TSM - It's Good to Be the King: 1 Trillion Incoming

Plus AEHR, APLD, NANYA, Suss earnings

As per tradition, TSMC will be free, and the rest of this week's earnings will be behind a paywall.

TSMC showed what it means to be the king. Its results were fantastic, and its shares have been fantastic for the last 12 months. Short of the entire semiconductor cycle turning, I think that will probably continue. Let’s review the results and take it from there.

Taiwan Semiconductor reports Q4 EPS NT$14.45 vs FactSet NT$14.34

Reports Q4:

Revenue NT$868.46B ($26.88B) vs FactSet NT$856.51B and prior guidance $26.1-26.9B

Operating income NT$425.71B vs FactSet NT$413.45B

Gross margin 59.0% vs FactSet 62.7% and prior guidance 57-59%

At first glance, this is mostly a “meet” and raise result, but a few specific callouts lead to quite a bullish feat. I think the big news was +35% Y/Y capex growth. This is a new high in TSMC capex, even higher than the 2022 peak.

Capex growth was higher than expected, but all of TSMC’s competitors' spending plans are in flux at this point. Samsung lowered capex expectations, and Intel is in the no man’s land. So, while WFE should benefit at first blush, it is a bit more of a nuanced story under the surface. Semicap has become a popular short, and the squeeze in share prices makes sense to me.

Anyway, back to TSMC. The industry’s revenue outlook was a bit more muted than it initially appeared, but with the broader market growing around 10% and TSMC growing in the mid-20s, the company is clearly accelerating its market share gains.

We forecast Foundry 2.0 industry to grow 10% year-over-year in 2025, supported by robust AI-related demand and a mild recovery in other end market segment. Supported by our technology leadership and broad customer base, we are confident we can continue to outperform the industry growth. We expect 2025 to be another strong growth year for TSMC and forecast our full year revenue to increase by close to mid-20s percent in U.S. dollar term.

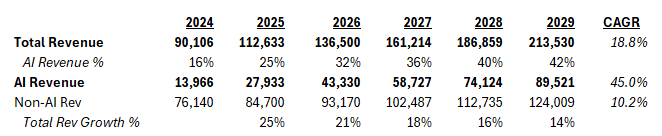

Now, one of the biggest contributors is AI accelerators. Because the rest of the industry is languishing, TSMC expects its AI revenue to double in 2025 and, for the longer term, CAGR to grow in the mid-40s for the five years starting in 2024.

Revenue from AI accelerators, which we now define as AI GPU, AI ASICs and HBM controller for AI training and inference in the data center, accounted for close to mid-teens percent of our total revenue in 2024. Even after more than tripling in 2024, we forecast our revenue from AI accelerator to double in 2025 as the strong surge in AI-related demand continues.

Doing some very simplistic math, if they assume a mid-40s CAGR starting in 2024, they expect ~87 billion in revenue by 2029. Assuming 10% growth for non-AI revenue growth, TSMC said they expect a high teens CAGR by the end of the decade.

Underpinned by our technology leadership and broader customer base, we now forecast the revenue growth from AI accelerators to approach a mid-40% CAGR for the 5-year period starting off the already higher base of 2024. We expect AI accelerators to be the strongest driver of our HPC platform growth and the largest contributor in terms of our overall incremental revenue growth in the next several years.

Now, let’s be honest—no one knows what the super long term holds. But as it currently stands, I think it’s easy to find massive conservatism in these numbers, especially on the AI side. I assume non-AI revenue grows 10%, mainly deriving the 7% long-term number with some share gain. If the AI revenue guide is right, TSMC thinks high teens are possible until the decade's end.

That is incredible. Few businesses can grow at this scale with this duration, so TSMC is king. And now, with its competitors mostly vanquished, it’s about time to reap some monopoly-like profits. With a 50%+ ROE, 20-30%+ EPS growth is likely for an extended period of time. That can all be yours for only 20x 2025 earnings, and that, to me, is probably the cheapest megacap company you can think of. Amazing.

Anyway, back to the results again. Let’s look at revenue growth by platform. QoQ growth was meaningful in HPC, while Smartphone sales growth slightly rebounded. Next year, the growth outlook for smartphones is "mild,” and smartphone seasonality means that next quarter, smartphone sales will decline.

But why does that matter when most of your business is HPC, which will grow faster in the future? HPC grew 58% year over year, and next year, it will probably grow at a similar rate, given AI revenue will double. Presumably, most of this is a higher margin, as a higher percentage of CoWoS is used, and TSMC is once again the leader there.

That was another bullish takeaway from the call. There have been rumors everywhere about cutting CoWoS orders in the supply chain, specifically for Nvidia and AMD. What was the response that sent most AI semiconductor companies up? Orders are not being cut; in fact, capacity is going up.

"Rick, as you said, there's a lot of rumor. That's a rumor. I assure you. We are working very hard to meet the requirement of my customers' demand, so 'cut the order,' that won't happen. We actually continue to increase, so we are -- again I will say that. We are working very hard to increase the capacity."

That calms some of investors' worst fears in the near term. Last but not least, I wanted to mention that base dies are a business. TSMC is starting to make logic base dies for HBM, one of the fastest-growing areas in the space.

We are working with all the memory suppliers, all of them. And that is because of TSMC's logic chip or logical technology more advanced and that meet our customers' requirement. So all of them are working with TSMC. Now we start to see some of the product coming out, but the high volume, probably you will need to wait for another half or 1 year to see the high volume and big contribution to TSMC's revenue.

There was some discussion of Samsung (doubtful) making its own logic die, for example, or memory companies pursuing this in-house. However, no one beats TSMC in logic, and this is yet another future growth vector.

Summing it up - man, is it good to be king! TSMC grew EPS by 40% this year and just guided another strong year of similar growth in EPS. There are many reasons to believe there is conservatism, as the bottom-up foundry estimate doesn’t match top-down estimates from Broadcom or Nvidia.

Margins continue to expand and will reach new cycle highs. Meanwhile, competitors continue to lose shares, and TSMC is experiencing the beauty of increasing margins and revenue and strengthening its competitive advantage. It has an ~800 billion dollar market cap, and I believe it will probably become the next trillion-dollar semiconductor company.

What a company. For more information on other companies and read-throughs, my typical earnings coverage is behind the paywall.