It's High Time to look at SiTime

Sponsored Deep Dive by Tegus: SiTime, the MEMS Timing Company

First - Let’s thank Tegus. So much of the work I did on SiTime was only possible through Tegus. I will split this write-up into two pieces, the business overview, history, and industry analysis will be in front of the paywall.

The competitive analysis, valuation, conclusion, and full 3-statement model will be behind the paywall. However, if you found this work informative and would like to read more, I sincerely appreciate your support through a subscription. I love doing rabbit hole dives, and each subscription allows me to write about the things that I think are compelling in this market.

I want to reiterate this is a two-part piece, and you should read the timing market overview before we continue to this portion of the writeup. This part will be exclusively about SiTime.

Here’s a brief outline of the company dive. Strap in. This is going to be a long one. I recommend printing it if possible.

Brief History of SiTime

SiTime Investment Thesis

Company Fundamentals

Unit Economics

Timer Market Sizing

Competitive Analysis

Product Overview

Competitive Strategy (paywall)

The threat of Entrants (paywall)

Current Cycle Problems (paywall)

Valuation and Model (paywall)

Comps

Discounted Cash Flow

Conclusion (paywall)

Pre-Mortem (paywall)

A Brief History of SiTime

SiTime sells MEMS-based oscillators. MEMS stands for Micro-electromechanical systems and are mechanical devices that use semiconductor fabrication techniques to make tiny devices. The same properties of physics that happen at the human scale are also consistent at the nano-scale, so why not make the accelerators, gyroscopes, and other mechanical devices tiny and use less space and power? There’s a whole class of these semiconductor-like devices that live in our phones and power our lives, but I’m going to focus on oscillators and timers. That’s the purvey of SiTime.

SiTime solved one problem that plagued technologists: a mechanical-based resonator to replace quartz technology. Resonators are simple to conceptualize as tiny tuning fork that resonates when energy is applied. This compares to quartz, which also resonates when electricity is used but is larger and often more fixed in function. We will discuss the differences in depth later (or in my previous post about timers - a must-read!)

SiTime is also the lone survivor of an arms race. They were not the first company founded to solve the MEMS problem, but they succeeded where companies like Sand 9, Discera, IDT, SiLabs, and likely many others failed. SiTime was first to market and, more importantly1, first to scale. SiTime was founded in 2005 by a group of engineers from Silicon Valley. The primary founders were based out of Stanford, and the company started essentially as a group of engineers with yet another idea for the MEMs timer market.

Like every MEMS timing startup, the goal was to disrupt the Quartz market. It’s always been a bit of a holy grail in MEMS research to make a stable resonator to displace quartz. The benefits seem obvious, with a cost-scaling roadmap aligned with semiconductor fabrication and miniaturization that could be smaller than quartz. However, the technology has a long way to go regarding potential improvements. The first idea for resonant transistors happened long ago, in the 1960s.

A resonator was always of interest, but good ideas take time. One of the primary problems was that MEMS resonators seemed to have real problems with aging and reliability. In particular, the MEMS device had to be isolated from its surroundings. A resonator would work, but it couldn’t have any interference from the outside world to be stable.

The founding team knew this, and one of their significant breakthroughs was an invented technology called Epi-Seal. The gist is that they surrounded and isolated the device with hydrogen, etched vents into silicon, and then baked the device, effectively hermetically sealing it in silicon. So now, the resonator was isolated from the outside world.

This was no mean feat and is a patented technology by the founders of SiTime. This was done in conjunction with Bosch, a partner of SiTime to this day. Silicon MEMS had been attempted before, but the big problem of packaging to make the MEMS resonator work was solved. SiTime’s novel packaging idea worked, and that is why I believe they “won” the race to MEMS oscillators.

The company then would toil away as a private company with zero revenue and intensive funding costs for a few years. The cumulative funding, according to Crunchbase, was approximately $105 million dollars, but the funding tables lack a series A or B. At this time, the primary problem was scaling the MEMS resonator process for high-volume manufacturing at attractive economics, as well as improving the performance and reliability of MEMS. They were not the only company pursuing this.

