February Semiconductor Monthly Roundup

What's happened this month in semiconductors - factor rotation edition!

Sorry that this is a bit late. I kind of forgot it was already March and I have been grinding away at a Silicon Carbide piece. Onwards!

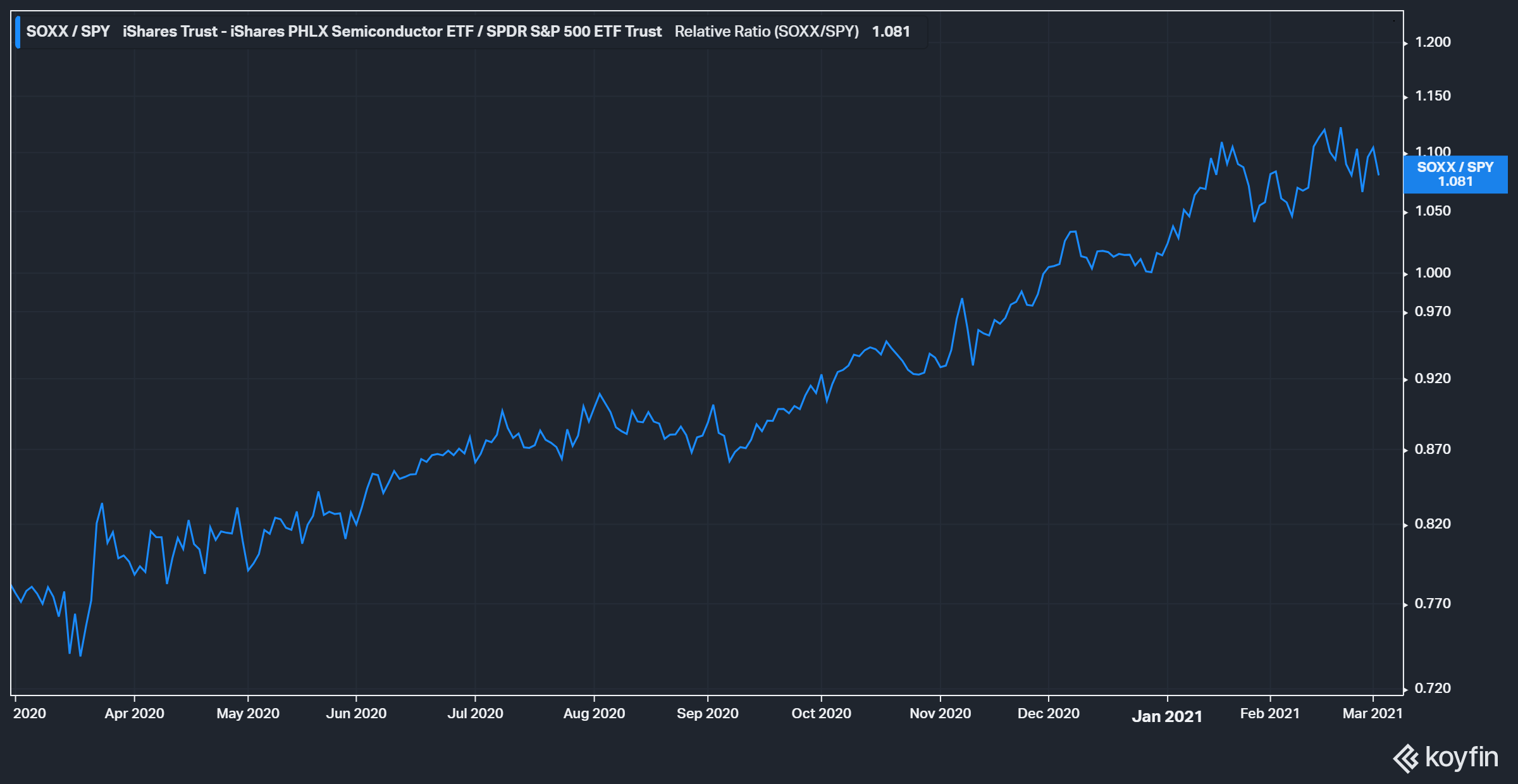

February was a dramatic month for semiconductors, surging ahead and then correcting back, while still outperforming the S&P, but much less so than January’s massive relative run. The real reason for price action drama was not because of the sector’s results, but rather the dramatic factor rotations of February.

