The Digital Transformation of Cars is Just Beginning

The shortages are the first chapter in the Automotive Semiconductor story

I was mistakenly under the impression that the semiconductor shortage would be one of the least likely candidates for a hot news story in 2021. Then again, before I started this substack, I thought my appreciation for semiconductors was pretty weird and niche…

Anyway, here we are.

Right now the headlines are exhausting. Capacity shortages are definitely a near-term factor, but I want everyone to remember to keep their sights on the forest on the horizon.

So let’s talk all about automotive semiconductors:

Why We’re in a Supply Crunch

Automotive Demand Drivers

Future Outlook

Underlying Changes in Our Vehicles

Why We’re in a Supply Crunch

This is pretty well covered. To sum: there is a global chip shortage, particularly for automotive companies.

During the pandemic last year, there was a sudden demand for servers and work from home related semiconductors in March. Think work PCs (surprising!) and servers. Then, when this slowed down, the broader live-from-home growth vertical took its place in the form of gaming PCs and GPUs.

At the same time, the automotive supply chain fell off a cliff from March to May. Large fabs such as TSMC reallocated their capacity to the customers with generally more resilient businesses, i.e. those still capable of fulfilling large orders. But something unexpected happened in the 4th quarter: automotive sprang back to life. This chart from SIA tells the entire story well.

Suppliers were caught off-guard. Texas Instruments commentary really matches the above chart with this quote from their recent earnings call. A just-in-time supply chain that went from 60 to 0 to 60 again.

And I think the best way to maybe describe what we're seeing in the automotive market is just a - just-in-time supply chain that's restarting from essentially a full stop that happened in second quarter. And just as a reminder, what we saw in third quarter was a 75% sequential increase, followed by this last quarter with a 20% sequential increase.

Companies during COVID turtled up to weather the shocks. The focus was on cash preservation, drawing down inventory, and staying alive. Eventually, when everyone stopped panicking, they realized that there wasn’t enough capacity for a return to pre-COVID demand on top of COVID-driven demand.

Everyone’s scraping by with stretched supply chains, which has actually resulted in less cargo capacity for international flights.1 NXP Semiconductor’s recent earnings gave great insight into the situation and why there is likely no end to this in the short run. There’s almost no spare inventory.

Now 1 last element on this, which everybody tries to understand currently, is about inventory levels. I think at the moment from anything we can see, the supply chains through the auto world are empty. And I say that because I know that every single product we are shipping is immediately built into a car. And so there is just nothing going on the sideline. It all goes through into production immediately. That's why we also clearly said we are supply constrained for the first quarter.

And as a reaction to this, I hear quite a few people in the industry speaking about the desire to actually ask for more inventory along the chain in automotive going forward. There is 1 large U.S. OEM, which actually made even a public statement about how much chip inventory they would like to see at their first-tier customers.

This isn’t an automotive-only problem: the situation expands to almost every company fighting for capacity. Similar capacity problems are being seen for GPUs2, notebooks3, and MLCCs4, among others. It’s what’s driving the eye-popping 45% YoY growth at TSMC, and likely a 20%+ year in wafer fab equipment (WFE) spending.

However, while automotive isn’t the only vertical with capacity constraints, it has one of the louder megaphones with which to complain. We haven’t seen this kind of broad-based shortage in some time. We’re seeing high demand for items ranging from simple wire-bonding and discrete products all the way to leading-edge wafers. I think this great chart by Bernstein puts it into perspective. The leading and lagging edges are now at some of the utilization rates we have ever seen.

So that’s definitely nice for owners of those businesses. But this will eventually abate. I want to now focus on the long term, and look towards the digital transformation of cars.

Automotive Demand Drivers

Simply put: there is more silicon in cars than there used to be. Most semiconductor companies outperformed the actual vehicle end-market in 2020, almost entirely driven by content increases. For example, NXP had segments in automotive that grew last year, despite the broad-based decline in auto markets last year.

The main reason for this is that our cars are getting smarter! It’s one area that digitalization hasn’t really sunk its grubby hands into—til now. With the exception of Tesla, most of our cars are very dumb. Historically, besides an infotainment system (to keep the kids occupied on road trips, of course) vehicles haven’t had much digital logic built into them.

