Semiconductor Outlook in 2021: It's Shaping Up to Be a Good Time

Plus! looking at Memory cycles from a long term perspective, and ideas that look interesting into next year

I know all the sell-side banks do a 2021 outlook around this time. While I think the practice sometimes can be silly, consolidating narratives and themes into one place and reviewing the year past is often a good practice. I’m going to summarize how I saw 2020, and what I think 2021 will look like.

2020 was a Surprisingly Good Year for Semiconductors

Additionally, SIA today endorsed the WSTS Autumn 2020 Semiconductor Market Forecast, which projects the industry’s worldwide sales will be $433.1 billion in 2020, a 5.1 percent increase from the 2019 sales total of $412.3 billion. WSTS projects year-to-year increases in 2020 for the Americas (18.7 percent) and Asia Pacific (3.8 percent), with decreases projected in Japan (-0.6 percent) and Europe (-8.4 percent). In 2021, global sales are expected to increase by 8.4 percent.

The semiconductor index also had a surprisingly good year, beating even software-focused ETFs (IGV). But under the performance at a high level, semiconductors had a great fundamental year considering the global pandemic. Notice PBW (clean energy) - as many companies in the semiconductor industry are applicable here.

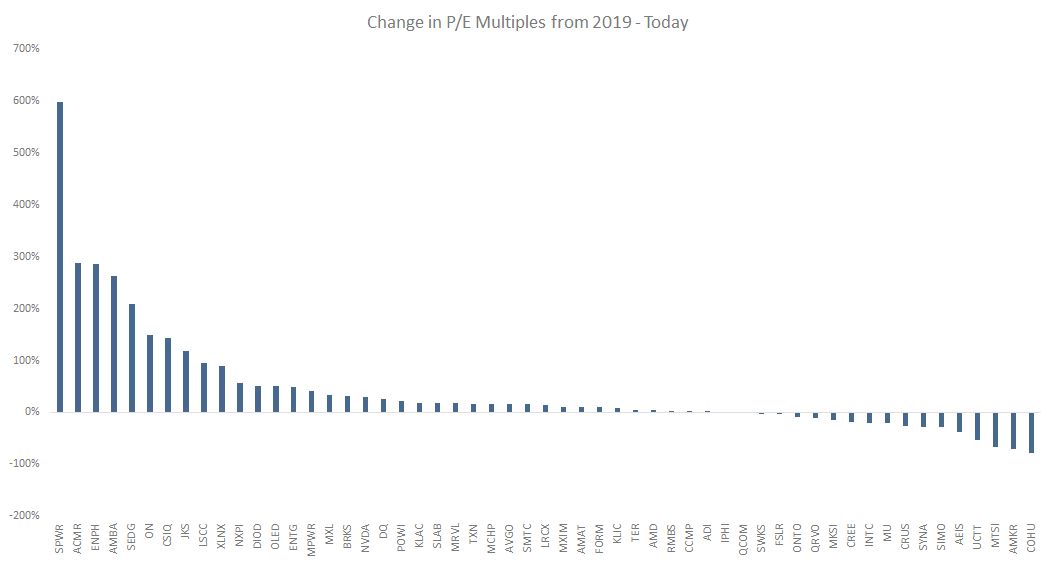

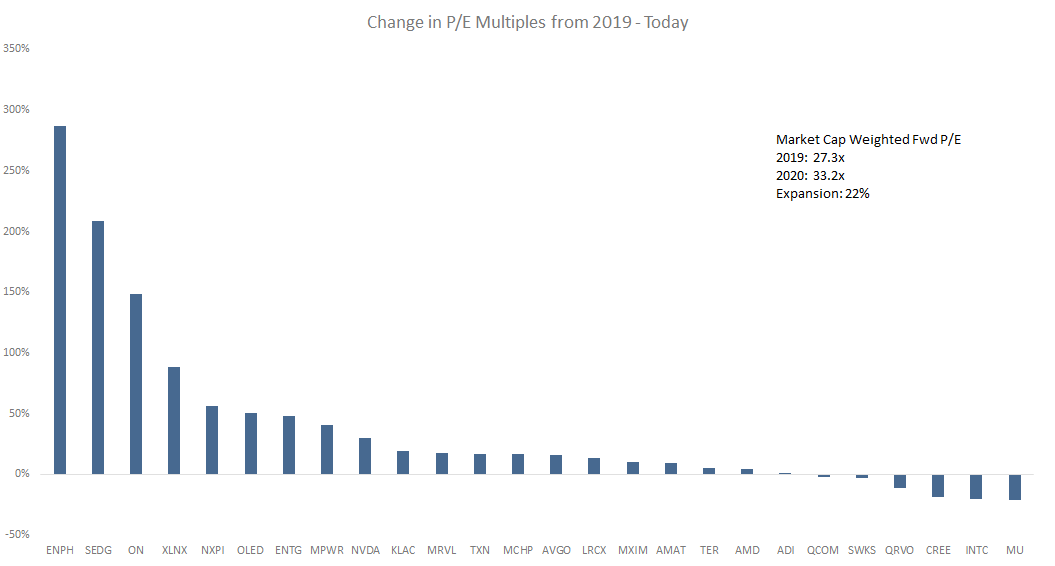

Multiples this year of course expanded. I only counted the domestic companies, but the market-cap-weighted multiple expansion is around 22%, which is less than the S&P 500 multiple expansion this year.

Pretty hard to read this - so I did a 10 billion dollar filter and the chart is below.

Of course, the largest multiple expansion was either due to solar and the subsequent massive ESG rerating, or related to power and tangential exposure to that same theme. Note that even stand out companies with very high multiples such as Nvidia did a paltry 50% multiple expansion compared to the likes of ENPH/SEDG.

But it wasn’t just earnings expansion in 2020. Under the hood 2020 actually was a year of revenue acceleration in market-cap-weighted terms. Mostly this was due to 2019 being the bottom of the previous semiconductor cycle.

What’s more interesting is that next year (orange) looks to be another growth year for many companies. Everything is sorted by 2020 growth (notice it isn’t organic - CREE divested a company), but most companies are expected to at least continue to grow but decelerate. These are sell-side estimates so of course, they are a bit low so there is room for beats.