Now it’s very hard to parse exactly where SOXX lies, but as of late, SOXX has been more correlated with momentum than value, and thus most of the factor rotations were a net negative for semiconductor stocks this month.

I don’t think this really matters as in my view many of the companies are among the cheapest, and thus “value”. But as for how they trade? Firmly with growth and momentum as of late. A decoupling of this would be nice. but I don’t expect this to happen anytime soon.

Anyways onto the winners and losers.

Us Listed Winners

First and foremost, I hope none of these names are unfamiliar to you! I have talked extensively about AMKR, KLIC, AMAT, UCTT, LRCX, and MU. There are a few others but it’s kind of great seeing most of my coverage do its thing. Let’s pick out some broad narratives.

Takeaway #1 - The Back End Leads Returns (KLIC/AMKR)

Amkor and KLIC clearly lead returns. This is because of the results both of them put up, and more specifically Amkor being put into a larger index. I wrote about Amkor and wrongly wanted to call the earnings because of the strong print of KLIC. What happened shortly after was an index inclusion.

I wrote about KLIC here, and AMKR here (I MESSED UP!). I think that the back end is running a bit hot, but there is definitely a chance the re-rating continues. One of the lingering and important parts of self-dependence is our over-reliance on Chinese OSATs. AMKR is an American company and could easily be a huge winner in the coming grants.

Takeaway #2 - Low Quality is Winning

UCTT, SYNA, and CCMP to me are clearly what I would call low-quality stocks, yet they showed up at the top of this list. For those who might remember, I wrote about UCTT being a levered AMAT / LRCX name in December on the basis that this is the time to buy junk. Year to date that seems like a wise choice. As long as there are a broad-based supply problem and a huge demand, stepping down the quality spectrum into companies with extremely low multiples and high operating leverage will not hurt you. But when the tide is out it will absolutely be a terrible idea. The tide is not going out soon in my opinion, but something to be mindful if you have any exposure to these companies.

International Winners

Takeaway #1 Again - The Backend is Winning

I would partially consider the likes of Winbond, Kinsus, and Besi as back end adjacent plays, and I believe that this is just the same theme being shown again but internationally.