The race for Silicon MEMs was still on, but many competitors were failing financially. This is where SiTime's next pivotal moment would happen, which would come in the form of Megachips (JP: 6875), which bought SiTime for $400 million in November 2014. Given the cumulative ~$80 million dollars of equity investment between 2007-2014, I don't think this was quite a homerun for private backers.2 Here’s what Megachips commented about SiTime during their acquisition.

SiTime develops MEMS timing devices that replace existing quartz oscillators. They have already been used in the digital cameras of major manufacturers, tablets, wearable devices and infrastructure equipment for server communication networks. SiTime is a leading company with a market share of over 85% in the MEMS timing devices market.

Megachip’s funding and stability as a larger company would help SiTime live through the cash burn, as at the time, SiTime was still subscale and losing money. Megachip’s financial sponsorship likely helped them weather the long cash burn to get to the other side while competitors everywhere failed.

SiTime had a productive time introducing products during this time. For example, their “Super-TCXO,” an important product that would help their traction in important markets. Later next year (2016), Megachips would state that SiTime has “more than 90% share of the MEMs timing device market”.

I think I need to mention another important player; Bosch. Bosch and SiTime announced a partnership in 2018, which looks like a fluffy press release saying they care about each other. However, beyond the fluff, Bosch is critical to SiTime’s story. The original patent award for Epi-Seal went to Bosch, and SiTime and Bosch’s partnership is inevitably linked.

Did I mention that Bosch is undoubtedly the largest MEMS fab globally? That partnership is important because where potential competitors could fab limits them given Bosch and SiTime’s mutual partnership. We don’t know what the partnership means, but they reaffirmed the partnership in 2020. Bosch likely is one of the primary beneficiaries of SiTime’s continued success. Below is Bosch’s market share of MEMS fabrication.

Speaking of partnerships, Megachips and SiTime’s marriage wasn’t going to last forever, and in 2019 Megachips decided to float SiTime as a standalone entity in the United States. The initial offering was for 53.3% of the shares, and after the raise, SiTime was still an effectively controlled company.

Upon completion of this offering, MegaChips will continue to be our largest stockholder and is expected to hold approximately 46.7% of the outstanding shares of our common stock immediately after this offering, assuming no exercise of the underwriters’ option to purchase additional shares from us.

Megachips was originally the exclusive distributor in Japan, but in 2021 to expand its distribution network, SiTime ended the exclusive agreement. Megachips has also been selling down its stake in SiTime, with follow-on offerings in February 2021 and November 2021. Despite this, Megachips still has a ~24% stake in SiTime. For astute readers, you’ll notice that Megachip’s Japanese market cap of ~$342 million trades at a discount to the value of its 24% stake in SiTime (~1.9 billion x .24 = $432m USD). I’ll talk more about that later.

Anyways that brings us to today – SiTime is the world’s largest MEMs timing business. They deeply partner with the largest MEMS fab; their other key supplier is TSMC. Megachips has sold down its stake but still is a relevant player. But I now need to talk about more recent history, particularly the pandemic.

SiTime benefited from the pandemic significantly, as the combined pandemic supply chain issues compounded with the AKM fire in October of 2020 left them as one of the few timing companies with supply. SiTime capitalized on this shortage to drive the adoption of MEMS higher. There are likely problems with this over-earning in the short term, but I think what's interesting is that distributors and former Sales executives at SiTime have rarely seen customers switch back3. This temporary adoption might be a kickstart in their penetration curve, which is interesting to the long-term market share story. There's a large opportunity ahead, and let's talk about why I think SiTime company should benefit. Below is the simple investment thesis.

SiTime Investment Thesis

SiTime is the leading MEMS oscillator player with a 90% share of the MEMS timing market, which is only ~4-5% of the global timing market (~$5.5 billion) and taking share. The timing market to date has been dominated by quartz timing, a reliable and legacy technology that will continue to be the majority of the market for the foreseeable future. However, MEMS should take some share because of cost advantages, programmability advantages, supply chain advantages, and an improving technology against a legacy and sleepy set of incumbents.

I believe that MEMS (by extension, SiTime) could address 15-30% of the total addressable market by 2040 compared to its 4-5% share today. Even assuming a competitive entrant and lowered MEMS share, the company should, in turn, grow revenue at a mid-teens rate for decades and grow FCF per share even faster. The equity, from this perspective, looks extremely favorable on a long-term investment horizon. A long-term DCF requires 16-22% discount rates for the equity to be fair value, which should reflect the expected return for the equity. Given the high beta (2.5), high risk-free rate, and equity premium, that’s probably the correct discount rate. However, I think qualitatively, there are many reasons to like the company’s positioning and growth prospects, giving you the confidence to hold the stock for the long run.

