Ready for Takeoff: Macau Casinos, Travel Retail, and Widebody Planes

I'm launching a second substack. It's sector agnostic stock dives. More ideas, less industry coverage.

Housekeeping: I will launch a newsletter focused on general stocks called Mule’s Musings, a throwback to the original newsletter. I am excited to have a second platform to write about non-semiconductor stock ideas. You can see more posts like this on my second substack in the future.

You can subscribe here! There will be free and paid posts, but this is an outlet for all ideas, not-semiconductors.

It will be a much lower frequency posting platform, with a goal of ~1-2 posts a month that are paid: an idea and a follow-up. Additionally, I will write about business things I find interesting!

I think I have something to offer there. For example, in my last non-semiconductor post, Trend Watch #1, I listed COTY, IPAR, and THRN as ideas. THRN ended up being a bit of a bad one, but the ones I had way more money at risk, IPAR, and then eventually COTY, which I bought after I published, have done well.

The pricing will reflect the lower cadence, with a $50 monthly and a $300 annual. I will be religious about price raises. Every 50 subs will be a price raise. Since it’s a lower-frequency newsletter, I don’t want to encourage scalpers (subscribe for a month, read the ideas, and bail). Don’t worry; there will be a good amount of free content like Trend Watch and other random business adjacent analyses I am excited about. I look forward to writing more.

Anyways on to the newsletter. I have been itching to write about the reopening of China trade. Here’s a high level of some of the ideas I have in the space and what future newsletter content on the second substack will look like. This one is good, in my opinion.

Slight Update: I debated what to name the new substack for so long that I delayed this post. Everything still stands except for Rolls Royce's 20%+ price increase. The analysis still stands.

I have been a massive fan of the reopening trade. I don’t think I made it clear in the 2023 outlook piece, but by that point, I was convinced that the reopening in China was the highest conviction trade I could find, and its implications were clear to bet on.

In just a brief time since the market has validated the trade.

But it isn’t time to throw in the towel, as the fundamentals are just starting. I want to discuss the different ways to play the reopening, as I have a few ideas. This will be a shotgun release, and in no order, I will post some ideas I think are especially compelling.

Casinos in Macau (LVS, WYNN, MLCO)

I’m going to write the most about this

Widebodies in 2024 (RR.)

Duty-Free and Travel Retail Ideas (IPAR, EL)

Casinos in Macau

I think this is my preferred and favorite levered play to start. We even have a compelling case study: revenge betting after the United States reopening. The difference between the US and China is that China’s lockdown has been going on for longer, and the revenge spending will be much higher than the United States.

My favorite call this quarter has been LVS and LVMH, which confirmed that things are back to full capacity in Macau this Chinese New Year (CNY).

The problem we have right now is you can't get a seat in the games in our buildings. We're running 95%, 100% occupancy in those games. And the same applies to slot ETGs. The big question everyone's thinking about obviously is premium mass. - Robert Glen Goldstein, LVS CEO & Chairmen

If that's the case, in fact, it started in January. We have every reason to confident indeed optimistic on the Chinese market. In Macau, where the Chinese can now travel to the change is quite spectacular stores are full, it's really come back very strong pace. -Bernard Arnault, LVMH CEO & Chairmen

The problem is it’s hard to extrapolate, but I have a solid intuition that the Chinese reopening will be wild. For example, MGM said that the casino's strength lasted until February. I believe a full reopening is in order, and casinos in Macau are the first place we will see.

Our daily mass GGR was on par with the 2019 level for the month of January during Chinese New Year, far exceeded last year's Chinese New Year level, actually. And we are also encouraged to see that direct VIP segment in terms of rolling volume far exceeded 2019 level as well.

It is also very encouraging to see that January run rate extend into the first week of February so far. So all in all, we are very confident in a solid and sustainable recovery of Macau market this year and beyond.

- Zhi Qi Wang, MGM China Holdings Limited

The Chinese economy has been experiencing a period of inactivity, with investment serving as its primary driving force. At the same time, consumers in China have been given more freedom to make excessive spending decisions than they have had in quite some time. The Chinese government is not likely to be concerned with restricting luxury purchases, as they need any spending. In other words, gambling is on.

