At the Heart of the Datacenter: 400ZR, PAM4, and Networking

A high conviction semiconductor / optical company that is a bit off the beaten path

Hello and welcome to the first paid substack post! While I love my free subscribers, I think that the amount of work here warrants me not giving it away for free. For the format of this writeup, I’m going to do one long single piece write up with references to later follow up pieces. This is a technical company, and there is a product transition going on, so there are many things that have to be explained.

Edit - I will not be doing a lot of the follow-ups anymore.

The layout is going to be simple

This core writeup

An industry writeup

Marvell Write-up

Inphi (IPHI) is at the Heart of the Datacenter

Inphi is currently at the perfect confluence of tailwinds. There are multiple drivers and technology transitions and Inphi is well-positioned within an industry that will become increasingly important for datacenter and warehouse-scale computing.

Inphi is currently a compelling investment because it is just beginning a long product cycle where it will be a dominant market share leader for the foreseeable future, it has long duration secular growth drivers and a history of consistent execution, and is finally hitting the flywheel of absolute R&D spending that has punished their operating margins for so long. The company in my estimate should grow at a 30-40% 3-year revenue CAGR from 2020-23 (this could prove conservative) and currently trades for ~26x (my earnings) next year’s earnings. The market believes this company is a commodity-like networking company, while Inphi has consistently shown it not only can outcompete some of the largest players in the space but also it has acquisition savvy and standout management team and culture.

Something very special is happening right now at Inphi, and without the right lens, most of the investment community is missing it. There are reasonable concerns about if their current win streak is sustainable, cycle risk and competition, and the dreaded revenue laps to come, but this is all noise. The best is yet to come for Inphi.

Inphi’s Revenue Opportunity

A 30-40% revenue CAGR implies 2-3x revenue growth over the next 3 years, and I believe that this is the “most important thing” for this company. There are other drivers, and as I have peeled back the curtain on this company, there are many favorable other attributes I will discuss later. But at a high-level, revenue growth is all that matters for this company’s stock. So why do I think it can grow so much?

Product Wins into a Networking Cycle

From a top-down perspective, this is the most important graph to appreciate its revenue ramp to come.

The company itself publishes this graph, but the PAM4 (we will discuss) observation is added by Citigroup. This is the crux of the thesis, Inphi has more content in the 400G cycle than it did in the 100G cycle, and it has more content in the 100G cycle than it did in the 10G cycle. As we sit here currently in the third quarter of 2020, we are on the cusp of the 200G/400G ramp, and the 100G ramp is well on its way. Many of the results year to date have importantly only been the impacts of a single large customer ramping 100G, Microsoft. Many more customers should ramp next year, and we are in an awkward time period in between. But before we go any further we must discuss what exactly Inphi “does”.

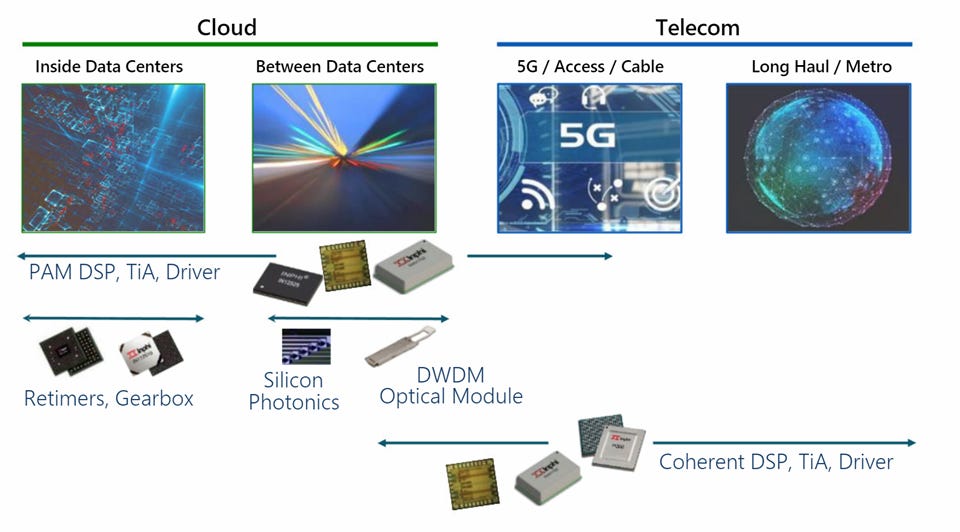

Inphi sells Semiconductor Components Primarily to Cloud and Telecom Customers

Inphi makes DSPs (Digital Signal Processors), TiAs (Transimpedance Amplifiers), and drivers for cloud and telecom customers. A simplified graphic from Inphi is below, and in the follow-up industry dive, we will discuss into the grittiest detail their entire portfolio. But for now, DSP’s and TiAs are the core products to know.

But to suffice - there are two big revenue pools for Inphi, and they even break it out in recent quarters. The ones we really will focus on are Telecom and Datacenter, and please note that a majority of the bars are my estimates.

The core observation here is that this business used to be more Telecom than Cloud-focused, and going forward it will be overwhelmingly more cloud-focused. Don’t put too much emphasis on these specific numbers, my revenue model is driven by a much simpler method, but directionally I think this is “correct”.

So splitting the above product portfolio into Cloud and Telecom, this slide is a pretty good overview.

Let’s mentally group the products into two buckets.