I believe we are finally seeing the analog-to-digital switch come to vehicles. My expectation is that most of this will unfold in the coming decade.

Our Cars are Digitally Transforming

The above graph by Deloitte is helpful, but I think it will prove to be fairly conservative. Even if electronic systems only consist of 50% of the cost of the next-generation car, I believe that the value of a car will almost overwhelmingly be derived from those components.

There are dozens of potential features that can be built on top of smarter vehicles, including robotaxis, driverless cars, etc. Some of these features might even turn into whole industries.

However, in order for something like robotaxis to work, we actually need cars that communicate with everything around them (referred to as Vehicle to Everything—V2X). To do that, you need more semiconductors.

It’s just one part of the many crucial transformations that are happening to our cars today.

Underlying Changes in Our Vehicles

Let’s characterize the two big things changing cars into ADAS (Advanced Driver-Assistance Systems) and EV (Electric Vehicles).

These two buckets make sense because their respective existence isn’t contingent on the other, but when combined, could do all sorts of crazy things.

I’ll talk about both independently but my base case is that both changes are occurring at the same time.

Advanced Driver-Assistance Systems (ADAS)

Each subsequent level of driving is often a superset of the previous level with additional features. The following is taken from the very helpful Deloitte Future of Autos and Automotive aftersales report.

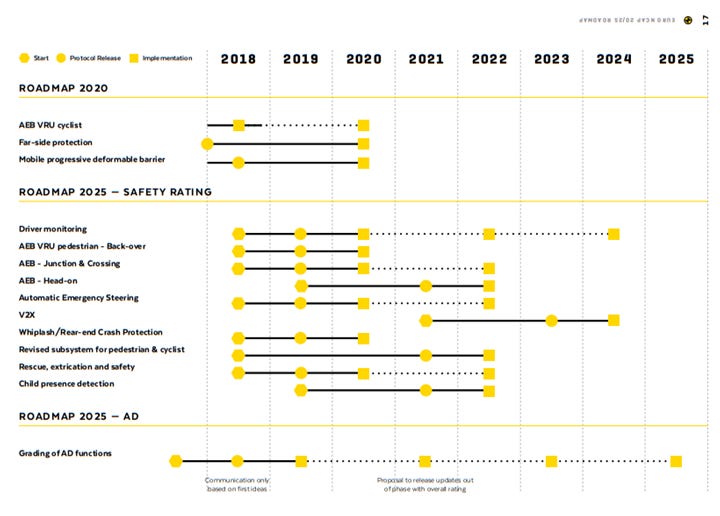

There is no consistent rollout of features. But we have some kind of indication as to what’s coming with the NCAP (New Car Assessment Programme) timeline. NCAP is a regulatory safety project in Europe, and some of the L3 features line up with NCAP dates.

Take a look at the NCAP 2022 targets5 and timeline:

The roadmap indicates 2022 as the start of ADAS feature implementation. The following features:

Driver monitoring

AEB (Automatic Emergency Breaking)

Automatic Emergency Steering

Child presence detection

All of these would require new silicon in the car! Can you see the S-Curve forming?

Now, these features are available in almost all high-end cars today, but those are a small percentage of total cars sold. NCAP adherence is still voluntary, but it will help drive higher ADAS content in the world’s most regulated market. The desire to comply with NCAP by global OEMs will eventually see these features trickle down to the rest of their product lines.

Beyond this, my favorite chart is the following:

As we approach Level 3 features, sensor demand should start to accelerate in cars. A doubling from L2 (today) to L3, and then another doubling to L4.

But it isn’t just the sensors that are accelerating in content. Here is a very delightful roadmap by BMW / Mobileeye6 on how much more silicon content they expect to introduce into cars:

Notice the increase from a relatively “dumb” car at Level 2 to multiple onboard Denverton CPUs, EyeQ5 (Mobileye SoC), and new Aurix (Infineon MCU). Paired together with the previous chart, we can understand that the number of sensors in cars is a direct correlate to semis spend. Not only that, note that Level 3 is the beginning of an S-curve’s inflection.