The company does not trade cheap and will likely shrink earnings next year. On my estimates, SiTime trades at ~24x 2023 and 28x FCF, which I expect to shrink compared to 2022. However, when the market rebounds, I believe that SiTime can easily grow 20%+ revenue and even higher FCF per share for a sustained period with reasonable MEMS penetration assumptions. In addition, the industry it’s disrupting seems to be responding in the classic “disrupted company” playbook, “the Innovator’s dilemma.”

This investment is not risk-free; I think it’s high risk. SiTime is a high-duration stock that is extremely out of favor as long-term discount rates rise. To mitigate that large concern, SiTime is FCF generative and has $25 dollars of net cash per share on the balance sheet, which should partially limit the downside to the equity. Meanwhile, there are no competitors on the near-term horizon; the company has taken and will continue to take market share in new markets like 5G, automotive, and military and aerospace applications.

Near-term problems are creating the massive YTD share drawdown of ~70%+, namely over-shipping products during a vicious global semiconductor inventory correction. This is what is creating the opportunity to own this long-term winner at a great price, with fabless gross margins (60%+), absolute price advantage over quartz (quartz companies operate at 30% gross margins), and an opportunity for this compound revenue and FCF meaningfully higher over the next decades. If you have the ability to have a multi-year investment horizon, this is a clear opportunity to own a near monopoly on a disruptor in a niche market.

Company Fundamentals

There are almost infinite ways to analyze a company, but the things I want to focus on in this write-up are 1) unit economics, 2) cash generation and balance sheet, 3) return on capital calculations, and 4) a segment overview of the business.

I believe that the company’s current financials show attributes of an immature company, but if you look closely, the incremental returns on capital, incremental gross margins, and ability to scale much further have a lot of promising characteristics.

Unit Economics

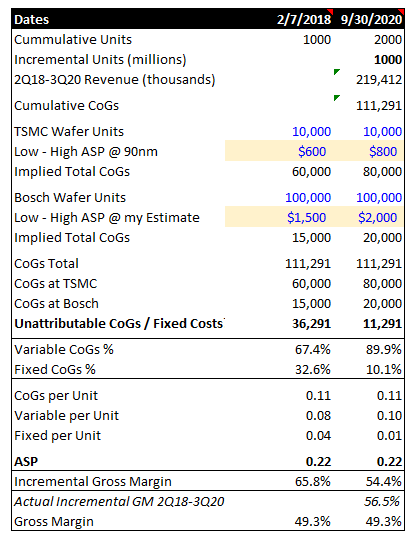

This is a tricky one that I will try to tackle with a range of units and ASPs to get a directionally correct answer. There are some important inputs here, first that they shipped 1 billion cumulative units in February of 2018 and 2 billion in 3Q 2020.

Next is that on earnings calls, they talked about how they get ~10,000 die per wafer at TSMC, use 90/45nm nodes, and get ~100,000 die per wafer at Bosch. The pricing at Bosch is unknown, but at TSMC, we can use a wide band of ~600-800 per wafer (remember, this is ~2018-2020 pricing). I use an estimate of $1500-2500 from this article.

This creates a unit calculation along the lines of this simple model.

So we can assume their incremental gross margins are around ~55-70%, and given the realized incremental gross margin for the company during this time period being ~56%, I feel pretty good about this estimate. In addition, SiTime said that fixed costs were ~10% of CoGs in Q4 2019, but given their recent capex, that number could be higher. The fixed cost estimate would lay within this range given above.

Astute readers will notice that the incremental gross margin is below their current gross margin, so how’s this possible? Well, it’s pretty simple - price. Below is the actual realized incremental gross margin of each quarter (change in gross profit/change in revenue). In the time frame of the original analysis where we have a unit estimate, the numbers align - but in 2021, incremental gross margins explode.

There are many potential reasons for this; total ASP went up, and SiTime has been selling higher ASP products.