In the first bucket, Cloud datacenters, PAM4, and short-distance transmission. Pam4 is the opportunity for short-range, intra-datacenter transceivers that have higher modulation rates than previous generations. By means of a new modulation technique, the same piece of fiber can have 2x the previous bandwidth.

The second bucket is 400ZR, longer distance transmission, and partially telecom customers. Additionally, “edge” goes into this bucket, as 400ZR will be important to peer datacenters to edge data centers.

What is PAM4 and 400ZR, and WTF does Inphi Do Again?

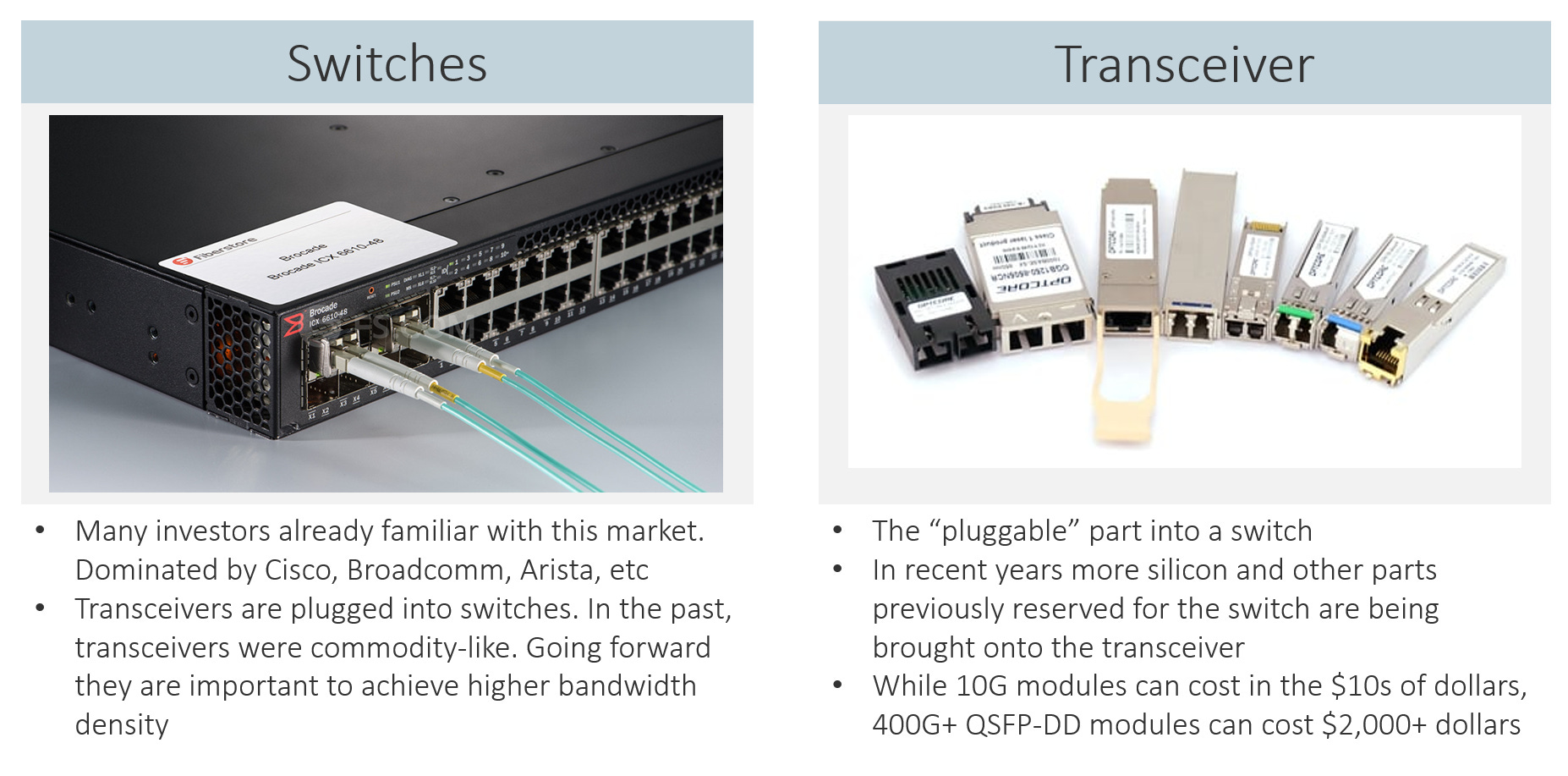

Inphi makes transceivers. Transceivers are plugs into switches or other datacenter chassis components. Transceivers sit at the end of a piece of fiber and are kind of like scaled up ethernet plugs.

Many of you are familiar with switches and routers. Transceivers are pretty much the turbo version of the ethernet cables that plug into the switches and routers that you may be familiar with at home. I think to understand Inphi’s transceivers, we should just think about a basic ethernet cable you have in your house, then scale that up to 400G.

The ethernet cables you know and love have bandwidth capabilities of 10-100 Mbps. The cable transmits analog signals which are converted via a typical DSP manufactured by the likes of Texas Instruments. The DSP lives in the box and these types of products are served by the typical analog semiconductors you would expect. In many ways, this is similar to the setup of transceivers in the datacenter but just harder.

Instead of 100mbps, it is 100-400 gigabits, it’s scaled up by a factor of 1000-4000x for 100GB and 400GB respectively. And what is a “solved problem” at 28nm+ higher geometries, becomes very hard at smaller sizes with more complicated bandwidth problems. Inphi is just selling that DSP that TXN makes in larger geometries, but 7nm and all the problems that come with a DSP for a product with 1000-4000x improvement.

