Semiconductor Earnings Blurbs for the Week of 10/16/2020

ASML and TSMC start the season off, here are some high-level takeaways

ASML Thoughts

While sometimes ASML can have interesting tidbits, I think ASML’s earnings release is one of the biggest snoozefests in all semiconductors/ semicap. EUV is inevitable, it looks like some orders got recognized this quarter. Despite some previous delays, they feel comfortable guiding to double-digit revenue growth in 2021, mainly driven by EUV (expected to grow 20%).

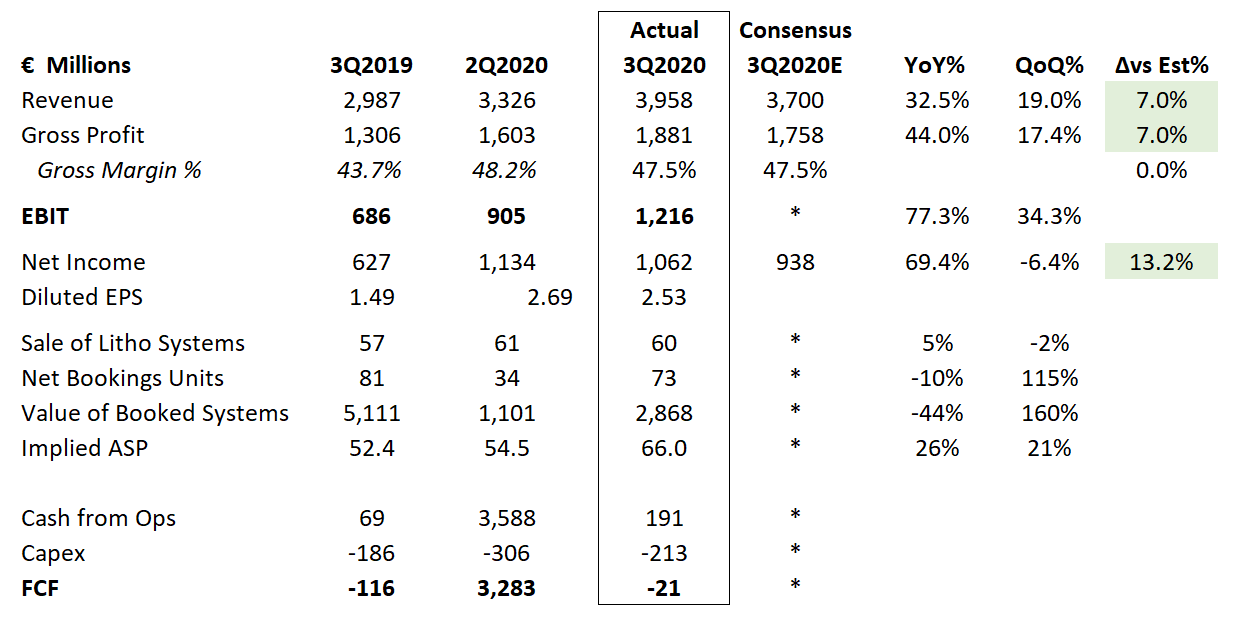

For those of you who are really paying attention at home – here is a quick 1-page earnings summary versus consensus.

Nothing really sticks out to me. I only have consensus for Revenue / Gross Profit / Net Income, but it was a clean beat across the board. ASML is doing what it’s supposed to do, be a boring compounder, growing revenue at double digits, and EBIT a bit faster. It’s multiple is a bit elevated, but it’s a monopoly trading at 35x. What’s new? Oh, wait before we go this chart from their presentation was interesting.

Oh, one thing I do want to note here is that memory kind of fell off a cliff this quarter. There will always be quarterly fluctuations between segments, but part of the growth story is contingent on higher penetration into the memory market.

Let us compare that to the recent jitters in memory land from Micron’s earnings

“We expect calendar 2021 industry DRAM bit demand growth of approximately 20%. We further expect that disciplined industry CapEx will result in improving DRAM market conditions and industry profitability throughout calendar 2021.

Calendar 2021 industry NAND bit demand growth is expected to be approximately 30%. Unless industry CapEx moderates from current levels or demand exceeds our expectations, we see a risk of challenging NAND industry profitability levels.”