2021 is when the entire timing market’s ASPs exploded (along with the rest of semiconductors), so part of this gross margin improvement is probably unsustainable. However, some part is likely SiTime moving to higher-end products, where a slight change in ASP and similar unit costs lead to much higher incremental gross margins.

Here’s a simple calc of what that would look like if we moved the ASP up 10 cents. SiTime has been entering the higher-end space of the market in the last few years, which includes TCXOs and VCXOs, where the ASPs are dollars, not cents.

So it’s hard to actually “know” what the incremental normalized gross margin will look like. If ASP increases from the timing market erode, the incremental gross margin number might look more like ~55-60%, but if they continue to grow at the higher end of the market (where they have a much smaller % of share), incremental margins on that part of the portfolio could easily be in the 85%+ gross margin level.

Cash Generation Ability and Balance Sheet

Something that is nice about SiTime is that we don’t have to debate the FCF profitability of the company. It’s a high-growth company with quite a bit of SBC, but the core free cash flow generation is not debatable, even excluding SBC.

If we include SBC, things get a bit more spotty. I still think that if we normalize that amount (these are my estimates), things will look alright. For me - I count SBC by increasing the share count in the future.

I think the cash generation of Net income to FCF will be at least ~70%, and their long-term net income guidance looks extremely achievable with 30% net income, implying a ~21% FCF margin. Given that they are already at their long-term net income margin and potentially higher gross margins in the future, a longer-term net income margin of 40%+ seems very possible if they penetrate the higher end of the market.

Lastly, I need to commend them on their capital raises. They raised ~$460 million from additional follow-ons in the market when the earnings multiple was in the triple digits. They also helped increase the float (Art Chadwick framed it this way - I like that) and lowered the Megachips stake. Today that cash raise is sitting on the balance sheet as ~$580 million in cash, and they are self-funding. I expect them to have ~$600 million by the year-end of 2022.

This is a war chest of a balance sheet and limits some of the downsides for equity in theory.

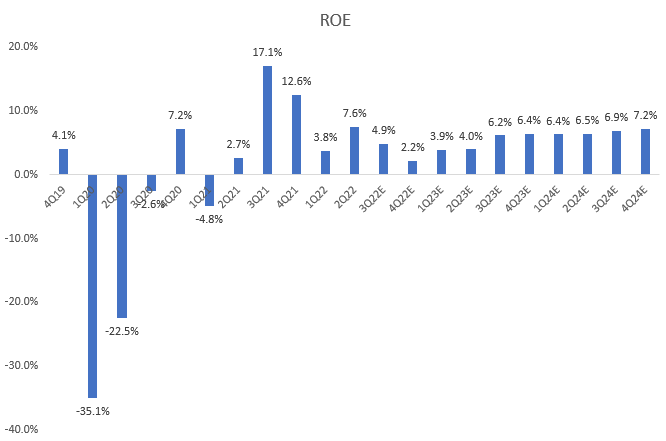

Return on Capital Calculation (ROE DuPont, ROIC, ROIIC)

I want to just do some quick sanity checks - how profitable are they on their equity? Because first glance does not look that great. Their incremental ROE is great, as their Net Income has gone from negative in 2018 to positive, but this doesn't look like a runaway profitable business. The problem is the cash drag.

Their ROIC tells a much different story. That is a metric that excludes cash. Notice that I expect their ROIC to correct downwards, but they should still have meaningfully profitable ROICs.

ROIIC - or Return on Incremental Invested Capital is a different and more interesting metric. It’s about to go massively negative as they are hit by a vicious inventory cycle, but I think the real normalized rate of ROIC they are making is incrementally in the high 50s+. That’s pretty good!

Regardless what I’m trying to get at here is that the capital they deploy in this business achieves high rates of return. They are spending ~$30-40 million in annual capex to grow the business compared to ~$30 million yearly in EBIT. I think that’s enough to show what kind of profitability metrics we have here on an incremental basis. Did I mention they are self-funded and have a war chest of capital? There’s very little financial distress here, and the company has plenty of optionalities given the cash pile and cash generation.

