Semiconductor Outlook 2024: AI's Adolescence

Its time to jog your memory. We've gone through the downturn, what does an upturn look like?

The year 2023 began with a significant downturn in the semiconductor market. Significant capacity additions were brought on after the historic shortages due to COVID-19, and then demand wobbled as interest rates quickly rose. Supply outpaced demand, and the market turned into a period of oversupply. That was mostly the story of the semiconductor market when I wrote about it last year.

Despite this, semiconductor stocks made a new high this year, even surpassing the previous high from 2022, as shares rallied in anticipation of a better market.

As of December 2023, we can see positive signs of the market's recovery. TSMC's monthly revenue is improving, as well as South Korea's semiconductor exports.

That isn't the big story for this year. The real story is the emergence of a completely new market segment that could be as significant as the data center or smartphone market. This is AI’s moment; 2024 will be its first year of adolescence.

AI’s Adolescence: Growth Spurts and Growing Pains

Let's analyze the significance of AI in the semiconductor market. According to the latest estimate provided by WSTS, the semiconductor market is expected to reach around 520 billion by 2023. To give you an idea, Nvidia's data center revenue for this year is anticipated to be around 46 billion. Assuming that most of it is AI-related, that accounts for roughly 9% of the market.

The AI market is expected to reach the size of the entire networking or automotive market in just one year. Although it will be categorized under the data center market, viewing this as a new market altogether is better. Historically, the data center market has consisted of a CPU-heavy cloud services market, while AI is focused on inference and training accelerators.

I anticipate the growth in AI will continue at least through the first half of this year. If we add AMD’s few incremental billion in accelerator revenue to Nvidia’s $90+ billion, the AI market should reach $100 billion annualized in revenue at some point during 2024. The debate is whether it will stay that large, but regardless, it’s a substantial portion of the entire market.

I strongly believe that the AI training and inference segments will become the largest semiconductor market in the world in the next few years. The PC and Smartphone market are each worth around $120-140 billion, and AI will be a stone’s throw away from that next year. Even with a possible correction, the AI market is in its early stages and here to stay. Hence, I’m calling 2024 the year of AI’s adolescence. It’s not a small market anymore, yet it still has immense growth potential.

But amid the growth spurts, I think there will also be growing pains. Most market participants know that comparable market growth becomes extremely hard starting in Nvidia’s fiscal second quarter. hey might be able to achieve growth until the fourth quarter, but the results will not be as impressive on a year-over-year basis. The concern is that the rate of growth of AI training implies that the entirety of the hyperscaler's capex budgets will be AI, in order for further upside.

The question of how secular AI training is will come into question this year. ChatGPT-like services are experiencing an increase in usage and users, similar to the iPhone moment. However, Nvidia and AMD are selling capital goods to service this secular market, and there's a possibility of overbuilding capital goods. As an example, TSMC was the primary supplier to Apple during the iPhone era and didn’t fill their fabs every year.

Nvidia is not standing still and will continue to offer new products. Namely, the upcoming B100, which will help increase the supply of compute for AI meaningfully. However Nvidia the stock is now climbing one of the highest walls of worry ever. The market is concerned about its competitive positioning, peaking revenue, and many other hard-to-solve debates. There will be growing pains.

Semiconductor markets always have moments of oversupply, and the AI market will be no different. No one knows if it’s this year or next, but investors should remind themselves to stay positive as this is an amazing secular market in the longer term.

Two years into the formation of AI, it’s already approaching the size of Smartphones and PCs. It will surpass these markets, and for all we know 2024 could be that year. Big generational shifts are hard to predict with that much precision. When the tide is large and unrelenting, it’s hard to guess how the eddies will flow.

I think some required reading on this topic is my Telecom Bubble piece, as that’s our best analogy to the AI market today. In my opinion, the big unknown is how rate cuts could spur another round of growth for the AI industry. Read more below.

The negative impact of AI on society might be acutely highlighted during the upcoming election cycle. AI has moved much faster than social media, and I wouldn’t be surprised to see a Cambridge Analytica-style scandal involving the use of generative AI.

This could become a big point of contention in the election year, and even if regulation is slower than the industry, this could be a huge headline risk. And while this may seem quaint today, it’s very common for multiples to contract in fear of impending regulation. Growing pains are ahead. Given the amount of spending, usage, and importance involved, it is unlikely that this will be a smooth ride. The upcoming election year could accentuate this issue.

Let's shift our attention to the memory market, which I think will have an interesting 2024.

Jogging Your Memory

I'd like to remind everyone about the memory market, which seems to have been largely ignored since the memory downturn. It’s hard to pay attention to a painful market, and this cycle has been historic. This cycle appears to be one of the most difficult and lengthy ones since 2000.

The memory market is capital-intensive and volatile, and I understand why that keeps many investors away. But many shares of memory makers are out of their previous lows and are approaching peaks. That can be a confusing story as the market recovery doesn’t seem strong enough to justify this rally.

But the memory market moves fast. And there is a lot of warranted optimism about memory companies as DRAM and NAND prices have bottomed. NAND prices in particular are skyrocketing and are on pace to return to 2022 prices.