-2020 Q4 Micron Earnings, Sanjay Mehrotra

For some context, this was kind of a shock to expectations at the time. DRAM strong, NAND weak, and maybe even unprofitable. While DRAM is the segment most concerned with EUV, spillover weakness in NAND could cause the memory players to freeze DRAM CapEx budgets. Just food for thought.

I don’t have any strong views on ASML, MU, or others here – just some things to watch and a higher level takeaways.

Also, a good time to point you to a write up on NAND industry dynamics in the coming years. I think this counts as a prediction gone right and is something any memory investor should be thinking about. I believe that YMTC will continue to absolutely destroy the stable industry dynamics, and I’m very cautious about that end market.

Read more here: S/o to @dylan522p

https://semianalysis.com/the-impending-chinese-nand-apocalypse/

TSMC Thoughts

So, my remark on ASML being boring could not be further from the truth for TSMC. TSMC is like the sun, and all the world’s semiconductor companies orbit around it. Whether if you compete against it (Samsung, Intel, Global Foundries), or you are reliant on it (everyone), what TSMC says and does matters. TSMC’s CapEx budget is pretty much the Semicap industry’s revenue. TSMC’s node ramps are pretty much how quickly the world gets to the next node. So, in summary, TSMC really freaking matters. With that context let us look at their results and outlook.

