[Special Situation Idea] Long-Term Tailwinds with a Near-Term Catalyst

The Winds of M&A are Blowing

I swear I don’t try to find buyout ideas, but here’s another post filled with b̶a̶s̶e̶l̶e̶s̶s̶ educated speculation about a company positioned well in the long-term that I think is getting ready for some near-term filthy M&A action. This one had a lot of screaming signs pop up to me that are all public signals.

I’ll lay it all out for you, but draw your own conclusions. I wouldn’t expect a quick turnaround like my last idea post.

Disclosure: By reading this or viewing the material you agree that this research is at your own risk. In no event should Mule’s Musing or any affiliated party be liable for direct or indirect trading losses caused by information from this research. You should do your own research and due diligence, consult your own legal, financial, and tax advisors before making any decision with respect to transacting in any securities mentioned herein.

The Run-Down

I believe that it is very likely that Camtek (CAMT) will be acquired by or do some kind of transaction with Nova Measuring Instruments (NVMI) in the near term. There are other possibilities but this is the most likely.

The Facts

Nova and Camtek are the two largest and leading Israeli semicap companies

Nova just raised debt on 11/12/20 and signaled they were looking to acquire

Camtek just had an equity offering on 11/23/20 that it didn’t really need (net cash) and said they aren’t pursuing an acquisition

Camtek has a 25% owner (Priortech) that has joint control with a Chroma, a Taiwanese company, which bought into the firm at a 29% premium to market price in 2019

Camtek CEO (who has Board control) is incentivized to look for a 40% premium to market price in a change of control scenario, per the proxy

If these were US companies, Nova could not fully acquire Camtek outright in cash, with ~$430 million cash on hand against CAMT’s ~$650m EV

However, Israeli business law allows for 25% voting shareholders to take control in certain scenarios, but in that event, minority shareholder ought to beware: no tender offer is required

Regardless, it’s still a good business with clear synergies upon acquisition

According to any conventional GICS screen, the three biggest semicap firms in Israel are SolarEdge (SEDG), Nova, and Camtek, in that order. However, SEDG operates in a wholly different end market (I don’t really consider it semicap), while Nova and Camtek are in the same vertical.

In fact, Camtek is just slightly downstream of Nova in the metrology value chain, so a union makes a lot of sense.

Both firms recently raised capital at the same time, and they have both discussed M&A in the past. I think Camtek was mostly interested in buying but doesn’t mind being bought.

Additionally, the air is thick with the stench of corporate dark arts. It is very clear that management is signaling they want a deal—there are some proxy clues that lead us to this conclusion. A reminder this is *speculative*, but I like Camtek long-term, so it’s a short-term catalyst on top of a really well-positioned company anyway. I want to also say it’s a ~800 million market cap company and is rather illiquid, this is not an investment for many funds.

Let’s go a little deeper.

Company Overviews and Deal Rationale

Camtek (CAMT)

I came across Camtek by searching transcripts for the keywords “advanced packaging”, “2.5D” and “3D”. After I filtered that down, Camtek stood out as the most promising. I’m in the midst of a packaging primer so we will revisit other candidates, but (spoilers!) Camtek is a top choice for the long-term.

Camtek’s core business is the sales of their Eagle product family, which is focused on 2D/3D inspection of semiconductor packaging. Packaging has and will continue to become more important due to increasing semiconductor engineering complexity. Camtek, as the purest-play packaging inspection company, should continue to benefit from the tailwind.

From their recent presentation here:

Also, as an aside, in my meetings with the Camtek management team, I’ve noticed that the storytelling can be a bit… lacking. If management could translate the story better for English-speaking investors (any of you work for a PR firm?) or if the firm were easier to invest in for bigger firms liquidity-wise, it would likely have a higher multiple. More on that later.