As you can guess by now, the DSP is the core product that Inphi sells. Inphi also sells something called Transimpedance Amplifiers, or TiAs for short. TiA is a crucial part of the analog to the digital and is tightly coupled with the DSP. The TiA is a product Inphi developed in house, and the DSP is a product that was added to the portfolio in the ClariPhy acquisition. Inphi makes other products listed above, but the DSP and TiA combo account for approximately half+ of the cost of the transceiver (per management), and based on public competitors’ gross margins, the vast majority of economic profits from each transceiver. Additionally, you’ll find the key differentiator between transceivers is the DSP.

Inphi, of course, has competitors but from my perspective, they seem like market share leaders in every market they are in. In TiAs they are considered the gold standard and have shipped more components than all of their competitors combined. In PAM4 DSPs, they have a 60-70% market share and only one real competitor and despite the consistent threat of entrance, we have not seen Broadcom’s PAM4 DSP in the market in a big way. 400ZR is not a market that has fully ramped, but if history is to repeat itself, they are likely a #1 or #2 player. According to interviews with experts in the industry, Inphi is one of the few key vendors in transceivers that will ramp 400ZR. Acacia, the leading 400ZR DSP has also fallen off as it has been acquired by Cisco. Now merchant silicon vendors will opt to go with Inphi over Acacia because of competitive reasons.

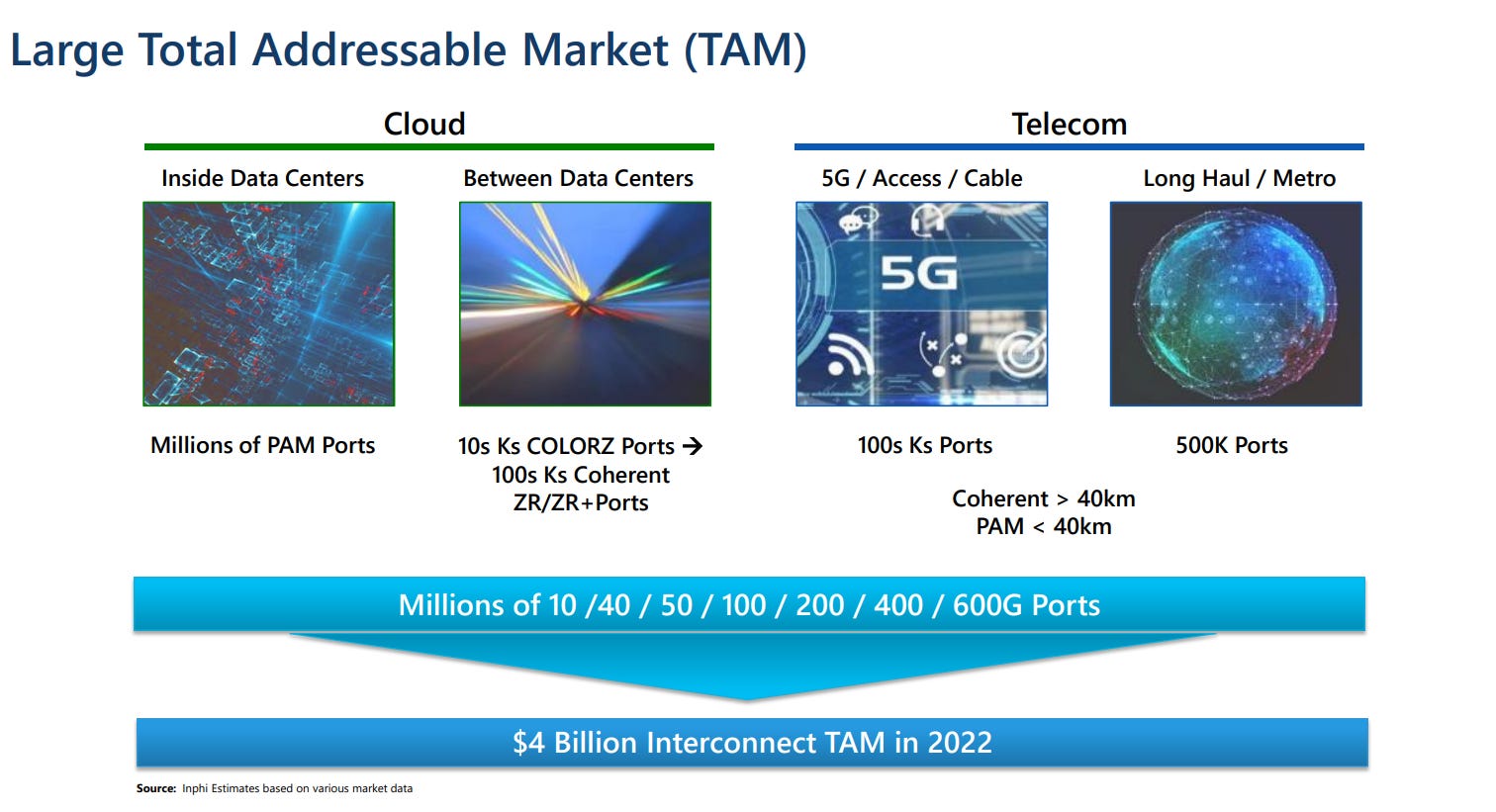

Together all of these large markets are growing at very fast speeds, and a simplistic way to look at it is their self-reported TAM.