Frankly, the most impressive part is the EPS growth for me. The average company meaningfully expanded margin this year, and next year it expects to continue to do so.

I think from a fundamental perspective this year was very strong, and partially that is driven by 2019 being the bottom of a semiconductor cycle as well as COVID-related demand pulls.

Let’s move onto the qualitative drivers of 2020. I think we can summarize 2020 broadly by these themes:

The huge digital boost from covid supported many segments, especially cloud infrastructure, personal PCs, and home devices.

Geopolitically this was the most important year for semiconductors yet, as China and the United States duked it out for more control over silicon.

Automotive was the clear industry loser, as sales declined due to covid closing dealerships and many staying at home thus not needing cars.

Renewables mostly driven by Solar was the clear outstanding winner, and sales and multiples accelerated

Intel was the clear loser, while Nvidia, AMD, TSMC, and surprisingly Apple look to be the winners at Intel’s expense. There are many more names, but the broad narrative was focused on Intel’s void.

I think what is more interesting is obviously not the past, but the future. We are going to discuss where the current trends will extend and where some end markets may reverse. So far, industry experts expect acceleration - and I agree.

The Trends That Should Continue into 2021

The things that I think will not change and only be exacerbated in 2021 by an eventual recovery are as follows.

China and the United States will not stop their tit for tat escalation, but Biden is somewhat of a welcome respite from Trump. The reasoning is this: There are likely to be increased licenses, and Anti-China is bipartisan, but the issue was Trump was erratic. At any given point, China / US trade could jerk one way or another, and I think Biden will continue the path but decrease the volatility. Things won’t normalize, but there will be a new normal.

Intel will continue to lose, not just because of process issues but because of the rise of the revolution in Semiconductors. The benefits of Heterogeneous compute are here, and the large tech companies are not going to be stopping anytime soon. Intel’s future losing will be more a function of ARM and accelerators than AMD, but AMD will not be stopping in 2021.

This means that many of the processes that support the rise of this new style of compute, such as advanced packaging, 3D chips, and 2.5D chips are going to become more important into next year.

