TSMC Earnings, CDW says IT Spending is Weak, and Further Networking Weakness

Earnings season kicks off with TSMC.

It’s become a tradition to post my TSMC earnings round-up for free. I didn’t find many interesting new things in TSMC’s earnings this quarter, but the knock-on effects captivated me. This post ended up as a top-down read on semiconductors and the economy. Read on!

TSMC Reported Earnings

Revenue finally decreased sequentially and YoY for the Taiwanese semiconductor giant. Their margins, however, look much better than I would have expected.

Taiwan Semiconductor reports Q1 EPS NT$7.98 vs FactSet NT$7.39

Reports Q1:

Revenue NT$508.63B ($16.72B) vs. FactSet NT$518.25B and prior guidance $16.7-17.5B

Operating income NT$231.24B vs FactSet NT$220.59B

Gross margin 56.3% vs. prior guidance 53.5-55.5%

Operating margin (OPM) 45.5% vs. prior guidance 41.5-43.5%

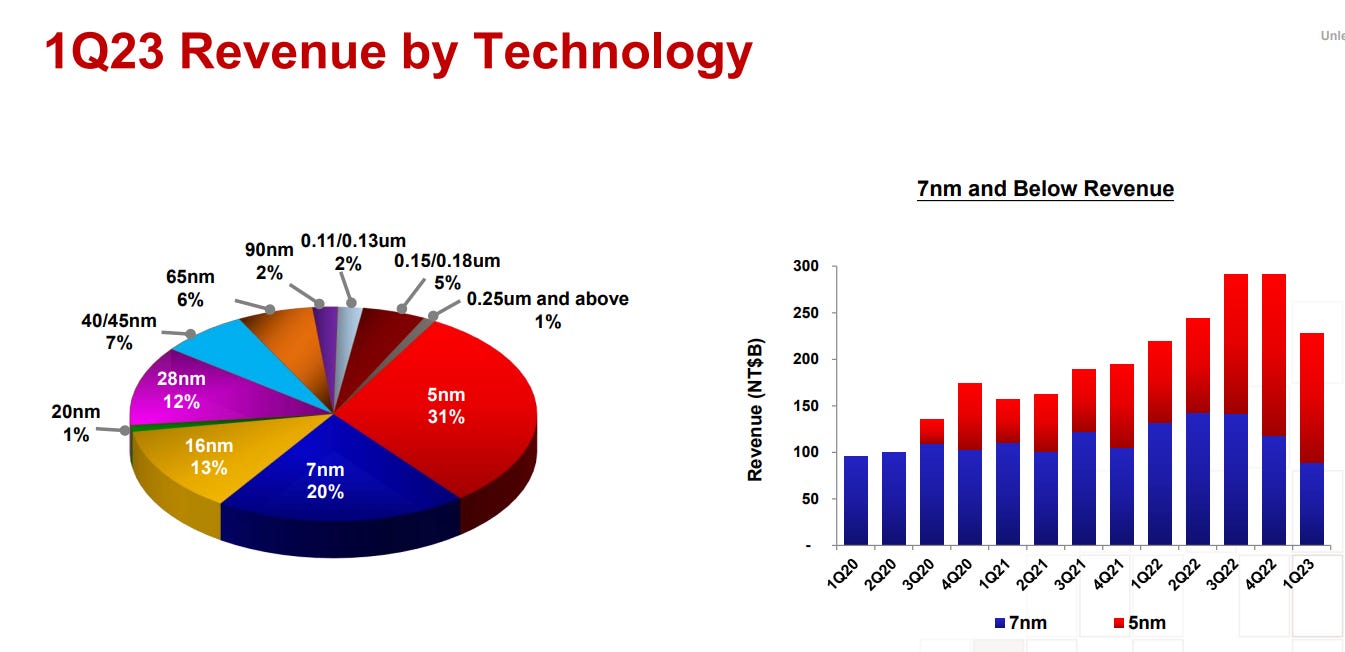

The 5nm ramp continues, but 7nm is starting to look particularly weak as revenue and utilization in the 7nm node are much worse. 7nm could be lower than 70% utilization or worse.

