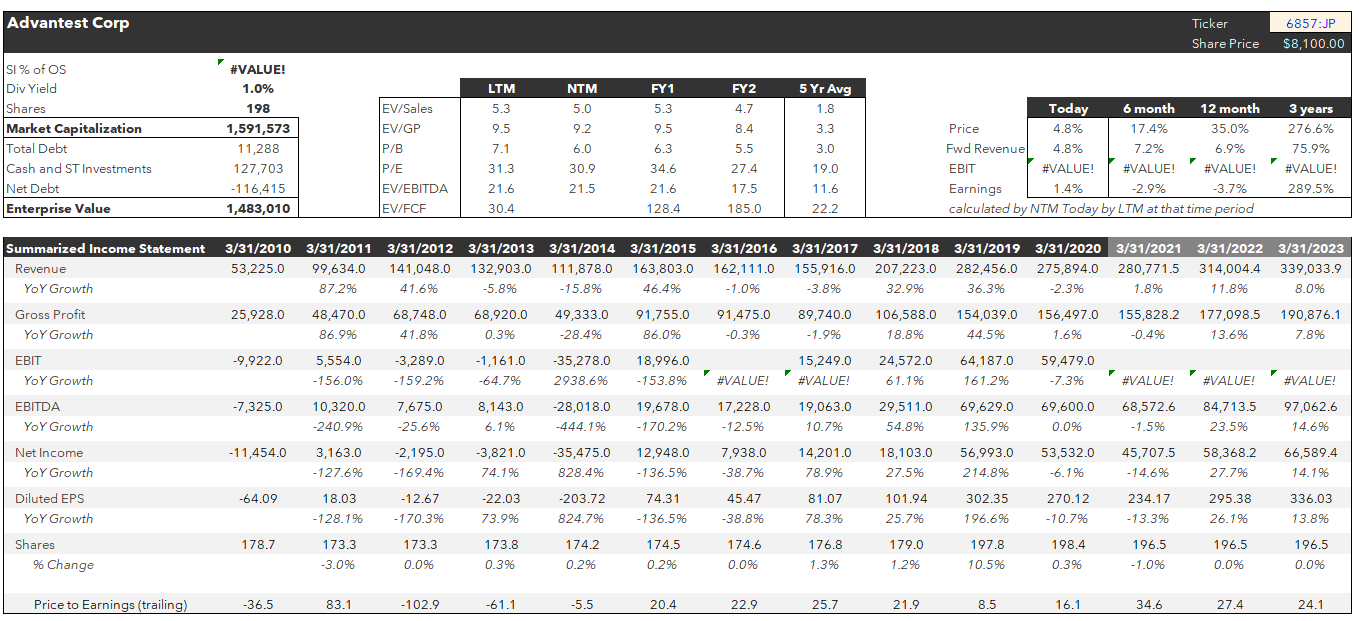

Advantest (6857:JP)

Advantest is the Japanese counterpart to Teradyne and has been a significant competitor since day 1. They are the #2 player in the duopoly (Cohu is a very distant third).

The founder actually visited Teradyne in its formative days in ~1970, and would eventually rename Takeda Riken Industries to Advantest in 1985. A more detailed history can be found here.

Most of what Teradyne does applies to Advantest as well. Note that Advantest has a very good IR presentation. Their documents provide much more clarity and color compared to Teradyne, which makes them one of the few cases where a Japanese company has better disclosure than a US-listed one!

This slide is somewhat dated but it helps put Advantest and Teradyne’s share into perspective.

Note that right now, Teradyne is taking more share from Advantest than it has in a while (I’m not assuming currency impacts but this is drastic enough for the point to hold even if I did). The 2018 number is not comparable given the acquisition at the time.

Now looking at their price-performance: it’s been similar in the last 6 months, but lagging from a yearly perspective. I think this is justified, but find it interesting that in the last 6 months the price movement has been similar despite much worse fundamental results. There is likely a relative value pair trade here for the investors who like that sort of thing.

No strong view on Advantest to be gained here. It looks like they have regular cycles of taking share from and losing share to Teradyne—the two are currently neck and neck.

Advantest Segments

Advantest actually breaks out memory and SOC (system on chip) exposures - along with other services and support segment items. Mechatronics is really cool but very immaterial - a good wiki and podcast here.

Advantest of course sells primarily to Japan, but S. Korea and Taiwan are also meaningful segments. Notice China’s continued and persistent rise.

Income Statement (Apologies for the Blanks)

First I want to note that FY 2021 numbers at best are uninspiring, and the last year multiples have moved much higher despite low underlying growth. In the last quarterly review, I pointed out that testing has done the best globally of any subsector - so expectations are clearly part of it. There are lots of reasons to be bullish but this is a rally that could only be justified based on expectations—not fundamentals.

Margins and Profitability

I want to focus first on the ROIC / ROE numbers - which are awesome except for the periodic cyclical puke. Regardless the business looks good - but it’s trading at the highest multiple it ever has.