Segments and Businesses

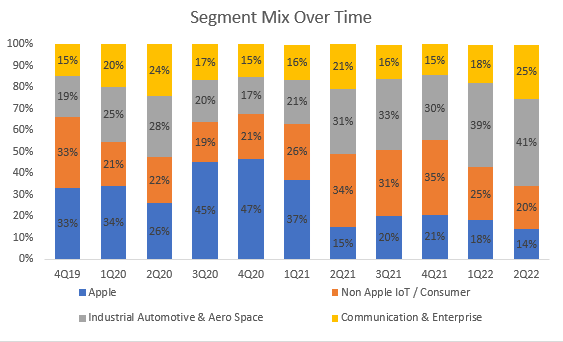

There are 3 major segments that the company calls out in the earnings calls. These are Consumer mobile and IoT, Communications and enterprise, industrial automotive, and Aerospace. I will further split the Consumer mobile and IoT business into Apple and non-Apple, as they are the largest customer of SiTime. Here’s the breakdown below.

Apple Segment (14% of Sales)

The first segment we have to talk about is their largest customer: Apple. Apple adopted MEMS timers early in SiTime’s history, which is an important part of its success. Apple is all in on MEMS except for the phone. Apple was using SiTime MEMS in the phone until consumers realized that they could brick an iPhone with some Helium.

This led to the design of SiTime MEMS oscillators in the iPhone, and a steep revenue contraction in 2018, with revenue growth rates of -40%. This was before SiTime was public, but they eventually had to fix this. I do not believe the MEMS timers were designed back into the iPhone, as Apple’s revenue recovered but not quite to previous levels. On SiTime’s website, they now mention that the latest generation of Epi-Seal is impervious to all gas.

These devices use MEMS resonators that are manufactured using the latest generation of EpiSeal™ technology which hermetically seals the resonator, making it impervious to all small-molecule gases

Regardless, this socket loss was big for the company, and it seems they would win back some of the business. Outside of the phone, Apple is essentially all-in on MEMS. Airpods, iWatch, and any other smart device use only MEMS and no quartz. Apple desires the customization factor of MEMS, but despite that business growing at a healthy clip, it’s starting to become a smaller part of the business. That’s a good thing, as it’s likely the kinds of timers in the Apple devices are 32.768 kHz time-of-day applications and thus a lower gross margin.

Apple, however, is likely one of the only “good” parts of the business this year, as they are expected to grow in 2023 over 2022, while the rest of their customers are ordering fewer products. Additionally, there’s a huge lever for additional upside here: Apple is designing its own in-house modem, and there’s a great chance that they are using MEMS. That could be a material upside to sales if that were to happen. Another ~240 million units of modems would be material for SiTime.

Non-Apple Consumer IoT Segment

This is the other time of day business, including sales to companies such as Garmin and other smartwatch and smartphone companies. This segment is a lower gross margin business than the other segments I will discuss. It’s an important segment and has a lot of torque to IoT device proliferation.

The reason why SiTime does so well in consumer IoT is twofold. First, their size lets them shrink their product to new form factors like Airpods. The second is that the performance, stability, energy efficiency, and size beat other time-of-day applications based on the quartz SKUs I have seen. There is a price premium here, but IoT device makers gladly pay for it.

This business is growing fast but is still shrinking as a percentage of the SiTime pie.

Communications and Enterprise

This is likely the highest gross margin part of the business. Reminders that the Cascade Clock ICs, Elite products, and Emerald are all targeting this business. Refer below to what that means in the competitive analysis portion.

It’s clear that the biggest opportunity in the very near term for SiTime is likely communications, where the ASPs and volume of 5G-related timing businesses are much higher than their traditional time-of-day products. Given that the 5G roll-out is ongoing, this makes a lot of sense to focus on in the near term. These gross margins are likely in the 80%+ range, and its recent growth has been massively gross margin accretive to SiTime.

Industrial, Automotive, and Aerospace

This segment, in my eyes, can be split into two meaningful verticals. First is automotive, where the timing opportunity is a function of more semiconductor content in cars, where the device count is going from 10s of timers in the low-end ICE vehicle to 60-70 timers. Automotive manufacturers seem to resonate with the vibration and reliability story of MEMS, and thus they are starting to see good traction there. Tesla is a notable adopter of MEMS and is all-in on MEMS timing devices. A very interesting topic is clock frequency, and the benefits of higher Q and different frequencies programmability can be further explored in this video about Tesla and their Dojo chip4. This is best represented in the Endura and Elite lines.