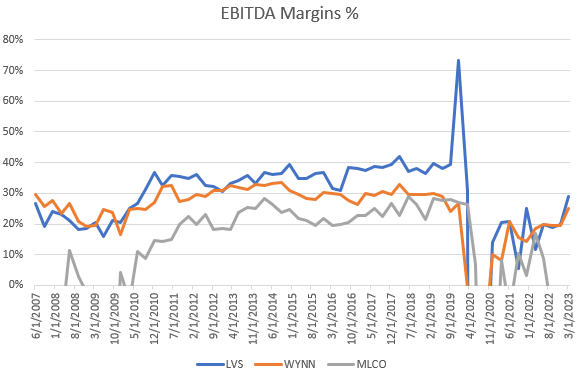

So What are the Casinos worth?

Let’s start with some assumptions. I fully believe that 2023 will be similar to 2019 levels of revenue for the casinos. The real question and the hard part of understanding is the margins.

First - the big overhang was that the Macau concessions would change their taxes on Casinos. The taxes stayed the same, which partially happened due to how horrible the current profitability of the companies was at the time.

Interestingly, the new concessions have a variable rate schedule, with the lowest rate seen in 2023. In 2021, LVS paid ~22 million a year for raw concession payments; in 2023, they will be paying ~12 million. This is a literal rounding error for LVS and other operators.

Still, amid the lean operations, slight tailwinds like lower tax concessions for foreigners and the shift from junkets (super high-end) to casino-sponsored VIP and premium mass could be huge tailwinds to the companies in the short term. Put differently; it seems that Macau should be able to see high cycle margins amidst revenue recovery to 2019 levels.

Revenue, however, has quite a long way to go.

I think the easiest way to try to value these things is by looking at previous cycle revenue highs and previous EBITDA margins ~28-38% and seeing where that nets you a price ~20% higher than today. That’s assuming a full reopening.

Where that gets you is an “easy” higher price of ~20% for both LVS and WYNN, and MLCO looks like it’s outrunning itself a bit.

But here’s the thing. Gaming came back huge in the US after the pandemic, and I think it will also come back for Macau. Marina Bay Sands (Singapore) has already hit a record high compared to 2019. That is an easy comp for what things should look like on the other side.

And what’s more, the revenue high is being done on lower visitation. When all is said and done, and visitation recovers to 2019 levels, revenue in Macau will be 20-30% higher. Additionally, while tables and slots are limited, more hotel rooms have been added to the properties in Macau since 2019.

In my opinion, we will likely see ~120% of 2019 levels for 2024. Adjusting for that, I believe shares could be much higher. Let’s assume 120% of 2019 levels and 100 bps higher EBITDA margins (buddy, that’s called conservatism) accounting for operating leverage.

That can underwrite ~50%+ higher valuations from here. I think that’s very attractive and, frankly, more likely than the base case of just pre-2019 normalization. I believe visitation should follow the trend that Marina Bay Sands is setting in Singapore and that by the end of the year, we should see new highs in Casino revenue and profitability in Macau. The shares look underpriced by at least 20-30% from here, especially LVS and WYNN.

Additionally, if you want to take way more risk, you can step into the local listings in Hong Kong. MGM China (2282:HK) is the best positioned from that perspective, as they took a meaningful share from the new allocations of gaming tables and slot machines.

Besides the fundamentals, I am mostly worried about the positioning and when to “quit” the trade. We have a deluge of good information, but the shares have already ripped. My “sell” decision starts whenever MTUM includes LVS and WYNN, which is not the case today. I’ll reassess the trade then.

Bus drivers to CEOs have been cooped up at home for years. It’s China’s huge reopening, and I think Casinos will be the place to be in the huge rush. There will be comparability issues in the future, but estimates haven’t even begun to move. This is a tremendous tactical trade.

Widebody, China, and Rolls Royce

Brief Update: This was written before the earnings post, and uhm, it went up almost 30% since! I still believe this company has incredible torque and is worth watching.

As someone who follows an industry with kinks in the supply additions and demand (semiconductors), one of the more exciting dynamics is that international widebodies have been shuttered over the last few years. One of the big reasons for this is China, which is now waking up with a vengeance. This could lead to a lagged supply curve, as supply is forced to catch up to demand over multiple years.