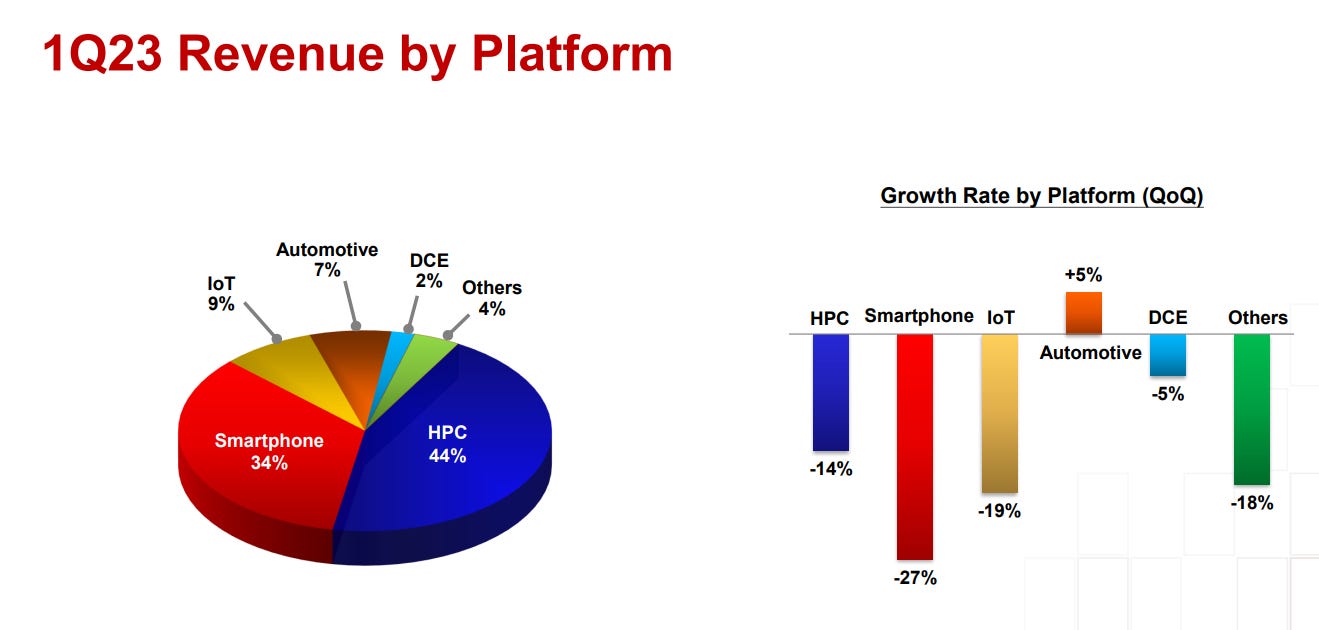

Smartphone revenue is the largest point of weakness this quarter. But HPC and IoT are weak, with Automotive as the only point of sequential growth. More on that later.

TSMC guided their second quarter, another sequential decline of 6.7% at the midpoint and -11% YoY. They expect gross margins to decrease from 56.3% to 53% because of lower utilization costs and higher energy. Energy costs alone will account for 50 basis points for the year, which implies a much better gross margin than expected if there weren’t energy increases. I’ve been impressed by the resilience of margins at TSMC.

Lastly, TSMC decided to reaffirm capex, despite wide rumors they would not maintain this level of investment for 2023 from Taiwanese media outlets (rumor mills). TSMC is instead going to focus on the long term and invest anyways.

They updated their outlook for the year, which is:

For the full year of 2023, we do our forecast for the semiconductor market, excluding memory, to decline mid-single-digit percent while foundry industry is forecast to decline high single-digit percent. We now expect our full year 2023 revenue to decline low to mid-single-digit percent in U.S. dollar terms

They continue to believe in a second-half recovery:

Having said that, we believe we are passing through the bottom of the cycle of TSMC business in the second quarter. While we forecast only a gradual recovery, for the semiconductor ex memory industry in second half 2023, TSMC's business in the second half of this year is expected to be stronger than the first half, supported by customers' new product launches.

Meanwhile, they are pushing out some fabs as Arizona is delayed, Japan is refocused on more advanced nodes, and Nanjing continues on time. But the industry callouts were the most interesting parts of the call.

Utilization in 7nm is horrible; CoWoS, however, was an interesting tidbit, as it indicates that Nvidia GPUs are growing massively. This is another proxy of AI demand.

I mean, that's -- semi says that, actually, just recently in these 2 days, I received a customer's phone call requesting a big increase on the back-end capacity, especially in the CoWoS. We are still evaluating that.