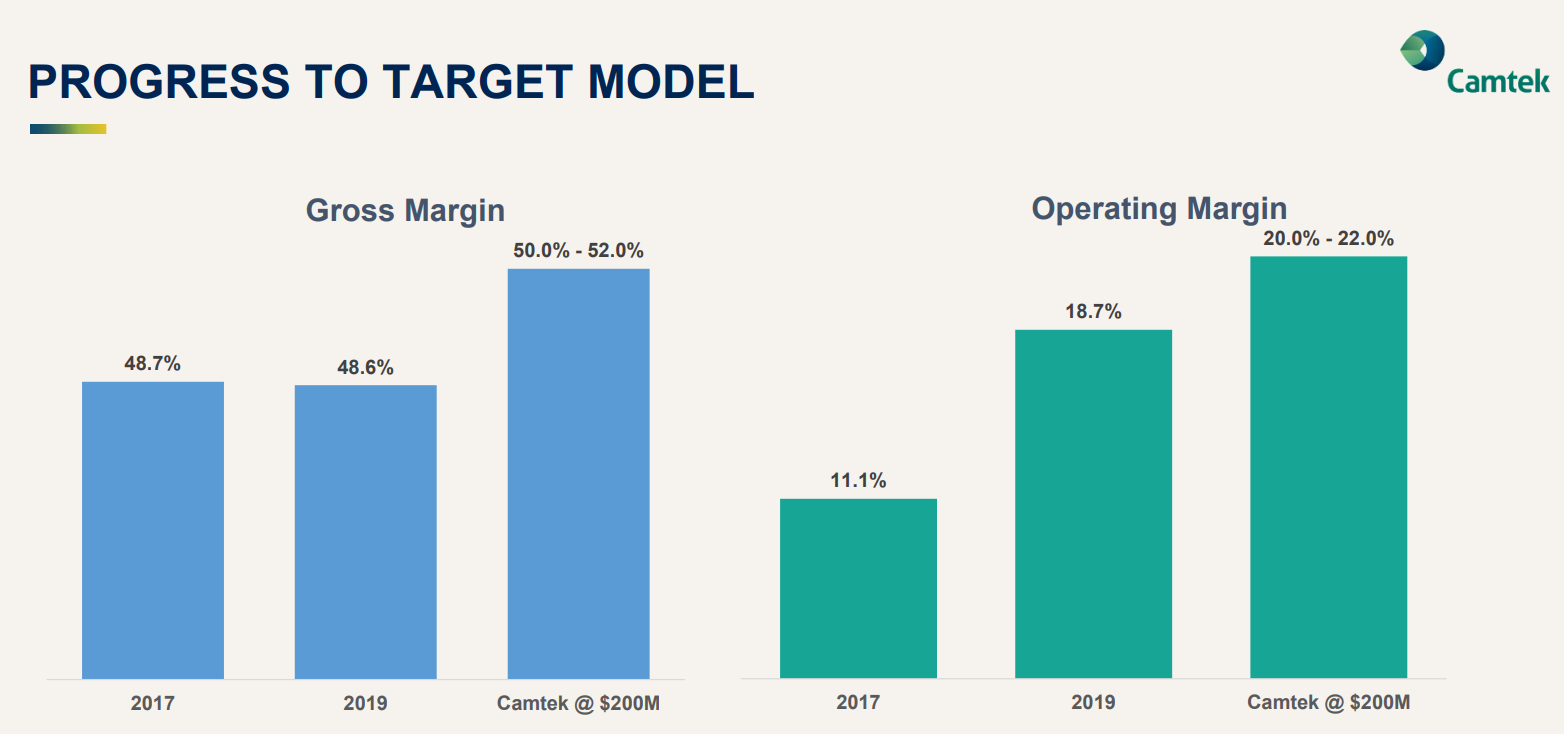

Fundamentally, Camtek’s position is quite strong and only getting better. The firm is hitting its stride on the virtuous cycle of greater revenue, improving operating margins, and better cash generation overall.

The below chart uses cumulative growth values, but note what happened in 2019: they managed to grow into a broad industry down cycle. Now that’s secular growth.

Fun fact: if you read my semicap introduction primer, you may have seen me use the term “Mid-End”—I actually got this from one of my conversations with Moshe Eisenberg, Camtek’s CFO.