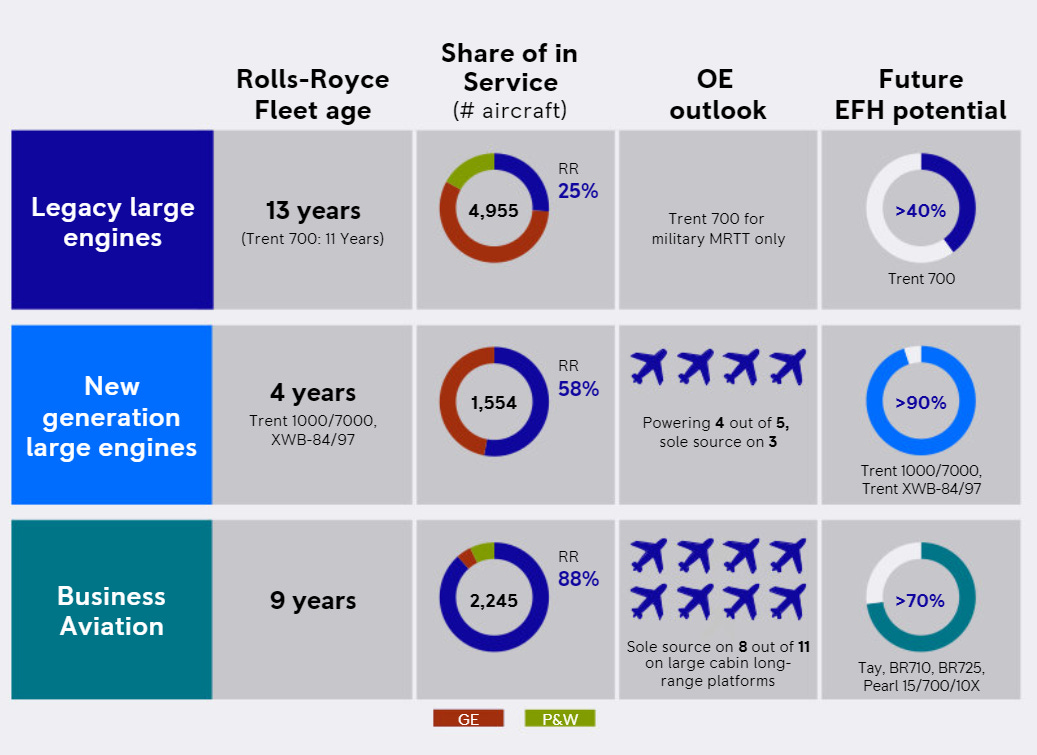

I have some ideas, but the one with the most torque is disgusting. Today I want to focus on the most exposed and worst-managed company of the lot; Rolls Royce.

But before I describe the opportunity, I have to give a context of this company. I remember the incorrect argument about afterbody sales at Rolls Royce in the 2017-2018 timeframe was that Rolls Royce would sell engines at a loss but recoup the upfront loss leader of the engine through aftermarket sales and service. It was even profiled in the book “Quality Investing.”

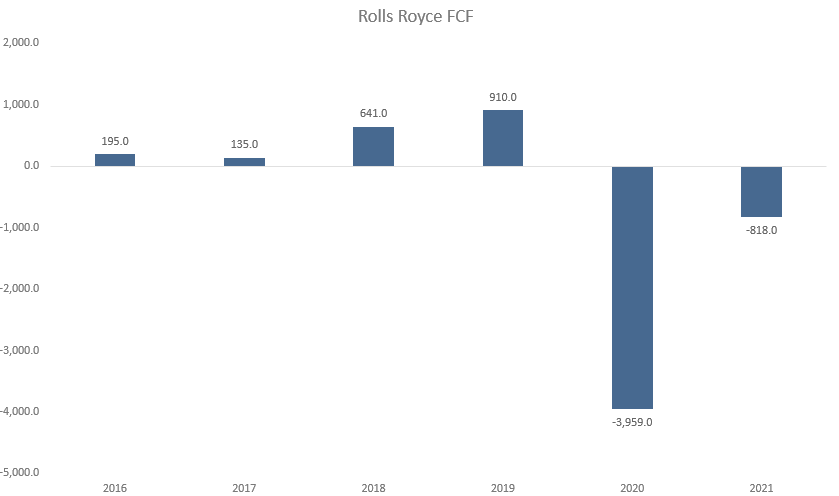

There was this legendary £1.2 billion in FCF by 2020 guide, which never came to fruition. This is from the 2018 Analyst day.