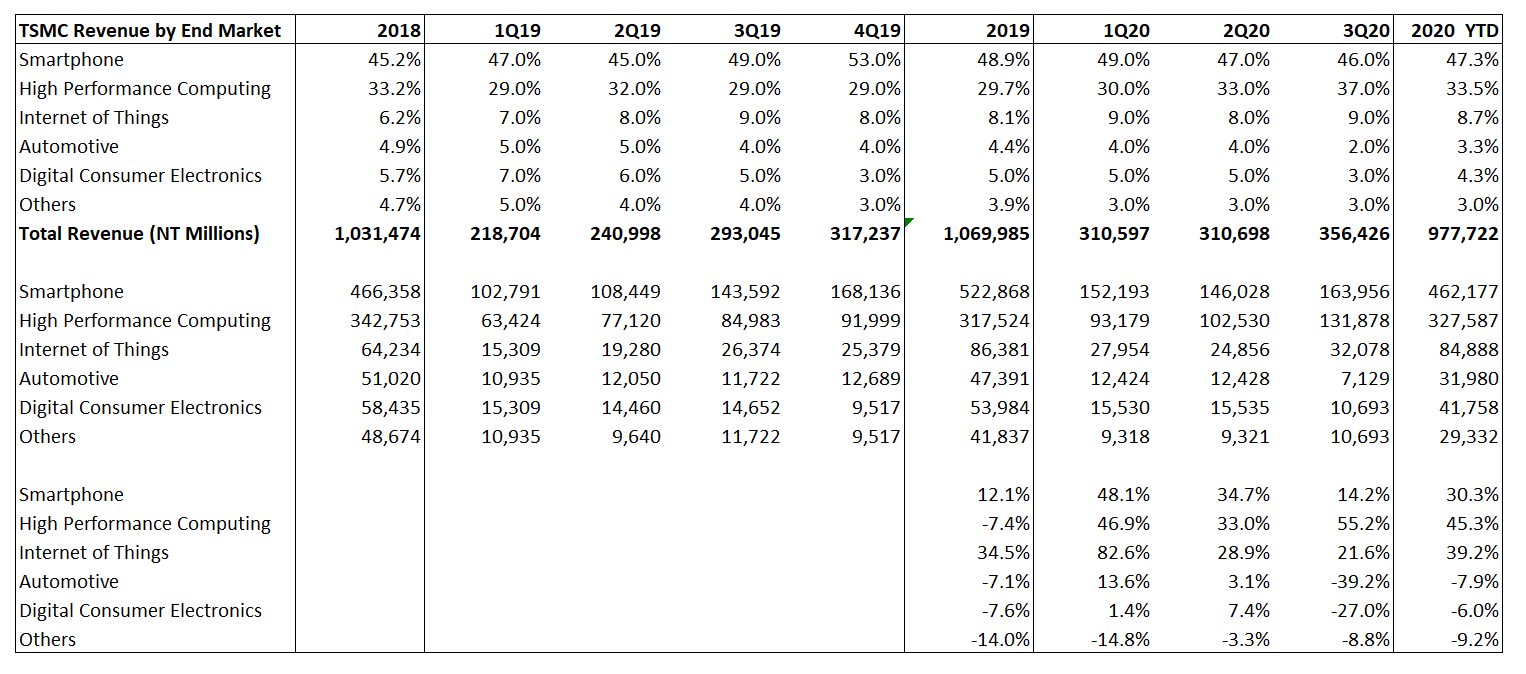

End Market Analysis

Sadly, for TSMC, there is not much benefit of doing an earnings 1 pager. They do monthly revenue, so if you are shocked, I guess you don’t really pay much attention. I think their high-level outlook is very important, however. TSMC is the single largest producer globally, and they tend to report earlier than others. This is one of the cleanest signals of end-market strength globally.

Simple takeaways are Automotive bad, HPC really good, Smartphone meh, IOT okay, Digital Consumer electronics bad. Automotive to me is the most eye-catching, as it has fallen off a cliff QoQ and YTD, Smartphones weakening, and unsurprisingly the only strengthening segment is HPC. This likely reflects large customer ramps, especially the likes of AMD for the gaming holiday season, but more information will confirm or deny these data points.

Some other forward-looking tidbits that I’m going to pull directly from the call are as follows:

On what is the fastest-growing segment

Okay, let me answer the question. We do see HPC platforms growth rate is higher in among our 4 platform, which is smartphone, HPC, automotive and IoT. And in the next few years, we continue to expect what we forecast, that HPCs growth will be higher than the corporate level. When it will cross over, I don't make any comment right now.

On mix next quarter

Okay, Bruce, we're not prepared to comment on geographic allocation among revenues in the fourth quarter. I can share with you that we expect the platforms that will grow in the fourth quarter will be smartphone and automotive, and the other 2 will likely to be down.

On HPC over the next several years

We don't break it down or disclose the platform mix of certain nodes, but we can share with you, as C.C. just mentioned, in the next several years, we expect HPC to be the largest contributor of our growth. So that should give you some idea. And these guys use advanced technologies.

On Advanced Packaging

Yes. Bruce, the growth of our advanced packaging in this year is close to the corporate but not as high. In this next several years, we do expect that on a CAGR basis it will be faster -- it will grow faster than the corporate average. And in terms of margins, its margins is lower than the corporate. However, its investment intensity, capital intensity is lower. Therefore, on a return basis, ROIC basis, it is acceptable to us.

Remember the absolute bullishness in the magnitude and duration of HPC for later. This is a core “you should be long this” theme.

On 5 Nanometer

Next up I think the other important point is that 5nm (or N5) is here!

It is not super meaningful currently, and it is likely to be a slower ramp than 7nm since it’s looked upon as a partial node, but it’s here and it’s shipping. TSMC charging forward while Intel is still at 10nm+++ should be terrifying Intel investors and delighting TSMC shareholders.

But for now, N5 is going to be a larger part of revenue next year, going to be margin dilutive in the near term, and likely in the very long term just as profitable as corporate average. And on N3, risk production starts in 2021, with a goal for volume production in 2022. What a time to be alive!

On Capex

Also, of note is their Capex guidance looks to now be at the top of their annual range. I remember them lowering the midpoint during COVID and thinking “what the heck aren’t they capacity constrained?”. I’m happy to see it up because this bodes well for Semicap, but more importantly, bodes well for TSMC.

TSMC is currently the most dominant global fab, and its ROE/ROIC numbers are impressive and improving. Improvements recently are more a function of the semiconductor cycle than of their competitive advantage, but importantly I would say qualitatively their moat has expanded quite a bit since their last 2016 ROE cycle high. I believe that in the next few coming years we could see a new cycle high for ROE/ROC numbers – and if TSMC feels confident that they can invest $17 billion USD at similar (or better) returns, as a shareholder you should be rejoicing. That is the most “money good” investment I am aware of.

If you enjoyed these quick little earnings blurbs, feel free to share on twitter some screenshots. Thanks to anyone whose reading this, and I look forward to putting forward better analyses going forward. This is just some quick thoughts on earnings for those who follow the industry from a high level.