Transformed into numbers, I estimate that vehicle semiconductor and ADAS spend should grow at a ~20-30% CAGR from 2020 to 2025. I back out of the bottom row cost per vehicle number7.

Electrification of Vehicles

While the ADAS case is very strong, the electrification of cars is the more dominant of the two themes, especially with recent announcements that indicate most traditional OEMs will be producing EVs faster than expected.

Ford recently announced that all of their cars would be EV-capable by 2030 (at the Super Bowl, no less). That would imply they were pushing the adoption curve ahead of previous expectations.

This is important because electric cars rely on power semiconductors more than non-electric cars. Check out the legendary Infineon breakdown of how much more semiconductor content goes into cars:

For hybrids - it’s approximately ~48% more content and for BEV it’s ~110% more power electronics. This looks like another doubling of semiconductor volume on top of what will be a huge growth vector in new EV cars. There’s a ton of potential for automotive power companies here. The benefit of both volume and value increases meaningfully.

Ultimately, this grows the absolute size of the automotive semiconductor market. This is yet another doubling on top of ADAS semiconductor features.

Takeaways

The near-term automotive semiconductor shortage headlines are just a drop in the bucket for the broader volume (and maybe even price) tailwinds. Taken another way: you’ve been hearing so much about automotive shortages because demand has accelerated to go beyond (plus ultra) pre-COVID levels.

The short-term story is an interesting segue into a longer-term and much more durable trend: the digital transformation of our cars. I believe that regulation like NCAP pushes ADAS and Level 3 forward in terms of adoption, and the broad sentiment for greener cars is pushing forward EV adoption by consumers.

Both ADAS and Electrification should double silicon content, independent of each other. And, as our cars become smarter, we should be able to see a tailwind from actual new industries built on top of new vehicle capabilities. The future of robotaxis and driverless cars can only happen after the cars load up on semiconductors.

Framed in growth investor terms, it looks like two very significant automotive-centered S-curves are powering semiconductor demand at the same time. I’ll be watching closely.

Appendix and Other Great Reads

I learned a lot about automotive semiconductors in this very beginner-friendly book - Sensors in Automotive.

A more advanced deep dive is this Understanding Automotive Electronics: An Engineering Perspective.

I also referenced both the Deloitte Future of Automotive Sales and Aftersales and the Deloitte Semiconductors - The Next Wave reports.

The Infineon Investor Presentation is worth a read

This Strategy Analytics Deck is Helpful

Everything Silicon Carbide Related at Cree / Wolfspeed

This is what alerted me to 2021/2022 being transformational years by the way.

https://www.freightos.com/freight-resources/coronavirus-updates/

https://www.theverge.com/2021/2/11/22278562/nvidia-rtx-2060-gtx-1050-ti-gpu-shortage-global-chip

https://www.digitimes.com/news/a20210209PD204.html

https://www.avnet.com/wps/portal/abacus/solutions/technologies/passive/capacitors/the-global-mlcc-shortage/

https://cdn.euroncap.com/media/30700/euroncap-roadmap-2025-v4.pdf

https://www.eetimes.com/unveiled-bmws-scalable-av-architecture/

https://www.eetimes.com/level-5-avs-unlikely-before-2035/

Thanks for the write up. Can you comment on which semiconductor companies manufacture chips for automotives? Thanks

Hey, mule, I enjoyed the article. Have you read “The Machine that Changed the World”? It describes Toyota’s reimagining of workflow in auto manufacturing. The nature of the auto industry’s transition into silicon reminds me of a passage in that book about the effect of national boundaries on the auto industry in Europe after the First World War. In that case, the author suggests that some of Germany’s political instability may have been an outgrowth of major industries, like auto manufacturing, being unable to efficiently source supply from beyond national borders. The scarcity of silicon seems like it creates a similar problem in a world that is now thoroughly globalized. I have to wonder if a certain level of political stability, both domestically and internationally, does not depend on how the auto industry makes this transition.