Cash Flow Analysis

The use of Capex has been ~36% cumulatively, but in recent years it’s interesting to see Capex become a smaller % of CFO. Part of this seems to be driven by expanding margins, so it becomes a smaller % of Cash from Operations. However, even when looking at a percentage of revenue basis, Capex intensity seems to have gone down. Compare this to steady-eddy Teradyne at ~25%. I don’t know exactly what’s driving that, but clearly, that has helped move FCF margins from MSD to ~20%. Is that sustainable? It doesn't seem like it from first blush - but there is likely something deeper driving this.

Their acquisition spree in the last two years also is meaningfully above average (and might explain the Capex gap) as acquiring new technology could make up for investing it yourself. The two most recent acquisitions are Astronics and Essai - both American companies that fit into their portfolio nicely as expansions of their ATE line.

Both companies pay out about ~40% in the long term of CFO, but Advantest prefers to do it in dividends while Teradyne prefers to buyback shares. Typical Japanese corporate actions like paying off debt and hoarding cash leave investors with a very cash-heavy balance sheet.

Valuation

Finally, valuation. Advantest on a forward basis is about as expensive as it’s ever been - even considering forward earnings. High 20s earnings multiple for a Japanese company is at the top of the range for what I’d pay, especially given lackluster results compared to its direct competitors. While forward estimates look to accelerate, I’m not exactly holding my breath here for Advantest. I would much rather own Teradyne.

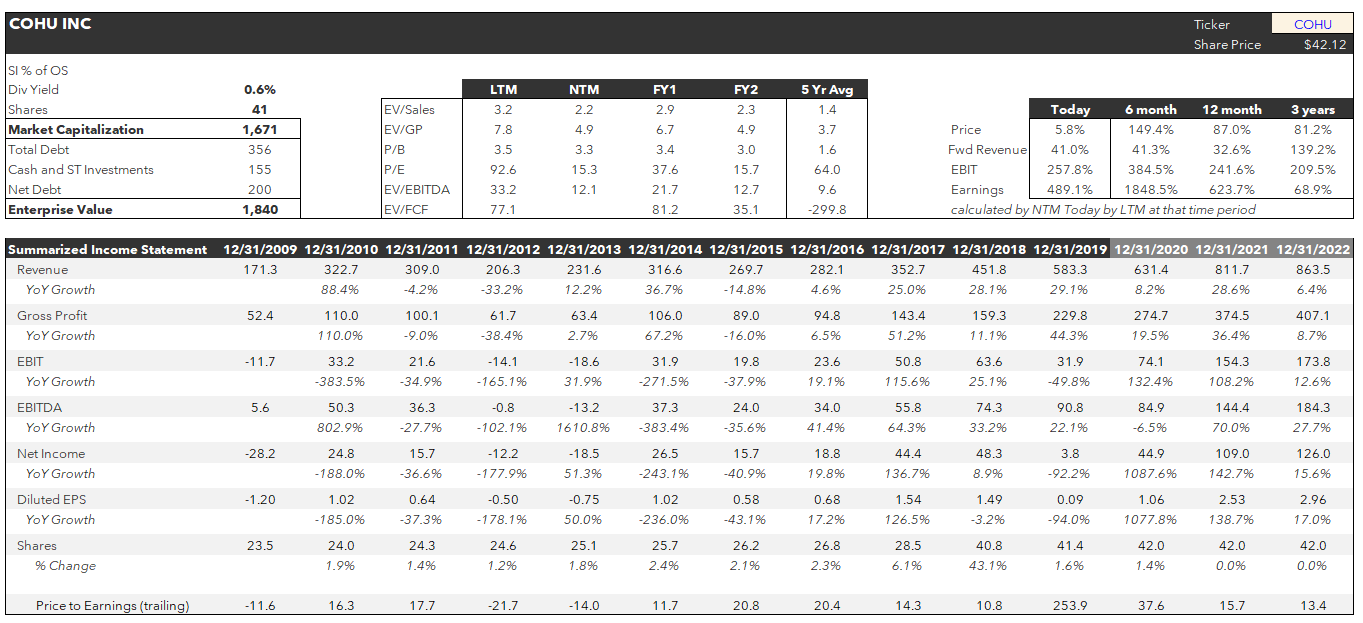

Cohu

Cohu is the distant third player in test behind Teradyne and Advantest. Cohu actually was the original Fairchild semiconductor test company that was the arch-rival of Teradyne back in the day. It got bought by Schlumberger during the conglomerate spree and was subsequently spun off in the early 2000s into its own company. There are some great slides from their deck.

This slide on testing intensity is helpful for understanding all 3 of the semiconductor testing companies, especially with regards to wireless test. The same drivers that contribute to mobile phone testing intensity right now will eventually drive 5G and IoT testing intensity in the future, specifically in the form of electronics comingled with Radio-Frequency devices.