The second part of the business is the Aerospace angle, which I think is the most untouchable of the SiTime business. Their Endura line is enabling reliability in space devices we haven’t seen before, with timing products that can withstand 1000s of G’s of force reliably, and as long as the space industry continues to grow, they will massively benefit.

Rolling it all up, I think that the Apple business could grow high single digits, the consumer IoT business could grow 15%+, the communications business could grow 20%+, and the Aerospace and Automotive business could grow 20%+.

The important distinction is that the fastest growing businesses are higher frequency and thus higher margin businesses. That’s great for the defensibility of their gross margins in the longer term.

Timer Market Sizing

One of the other problems I have had difficulty understanding is how big the market is and what MEMS can and cannot penetrate. There are several ways to calculate this, but I’ll start with SiTime’s own expectations of the market. This is high, in my opinion.

The problem is that Oscillators and Resonators seem to be duplicative. Remember that a resonator goes into an oscillator and that often times oscillator companies themselves are just OEMs of another resonator and a piece of silicon circuitry. I believe, in this case, this is double counting. Another metric of how big the market is more reasonable from TXC.

The market for crystals and oscillators, I can comfortably say, is ~4 billion, while the market for clock generators is ~1-2 billion, depending on who you talk to. SiTime seems to push some aggressive growth assumptions in 2024 to reach their potential TAM, but I handicap them a bit. My guess is a bit below SiTime’s numbers (they tend to be promotional in all things), and my TAM base is 2021 at ~4 billion in oscillators and resonators (not double counting), 1.5 billion in clock ICs, leading to a 6.5 billion total TAM.

I expect a down 8% year in 2022 and a sharp rebound to up ~7.7% in 2023. An alternative TAM I trust a bit more is building from the Timing Market Calculation of TXC, which puts the market at ~4.4 billion in Oscillators and Resonators. I used a report from CS&A Associates to further split the market into high and low-end oscillators and resonators. I made some pretty simple market growth assumptions and then got to a TAM number that I believe is more reasonable. Let’s compare the sizing of these TAMs.

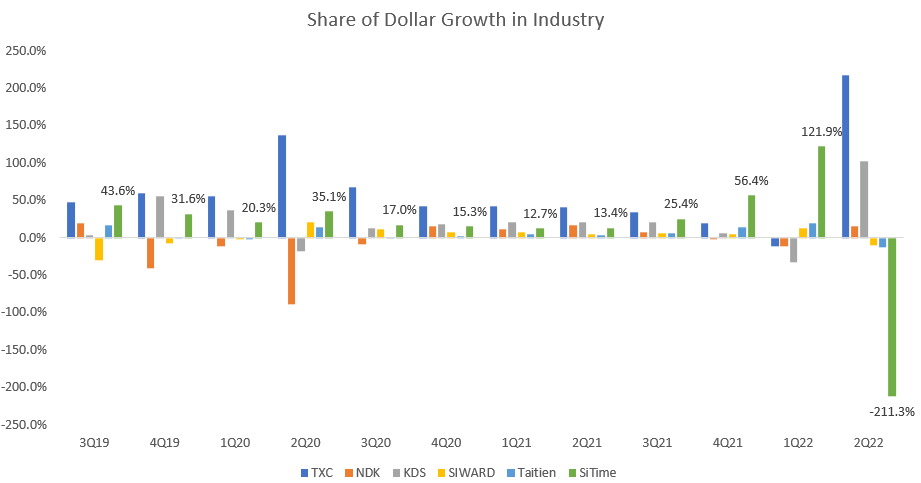

I have my base case as total MEMS penetration of the market at ~32% in 2040; this assumes about ~100 bps of share gain a year after 2024, below the massive share gains SiTime achieved in 2020 / 2021. That makes sense to me, given that the AKM fire was a pull forward in share gains. Another way to think about it is their share of dollar gains in the industry.

This puts them between ~30% share of dollar growth, this seems consistent with what they were doing before the Quartz fire crisis. Another way to think about this is that they are taking ~100 bps of share a year, consistent with what they were doing before the fire.