This is a pretty nutty graph, and if true consensus numbers are totally off for the out years.

Top-Down Revenue Estimate

There is no way to reconcile these numbers without believing there are huge market share losses into the out years, and while I think that is possible, I do not believe it is probable at all. In fact, I believe Inphi can likely maintain its market share into the out years (discussed further below)

Bottoms Up Revenue Estimate

Another way to look at the revenue opportunity is from the bottom-up approach, specifically look at ports and ASP. We are going to calculate this roughly as Port Count x Port Share x ASP = Revenue x Inphi Share = Inphi Revenue

Starting with Ports - we use the two graphs provided by Inphi.

I extracted the data from this chart, and that is my total 100G/400G port opportunity. Next, I interpolated port count from this graph provided by Inphi and got to our break out of 100G/400G port count.

That results in these numbers

It seems to me that the chart is plotting total units - so I assumed the difference is the number of modules that will be sold.

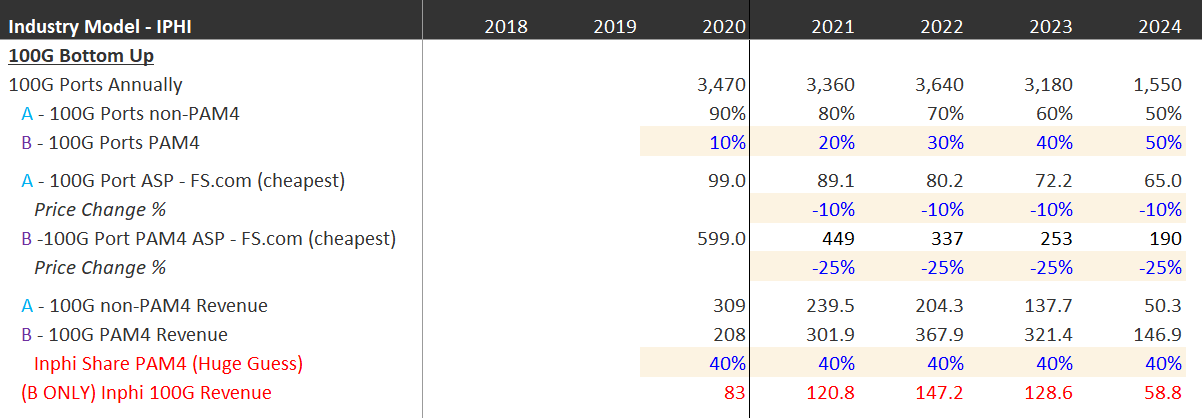

I first attempt a bottom-up revenue model for Inphi for 100G PAM4 units.

Note that non-PAM4 units probably do not apply at all to Inphi, and so are excluded from the roll-up revenue number. But clearly, there is some amount of revenue associated with 100G PAM, as Microsoft has not deployed 400G PAM and is primarily associated with the ColorZ product. According to the transcript,

“We sold (ColorZ) primarily to Microsoft. We’ve done — I think by the end of the year, it will be over $200 million in business with that product primarily with that one customer. It’s been a a very good product for us. It does enable people to connect data centers with a passive optical MUX. And in Microsoft’s Case they have 100 terabit - terabyte between those datacenters within 80 kilometers. We have the next generation of that technology coming along now”

-John Edmunds, CFO at the Deutsche Bank 2020 Virtual Tech Conference - 9/14/2020

From this perspective, the 100G PAM4 revenue estimate seems pretty conservative, but heck when you’re modeling a meaningful growth company like this, you want some levels of conservatism. I also have no idea what the market share is like from the company, as it hasn’t been publicly mentioned, and the estimates for PAM4 100G modules pretty much don’t exist. ASP declines are only 10%, since 100G is a much more mature process.

Next, we approach the 200G/400G market opportunity for Inphi

This is really the meat of the incremental revenue that Inphi will be doing over the next few years. I assume that 200G/400G numbers include Coherent/400ZR modules that will come online, and the 400ZR price premium will be about 100%. I use prices for transceivers from Fs.com.

For ASP assumption checks, I use this page for 100G price estimates, this page for 400G prices, and I choose the most popular (often cheaper than average) transceiver for ASP. It is likely that large batch orders get better pricing than FS.com, however, I want to stress I consistently choose lower specification models so there is some aspect of conservativism here. I will discuss the slight differences in modules later, but I think this likely leans conservative once again. I assume 25% price declines annually, which is in line with the historical 100G price decay.

For the DSP portion of the revenue, or the part most applicable to Inphi, I use 50% of the transceiver ASP. I know that there is some huge price discrepancy from the gross price of the transceiver to customer and net to ODM, but in conversations with management, I was quoted a 4,000 module cost, with DSP being half of that cost. This is inconsistent with pricing, but makes sense as the products that will be deployed won’t be cheaper stopgap SKUs, but fully featured products for large scale datacenter rollouts. Additionally only assuming its DSP revenue is another layer of embedded conservatism, as the TiA (Transimpedance Amplifiers) is often another material part of the cost of a transceiver, and I don’t assume any higher take rate for that. Yet another level of conservatism.