Anyway, onto their financial profile.

Income Statement

Cohu is a much smaller and higher beta play on semicap. Their last year was one of the most interesting in the space. They were the clear testing winner in terms of price performance in 2020, but that was partially driven by how beaten down Cohu was at the beginning of the year. Cohu went to a single-digit P/E in March, had their numbers cut, and then proceeded to have a solid year and multiple expansion, exceeding dismal expectations. Quite the round trip.

In the last few years they have consistently grown, but that largely seems to be driven by the large 2018 acquisition. This is in stark contrast to the boom/bust of Teradyne and Advantest.

Margins and Profitability

What is most interesting here is that we 100% know that this business should be able to support ~50% gross margin, but it’s 1000 bps behind. This is a clear opportunity as they continue to scale revenue and incremental profit.

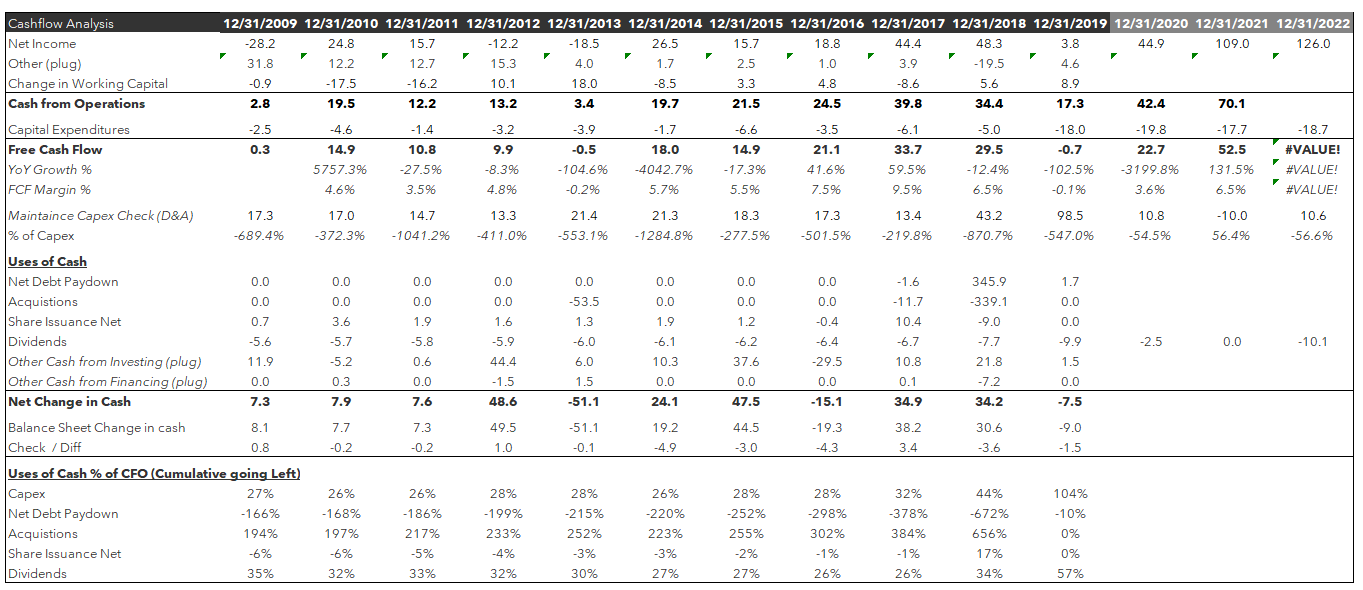

Cashflow Analysis

Unlike the steadiness of Teradyne and Advantest - their cash flow is a bit more acquisition focused with a secondary focus on dividends. The large 2018 acquisition was clearly transformational - and moved the company from no debt to ~340 million to finance the acquisition of Xcerra.

Valuation

Finally, valuation. Cohu had quite an exciting year in ~2020 with an 80% expansion in market cap. A large part of this was the meaningful estimate uplift, especially for FY 2021—but I really don’t have a strong view on this one either. Cohu is firmly the 3rd place player in a historically cyclical industry. That risk profile is going to get the returns it deserves—I don’t like buying the second-best, let alone the 3rd best player.

Formfactor

Formfactor differs from TER / 6857 / COHU in that it’s focused on a separate but similarly important part of the testing market: probe cards. Thankfully their IR team does a much better job with disclosure and their analyst day presentation has a pretty good layout of what they do.

Probe Cards

Probe cards are an electronic interface that serves as an electrical path between a piece of silicon and a testing machine (like Teradyne or Advantest). Probe cards are custom made for each piece of silicon and have the important task of verifying if the piece of silicon is working as it should.