C. C. Wei noted that Automotive is now seeing weakness, while AI is starting to grow again. AI within the data center looks strong, but HPC, in the aggregate, is weak.

We observed the PC and smartphone market continue to be soft at the present time, while automotive demand is holding steady for TSMC and it is showing signs of soften into second half of 2023. I'm talking about automotive. On the other hand, we have recently observed incremental upside in AI-related demand, which [ has ] the ongoing inventory digestion. What is the second question?

I want to branch out on the automotive comment because this is the most interesting statement and the biggest delta from reality. Remember, until now, Automotive has had quarter after quarter of levitating growth, and despite the concerns of over-inventory, they have yet to come to fruition.

Automotive Semiconductor Cycle Turning

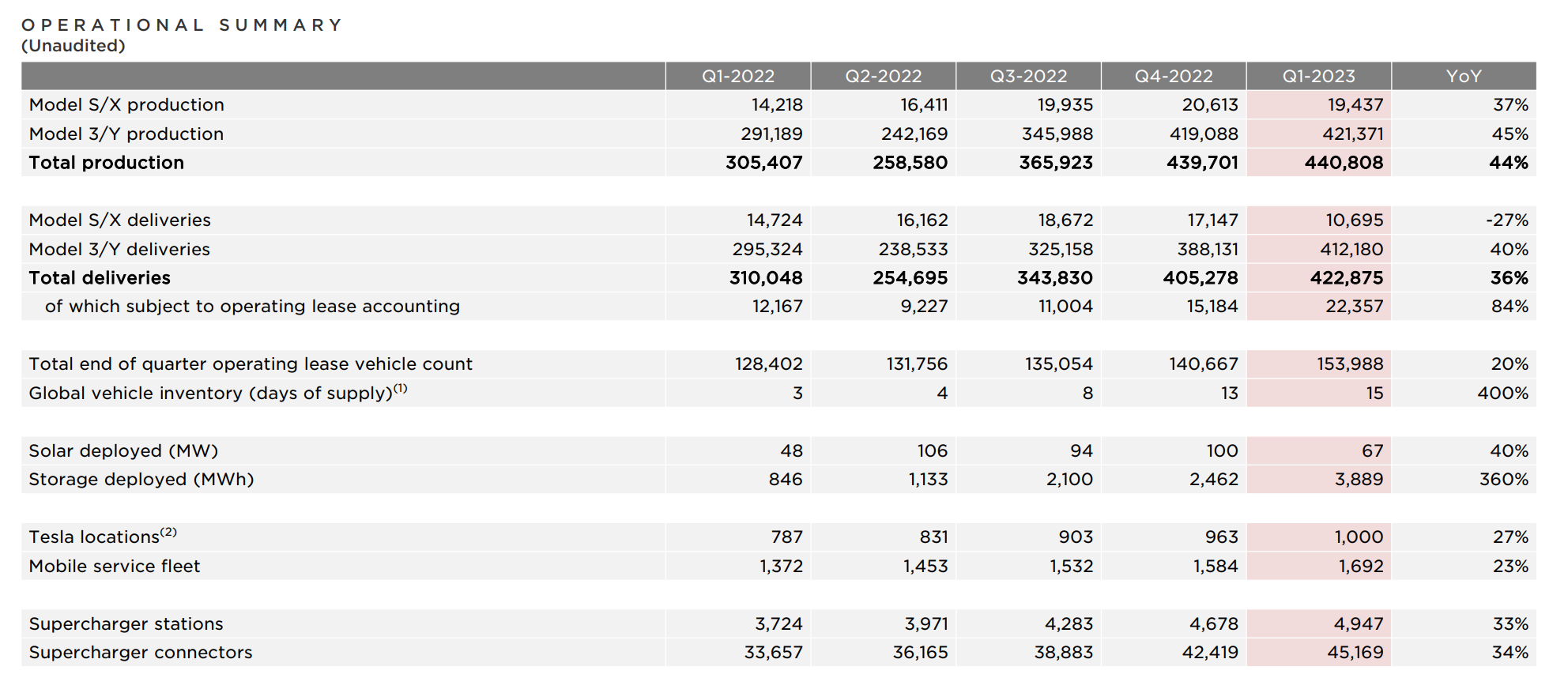

It’s looking like now is finally time for the automotive cycle to turn. Let’s read Tesla’s recent results in conjunction. Tesla has had to start dropping prices, and BYD has started to create extremely cheap electric cars to export. While I think EV adoption has a long way to go, we will finally see the shortage become a bit of a glut in the strongest market in semiconductors; Automotive.