Strong demand vectors like AI and 5G will not abate. We will likely see something that is as headline-grabbing as GPT-3 was this year, and start to appreciate the compute intensity of AI more and more. Check this tweet out about the recent Alphafold announcement. Each time a protein is folded, there will likely be a significant semiconductor tax, often in the 10’s of thousands of dollars.

Victorious Cake@victoriouscakeAlphaFold only used 128 TPUv3 cores over a few weeks to train itself (equivalent to 100-200 GPUs). Pretty remarkable. "AlphaFold develops strong predictions of the underlying physical structure of the protein and can determine highly-accurate structures in a matter of days."

Victorious Cake@victoriouscakeAlphaFold only used 128 TPUv3 cores over a few weeks to train itself (equivalent to 100-200 GPUs). Pretty remarkable. "AlphaFold develops strong predictions of the underlying physical structure of the protein and can determine highly-accurate structures in a matter of days." 8:24 PM · Nov 30, 202011 Likes

8:24 PM · Nov 30, 202011 Likes

The Things That Should Change in 2021

But not everything stays the same, I think there are some big change points that are in focus for me.

Cloud computing will have a digestion year. The first half will still likely be strong, and the comps for Q4/Q1 are soft, but Q2 and onward will have some kind of growth abatement. This is healthy and normal, and if you are long term minded this is nothing to be concerned about. I do not think that Cloud will shrink, just relative growth rates will decline. This doesn’t mean their net new dollars will shrink.

Automotive looks positioned for a strong year as demand comes back, and we are already seeing signs of shortages. Analog and other devices should benefit, not only from the increased penetration into auto, but volume as well.

The Memory market may finally fix itself, and my memory outlook is that supply and demand rebalance, and we could potentially see the “hard” part of the memory cycle. I characterize the hard part of the cycle as supply shortages, followed by price raises, followed by massive profits that are reinvested into semicap, thus increasing supply and eventually lowering prices. Memory has been uncharacteristically quiet since the last ~2018 cycle, and 2021 has the potential to remind them of what a party looks like. Note that Micron has already raised numbers multiple times so far in the back half of this year.

If the above is true, I think we could easily see a 10%+ maybe even mid-teens growth year in WFE (Wafer Fab Equipment). Tokyo Electron believes that we will see 10% for 2020, and frankly, this year was tepid compared to what recovery could look like.

The Things that Worry Me in 2021

Despite all this and a very rosy outlook compared to most, the things that worry me boils down to a single variable that is out of my control: China.

A really good thread or person to chat about the risk of war in the pacific is Fritz at https://fritz.substack.com. Some of the things there scare me, and I frankly don’t know how to handicap a worst-case scenario at all. But I do note that the temperature in the room slowly rising scares me.

It goes something like this. China is rising quickly in the world and wants to cement its lead by owning a very important item in its supply chain, semiconductors. They have all kinds of plans to do so by 2025, but realistically they can reach semiconductor independence only if the United States lets them. This applies specifically to EDA tools and Semicap.

The United States sees China’s rise and a very strong potential chokehold and can strong-arm (hah!) their development for 10 years by cutting off their technology access. So they hold back as much as they can and throttle China’s ability to pursue independence. This would be a game won for the United States if there wasn’t for one little thing called Taiwan.

Taiwan is geographically close to China and makes this complicated. China owns the geopolitical sphere there, and additionally, they can achieve all their goals at least in the near term in one terrible fell swoop.

Sure the US could rebuild, but it would take years while Taiwan was occupied and gives China a very hefty near-term advantage. If Taiwan was seized it would instantly put the impetus on the United States and we would be forced to retaliate or break our entire supply chain in ~6 months. There even is a twisted metaphor to be found with Oil and Japan in WW2. The thing I like the least about this is that I understand how both players will and should act in their self-interest, and it could lead to a mutually assured terrible outcome. I’m nervous, but to be honest this is completely out of my pay grade. Any de-escalation on the back of Biden will help dissuade fears. Part of the recent rally has been the assumption that Biden will be nicer to China and normalization will begin.

The End Markets and Companies in Each

Please do not take these as recommendations, something I find over and over is if you have a very public long-dated “pitch” it ends up being terrible. And often the third-best idea that you’re too ashamed to pitch publically is actually the one that works. I am just going to categorically state end sectors and companies that are exposed and what looks interesting or worth a deeper look.