For market share in PAM4, I assume 70% this year, as they mentioned 65% share in Q1, and “even better in Q2”. As other competitors ramp (they have yet to do so) it should go down, but likely Inphi will retain a meaningful part of that share given it is now the embedded and qualified DSP so far. Similar to other Analog companies, when all the parts work together, it is very unlikely to be designed out. Especially in the case of physics sensitive products like Inphi’s DSP. This is very similar to the RF products in phones, but obviously a bit less sensitive in form factor size. This is an aside - we will discuss this later in follow up posts.

Rolling all of this up we get to the bottom-up revenue estimate. I do realize that the 2024 number starts to fall off a cliff, but this is a function of my PAM4 share estimates from 400ZR. I think being myopically focused that far out on pretty made-up numbers is a bit tricky - and I would guess we are seriously discussing an 800gbe revenue ramp by then (of course Inphi is well-positioned for this).

I think that there are many levels of baked in conservatism so I feel decently confident in these numbers. I could be utterly wrong, but for now, I believe that the sell-side is a bit scared to actually assume the revenue ramps continue and that this isn’t just COVID pull forward because what that implies for the revenue numbers for 2021/2022 are materially head of the street. I also think that this company kind of skews small in the sell-side coverage universe, and thus they are just waiting for management to give them the next year's revenue estimate.

If any of the numbers that management themselves give out (the port count number is from Inphi corporate presentations) is correct, their next year's revenue should grow meaningfully, and this is in-excess of street estimates by high teens. I also think this is amid multiple levels of conservatism into this bottoms-up revenue number. Additionally, I want to note that the number count from management seems a bit stale, the LC total port count is from 2018, the by speed from 2019. I believe both have been slightly moved upwards, but I don’t have access to the full data.

I hope these frame the revenue opportunity, and why I think it’s going to grow 30-40% (or frankly higher if the adoption curve gets moved forward) for the next 3 years. The top-down estimate nets us 40% revenue growth, the bottom ups get us to 30% revenue CAGR.

We have just been talking about revenue this entire time, and I can meaningfully point to above street estimates. Let’s get down and gritty to another truly interesting part of the story; margins. Specifically what investing to hide core profitability can do for Inphi’s operating profits.

Margins and Incremental Margins

This is part of the story that I am most interested in. Inphi is a very interesting story partially because despite growing so fast for so long, their profitability has been lacking, to say the least.

The company has managed to over 10x revenue, yet struggles to be profitable. Why? Why are they so unprofitable when their competitors have been decently profitable in comparison?

It’s not their gross margins, as they have consistently been better than peers over time. This can partially be explained because they have more silicon content (better margins) than optical. NPTN for example will never have 50% gross margins.

Clearly, it’s not their revenue size, as they have many much smaller competitors that are more profitable.

But rather it seems to be this - R&D as a percentage of sales has been something else.

This is just absolutely nutty - Inphi has been spending 40-50% of sales on R&D for a long time! Assuming a normalized ~65% gross margin, normalized 50% in R&D, and around ~20% of sales in SG&A - this company has been investing in growth at the max amount possible for the longest time at the highest level, and is a very weird or special story from this light.

Check out their absolute dollars in spending for example (sorry my data plugin does not have 2020)

Inphi has been spending with the rest of them for a long time. For example, look in the 2015-2017 time frame, wherein absolute dollars Inphi spent ~87m-182m, or slightly under the amount Acacia and Maxlinear spent a year combined. At this time Inphi only had ~200-300 million in revenue, yet spent slightly less than Acacia and Maxlinear combined did, which combined had revenue of ~2x bigger than Inphi. This is just mind-boggling amounts of spend! But in hindsight, it all makes “sense”. Inphi brought to market some of the most technically advanced products and went “all-in” on PAM4 and 400ZR before anyone thought they were a real market.

It is not surprising that they won, and in every conversation for 400ZR / PAM4, they are mentioned, when a few years ago they were the smallest kid on the block. I think this is where the next part of the story gets really interesting, and that is Management. Ford Tamer looks to be an incredible CEO, with an incredible eye for acquisitions, target markets, and strategy. There is no other way about it. You can deck him for financial discipline, but you cannot deck him for being the absolute outsider and winning the entire market. I will discuss more in management, as I think it’s an important part of the story, but clearly, we have something special on our hands.

I think it’s best captured by this quote at Stifel on June 20, 2020

Tore: Yes, Ford. So maybe I can start with you. And if you don't mind, I would like to start at the higher end of things and moving to specific questions throughout the call. And you may be getting a little wary of PAM4 questions. So I'm hoping to take you down history lane. You became CEO of Inphi a little more than 8 years ago, and I met you about 2 weeks into the job, I believe. And I've been able to remember what you told me at that time, you basically said, "Tore, we're going to invest a lot of R&D dollars in the next few years." So with that backdrop, can you give us a summary of the 8 years? What went right? What went wrong? And what are some of the most important things you've learned as a CEO along the way? I know it's a long-winded question, but to the best -- so although if you can give us a summary, that would be great. Thank you.

Ford: Thank you, Tore. You've got a very good memory. So the first thing that went wrong, if you remember is, when we said we're going to invest a lot, the stock went down from -- when I joined at $14 to a low of $8 that year. So it was a good awakening. And we -- then over the next 8 years managed to gain the trust and confidence of our investors, and they allowed us to continue to invest because we've shown to be good stewards of their money.