Since probe cards touch the silicon, they tend to accumulate debris on the tip of the needles and must be replaced every so often. To sum, probes are highly custom and consumable products that are replaced over time and are being used at higher rates due to more wafer-level package testing. A youtube video showing the process is below:

The current shift to advanced packaging will result in a large number of varied semiconductor patterns and increasingly complex structures, which means that probe cards will see greater demand (volume-wise) and become even more mission-critical. Probe cards should and will win market share in the coming years for test products. They are a perfect play on the advanced packaging cycle and have more direct exposure than the traditional testing companies. Management is doing a very good job of expressing this:

And based on this somewhat dated market share estimate from VLSI, Formfactor is the purest play:

Management makes a strong case for why they should grow revenue meaningfully above the market and above competitors. It isn’t very farfetched given what we know about advanced packaging.

They believe that they can win market share in a growing segment, and I believe their focused pure-play nature will help.

At that higher revenue number, there will be margin expansion.

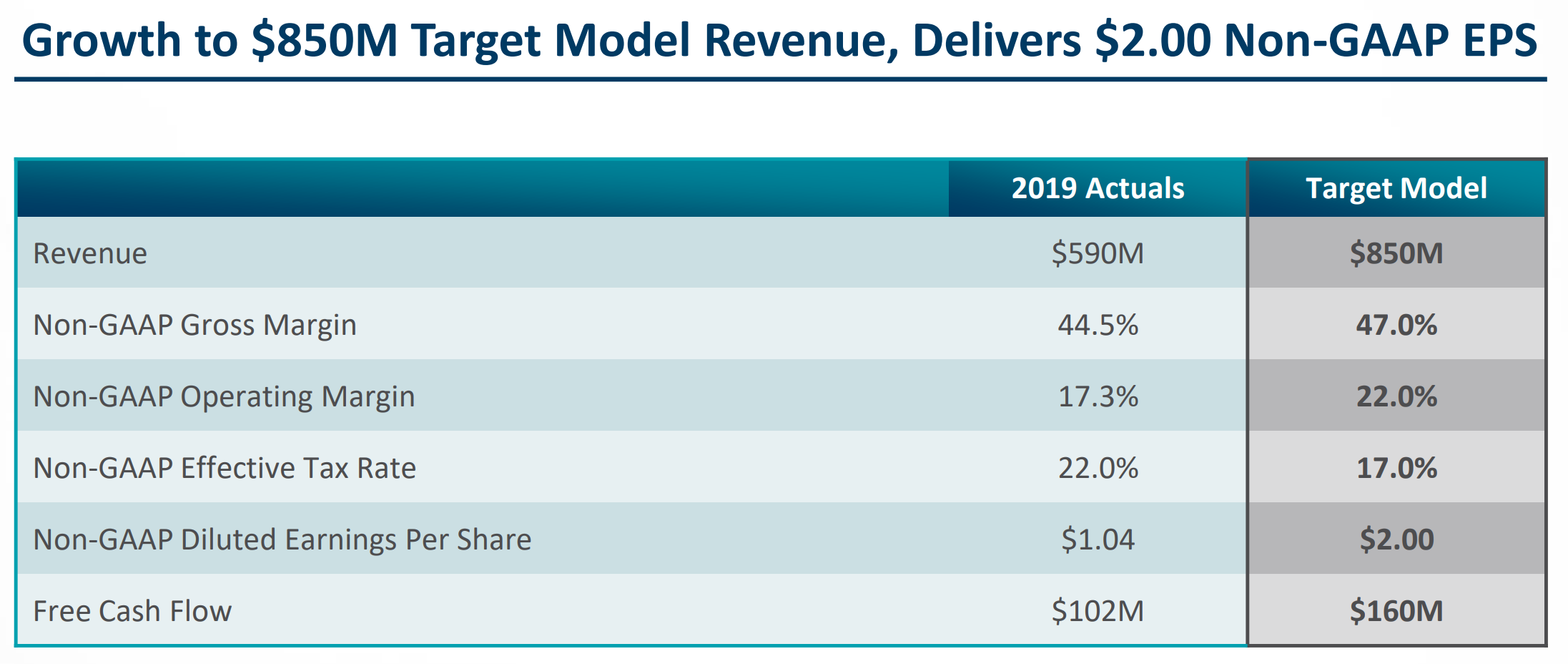

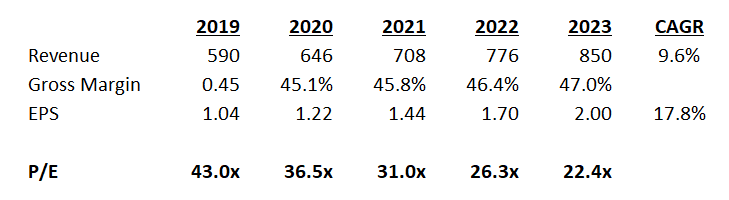

Let’s convert their guidance into a really simple spreadsheet - here I take management expectations literally and assume it happens in 2023.