This is a comparison of quarterly absolute dollar growth from the largest pure-play listed companies, and SiTime has been growing its share of absolute dollars among the fastest ex-TXC, the largest company in the quartz timing space. The negative result in 2Q22 is because the timing industry shrank in that quarter while SiTime grew. This should partially unwind as the inventory destocking happens - but I believe this pace of share gains has been consistent with what SiTime has already been doing.

Lastly, I think Quartz's real implied assumption is that many sleepier players start to lose share. Some Japanese companies are exiting the low end, ceding share to SiTime. I think SiTime will continue to take the low-end share.

Below is a bit of a competitive analysis of how they plan to enter markets, focusing on lower and higher-end competitive strategies.

Competitive Analysis

In the last piece, I referenced the competitive dynamics pretty in-depth, but I wanted to do a bit more analysis in this piece. I will discuss product lines that are higher-end frequency, where they compete, and why.

Elite Product Line

SiTime’s Elite platform is a precision oscillator focused on synchronous communication networks and important networking and communication markets.

Elite, in particular, has DualMEMS, an interesting application of MEMS to make a product that Quartz couldn’t replicate, and an example of creative engineering using MEMS technology. The “Super-TCXO” uses 2 MEMS to create an extremely close feedback loop. The first MEMS resonator is the timing resonator, while the second acts like a temperature sensor used as a feedback mechanism for the temperature correction sensor.

The MEMS resonator dies can also be mounted on the package of a CMOS IC, which couples the resonator much closer to the actual source of temperature change rather than further away packaged on the PCB.

The net effect is a .05 PPM temperature stability with resistance to vibration, high operating temperature, and the programmability of 1MHz to 220 MHz. In particular, the goal of this product is designed for small cells, 5G front haul and backhaul, GNSS/GPS and is miniaturized for these applications.

This is their best TXCO product and comes at ASPs of $20-60. The rub here is that Quartz offers this level of accuracy and often at very comparable prices. The trade-offs between the products will likely go to SiTime if high ruggedization is desired, which might be desirable in the case of small cells. SiTime has a competitive product but is on the same playing field as quartz.

Emerald Product Line

Emerald is an OCXO product or an oven-controlled oscillator. SiTime boasts the smallest Stratum 3-level timer, a type of network reference clock5. Stratum is a network clock system that synchronizes clocks and is a network time protocol. At level 0 is the reference clock, which is often an atomic clock standalone from the network.

Stratum 1 connects to Stratum 0, providing time to Stratum 2, and so on and so forth. There’s a total of 15 levels of stratum synchronization levels possible, but the Emerald product only focuses on Stratum 3 / 3E. These are particular requirements for accuracy, and in the case of Stratum 3 products, this is +/- 5 ppb time. The package size is industry standard, and the product looks competitive but is not category-defining. It’s extremely niche and doesn’t address the entire Stratum stack, nor is there any inventory anywhere in the world. In particular, one of the benefits of MEMS OCXO timers is that they solve the cold start problem, whereas quartz has to warm up for stability.

I give the advantage clearly to quartz here. Stratum 3 products from SiTime compete on ruggedization and size, but that isn’t enough. SiTime has an opportunity to launch more Emerald products, but this is likely going to be a low-priority product in the near term, in my opinion. The ASP here is in the 100s of dollars as it’s a super high precision product. SiTime has a huge profit opportunity and is early in this market.

XCalibur Product Line

SiTime's XCalibur launch is new, this is a product launched in February of 20226. This is an active resonator, a relatively new product, and a small niche in the entire market. This is a $200 million dollar SAM compared to passive resonators, often connected to standalone MCUs. The goal here is likely a credible second source to quartz and a co-packagable design.

The “pitch” by SiTime here is that they don’t have the cold start problem (something that exists in OCXOs in particular), and it’s highly programmable. Additionally, it’s less susceptible to strong EMI fields because it's a mechanical process. The goal here is likely automotive and industrial applications, where qualifications are hard, and once an active resonator is qualified, it can be tuned for multiple applications instead of requalifying each quartz resonator.

This niche product targets a new emerging use case, particularly automotive. An active resonator doesn’t need another element to excite it, while passive resonators are more commodity-like and lower ASP. The ASP here is as low as ~80 cents and is a drop-in replacement for quartz resonators. There’s a real chance that quartz oscillator companies could start to adopt MEMS resonators and sell MEMS solutions (Abaracon is rumored to be doing this already), but that, at the time, is a bit far away. This is a niche new growth vector.