So what were the things that went right or wrong. I think the first thing that went right is really the team, which was a foundation for everything. So I joined Inphi because we had a just phenomenal founding team, done in Westlake Village, folks from Hughes Research and -- above Malibu and some folks from Broadcom, and that founding team is still with us today in the company. We then proceeded to add to it a very strong DSP team out of Broadcom and Marvell. We added a phenomenal silicon photonics team with our CTO, Radha Nagarajan, who joined us from Infinera, and a few people that he hired from different optics company in the Bay Area as well as Singapore as well as Westlake Village. And then we've added multiple teams from acquisitions, so the Cortina team up in Ottawa; the ClariPhy team in Irvine and Cordoba; recently, the Silicon team in multiple geographies worldwide, and continued to hire around the world. So I think this is probably still the basis for why we are able to do what we do is really the phenomenal team that we have in place today.

The second thing, I think, is the courage to dream and invest. It's not easy to invest in a sector like ours because people are not used to see companies grow. But we set our goal on growing above industry average, and we have done so for the past few years. And directionally, when I first joined and we had a $35 million-or-so semiconductor communication business, and we're talking about getting to $0.5 billion people didn't believe we could do it. Now it's clear we're going to go past that, and our goals are on $1 billion. And I think we'll get there in a couple of years. And so really the courage to invest and to dream big, I think, is probably the second foundation.

Anyways which brings us to target margins. I don’t think Inphi is going to continue to wreck profitability at the expense of investing as much as he did in the past. There is something nice about Inphi finally hitting the size it can, is that it can now outspend its competitors in absolute terms with a smaller percentage of revenue. It also helps that they are among the highest gross margins in the sector.

When I was on a call with IR, they mentioned that they expect to grow SG&A GDP+, R&D will grow in absolute dollars but drop eventually to mid-20% of revenue over time, and that operating margin should be in the 20s-30s in the next 18 months. They clearly have not put out a target operating model, and this is all Non-GAAP, but that is clearly really good news for shareholders.

My high-level numbers from my model have them flexing something like 30%-40% incremental operating margins. While that still does not lead to insane margins, 40% is about as good as it gets in EBIT margins for semiconductor companies (NVDA for example - fabless and growing fast at 40% EBIT margins is pretty much the best case) but I think that they can get to that over a longer period of time.

Let’s say they could get to 35% Non-GAAP EBIT margins in 2022, let’s see what that gets us.

Once again - meaningfully ahead of sell-side (sorry not to bash them - I get it, it’s scary to project this honestly). There will be a fuller discussion of Capex, capital returns, and other information in follow-ups, but for now, I think just focusing on their extremely good underlying unit economics, and the likelihood of stronger incremental margins is really attractive to me.

Valuation and Rolling it All Up - What’s It Worth

Inphi to me is a really insane growth story with a lot of things going its way. We will talk in further detail in follow-ups, but it seems very clear that Inphi is the most important part of an incremental hardware cycle, with some of the strongest customers and one of the most secular themes around (Cloud computing, edge, streaming video, games, etc). Inphi should exhibit above-average growth for a long time, all while growing operating income above revenue as they grow their absolute R&D budget larger but slower than revenue. The revenue growth and margin story are one of the best growth stories I’m aware of - yet it trades for 32x 2020 street earnings, which I believe are 30%+ too low. I will not give precision, but rather a range, but I believe that Inphi will do ~3.40/4.40-4.80 in FY20/21 - or 23-30% above street estimates.

Assuming $4.60 midpoint, I believe Inphi trades ~26x earnings at a price of ~$120, and you get to invest alongside one of the most driven and exciting growth stories in semiconductors, opticals, and cloud computing broadly. EBIT growth is not slowing either - and Inphi should feasibly grow 40-50% EBIT CAGR until 2023/24. There are also a lot of additional ways to win - as Ford Tamer is literally a genius allocator and has alluded to a new product launch. There may be problems with terminal growth, but network growth and its continued importance in our lives are likely secular, and Inphi will probably acquire or invest in new adjacent categories to participate.

Inphi is expensive compared to peers - and while other competitors will likely “beat” earnings I believe Inphi’s earnings beats are likely far ahead of competitors. A more detailed comp sheet will be coming - and we will be discussing comps pretty in-depth as well.

Additionally, I believe that we are on the cusp of Inphi’s relative advantage compared to peers, as DSPs and transceivers will become a more important part of networking during the 400G+ cycles. I think there even is a case to be made that they should be comped closer to the data center growth semiconductor companies categories, which would make this thing trade at a “discount”. The logic might seem insane at first glance - but behind servers, interconnect is the #2 source of spending in Datacenter, and in many ways is just as strategic as GPUs right now.

It’s also not lost on me that this list likely contains a lot of other winners. In particular, LITE trades cheaply and has had a great history of returns. MXL is also no slouch either and is a real competitor to Inphi. Cisco for all the hate has a very compelling capital return program. Heck Broadcomm always screens cheap considering its growth profile. The entire industry is reasonably attractive (don’t kill me - this comp sheet is a bit messy, some optical some semis), and importantly is becoming more strategically important going forward. If anyone is paying attention to the product announcements at Nvidia, they should understand intuitively why this applies particularly to networking. Inphi as it currently stands is the one that I think has the best mix of pure-play growth, potential upside, and management team mix to become a glaring attractive investment.