The one worrisome aspect here is that the price seems to have outrun the given guidance. It’s trading at 22x the “target achieved” price. While I think long-term guidance is fairly conservative, I don’t think it’s this conservative, and even if we were to assume ~30%+ growth CAGR, you’re buying it at ~15x 2023 undiscounted earnings. That seems expensive.

Regardless it’s a secular winner, and worth keeping an eye on, especially for large M&A.

Summarized Income Statement

For a company growing revenue and EBITDA at ~15% / 28% in FY 20, 28x forward earnings look expensive relative to their history, but it’s worth noting that they are meaningfully more profitable than they have ever been, with strong gross margin expansion and potential for more.

This is what a shallow glance at historical numbers would be missing. Going from ~28% gross margin to ~45% today is impressive, but I don’t think anything stops them from hitting a 50% gross margin and ~25-30% EBIT margin. That is likely how the company is “cheap”—it would exceed long term guidance by quite a bit.

Margins and Profitability

Cash Flow Summary

Unlike most of our other steady growers here, FORM has never meaningfully returned cash to shareholders. I don’t think you should expect that to change given their growth opportunity. Frankly, I would want to see them acquire some of the smaller players and strengthen their position. Given their net cash position, it probably happens sooner than later.

Valuation

The business is an interesting growth investment, especially given the potential of incremental margin growth and the likelihood of Probe cards taking share in the test market. I do want the stock to chill out a bit, and eat into its multiple over the next few earnings. I’ll be following this one for a while.

Nova Measuring Instruments

Nova is likely the largest independent Metrology company globally outside of AMAT / KLAC. A friendly reminder is that Metrology is the step that happens immediately after the manufacturing process finishes. You “cut” the semiconductor and then you “measure it” to make sure the nanometer scale process step was correct.

Before we proceed further, I think it’s worth noting that I believe that Israel is a global metrology powerhouse and we should assume Nova and Camtek know what they are doing more often than not.

My reasoning is this: the last and most important metrology acquisition was Orbotech, an Israeli metrology company that was bought by KLAC (the global leader in metrology and inspection) in ~2019. Here is the slide from the announcement:

The thing that really turned my head was the Applied Materials acquisitions of Opal and Orbot in 1997. Both of these companies were Israeli metrology and inspection companies as well! Orbotech actually has a large chunk of ex-Orbot employees, and today Nova’s team has many ex-Orbotech people, including the CEO and the Chief Business Officer (?). The Chairman of the board is ex-Opal and ex-Optrotech (pre-cursor to Orbotech), and 2 other board members are ex-Orbotech.

What I’m trying to say is that Israel is likely the inspection capital of the world, and Nova is their current national champion. I once doubted the technical prowess of Camtek and Nova, but the evidence now makes me believe otherwise. It’s likely that they are credible challengers based on a geographic hotspot of knowledge that is better than anywhere else in the world.

Anyway, onto a quick primer about Nova Measuring Instruments.

Nova Measuring and Metrology

When I first started learning about metrology, I thought it was a single horse race featuring KLAC. However, after some time, I’ve come to discover that market share data is a bit hard to find and is difficult to reconcile with public presentations. My best guesstimate is that KLAC is approximately ~50% share of metrology, Nova is ~20%, and the rest is split among the remaining firms.

For Nova, I am going to use their estimate of ~21% in 2018 and a TAM of ~$4.285 million in 2018.

Competition here is partially driven by design wins, but switching costs are high and firms like to grow into a customer’s installed base. This means Nova is fighting an uphill battle. Even so, they’ve done a great job against the giants at Applied and KLAC.

There were a few acquisitions along the way, but it’s clear they have been doing a great job operationally. And I think given the Israeli dominance of Metrology, there is something here that’s driving that. Their core bet (also mine) is that metrology matters more as manufacturing scales to smaller geometries with more advanced packaging.

The opportunity for them is winning share through a focus on the steps in new processes. I think it will be difficult to win against the likes of KLAC, but they will likely gain share from tail donors.

All in all, NVMI seems like a credible company with promising technology, but quantitatively it seems to grow similarly to KLAC while trading a premium. This is likely due to a presumed acquisition bid—NVMI is a logical buyout for KLAC at any given moment.

This may not be the chart you want to see. NVMI should at least be putting up meaningfully better revenue growth estimates than KLAC to justify this premium fundamentally. Perhaps the market thinks that incremental margins are much better, but I can’t really square it away. Anyway, onto the financials:

The longer-term revenue CAGR is impressive and grows much faster than WFE (wafer fab equipment).

Margins and Profitability

Gross margin has expanded significantly over time and should be able to continue expanding. ~60% looks to be the gross margin cap achieved by KLAC, which I think Nova can get to if revenue doubles. The incremental EBIT numbers seem to demonstrate that at least ~40% EBIT margins are achievable.

Cashflow Analysis

The high amount of Capex last year is the first thing that pops out to me. They tend to buy back some shares but the capital usage is pretty conservative in my eyes.

