SiC as a Dog: Tesla Investor Day

A quick note about Silicon Carbide, and who wins and loses.

This will be a concise update on the SiC blowup after the Tesla Investor Day this morning. I will assume you know about Silicon Carbide; if you don’t, please refer to a somewhat dated piece I wrote about Silicon Carbide here.

Another nice-to-read piece is the Wolfspeed Analyst day, which gives context for how much Silicon Carbide capacity is being ramped. On to the update.

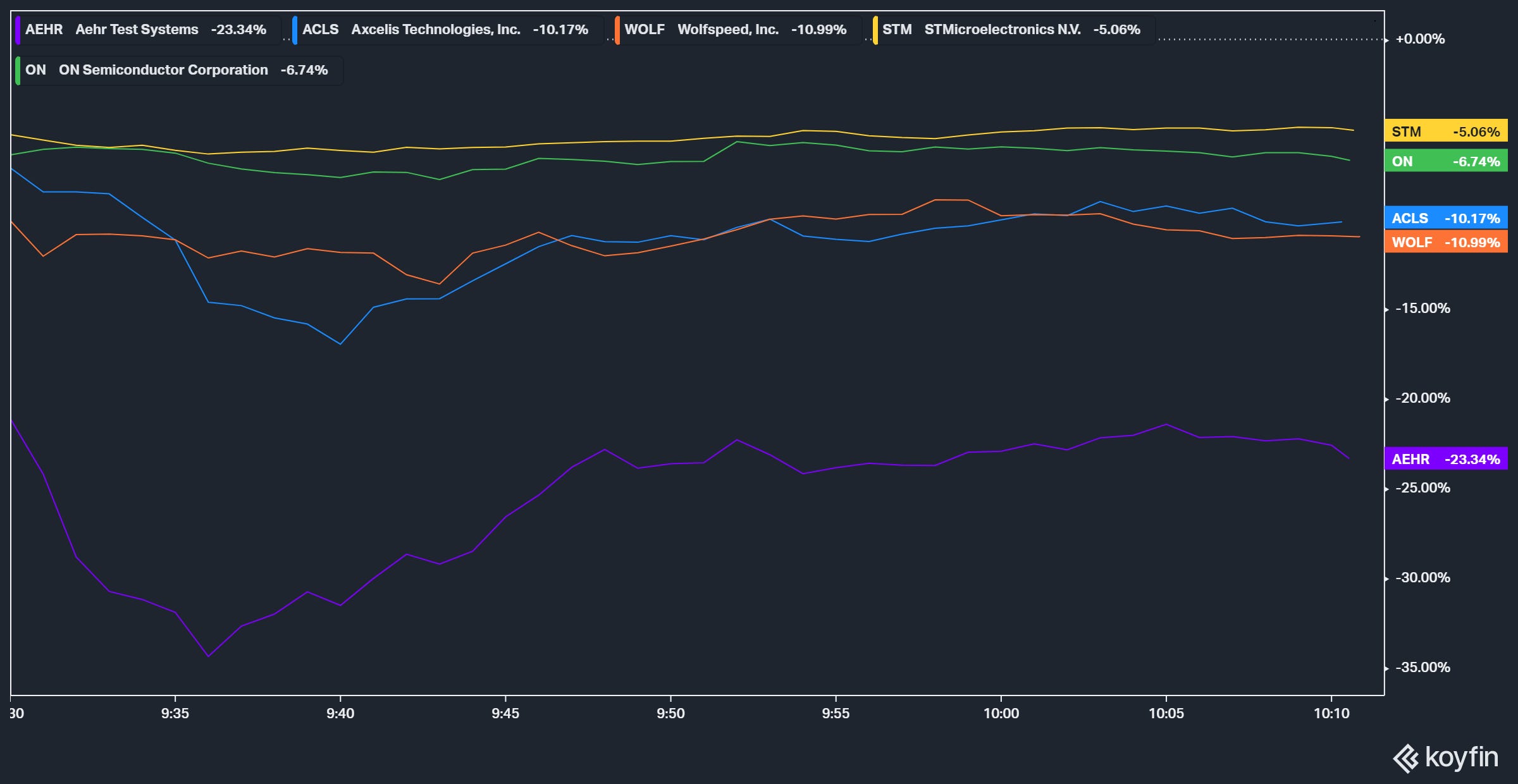

If you didn’t see the big news, Tesla believes their new drive unit will have ~75% less Silicon Carbide than their current drive train.

That is a massive wrench in the Silicon Carbide content story, and shares of almost every Silicon Carbide exposed company are down meaningfully. That’s happening as we speak.

I think the risk here is the longer-term timeframe for SiC. If Tesla really can reduce the content by 75%, then that’s quite a bit less SiC, and the massive builds being done at WOLF will be a systematic oversupply for Silicon Carbide.

But before we jump off the cliff and short all the companies into the hole, I want to step back off the cliff and talk about some puts and takes. I think today’s share decrease is a clear opportunity for some companies at cheaper prices but an apparent detriment to others. I want to talk about which is which, but of course, that will be behind the paywall.