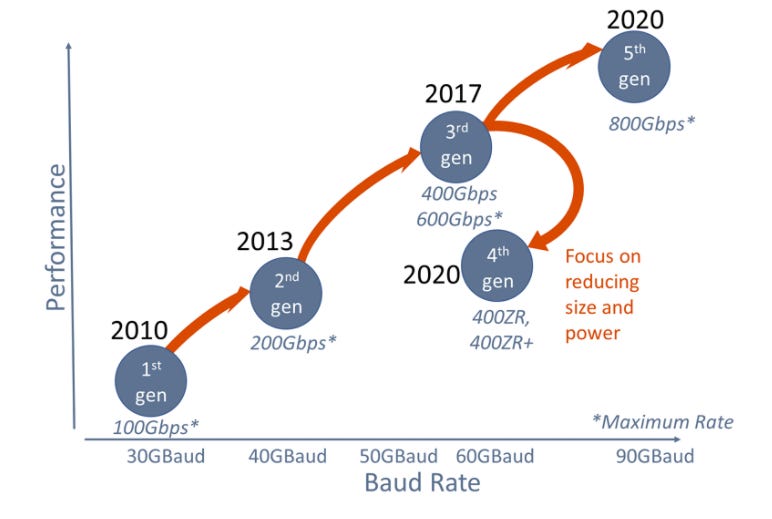

A Side Note on 400ZR Adoption

The thing that really excites me about the 400ZR (and partially PAM4) adoption rate is the “better faster cheaper” aspect of 400ZR. 400ZR is a bit different than the previous generations’ past.

This handy graphic from cignal.ai really puts it into focus. The initial 400G cycle actually happened in 2017, and mostly focuses on the long-range transmission of data. The 400ZR cycle is something totally different.

source: https://cignal.ai/2019/12/5th-generation-optics-4q19-update/

The 400ZR cycle is kind of a mini-cycle, where the form factor and power are reduced while offering similar speed to previous 400G generations. The difference though is that at a smaller size and footprint, the industry can replace a previous component that costs money to achieve the same result. So while 400ZR modules are expected to be expensive, the net savings will likely be a lot cheaper. Many industry participants are making this claim, and some believe that it will be an order of magnitude cheaper. This is what really is exciting about Inphi and 400ZR to me - we clearly see a substitution product that can replace hundreds of thousands of ports at a high ASP, while still offering large net savings to the customer.

Here are some graphs that kind of represent this, this time from Arista networks.

Another really interesting trend that goes hand in hand with 400ZR/PAM4 is IP over DWDM. This simple chart below inelegantly gets at the heart of what is going on here. 400ZR transceivers are replacing another product in networking, and while 400ZR transceivers are expensive, their total cost is much lower because it gets rid of the DWDM transport / ROADM layers. It also leads to much simpler network topologies.

The company that is most exposed is CIEN. While CIEN overwhelmingly skews Telecom rather than datacenter, but if I’m right - I believe that CIEN is the product that is primarily being replaced. I don’t have a strong view on Ciena long or short, but I do have an interesting story - and that of course is another post.

Risks

Competition - This is probably the first question that comes to mind. “How can Inphi compete”

This thread I wrote on Twitter is 100% about Inphi.

I think that is the primary thing that will keep the competition away. Being first to scale volume and being the first to 5/7nm. There is real threat of entry notably by Broadcom on the PAM4 side of the business.

We're always sanguine about not being -- and particularly with some of the volumes we're doing that the market will want a second source, that there will be a second source come along. And I think people get tired of us -- hearing us talk about it and never seeing a second source seem to show up.

So there are people who are qualifying that have their chip technology built into modules, and they're trying to get them qualified, most specifically Broadcom and MaxLinear. We're working with different players and on different parts of the market, but they're -- they've clearly developed the technology. And it's difficult to get qualified in part because you've got to have all the firmware developed and tested and all the nuances and be able to handle all the cases in the firmware. And that took us a while, and it's not surprising to us that it would take the other guys some time also to work through that.

So we assume that they will get qualified. We just don't know what the holdup or the timescape -- timetable or issues. In the meantime, we take orders, and we fill them, and we keep moving. And people seem to be very happy with our products. So I don't know that there's a terrific amount of urgency.

And they're also stuck with COVID-19 if they're trying to get new product qualified and have access to labs. The whole process of interacting has just become slower from that point of view. So having a technology that's already qualified is a big plus from that point of view because we can supply them, and there's no slowdown or hold up or testing that has to take place.

So I think it's very positive. It looks good for us. Obviously, no sighting so far. And we may not have a sighting until the fourth quarter or sometime later. But we just have to keep supplying and filling the orders. And then fairly soon, we'll be focused on 800-gig technology and getting that ready for the next generation. So that's where the next battlegrounds will be for us.

Cycle risk - This is my biggest concern. The current set up right now is that Inphi skews overwhelmingly to Datacenter, which has been shown to be strong. Microsoft earnings will give some magnitude to Capex YoY comparisons and is a strong read through for Inphi. Microsoft reports before Inphi, so it can help with positioning.

But it’s not completely immune. We won’t know what cloud spending is like, and FSLY’s first read was concerning. Obviously growing, and FSLY/AKAM/NET are partially end customers to Inphi as well.

The other side of the equation that we know is in the doldrums is enterprise and campus. Check out this survey from MS for enterprises.

I think Inphi is well-positioned relative, but it could suffer in absolute terms.