What Mid-End refers to is the step after the fabrication (Front-End) but before the dicing (Back-End). Camtek’s an emerging contender in wafer-level packaging (that’s hot right now), which makes the company dream-like in terms of competitive positioning going forward. They are right in the sweet spot of emerging packaging technology.

No one knows how the Mid-End segment is going to shake out, so management is starting to move towards the front end. Per management in 20Q3:

“I will take the question. Well, I think we've said it a number of times. We are baking 2 more segments on the front-end. And definitely, this is part of the forecast that we are seeing into the fourth quarter and the first quarter of next year. And we are getting traction from quite a few customers. And definitely, this is becoming the segment that is meaningful to the customer -- to the company.”

Well, I think we're still in the first stage. We are in a number of customers in different areas of the front-end. As we said, it's the back end of the line, but definitely, we are gaining more and more traction. When our customers get to see our machines, they like it, they own [ the more ]. Other companies here with us, it's the market presence. It's the overall market and technical capabilities that we are gaining as we enter more and more customers.

It seems likely that their biggest problem reaching the front is not a product issue, but a lack of existing footprint. Pitching to a fab as a back end manufacturer is like breaking a style box in investing—very hard. The sales forces have different customers and it’s difficult to get people to switch.

Nova Measuring Instruments (NVMI)

Nova sells traditional metrology (the study of measurement) tools for semiconductor fabrication equipment. You need these tools to double-check your work after a semiconductor is fabricated. If you do a step in lithography and want to make sure it’s up to quality standards, metrology gets you there.

Each type of metrology applies to a different step in the semis manufacturing chain. Below, you can see Nova’s portfolio of metrology solutions. They often compete against the likes of KLA Corp (KLAC) and presumably would have been acquired if weren’t for antitrust issues. Nova is a typical Front End metrology player that is I would generally classify as a tier below KLAC but clearly a strong player.

Nova did a recent convertible debt capital raise (11/12/20), and this is their commentary on it during their recent Q3 earnings call:

Based on our long term trajectory, which combines both organic and inorganic growth drivers, we have decided also to raise capital to support our next level of expansion. In October, we completed a successful private convertible note offering of USD 200 million. We initially announced an offering of $150 million but upsized it due to a strong demand. The offer was closed at attractive conditions of 0% interest on a conversion premium of approximately 27.5%. The fact that over 100 institutions applied to participate in the offering was a very positive indicator to us with interest extending beyond U.S. borders, including Europe and Israel.

Beyond the fact that this recent move created a favorable position for us to leverage our company assets for inorganic expansion, it is a broad vote of confidence in Nova's business trajectory. Following the transaction, we will continue to seek investments in disruptive new technologies, pursue attractive merger and acquisition opportunities and enhance shareholder value.

The Initial Fit

So,

Nova is a Front-End player that is prowling around for acquisitions after issuing debt

Camtek is a Mid-End player that wants to get into the Front-End but is suffering from a lack of footprint

These puzzle pieces fit perfectly. Cost synergies would be easy to obtain—I mean, check out their San Jose offices. Revenue synergies are likely pretty impressive as they could sell into the much larger Nova installed base with their well-positioned product.

Frankly, many companies could acquire and would want to acquire Camtek right now (KLAC, maybe?). And even if they don’t, I think the company by itself is an attractive enough investment to justify the investment. (More on that in the appendix.)

But wait, there’s more!

The Curious Case of Camtek’s Cash Raise and Related Parties

This is where it gets weird and somewhat sketchy for US-based investors. Camtek also did a raise (11/23/20), but with equity. Why equity? I think their stock is cheap but historically, I wouldn’t call management’s capital allocation a strength. I originally chalked it up to shares at all-time highs. Anyway, here’s the language:

Camtek intends to use the net proceeds from the offering for general corporate purposes, including, but not limited to, potential acquisitions, working capital, capital expenditures, investments, research and development and product development. Camtek has not determined the amount of net proceeds to be used specifically for the foregoing purposes and has no agreements or understandings with respect to any acquisition or investment at this time.