Valuation

Yet another premium price, especially recently, but it seems somewhat reasonable given strong historical growth and buyout candidacy. It would be nice to see them buy out a company, especially Camtek (logic outlined here).

Camtek

Disclosure: I own shares of Camtek.

First I want to direct you to my recent write-up on Camtek. We will see if the merger between them and Nova is still on during the fourth-quarter results, but make no mistake: I still like Camtek as a standalone. There has been no deal announcement, but the stock has worked all the same. Think of a buyout as a put for this well-positioned company.

Instead of retreading the thesis here, I’ll have you refer to the appendix for Camtek or give the piece a re-read. I like the asset and I still think the company is well-positioned. Recently the stock price hit the premium I would have expected from a deal just on incremental good news.

Income Statement

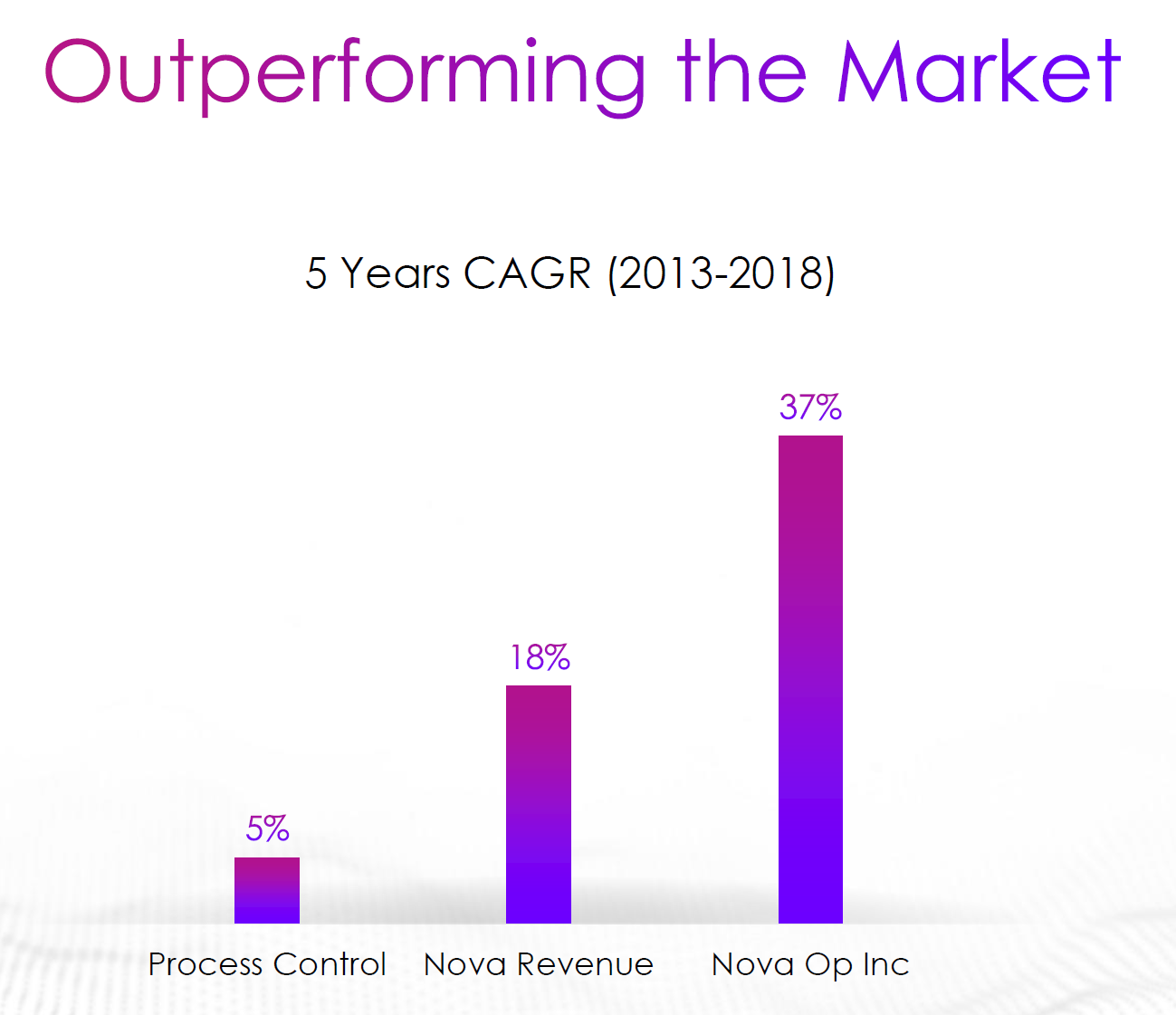

The best thing about Camtek is that they grew straight through the 2019 downcycle. Every semicap company in 2019 had revenue shrink except Camtek. This is confirmatory evidence that their products are secularly growing. If advanced packaging inspection continues to increase in importance, as I expect it to, Camtek’s business case will meaningfully benefit. The company itself has very poor disclosure, with random 8-ks of “new orders” and very little analyst coverage.