Customer Concentration - There is one big ole customer and their name is Microsoft. My concern here is that Network inventory might be built up in Q2, to account for future supply chain concerns. We will see if this bears out to be true. This is from Deutsche Bank 2020 - Virtual Tech Conference

Yes. I think it's fair to say that in 2020, there's been a lot of thought around supply chain, not just in technology or cloud within every single industry. Companies are looking at where their supply chain resides, how is it globally resilient and how can it respond to different global events. And Microsoft and our suppliers are no different.

So we continue to look at where we're sourcing our components from, how that can meet our business needs and how it can withstand the most unpredictable events that may occur, such as the global pandemic. As we look at that, we, of course, are continually innovating, both in terms of long lead activities as well as ensuring that we have the appropriate buffers and reserves to be able to respond to events, wherever those events occur in the world.

And we, of course, are balancing efficiency here with customer responsiveness, and we continue to tweak and evaluate this approach based on our learnings. And during COVID, the fact that we had a number of reserves allowed us to rapidly scale. And then we have continued to optimize that formula based on our experiences.

We've also had some learnings on our supply chain and continuing to diversify this globally to remove single points of dependence and to ensure that we have diversity across all of our fleet. And that's meant then the use of different parts of silicon. It's been continuing to do the work we do across different suppliers and then continuing to build partnerships across the industry. So definitely, as we look at capacity, buying patterns and all of the work that we're doing, we're, first and foremost, focused on ensuring customers continue to grow and that they can move the workloads that they need to move.

However, on the other side of this, sequential HPC strength at TSMC shows that the end market at a high level is strong. And that all this work from home is no slouch. Inphi likely will be okay - but we will have a customer to monitor.

On moving off of Inphi from Microsoft. I don’t think Microsoft would do that. They would have to go out of their way to deworsify their supply chain, and a second source is still a second source. Inphi will be the product ramping 400G first, and to choose another partner would be like going out of the way to find the worst partner.

China Risk - This is my favorite boogeyman. Also, the easiest to explain.

As you can see from the Q2 filing, 50% of the revenue is in China. Doesn’t this make it a huge Huawei risk?

The key thing to note is Thailand. This means they are shipping to OSATs, and it is likely OSATs in China (which China has a majority share in). This is well explained by Inphi.

Deutsche Bank 2020 Virtal Tech Conference - John Edmunds

Yes. I think on the cloud side, PAM technologies have done quite well, both the 200-gig technology, the so-called 50-gig Polaris with -- being used primarily by Google. And I think we'll see another large cloud player shipping late this year or early next using that 200-gig technology and then the 400-gig technology that's being deployed by Amazon now.

And these are both chips that we have been selling in part into a large Chinese module maker. People may remember that Google started their own module integrator in China company by the name of InnoLight. It's one of the reasons we show so much in sales into China is because those -- that Chinese module maker is making those modules and shipping them right back for U.S. cloud consumption. And so that's part of the reason that we show as much China ship-in business as we do and why it would have grown over the last year when Huawei would have been falling off.

So I think that business has done quite well. Google continues to buy at a pretty good clip. Amazon tends to be driving more of the growth overall in the business, but they're also -- look like they'll be continuing to buy on into next year. And then we'll add, we hope, another cloud player in one of the BAT, so-called in Asia, hopefully sometime in the fourth quarter, if not the first. They both seem to be making progress and will be in that time frame.

Also from the Q2 2020 Call

Paul, I'll let John give you some of the details. But at a high level, you should think of the China revenue, a large part of the China revenue comes from Cloud data center in the U.S. So we have some very significant shipment to our module partners in China, who are doing quite well, and that represents a pretty large percent of the revenue.

What you also should think about is this 5G ASIC that has now started to ramp for mid haul and back haul, they were doing with another telecom OEM operator, and that is also growing. So just don't think of China as Huawei. There is multiple customers outside of Huawei in the Telecom space. There are some strong 5G on both PAM and Coherent. There is some Cloud module -- U.S. Cloud module makers that are -- module being made for U.S. Cloud. And all of this is coming from China.

Huawei for example is less than a 10% customer

If things change, they hopefully will change to the better, and we'll have more freedom -- degrees of freedom to provide service. Huawei this year will be less than a 10% customer. So I think, overall, it's -- this whole situation has hurt the market and hurt our business. But they're a good customer. They develop good technology, and we'd like to continue to do business with them. So you will see us trying to support them at some level as we move forward here to -- certainly to the degree we're able to.

Huawei is also not in the Q3 guidance. But it’s likely at least for the Q3 they will be fine regardless. NPTN’s pre-announce for revenue was above the midpoint of revenue, and as of Q2 2020, Huawei was a 52% customer. This means Huawei shipped into Q3 for NPTN, and likely for IPHI, but IPHI doesn’t have Huawei included with guidance. So there shouldn’t be an earnings blow up in the near term.

If you somehow made it this far - please do give this a share! Anything helps now that I’m trying to grow this Substack. Thanks! Feel free to mention it, take partial screenshots, etc. Hope this is informative, and I’m excited to do a lot more value add research.

Other Writeups will be linked here

The Much Deeper Industry Dive

A Deep Dive into Transceivers

Culture and Management

In-depth Financials + Model

Disclaimer: Nothing in this post should be construed as investment advice. Author has a position in the mentioned company.

Hi - I am a big bull on IPHI but your PAM4 estimates are too high. IPHI only sells chips, not transceivers. ASP is closer to $100 than the $1000 you're using. That said, your port count estimates are too low at least for 2021.

You can get some help from here. https://ip-fiber.com/