The wording is strange. They note no agreements or understandings to an acquisition or investment, but the language notably excludes the scenario where they’re fielding offers.

What can they do with the cash? The company has historically issued special dividends when the cash balance is too large, but management recognizes that it doesn’t really make sense to do an equity raise and immediately pay out shareholders.

In any case, cash on the balance sheet as of 3Q20 is now ~106m + 68.4m raise for a total of $174.4 million. There aren’t really any firms that fit into their expressed strategic goals in that price range.

From Camtek’s Q3 Earnings Call:

I think, definitely, the first priority before we consider dividend is to look for opportunities and M&A. But we don't want to go to any adventure. Sometime you make M&A and then all the management invest all the effort and attention, and it can affect in our potential to grow and to take advantage of the organic growth. So we have to do it very carefully. We are looking for mature companies, companies who don't tend to do micro management, companies that show stable profit. This is okay for us. And also, of course, we would like to look for a company in the semiconductor arena. We don't want to start this company that we have no clue about market, what they do. I think that we have no -- we cannot contribute this. It was a very strong organization. And definitely, we can take small, midsized companies and we give them a lot of tool to leverage their success. So right now, we are evaluating a few companies. But as I said, we do it very carefully, and we don't intend to make any venture by looking for startup a company that targeted the stage of investing and losing money. This is not the type of M&A that we are considering.

Governance Oddities and Corporate Dark Arts

Priortech (TLV:PRTC)

Priortech is a public Israeli conglomerate that currently owns ~24% of Camteck and reports the firm as one of its three operating companies. (Under Israeli securities law, 25% ownership of voting rights is enough to grant control if there isn’t someone else who owns >50%.)

Camtek’s CEO is ex-Priortech. It’s safe to assume that their interests are aligned.

Prior to that, since 199 Mr. Amit has served as the President and director of Priortech and has been the Chairman of the Board of Directors of Priortech since 1988. From 1981 until 2004, Mr. Amit served as Priortech’s Chief Executive Officer.

Chroma (TAIEX:2360)

Chroma is a Taiwanese firm that purchased 20% of Camtek from Priortech in 2019. The agreement mainly concerned a technology JV to use Camtek technology for complimentary non-competing projects for a fee. Additional conditional royalties to Camtek would be paid at certain checkpoints. Chroma clearly thinks Camtek is a good asset.

With regards to governance, Chroma and Priortech agreed to vote together, and are considered to be in control.

Chroma closed this private placement for a 29% premium to share price in June 2019 (more on this later!). The immediate rationale is beyond me as they are clearly a backend test company focused on parts of semis. So add another one for weird corporate actions that don’t necessarily make sense to US investors.

What Could Happen

So,

Camtek is a net cash-heavy company with a weird related party structure and fiending for an acquisition.

Nova had ~$238M in cash and just raised ~$190M net, to a pro forma ~$428M cash balance.

This is not enough to take out Camtek but is likely enough if they issue shares.

Let’s speculate.

Camtek has several choices, and all seem like decent options to a shareholder.

Camtek continues to execute well. It’s a good long-term investment in my opinion and (the thesis is in the appendix).

Camtek gets acquired by Nova Measuring, which creates an Israeli national champion focused on metrology. This would meet several strategic criteria for both firms, but the details of any such transaction are unclear.

Camtek acquires a company - It makes sense if they could find a reasonably sized firm to acquire, but I just don’t see it. I have scoured the world far and wide for a semi-legitimate and well-positioned ~100-400m market cap semicap company and cannot find one that fits the bill. There are few Japanese companies that I don’t follow on the small side. However, the CEO’s PRSUs will no longer be performance-based vesting and just time-based—so the incentives here are big for management.

Camtek gets consolidated back into Priortech. This is the least likely option. Rafi Amit, Yossi Shacham-Diamand, and Yotam Stern are all affiliated parties here. It’s possible, but doesn’t seem like what they’re gunning for.

From this perspective, Camtek is most likely fishing for an offer. I think Camtek acquiring a company or being reconsolidated are the worst cases, but they aren’t especially likely to happen. Because there is a lot more than meets the eye.