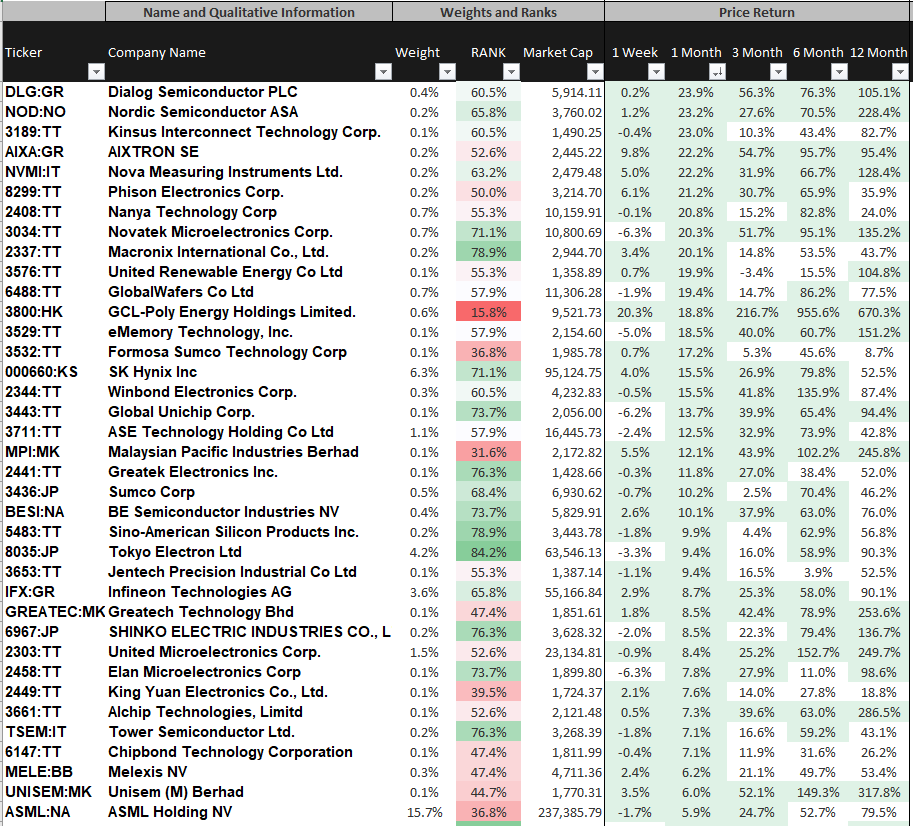

Global Losers

Takeaway #3: Large Cap Losses Amid Rotation

This is where it’s easiest to point out some themes. Some of these are last month’s winners, but overwhelmingly the thing that pops out is the size effect. The weighted average market cap of the total list is ~$3.6 billion, and not shown is large companies like QCOM and AVGO relatively underperforming as well. This very simple chart of IWM (small cap) versus large indices tells the story almost too well.

And Other Headlines

Kind of a short one, but I thought this month was relatively benign in semiconductor-related news. We are just digesting earnings and waiting for the next shoe to drop. I’m going to post some things I think are worth reading about.