I believe that nothing is stopping this company from growing ~15% a year going forward, especially into 2021 on a strong WFE (wafer fab equipment) growth year.

Margins and Profitability

Once again, I am asking you to notice the beauty of incremental margin improvement. ~20-30% incremental EBIT on a mid-teens base is how this stock will continue to be “cheap” yet trade at premium levels on a forward P/E basis (there is 1 analyst covering this stock, so take the forward estimate with a grain of salt).

Cashflow Analysis

The company insists on paying dividends, which is odd to me given their size and express intention to do some kind of M&A. This likely is driven by a desire to pay their parent company tax-free dividends in Israel.

Valuation

It’s quite unfortunate (for us) how Camtek went from being cheap on a trailing basis to expensive on a forward basis. Frankly, the forward numbers are likely wrong given the aforementioned patchy analyst coverage. I do not have a strong view of forward numbers, but always keep in mind that this company is a secular winner in advanced packaging.

That being said, up 100% in a year is quite a run, and was more a function of its previous multiple than its future. The company sits in a weird middle ground of being expensive and strategic—I will likely hold it for a while.

Onto Innovation

Lastly, let’s talk about Onto, the result of the 2019 Nanometrics and Rudolph merger. They are the main competitor to Camtek’s optical inspection platform and the two firms collectively make up the duopoly in optical inspection for advanced packaging. This graphic below is great and puts together the rationale of Onto stepping out of the minor leagues and into the big leagues.

They cover a broad spectrum of products, but the acquisition rationale was to really create a strong competitor in Advanced Packaging.

It’s always easier to bring total solutions to market rather than be a niche player fighting complementary products.

A broad overlay of their portfolio is below. I’ll briefly mention what each does.

Metrology

Atlas System - Atlas is a traditional optical metrology tool that likely leans memory heavy. Interestingly, they use pretty advanced non-X-Ray optical technology, which is very helpful on the sub-scale (X-ray has trouble). The III system is for Gen 5/6 NAND, while Atlas V is focused on Gen 7/8 NAND and 1z-1yy DRAM and 3nm / GAA metrology.

The Impulse system is for CMP (Chemical Mechanical Polishing) process steps and is used in conjunction with other systems to verify the CMP process. The Impulse V system is an extension that is used for deposition, etch, and litho inspection as well.

Metapulse is for measuring layer thickness, especially in metal films. This is likely an advanced packaging type exposure, as more complex metal packages are delivered. There are a lot of specific applications so it looks like a broad tool.

The QS system was the least informative for their company display. It seems like it’s focused on measuring Epi (epitaxial growth, often silicon crystals deposited on top) and doping thickness.

Macro Inspection

NovusEdge looks to be an interesting tool that focuses on the edge, notch, and back sides of the semiconductor wafer. This is mostly pre-processing but post-doping (refer to the doping part in the lithography writeup). At this point, there are no patterns etched into the wafer, but the wafer needs to be measured to see if the layer was correctly applied.

Dragonfly G2 is a product that measures bump height—this offers direct exposure to advanced packaging.

NSX 330 System is another advanced packaging focused system with an emphasis on wafer-level metrology, micro bumps, RDL, TSV, and other processes. These are all discussed in the packaging primer and are all secular growth segments of WFE (wafer fab equipment).

Lithography

There are multiple Jetstep systems. Some are focused on lithography for display (a worse business) and some are targeted at advanced packaging lithography inspection. Don’t get too confused, as this is not a lithography business, just a lithography inspection business.

Software

Last but not least is the software, which management takes the time to highlight. I like thinking of it as comparable to enterprise software. Often it is not sold as independent units, but in tight cointegration with the tools. These are never broken out and sometimes can be bundled in services.

Summarized Income Statement

So first off, this template is not smart enough to appreciate organic revenue versus acquired and teasing out organic revenue out of the deal post-merge is pretty hard to do without a lot more work. Anyway, the good news is that we get to keep up with organic growth going forward!

The most interesting thing to note is that Q2 to Q3 saw a sequential decline which I believe is a large share loss relative to other players. They expect a large sequential increase next quarter and to “end the year with inspection growth over 25%” (that’s a specific segment, not the overall top-line).

This messy revenue post-merger is to be expected. In meetings with Camtek management has insisted that the merger of Onto created noise within the organization that Camtek will capitalize on. That advantage won’t last forever—the semicap sales process favors expansion from the installed base over specific areas of upselling—so Camtek will have to fight against a much larger competitor soon.

Margins and Profitability

Look at that gross margin compression! This is fixed cost leverage rearing its ugly head. A 5% revenue drop flowing into a 40% EPS drop is something you only get to see in Semicap (ain’t it beautiful?). However, notice that in the good times, the business consistently pushes ~30-40% incremental EBIT margin vs. the current ~ mid-teens EBIT margin base.

