Quantifying the Adpocalypse

Someone is off sides - advertising revenue in the time of COVID

Disclaimer: Nothing is investment advice. Also, this will be different from my past pieces and much more financially focused.

In my extremely noisy twitter feed over the last few weeks, there is a single thread that I keep coming back to. Advertising and digital advertising especially would be different this time than last. And as far as I’ve seen it, it would suffer a very significant contraction for some common sense reasons. The stocks so far seem to think otherwise, and I just wanted to start with a very simple build-up and then comparison to sell-side numbers. While some revenue cuts have come, large-cap digital advertising to me seems to be living in fantasy land. The companies themselves have ample cash, extremely durable platforms, and are going to survive. We just need to check some expectations at the door. Let me walk you through what I am thinking;

The Inescapable: Advertising is Cyclical

I guess the first debate is the secular versus the cyclical aspect of digital advertising. Many could point to the 08, and the ability of google to grow during that downturn. I would point to penetration. Digital advertising is now the largest segment of advertising and will suffer if advertising suffers broadly. I believe they will do relatively better than traditional TV, but COVID comes for all.

If the historical relationship of cyclicality holds still, there is no way you can justify positive advertising while GDP growth estimates for Q2 / FY2020 with anything positive in terms of revenue growth out of digital advertising giants.

Digital Advertising is Liquid Opex Cuts

Unlike committed spend to now canceled events, programmatic (the preferred way to buy digital ads) is liquid. Anything that can be cut will be cut, and what’s liquid is a great place to start.

A quick reminder, programmatic is the term used for buying advertisements on demand. Each time your screen loads with Facebook ads, Facebook auctions off your eyeball’s value to an advertiser. The advertiser bids on the ad inventory based on how much it is worth it to them knowing information about you provided either from Facebook targeting or first-party data you bring to the platform. These bids are near real-time. What’s also great is if you are now not able to sell your product (travel/retail), or your product is discretionary and your customer is uncertain or affected (auto/discretionary purchases), you can turn that hose off.

Now imagine you are one of the many companies impacted by COVID. Your revenue is down a ton, you are forced to do layoffs, do you think you protect a super liquid discretionary opex line item before everything else? If you’re a test budget or further down the chain of unproven advertising inventory, or just not meeting ROAS, turn it off. It’s that simple. Below is a simple graphic of what is the first and last to go from right to left (sorry).

This graphic is directional, each platform varies in its usage

Note the inverse side of this as well, If the economy has a quicker than expected recovery the ad dollars can be quickly turned on. If there was a very quick recovery, ad digital ad spending would be quickly turned back on in ways that ad commitments to large TV-based events couldn’t be. But that depends on what the shape of the recovery will be like.

Usage is up, Revenue is not up

There are a variety of sources that point to it, but clearly, usage on social media and many digital channels are up. I’m going to use the Verizon report as my base case, that broadly web and impressions are up ~25%.

So we can guess that inventory/impressions are up 25% while assuming the same ad load, it means you will be served more ads. You may even click through more, but if you do not make the final purchase, advertisers will be less likely to pay for the lower conversion. Importantly consumers must have the willingness or ability to purchase the items. There is a marginal return on seeing more ads in your feed, and it makes sense that CPM rates would fall as inventory (supply) raises and demand (purchase intent) falls.

If I lost you in the AdTech world, all you need to take away is there are massive negative marginal return rates on ads in your feed. Being bombarded by more ads does not mean you will make more purchases, and even with higher usage, there is a world where we have more impressions but less spending.

I like this succinct quote from former AOL CEO which sums it up nicely

“For the first time in history, you’re probably going to have the highest point of media usage in the history of the United States and the lowest point of advertising in the U.S.”

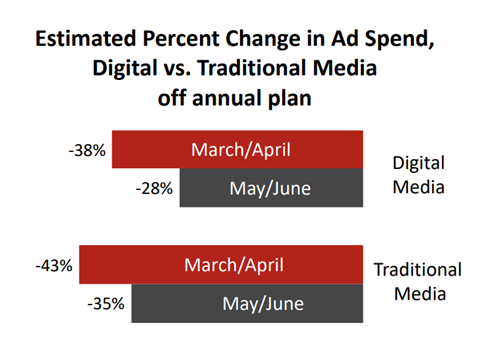

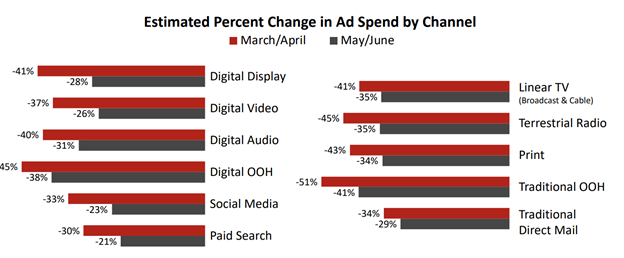

There’s Evidence We’re Already There

This is going to be the anecdata section, and while there is data everywhere it’s hard to have a representative sample size of a 200 billion dollar market. I think the key ones that I feel comfortable relying on are the IAB survey, which is a meta survey and probably the largest sample size we have. Some high-level survey results are posted below. I encourage you to click through.

A reminder that the math is the advertising cuts assumed in the IAB survey is the contraction from previous spend estimates, which I’ll use a +15% YoY napkin math number for. Assuming this is indicative of total advertising spend, and that ad spend in digital was +15% YoY before, this would broadly mean a ~29% contraction in March/April, and a ~17% contraction in May/June. Assuming monthly ad spend is equally weighted, this is a -20% ad spend for digital in Q2.