ApexMEMS

ApexMEMS is similar to the XCalibur product as it’s a stand-alone resonator. ApexMEMS is a passive resonator that can be sold to anyone who wants to create their own oscillator or timing product.

I’m going to call this a bit of a niche product, and similar to XCalibur, there’s a bit of an adoption curve here that the other OEMs will have to face. Will other quartz OEMs want to buy MEMS products to create their own oscillators to compete against SiTime? Abracon does in small part, but wide adoption seems far away.

Endura Product Line

Endura is one of the products I believe MEMS is 10x better than quartz, and quartz doesn’t have a good response product. Endura is a platform focused on Aerospace and defense, and in particular, can withstand 1000s of G’s of acceleration and 10s of Gs of vibration impact. The applications are obvious - defense and space.

When you’re launching rockets, trying to tell time on a satellite, or other mission-critical applications where failure is not an option, SiTime is the better product. Imagine fretting over a 50-100 dollar product in a multi-million dollar satellite that will eventually fail. The timer aspect is a small part of the BOM, yet a failed timer could ruin the entire missile or satellite. In my eyes, this is an absolute no-brainer product, and SiTime has a real advantage with MEMS that will continue.

This is a pure-play way to bet on the continued growth in space and partially in the defense industry. There’s no competitive threat from Quartz here, in my opinion, either. The problem is that this is still a very small part of the overall timer market, but one that SiTime will likely have the vast majority of share over time.

Cascade Product Line

SiTime launched Cascade in August 2020, and this is another networking and data center-focused product. In particular, this focuses on the Clock IC part of the market, a 1 billion dollar market SiTime that has had very little traction.

Cascade is a clock IC, so it’s one step past an oscillator where SiTime traditionally plays. Clock ICs if you remember, keep multiple frequencies as a reference, and SiTime’s product is just a clock IC with its MEMS inside it.

This product competes mostly through miniaturization. This is desirable in small form factor advanced packaging products. The product is in-line with phase noise offered by other companies, and SiTime is stepping up the stack to compete with some of the bigger companies like ADI, TXN, MCHP, and other analog timing companies.

The benefit that SiTime likely can offer that these companies cannot offer (except for Microchip) is full integration. Most competitors here are OEMs, meaning they buy oscillators or have silicon circuits (much noisier but cheap) to keep time. SiTime has a more integrated product and can compete here, but adoption is something that will take time. This is a market they just entered.

What is SiTime’s Competitive Strategy?

So most of the product categories I listed above seemed nascent, and that’s because it is. Clock ICs and Resonators are products that SiTime only entered in 2020, and it takes a meaningful amount of time for any kind of traction as a new competitor.

It’s clear they have also been gaining a meaningful amount of share in traditional oscillators, and I have tried to have a balanced view of MEMS product that the management team of SiTime doesn’t have - and that’s MEMS is a good product with tradeoffs that won’t perfectly replace quartz. SiTime, however, says, “we are 10x better, cheaper, smaller, more reliable, and have a lower mean time to failure,” I need you to take that with a grain of salt.

SiTime’s marketing has been very consistent, and it’s a borderline pysop to convince everyone that MEMS is better. I think reality, however, is a bit more nuanced. This has made understanding performance claims a bit tricky. SiTime, claiming MEMS is 10x better in every metric, has created a lot of haters in the quartz community with the apples-to-oranges comparisons. It’s hard to get a non-biased source, you’re either with MEMS or against it, yet SiTime is still gaining share. How and why?

I think this is where the programmability of MEMS comes into play. I will try to characterize how they compete in the two main parts of the market, low-end and higher-end precision products. Everything from this point forward is my conjecture of comparing different MEMS SKUs versus quartz-based SKUs. I’ve spent a 10s of hours trying to compare products at different frequencies, PPM accuracy, and price (which is illustrative when it’s from a distributor). Here are the broad-based conclusions I found.

I’m going to leave it here for the free section. I think I want to make sure everyone has a good understanding of the tradeoffs before I go a bit deeper into their strategy and the stock itself. If you’re interested in that and a full model, that’s all behind the paywall.