Automotive

Infineon, Maxim (ADI), NXP, On Semi, Rohm, Cree, and ST Micro are companies with large percentage revenue exposures to Automotive. Most of their revenue growth has been tepid for a while and they have always listed Automotive as this huge potential market. The huge slate of EV cars from large OEMs, or more level 2+ features might make this finally their year.

Here’s a simple overview from the tracker. STMicro looks stand out, and the momentum, revenue CAGR, and incremental margins look great. That being said it’s one of the expensive in the group.

Memory

The company that always stands out because it’s always cheap is Samsung here. NAND markets despite the YMTC entrant have started to stabilize. DRAM is positioned for a very good year. I talk about Memory above but this has the potential to be a great year for them if broad-based semiconductor demand happens. Additionally, for Samsung, their foundry prospects, in particular, seem to be working quite well.

You obviously are owning a lot more than the memory part of this business, but it doesn’t hurt that the company is net cash and trades at ~6x EBITDA, and has grown historically. Obviously, there are some foreign company aspects that might make this harder to own than say Micron, but food for thought especially if you’re an EM-focused manager.

Semicap

This one is interesting because hey I actually know 10s of names in this bucket. The one to me that still really sticks out is Lam Research. They continue to benefit from Memory (discussed above) and even potentially 3D packaging as thru silicon vias become a larger and more important part of advanced packaging.

ASML looks just punitively expensive, but still, I understand the appeal. Something I want to harp on is the foreign versus the domestic aspect of this tracker. You should always prefer non-US semicap companies because they get to sell equipment from a neutral place and thus easily into China.

Mobile

The company here that looks interesting to me is Qorvo. I am kind of stale on the name but they have a strong market share in filters, have historically grown above peers, and RF likely has higher content into the 5G cycle. Their recent spree of acquisitions look very smart in hindsight, but I am not exactly an expert in the RF chain. This is a company I would like to research later. I hope to write a primer on that eventually.

5G / Telecom Infrastructure

Lastly, we have 5G / Telecom infrastructure. I find Marvell to be interesting as a strategy, but obviously, it’s one of the most expensive it’s ever been and it still has a secularly declining business in memory controllers. Maxlinear screens very cheap, and it’s very nice that they will likely benefit from Infrastructure and consumer broadly, while not being remotely as expensive as the other publically traded companies.

How I’m setting up for 2021

I am going to go ahead and say it. I think it’s time for a “hard memory” cycle. NAND is going to be more tepid with lagging prices, but DRAM looks like it’s off to the races, and the Micron power outage helps. Pricing has turned positive broadly in November YoY, and it seems like demand is roaring ahead. Meanwhile, Automotive and other sectors broadly will help a broad-based strong semiconductor cycle, and Memory tends to benefit when the entire ecosystem does well.

The typical ways to play are Micron and Lam Research. Especially if Memory players turn on the capital spigots, Lam Research could accelerate revenue meaningfully. Meanwhile, Micron has already begun to move up numbers, this is likely the beginning of a multi-quarter up-cycle. Samsung is another “cheaper” and differentiated way to play, as their Foundry success is likely to become front and center in 2021. I think all three are set up well for 2021 and are the places that are the most interesting to me.

I also want to hark back to something I wrote a while ago, and I think that is really applicable in this case - or the S-Curves piece. This is my favorite way to frame the memory cycle without an obsessive focus on the DRAM spot prices (I also don’t have a subscription to pricing - maybe when the substack is a bit bigger!).