The Nail in The Coffin

This is where the Non-GAAP brain comes alive (thank you so much @NonGaap for taking a look, this guy is a friend and a mentor, sub to his substack please!)

On May 27th, 2020 a proxy filing added a ‘change in control’ clause, specifically with a new and very randomly specific deal premium clause added. “40%”. Not 20-40%, or even 50%. 40%.

Our Compensation Committee and Board of Directors shall be authorized to grant an Executive, in connection with an event of a change in control, a cash payment of up to 6 monthly Base Salaries, provided that in such change in control event which results in the receipt by the Company (or its shareholders) of consideration with a value representing, a premium of at least 40% above the average of the closing prices per share of the Company’s ordinary shares as quoted on the Nasdaq Stock Market over 20 trading days ending one day prior to the execution of the term sheet (or similar instrument) for such change of control event, such cash payment may be increased up to a total of 12 monthly Base Salaries of such Executive.

On July 7th, 2020 Camtek held a special general meeting where they approved the 2019 equity grants, this was partially due to COVID-19 interrupting their ability to hold last year’s meeting. However, there is an interesting tell here. The board goes out of their way to praise the CEO (reminder Amit is on the board and is considered to be in control!) for his “pivotal role”. Furthermore, the “efforts and success in leading and closing such transaction were not adequately rewarded” in the Chroma investment, so he was rewarded with a $100,000 bonus.

This will be important later.

And just a few months later on September 24, 2020, another general meeting is held, where they make sure to get the 2020 grants out of the way before a possible deal. In this proxy, the change of control clause notes that CEO PRSUs will vest on a double trigger acceleration and on a time-basis. Effectively, Amit would get ~$150k more in payments after a deal goes through, regardless if there is a 40% premium or not. Double-dipping!

Here is my timeline of everything so far.

If this was a US company, this would be a pretty strong signal to buy. But we’re not in the US.

Welcome to Israel! Special Tender Offers and Control Blocks, A Rather Reluctant Primer

If you are faint of heart and a shareholder, best look away now. I recently have learned a lot about shareholder structures in Israel, and the image that comes to mind is a vaguely East-Asian-themed dystopia. Cue the Blade Runner soundtrack.

Let’s start with the worst: there are rules around Special Tender Offers and controlling stakes that are completely unique to Israel and will shock minority investors everywhere.

If a controlling company sells its block of shares it can effectively sell the company but at a much smaller price. This is mostly used to continue to control the entities in Israeli multi-layer pyramid-shaped business structures. So if Nova comes to Camtek, offers a premium for the controlling block of votes (25%), it will effectively become the de facto controlling block and can do whatever they want with it, without the need for a tender offer. This is why a 46% proposed acquisition of an Israeli company by a Dutch firm didn’t require a tender offer to all shareholders.

The puzzle pieces fall into place. And boy is it an ugly picture.

Look at this language:

Further, upon an event of change in control of the company (a “Change of Control”), as shall be defined in the Mr. Amit’s Notice of Grant

That notice of grant is not public. And I believe it only refers to a change of control on the controlling block. So what could happen is Rafi Amit could still get the bonus payment for a 40% premium but only on the controlling block. Let’s now look at how far the ~$430 Nova raised will go.

Oh shit, it’s almost the controlling block premium in cash. They are a little short but I’m sure they’ll figure something out. So this means that they could effectively get the deal for cheap and “take under” the company. All they need to do is purchase the Priortech / Chroma controlling stake to be granted the keys to the kingdom. They can do the rest of the equity in all stock which is likely instantly accretive to Nova. My understanding is in these cases they usually still offer a premium to shares, but not quite the eye-watering 40% premium listed in the proxy. The shares would move based on announced deal synergies. I’m thinking 10-20%+ in this case.

Also, the second cash raise by Camtek now finally falls into place. If you desperately wanted a deal and wanted to lower the price to make sure you hit the 40% premium how would you pummel your stock? The cash raise is a nice cushion for both companies post-merger. An all-stock deal will leave them cash poor but Camtek’s ~170 million looks just enough for the combined company.