Cash Flow Analysis

I think that the FCF number is a mistake in my template so please ignore it.

Valuation

Last but not least: valuation. The thing I like about ONTO is that it seems the most accessible in terms of price and valuation—I’m comfortable paying this price if ONTO works. They are in all the right products and categories and have much more scale post-merger than they had in the past. ONTO is the company that I think I’ll be paying attention to the most going forward because I believe the set-up is very attractive: they’re going to hit a post-deal fundamental performance sweet spot, have had near term disappointing results, and are positioned well for the long term. The key metric to follow is share shifts: if they start to win share, I know it’s working.

Conclusions and Takeaways

In the near term, I think the testing and inspection segment of the market is running a bit hot and would like it to cool off for a bit before getting comfortable again (why yes I understand that these are famous last words).

I think Teradyne is fairly priced given its recent momentum, but am unconvinced it can grow sequentially through its large slew of recent orders. There will likely be an adjustment period sometime in 2021 for Teradyne that I think could prove to be a much better buying opportunity than today. Long term, Teradyne is well-positioned for rising testing intensity.

Advantest is hard for me to really parse through and I have been unimpressed with recent results. That being said, I will follow it closely. Might be a time where I take some bites of this apple.

Formfactor has the best secular growth opportunity of the testing bunch, as probe card testing intensity is expected to go up. I am not exactly a buyer here given its recent run and will wait for incremental fundamental news or a change in price before re-evaluating.

Nova Measuring Instruments is a strong contender and will likely be a player for a long time, but the valuation isn’t very compelling for me.

Camtek is a good firm, but I believe that the story is starting to become more appreciated given the recent price movements right around to where my projected “buyout” price is (see my piece about it last month). I still like the company and the end market, but have trimmed a bit on the run-up. The next big release should be earnings or right around that time.

Onto is the company I find the most interesting. It’s the cheapest of the bunch but obviously has had some operational issues in the near term. If you look at the history of these companies it’s weird for them to trade so out of whack. Onto isn’t a bad business by any means and is trading at a multiple turn discount. I’m constructive but not outright bullish quite yet.

KLAC is only being mentioned here at the end. I didn’t formally write it up earlier, but you basically know what it does. Just take the metrology explanation for Nova and Onto, pump up the market share %, and you’ll arrive at KLAC. Despite their much larger share and scale, they trade very undemandingly, even on an EV/EBITDA basis. I think this is one of the few times the large-cap business in the industry looks better than the small-caps—and KLAC is really a wonderful business. I think I’ll cover it later in a piece specifically about process control.

APPENDIX

Questions for Management

Teradyne

Ask about Universal Robots segment acceleration - what they think the total size could be there

Ask about packaging trends in the near term and if they have any opinion on probe card versus testing

Can they quantify testing intensity increases? What would that look like for Teradyne?

How did they win so much share relative to their competitor when testing at large seemed very placid this year. Ask specifically market share dynamics between SoC and Memory

Advantest

Ask about packaging trends in the near term and if they have any opinion on probe card versus testing and why they sold it to Formfactor if its going to grow above average - ask about advanced packaging specifically.

Can they quantify testing intensity increases? What would that look like for Teradyne?

How did they lose so much share relative to their competitor when testing at large seemed very placid this year. Ask specifically market share dynamics between SoC and Memory

Ask about Mechatronics as it’s grown consistently as a part of their business (this is their UR)

Formfactor

Probe card testing is going up - how does this impact their TAM

Do they have thoughts on acquisitions? There seem to be a lot of niche players that seem like viable targets?

Who are the biggest competitors that they are worried about?

Nova Measuring Instruments

Ask about acquisition plans since they have been so open about it

Where do they see market share gains come from? Ask them “why do you win”

Ask about long term end state margins and where they could see EBIT go with subsequent revenue size

Camtek

Ask about what they think about being acquired (Moshe will actually entertain this question)

Ask about what they think their market share is - how is Onto integration going for share gains and losses

Ask if they have any traction into leading-edge segments and how large do they think leading-edge inspection could be? They tend to size the market this year - so ask what forward revenue growth could be as well

Onto

Ask them about the deal rationale, expected synergies, what do they think they can accomplish together they couldn’t do apart

What is the run rate revenue growth possible between the two businesses, and what revenue synergies they have seen so far?

Frankly ask them what have they learned being a larger company so far

You mentioned above about Advantest owning share in the probe card market, is this still true after Formfactor had acquired their advanced probe card assets? I was under the impression this was the entire business as it was no longer viewed as a strategic asset for Advantest, or did Formfactor only acquire a specific part of that business?

One correction needed I think (I know it's an old post... sorry!) Universal Robots is owned by Teradyne and isn't a competitor.