If you took away what you understood about EVs and their adoption, an industry with higher inventories, price cuts, and margin erosion sounds like a classic over-inventory cycle. That’s automotive. Let’s take a look at Tesla in particular. Inventory at Tesla is growing much faster than deliveries.

Meanwhile, gross margin is eroding as Tesla cuts prices to sell more cars in a weak macroeconomic environment.

One of the things that kept automotive makers so strong this cycle is that pricing was so particularly strong, as automotive makers artificially lowered supply and only sold higher-end, more feature-rich cars. This is best shown by the Manheim used car index.

That works in a Goldilocks environment, but now that rates are still rising (more expensive to finance a car), the economy is slowing, yet automotive sales are still increasing, and the price cuts are telling. Auto dealerships will start using promotional behavior, and consumers will trade down.

Falling prices to move through increased inventories sounds like the problem of the over-inventoried sector in every semiconductor market except for automotive now. It’s likely time for the shoe to drop at Automotive, and shares in automotive heavy companies reflected that today.

I wrote a bit about inventory increases in this post in February, and I will use this as a guide as to whose worse impacted.

{kind=link}

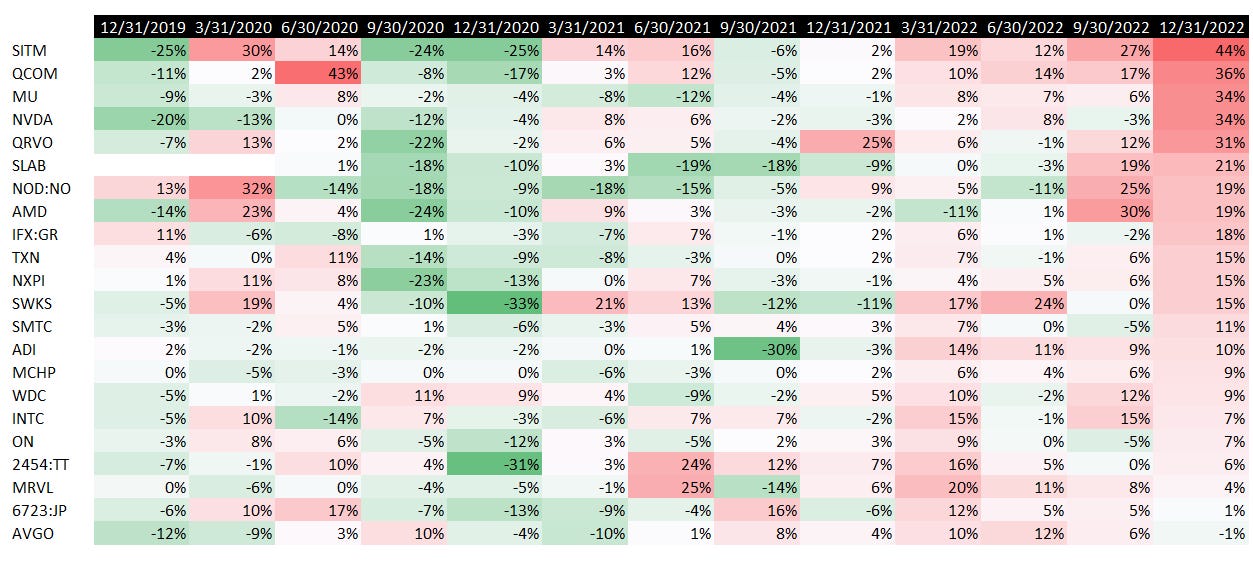

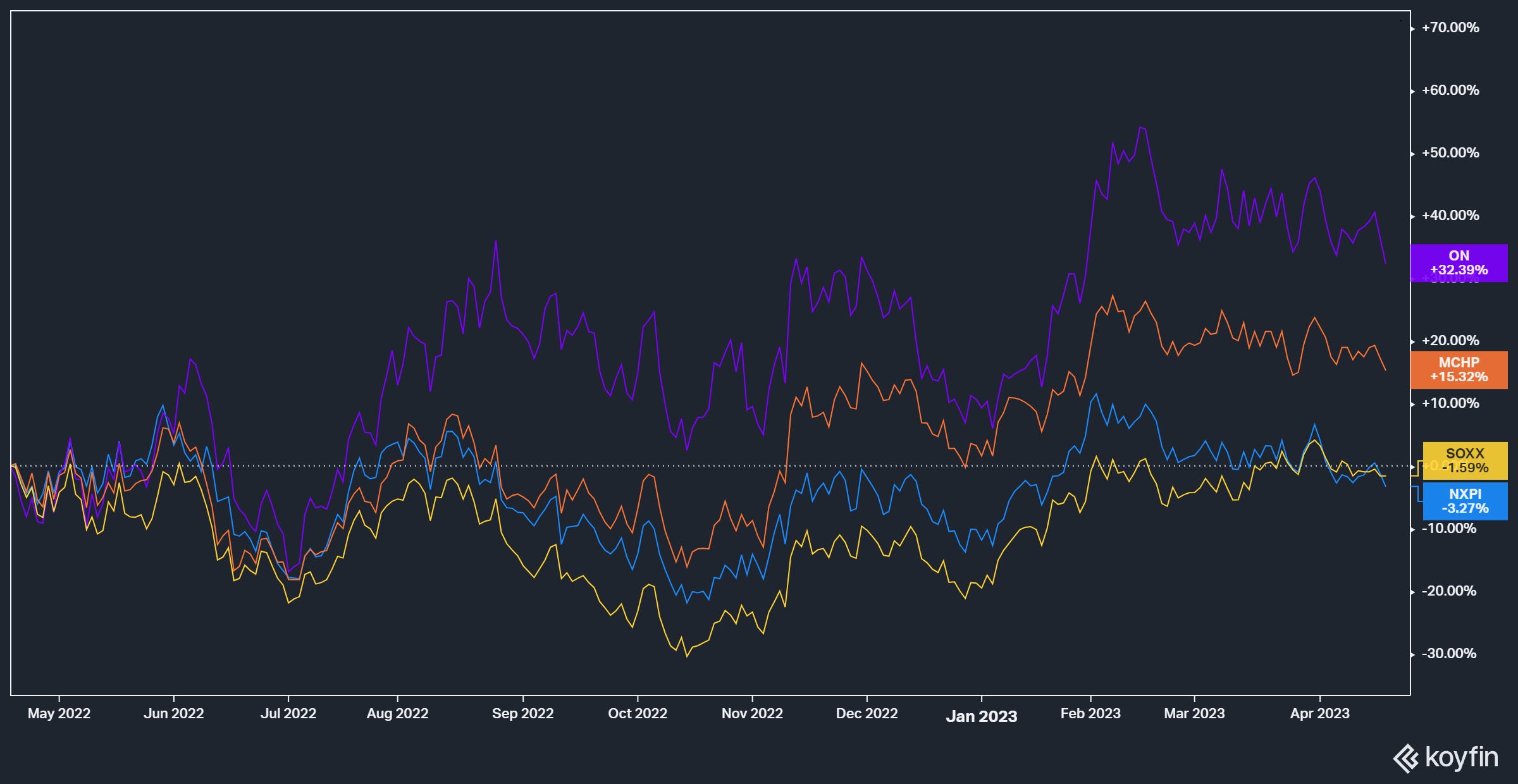

In my opinion, NXPI, ADI, and TXN have already started to crack a bit, and now it’s likely time for ON, IFX, STM, and MCHP to follow as well. This upcoming quarter we will likely see inventory increases accelerate.

I wrote back then that industrial was beginning, and now I think this is likely a strong short candidate in this environment. In particular, I would look at ON’s staggering relative performance to collapse into SOXX.

Something that worries me is that it looks like the inventory cycle for industrial companies is just beginning. IFX, ON, TXN, NXPI, and MCHP just started to increase inventory days.

It’s time to avoid industrial exposed companies, as their inventories are increasing, automotive is weakening, and they are the next shoe to drop. Stay away. PC is likely to bottom, as PC ODMs have bottomed in revenue. So remember the FIFO of this inventory cycle, Crypto GPUs, PCs, and Memory, and then Handsets and now networking. Industrial and Automotive look next as weakness in the broader economy hit their P&Ls.

For short candidates, this great graph (H/T NuanceCapital). Honestly, Melexis, ALGM, and NXPI look like great candidates. NXPI’s inventory is increasing quickly.