I am going to post some more sample sizes that are “making the rounds” and some things I found interesting.

Other Links & Quick Summaries

The Online Ad Revenue Index

This is a rough proxy for publishers on display ad rates over a supposedly large sample size over the ad sense network. This is a good proxy for the “Google Network Member” line item on Google’s income statement. It’s down ~40% YoY.

Socialfulcrum on what they are seeing on Facebook:

CPM down ~45%

CTR unchanged

CPC down ~45%

Onsite Conversion down 53%

Overall, Cost of Customer Acquisition up 28%

Within Retail and what they are seeing in Google / Facebook

Omnichannel Facebook spend is up, while Google spend is down

Pureplay Ecommerce is down ~30%, with Google down more than Facebook

Fashion is down with Google spend down more than Facebook

Essentials spend is up, with Google up more than Facebook

Luxury spending is down, with Google and Facebook similar spend

They manage ~$500m in spending

Tinuti on what they are seeing

Impressions are up massively, with 60-80% during the second half of March

CPMs are down, conversion is down

For them still growing Y/Y for Facebook / Instagram

Amazon growing teens spend

Google Spend declines Y/Y as conversion falls

Adexchanger Round up on impacts

Bustle, G/O media, Maven Media, and others are laying off staff

40% decline in programmatic CPMs

Adthrive – Less bad than expected on Q2 Day 1

Twitter Update

While the near-term financial impact of this pandemic is rapidly evolving and difficult to measure, based on current visibility, the company expects Q1 revenue to be down slightly on a year-over-year basis. Twitter also expects to incur a GAAP operating loss, as reduced expenses resulting from COVID-19 disruption are unlikely to fully offset the revenue impact of the pandemic in Q1.

Facebook Update

Much of the increased traffic is happening on our messaging services, but we’ve also seen more people using our feed and stories products to get updates from their family and friends. At the same time, our business is being adversely affected like so many others around the world. We don’t monetize many of the services where we’re seeing increased engagement, and we’ve seen a weakening in our ads business in countries taking aggressive actions to reduce the spread of COVID-19.

Pinterest Update

“The near-term financial impact of this pandemic is rapidly evolving and difficult to measure and quantify. First-quarter revenue performance was consistent with our expectations through the middle of March, when we began to see a sharp deceleration. Fortunately, despite weakness across nearly the entire advertising market, our exposure to some of the most affected segments like travel, automotive, and restaurants has not been significant"

To be fair to Pinterest, I’m impressed with their relative strength.

Amazon, Walmart Suspending Marketing Deals

Amazon and Walmart have temporarily suspended commerce marketing deals with digital media firms such as BuzzFeed, two people familiar with the situation said.

What’s more interesting are these companies are thriving during COVID, which creates an interesting situation. Some companies have such strong demand pulls there is no reason to advertise for demand creation. If you’re forced to buy something online, you’re going to be searching on Amazon.com, not on Google. Other smaller eCommerce companies such as Zooplus have paused spending as well.

Booking and Expedia Alone Can Account for Meaningful Decline

The travel giants account for single digits percentage of revenue for Google alone, and many other large customers are likely not spending anything during this period as well.

Summary: There are a lot of small sample size bets and updates from companies that seem to support there is a significant contraction in ad spend in late Q1 / Q2. While the recovery debate rages on if it is a V shape or a U shape, it’s clear that there is a material impact on revenue. Let’s lastly compare to sell-side estimates.

Sell-Side Consensus and Reconciling the numbers

So this brings everything to this, how the hell can you possible reconcile everything above with what is below? How can any AdTech platform post 1) flat Q2 numbers 2) positive FY20 numbers? I believe bottom-up estimates are wrong.

This is based on Bloomberg consensus right now as of 4/8/2020. Ty @son2dweeb for help on this.

I have a hard time believing these numbers. It could be that buy-side is already ahead of the cuts but with this much uncertainty, it’s anybody’s guess. I think that in the coming days this debate will be solved into earnings, and I guess is that the above numbers are exceedingly optimistic. I think we have quite a gap in expectations here, and either everything I’ve highlighted above is wrong, or we need to be checking our expectations right now.

My guess: Advertising is broadly down 20% in Q2, with social outperforming search as of the end of March. As we continue and more discretionary purchases wane, social will become more in line with the average digital advertising cuts.

While the above IAB estimates look drastic, I would guess smaller brands and SMBs are impacted even worse. Facebook and Google are materially exposed to both. I believe ad spending intent will slowly pick up as we recover, not quite following for the first quarter or two, but eventually outpace the economy next year.

Time and the shape of the recovery will tell if this becomes true or not. I hope everyone is well in this uncertain time. If you found this post helpful, liking or sharing it is appreciated!

Now that both GOOG and FB have reported their earnings, it would be interesting to see an retrospective analysis taking those numbers into account.

Clear from the above that you are thinking like a jr buyside analyst and not a seasoned PM. Everyone knows Q2 numbers will be terrible and sellside consensus is way off. That doesn't matter. What matters from here is the shape of the recovery and what rev / EPS looks like in 2021 & beyond. Stop trying to look backward and explain how we got here. Stocks discount what is happening in the future. A more insightful post would be trying to frame the shape of the recovery and how those expectations are discounted differently across the advertising exposed public companies.