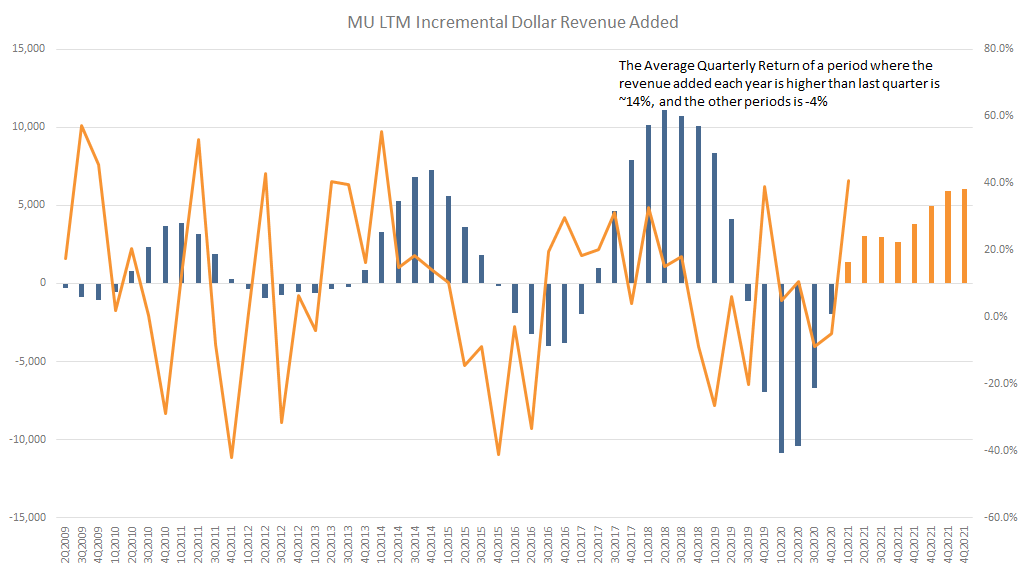

This is Micron’s dollar revenue growth and future estimates and you can clearly see the cycle at work.

Orange is future numbers and I can tell you that easily numbers are meaningfully way too low, and we are just beginning the “growth” phase of the cycle. You visually can see where they would have to grow to match the previous cycle’s high, and there is reason to believe that this cycle will be stronger than the last (AI demand for DRAM). That would mean meaningful percentage beats for revenue for multiple quarters in the future.

This second (and messy chart) is the stock return (right-hand axis) based on the dollar revenue change YoY (left-hand axis). A reminder that this is calculated as LTM this quarter - LTM last year, thus the new dollar revenue change year to year.

In the past, you want to buy when the trough starts to flatten out, or in this cycle’s case, in ~1Q2020. As the cycle continues it usually is accompanied by higher new dollar highs, and you want to be long the company as long as the new dollars added to the business is higher than last year’s dollars.

The time to get out or a signal that the memory cycle is over is when revenue is decelerated by adding less new dollars this year over last - in the last cycle’s case that was ~2Q18. Right now we are just at the beginning of this cycle, and we are likely running ahead of what is the “correct” price in the short term, but if they bang out 5 quarters of meaningfully higher than consensus revenue, estimates will chase and Micron will be cheap again. Micron moving up earnings recently is also a sign.

This bodes very well for memory broadly and tells me that it’s time to get long. The memory cycle is extremely cyclical, and the violent upsides are just as drastic as the downsides that keep many investors out. It is looking like everything is coming together for memory this year, and thus why I believe Micron, Samsung, and Lam (and semicap broadly) are extremely well-positioned. It’s looking like a good year for semiconductors in 2021.

Until next time! And here’s to a better 2021. Cheers!

Thanks Mule for a excellent article! I have worked in storage industry for 10+ years designing NAND and various SSD based products. It was delightful to read a industry level article here.

My 2 cents, on comments below. I would not worry about Optane too much ( have spend many years on it). To me it is a great science project, but when it comes to TCO or Dollar cost it is just going to be a solution for any hyperscalers.

One area to watch is CXL, this interface will enable companies like Micron to designer a cheaper DRAM and put it on a PCIe interface (sorry if this sounds too nerdy). And this will be a nail on coffin to some projects like Optane in long run. Plus, I have no hopes on Intel doing anything right given their sell of memory business to SK and merging Optane to their DataCenter. For a second, one can imagine if I am the VP of the datacenter group, where would I put Optane in the things of problem I need to fix.....geez I guess would be pretty last for me given all the other woes :).

Noob questions,

1. In the excel snapshots of companies, what does Weight % mean?

2. Any key non-USA tech companies you like other than Lam Research there? Specially looking to the ones who will be supplying to China?

What do you think of HSMC failing and Tsinghua defaulting (YMTC parent)? Also another memory question; we've started seeing stuff like Optane actually go into racks. It populates channels where DIMMs would be but serves a function between memory ranks - do you think it materially cannibalizes DRAM this cycle?