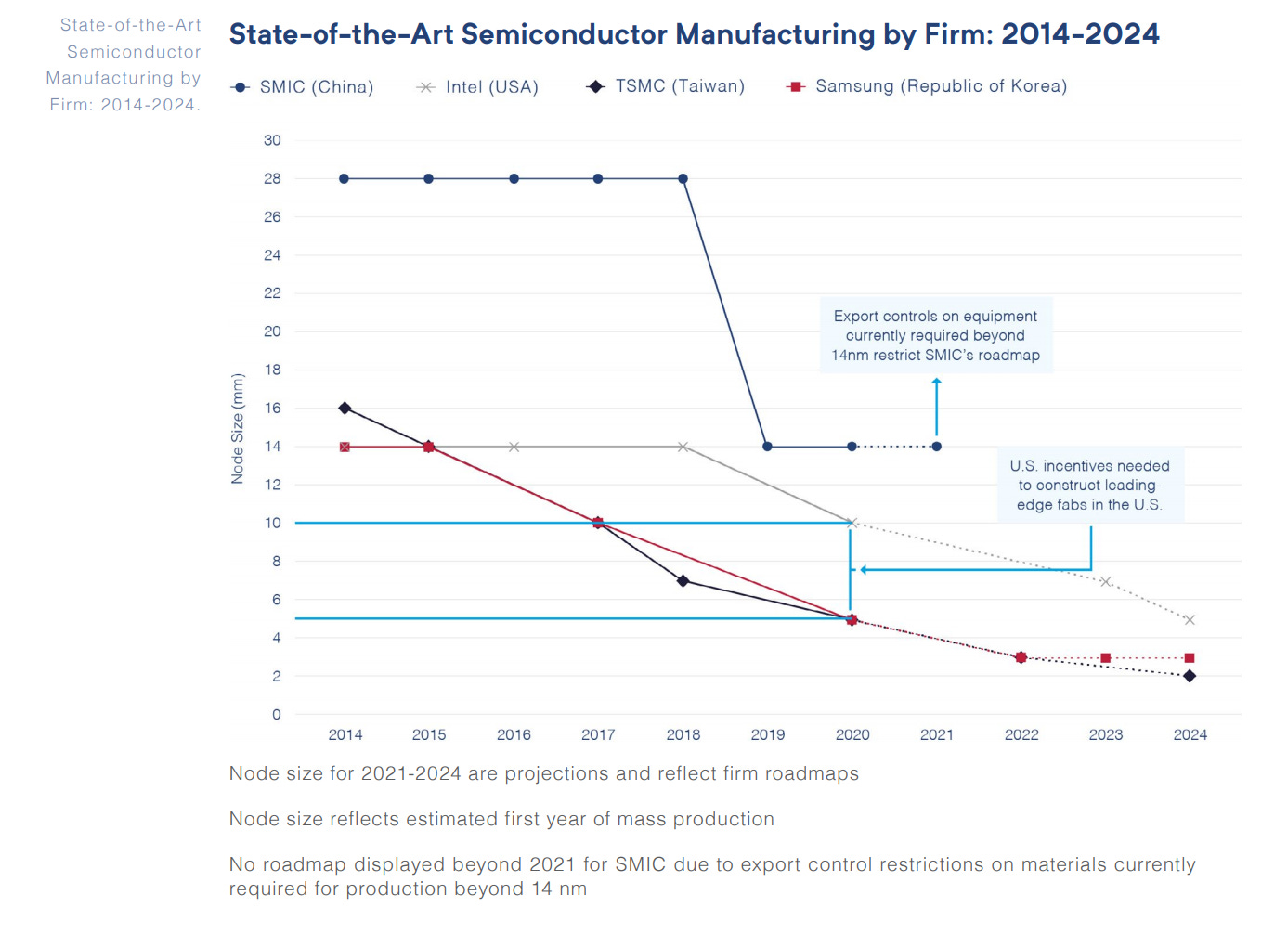

SMIC Is finally getting to purchase Semiconductors Again

The first thing they did of course was to buy ~$1.2 billion in ASML tools. It’s hard to guess what is leading or lagging edge, but I want to note that DUV can go as low as the TSMC 7nm process.

Another thing I find interesting is the National Security Commission on Artificial Intelligence endorses the CHIPs act.

I tweeted briefly about this - but the 40% tax incentive number seems kind of inevitable especially when “other leading semiconductor manufacturing nations such as South Korean, Taiwan, and Singapore offer 25 to 30 percent cost reduction, roughly double what the United States currently offers”. I don’t think the market is going to fully appreciate what 40% would look like until it happens.

This Thread on Semiconductor Startups in China is a must-read

But I find it also very funny to read while paired with the huge shuttering of the HSMC fab. That was reportedly $20 billion dollars spent that looks to partially be defrauded or defunct. They laid off all employees and there are no plans to restart manufacturing anytime soon.

But despite this setback, it’s not like China is going to quit. It’s kind of enviable their persistence and how seriously they are taking this. The US and EU need to step up as well if they want to keep up. It seems easy to draw a cold war narrative, and the formal recommendation of the NSCAI was to “keep two nodes ahead” of China.

Magnachip looks to be trying to sell itself

This is a very good idea on Magnachip’s part in my opinion and could be worth a speculative position. It’s up meaningfully on this news, but it is firmly in the desirable part of the market currently, automotive. Given the bidding wars at COHR and the renegotiation for ACIA higher (optical but still), it seems like this one could go for a pretty penny.

Anyways that’s it for today. I expect to have two more large pieces before I freeze payments for Substack (for those who don’t know, read my about page). I now am going to be freezing my payments a bit early so I feel like my readers still get some value. I think March 15th looks to be the date, and I understand any churn. I hope to post the SiC piece this week, and a broader automotive semiconductor piece in the second half of March. Thanks for reading and I appreciate everyone whose been along the journey so far.

Thoughts on ASML at these levels? Know you've mentioned that ASML gets/has been expensive in the $600 range - Still expensive here in the $500's? Also, We'll miss the posts, but wish you luck on the journey!

I wonder your thoughts on big a risk this is https://www.bloomberg.com/news/newsletters/2021-03-03/chip-shortage-2021-it-s-time-to-start-worrying-about-a-glut?sref=UVzE81xN