As you know, we have not given guidance on 2019. Our market consensus is just north of £700 million or so, I think. You know that we have guided to £450 million free cash flow for this year and are on a track to now go beyond the £1.2 billion in 2020

They got close to that number, and then COVID hit. Now Rolls Royce is losing almost a billion a year. However, I think a fresh look is warranted.

The reality is that right as FCF was supposed to inflect, a global pandemic lowered travel hit. The worst part is international travel, where Rolls Royce was best positioned, got hit the hardest.

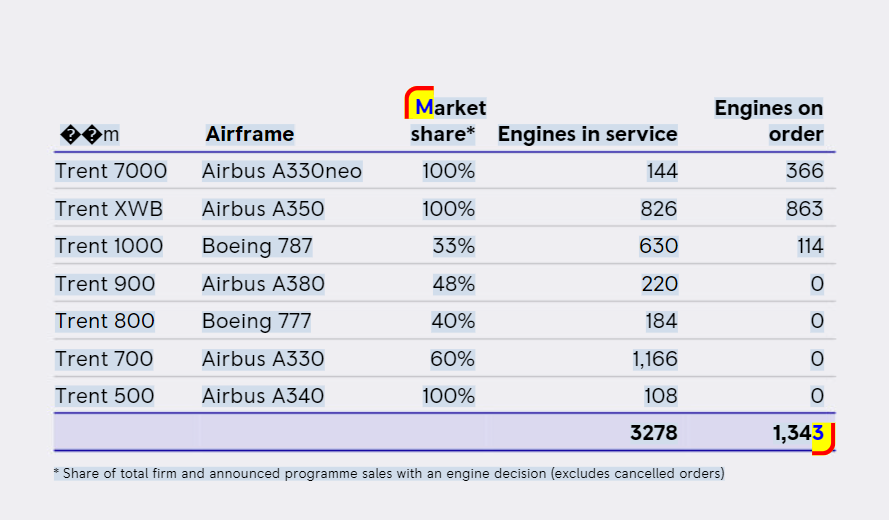

In particular, they dominate widebody planes, and their fleet of engines is lower than average and skewed to international widebody travel. Well, what hurts for Rolls is that widebody travel didn’t happen for 2020-2021, and their engines are getting less used than expected. This is the worst case possible.

Shares have reflected how bad it’s been for Rolls in particular. And the company was in the midst of a turnaround. And amidst that issue, there is now yet another CEO. It’s been one of the most depressing and frustrating journeys for Rolls Royce of any public stock. Here’s a comparison to the other engine maker, Safran, to show how bombed-out Rolls is.

But if you squint, you can see the green shoots. Widebody is beaten down and is already starting to recover slightly. Here’s a graph of the percentage of 2019 flights from China.

I cannot express how much torque the Chinese reopening Rolls Royce has. They massively over-index China, and China has been a dead market for years. They are the clearest direct benefactor from an aero OEM perspective.

For this note’s focus on direct Chinese reopening plays, I think it’s clear that Rolls Royce has the worst financials, the most leverage, and the most torque for the Chinese reopening. But it’s also been among the worst-managed and the most painful stocks to own. Could it be different this time? Who knows.

Here’s a simple estimate of what they could earn based on a percentage of 2019 travel. Each 1%, according to management, is an incremental 30 million in FCF.

If we see 100% of 2019 levels in 2024, that is an 11x FCF multiple. That’s relatively cheap against Safran’s ~30x earnings.

Update: It’s more like 18x forward FCF on a ~800 million guide they gave, but I still believe that is conservative. Shares are still priced well! Compare that to Safran, which is 30x+ earnings. The run rate FCF could easily be north of 1 billion this year, in my opinion, making it still cheap! I believe the EV calculation didn’t change much, given cash didn’t burn!

Duty-Free Cosmetics

I mentioned briefly that duty-free is a great idea, and I have a few thoughts. First, there are the companies like DUFRY, which, literally as the name says, operates duty-free stores in airports. But I think there is a more nuanced idea set here.

LVMH, for example, has a meaningful Duty Free business, Estee Lauder historically over-indexed physical retail in China, and IPAR’s duty-free business used to be 15% of sales compared to 8% today. All of these ideas have reopening torque.

Duty-Free was once the fastest-growing channel before COVID, and was the place to be given the over-index of Chinese consumers. Now that trade is alive and well, and it’s time to review the duty-free channels that are most exposed.