Remember Chroma? This is a similar set-up for the Chroma situation where they sold their controlling block at a 29% premium to the market, at ~$9.50. Shares reacted well but not quite to that premium Chroma paid that day. This was the very near term result - a ~20% pop in the stock.

Then, in the following proxy, the board (controlled by Rafi) decided to heap praises unending onto Rafi, alongside the $100k bonus. In that same document, the board gives Rafi a reward in case he’s able to secure a 40% premium for a change of control premium.

Remaining Questions

Is Priortech actually still a controlling party? They own under 25%, but they have a voting agreement with Chroma. Is this still considered a controlled company? It says Priortech AND Chroma are the controlling party and do the rules apply when it is two members in the block? There are some basic duties to all shareholders that still apply. Also, Chroma clearly wants to be a part of the Camtek story. They could easily have an interest in acquiring it. Their two board seats are important now and they could swing the deal the other way.

Something that is also interesting is that these kinds of deals happen all the time in Israel, but not on two dual-listed Israeli companies. Both Nova and Camtek have Nasdaq exchanges, and the optics frankly look terrible if they decide to do this take under. It doesn’t seem like a smart move.

Frankly, this is also really outside of my wheelhouse and something I am cognizant of is that there are a lot of unknowns. Can another company come in over the top? Please send this to KLAC management if you know anyone there.

They could just do a vanilla premium with a cash and stock deal, and that would be really great. I didn’t want to have to write about the bear case, just a strategic asset that I know will appreciate. This is still possible with the Nasdaq listed aspect in play.

Conclusion and Thoughts

Clearly, Camtek is working on a deal. It could be a take under or a typical premium based deal, or even an acquisition of another company. We really have no way of knowing without being in the board room. But I still believe Camtek is very compelling given these circumstances. Camtek should still appreciate somewhat on an all-stock offer or the worst case which may not even happen. My guess is that a merger can take out a meaningful part of the SG&A completely out of Camtek. For the sake of illustration, I’m going to assume 50% of Camtek’s SG&A is going to zero and they keep all the R&D. That is 22% accretion in the combined companies EBIT. Revenue synergies are meaningful as well.

My very quick proforma has them doing impressive numbers over a longer period of time, especially assuming that the SG&A growth collapses. I think this is very conservative, and considering a post-deal EV of ~2.4 billion, it trades in-line with Nova’s current EBITDA multiple.

Regardless, I think the company will move on a deal, and your worse case is you own one of the most strategic assets in semicap as a downside. The company trades at ~30x forward earnings but frankly, the earnings estimates from the few analysts that cover it always seem to be massively conservative and I expect an acceleration. The risk-reward here seems favorable.

It’s compelling. Just like Inphi (IPHI), it might even be better as a long term investment than a quick sugar rush buy. But, just like Inphi, there might be a short term catalyst waiting in the wings.

Do your diligence—and be sure to check the liquidity.

Thanks for reading! I really enjoyed this research and hope you did too.

APPENDIX: The Brief Standalone Camtek Investment Thesis

I’ll paraphrase some other things from the last time I chatted with them but between them. Here is my high-level thesis on Camtek

Onto and Camtek are the only two players in this Duopoly, and Camtek is more focused and has taken share

Camtek can easily grow 10-20%+ revenue as they continue to step into the front end of semicap.

Camtek is increasing gross margin, increasing EBIT margin, and hitting scale as they experience the virtuous cycle of scale in semicap.

Assume they hit 22% margin on 200m in revenue in 2022, or a 15% rev CAGR - that is 16x EV/EBIT for 2022 numbers for a very strategic asset

The company is extremely undercovered. Expensive by traditional forward metrics from sleepy sell-side analysts, but they managed to grow revenue in a down cycle year during 2019, and their end markets are accelerating.

The company is net cash - so that partially allays extreme downside issues. They are additionally cash flow positive.

The company is highly strategic and would be considered a jewel asset in the likes of KLAC, AMAT, or really any front end supplier.