CDW Says Further IT Spend Weakness

CDW is a company I haven’t thought about in a long time, but it is one of the best reads on global IT spending. They are a leading provider of hardware reselling to multiple governments, businesses, and education. Here’s their revenue breakout. Notice how big of a sample size that is, $20 billion!

Well, CDW put out one of the scariest guides for IT spending we have seen in a while.

The first quarter was marked by a period of intensifying economic uncertainty that led our customers to spend more cautiously and prioritize mission critical initiatives," said Christine A. Leahy

Given first-quarter market performance and near-term conditions, we currently expect the US IT market to decline at a high single-digit rate in 2023, recognizing that a number of wildcards may impact this view as the year progresses. Despite these market conditions, we continue to target net sales outperformance of approximately 200 to 300 basis points in constant currency.

For context is past recession performance, meaning this will be almost as bad as 2008-2009! High single digits is one of the worst declines we have seen in decades, and it’s time to take note.

And before you say, “Well, isn’t this just software spending declining?” I want to point out that the majority of their revenue is hardware. They have a detailed breakout, but 30% of their revenue is PCs, and 11% is network equipment, which has to be the ultimate indication of weakness in hardware. Below is their breakout from their Annual report.

Watch out - things are bumpy there! Let’s now talk about networking again.

Not A Good Word About Networking

I wrote that networking looked bad in my “The Optics Aren’t Good” piece, but honestly, at this point, I need to state that things have gotten worse because every incremental piece of news has been bad.

Viavi VIAV 0.00%↑ - a network testing company pre-announced negative.

Viavi Solutions guides Q3 revenue $246-248M vs prior guidance $256-276M

"The pullback in R&D spend at network equipment manufacturers (NEMs) and semiconductor companies was much higher than anticipated leading to revenue and non-GAAP operating margin coming in below the lower end of our guidance...The spending conservatism and rapid slowdown

ERIC - the Swedish Telecom giant, put out weak results.

Outlook - expects the slower growth the company saw in Q1, caused by the slower global economy, to continue in Q2

AT&T put out languid capex, and their working capital issues lead to negative FCF. This implies too much inventory at telecom companies. This will likely hurt many networking companies immensely.

Capex $4.34B vs. Consensus $5.25B

With all this incremental information, I have to reiterate that it will be ugly for networking and networking-exposed semiconductor companies. It’s time to consider shorts in this space.

The very dumb way to think about it is this chart. (Also from NuanceRocket on Twitter) is to probably want to get short companies with higher exposure to wired communications. That would be MTSI, MRVL, and MXL, first and foremost.

These will all disappoint, and shares are down, but it usually persists for a bit when the inventory cycle starts.

Advantest and LLMs

A parting thought - Advantest had one of the odder callouts, and given their testing base is mostly HPC instead of Teradyne’s Apple, this makes sense. Automotive, Industrial, and Networking are all weakening, yet LLMs and GPUs are accelerating.

Advantest observing spike in demand for chip-testing devices - Bloomberg (¥11160)

In an interview, Advantest Co-Chief Strategy Officer Yasuo Mihashi says that Advantest is the industry's dominant player, and so benefits when something like ChatGPT expands uses of high-performance computing

Despite that, HPC at TSMC is negative. LLMs today make such a small portion of the big picture it’s not enough to bail out TSMC yet. It seems that ex-Nvidia, it’s very small.

I’m going to leave it here for today. I will write about ASML and Lam Research behind a paywalled post with this analysis. I actually found Lam Research’s call very bullish for memory, so I want to write about that shortly.

For free readers, this is pretty much what I typically discuss during earnings season, and if you’re trying to keep up with the space, this is what a typical paid post looks like. Lots of insights and ideas.

I think I do a good job, and while I’m not always right (that’s impossible), I do my best to create a straightforward feed to read and be on top of the semiconductor space. If you found this helpful or want to support me, consider a subscription. Even a share helps!

For paid subscribers, expect another post about Lam and ASML this weekend.

How do we square a slow down In Automotive with the extremely low inventory on hand, inventory to sales ratios are still at a fraction of pre-COVID and cumulative production is many million units below where it was trending pre-covid. Do have any visibility into chip inventory at the auto OEM’s? What you are saying makes sense but trying to square it with the end market supply-demand.