The thought here is some of these businesses are secularly advantaged (skincare, fragrance) and have grown despite meaningful parts of their businesses being closed for years. Estee Lauder and Interparfum are two businesses I am most familiar with. I’ll start with IPAR since I mentioned them in my trends report.

Perfume, in particular, has always been a heavier retail segment. That makes sense since it’s hard to smell scents over the internet. But given that fragrances are having their moment despite global travel closures, I think this is a case of an advantaged business getting another tailwind at its back.

Take the case of IPAR; in 2019, its travel retail business accounted for 15% of revenue, and now it accounts for 8%. Total IPAR has grown 30% since It’s grown 50% since 2019, yet the travel retail business is still below. Since 2019, yet the entire travel retail business has shrunk in absolute terms.

Assuming that the retail travel channel returns to 2019 terms in absolute dollars, that’s another 2% tailwind in revenue. Assuming travel retail gets back to 15% in total revenue and it is genuinely incremental, that’s a 7% tailwind to revenue. Shares are expensive, but I like the strong companies with a distribution thesis for IPAR. Given that consensus estimates are +7% for 2023 revenue growth, this seems like a meaningful tailwind if estimates are too low.

IPAR trades at 30x ‘23 earnings, which is a bit rich. But i think revenue will come in meaningfully above consensus (say 10% versus 7%) and then EBIT should be meaningfully more incremental (say 15% eps versus 5% growth). That’s still an expensive 28x earnings, but I still strongly believe in fragrance stocks.

Now I want to talk about Estee Lauder, which has done surprisingly poorly in 2022. Estee Lauder is having some problems with its core brands, and despite growing much faster than competitors for years, given its skincare exposure, it hasn’t kept pace with larger peers like L’Oreal this year. I think this is an opportunity.

If I had to guess, part of the reason for this divergence is the retail travel segment. I read Estee, A Success Story, and one of the big standouts is that Estee Lauder was and always will be very levered to department store sales. It’s how Estee Lauder got her literal start and is a deep part of the company’s DNA.

Before the Pandemic, Estee Lauder’s sales were 26% of sales. Their largest customer for example, primarily sells products in China travel retail, accounting for 13% of sales in 2022. That’s quite a lever towards Chinese travel.

I have a more challenging time calculating what kind of torque EL has towards China retail traveling, but it’s material. Estee Lauder has a meaningful Chinese exposure that has been a headwind on sales for years. The multiple has gotten more expensive, but I think Estee looks the best positioned relative to peers, given their 25%+ travel retail exposure.

Buying L’Oreal could also be the answer, as they seem to always benefit from every trend and have a meaningful travel retail business. That could be an example of a strong business getting stronger with the addition of travel retail as a tailwind.

Parting Words

A few other beneficiaries are Luxury stocks and energy. Luxury companies simplistically should be bought on a percentage exposure to China, which include Swatch, Hermes, Burberry, Moncler, and Tods in that order.

On the energy front, I can’t pretend to have special insight into the supply and demand relationship there. I think energy will benefit, but I lack special insight.

Final note: I got mentioned to me that the EWQ (MSCI France) is a reopening ETF. Top holdings include LVMH, Kering, Safran, Airbus, L’Oreal, and hell; even Dufry is listed in France. A rough approximation of “reopening beta” as a percentage of ETF is 37-40% of the ETF is exposed directly to reopening themes.

That’s pretty good for an ETF! The exciting thing about the ETF is that while it is massively illiquid and hard to get calls (literally, I tried to get these), the IVOL is insanely low. If you can get it filled, this is a good beta. Or if you’re just a poor professional investor that cannot own individual stocks in their PA, EWQ is an exciting tool for the Chinese reopening.

I hope you found this post interesting. I want to write more about non-semiconductors, and I hope this is the right platform to do it. More information about what that will look like in the coming weeks - but I’m excited about this new chapter. I will still cover semiconductors, but I like ideas that make you money. And frankly, I have them less often than I’d like in semiconductors.

I understand Rolls Royce has had years and years of disappointing results even before COVID. Challenging operational issues. Yes there's a new CEO (again) but how can one be somewhat more confident that those issues are behind them?

Kicking myself for missing IPAR after you wrote it. Really like the EL & EWQ idea