This is not a trivial part of the market. The entire market is in the 10s of billions, and next year, we should expect 40%+ price increases and 15-20% volume growth. That’s quite the comparable year. Now, this doesn’t mean I think memory companies are well positioned; in fact, this publication’s take is that, more often than not, the memory companies are heartbreaks waiting to happen. Semicap is usually a better bet.

There’s a new market emerging that I would like to draw your attention to. If we consider 2023 as the year of AI’s inception and 2024 as the year of its adolescence, then I believe that a new memory market is also starting to take shape in 2024. That market over time could become one of the largest categories of memory, and it’s called HBM.

HBM stands for High Bandwidth Memory and is a critical bottleneck for training and inference. It’s usually packaged near logic and is the key defining trait for every accelerator today. The memory bandwidth on the chip is more important than the FLOPs of an AI accelerator. The memory wall is a significant issue, and HBM is a crucial solution to this problem. HBM capacity and speed are more critical than even CoWoS capacity today, and access to the top bins of HBM is the critical factor that makes or breaks an AI accelerator.

The clear leader in market share and quality of HBM has been SK Hynix. The company announced that their entire year’s supply of HBM has been sold out. Today it’s a small part of the bill of materials (BOM) for an accelerator, but it can still become 20%+ of the memory market. HBM is that important, and I think that regardless of who is shipping the best logic, all companies will be scrambling for the best HBM.

HBM will be a secular growth market, and even if AI demand has a temporary slowdown, the demand for HBM will be insatiable. This trend is likely to result in a highly profitable market in 2024.

It’s expected that DRAM memory, excluding HBM, will perform well this year and NAND memory is quickly recovering from one of the worst markets in memory. There are already signs of improvement in memory capacity spending, which has been one of the worst segments in the entire market. Next year is looking to be much better than this year.

I’m surprised there is any doubt about this right now. And as the year goes on, memory markets and spending will shift to a much more constructive tone. Historic underutilization should lead to an above-average year on the other side. And in conjunction with the emergence of HBM, I think that memory has a chance to be one of the big stories of 2024. And I just wanted to jog your memory before it happens.

Chips and Sovereignty: The Same as It Always Was

This year in Chinese-US tensions within Semiconductors felt the same as it ever was. China surprised the US with its capabilities (Kirin 9000S, YMTC, CXMT, WFE Spending), and the United States enacted another wave of export restrictions. You could argue that the 2020 Huawei restrictions and the 2022 October restrictions were very similar.

The US and China's efforts to control their respective supply chains are a story of hegemonies. To control their fate, they must control their own chips.

Semiconductors continue to prove how important they are on the global stage. They are the lifeblood of every digital economy and each nation. Controlling the flow of semiconductors is a huge power source, so we should expect the China and US tensions to continue. Being the best at semiconductors will matter as long as we continue to live digital lives.

The Chip sovereignty story will take decades to play out, and I expect it to continue next year, especially during an election year in the United States. I would expect the beginning of the year to be relatively tame and ramp up in headlines into the end of the year. It’s not going away, but it’s the same as ever in some ways.

The best place to keep updated on China is Jordan Schneider’s ChinaTalk.

Something to consider, however, China is that China is on its knees as an economy1. Trade ties might be more important than in the past, so cooperation is coming from a place of weakness. However, for those who closely monitor China, it's clear that Taiwan is not just about semiconductors. The United States will remain anxious about this crucial island, and that anxiety is unlikely to dissipate anytime soon.

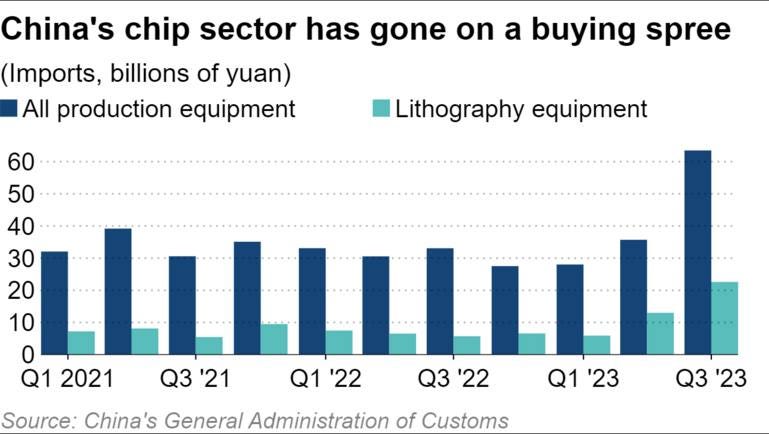

But if you look a little closer the new AI October restrictions seem like a liberalization of the semicap restrictions and a tightening of the AI restrictions. As a result, China’s historic splurge on semiconductor fab equipment has become one of the year’s major stories.

Another way to look at their spending is through the big five semicap companies. As of Q3, over 40% of all spending was from China, suggesting that for this brief moment, China is the biggest spender of semiconductor equipment tools in the world. I don’t believe that level is sustainable, but their spending will be higher than in history, leading to a significant increase in WFE spending overall.

China’s spending helped rescue what was expected to be a bad year for wafer fab equipment. Gartner forecasts that total WFE will only decline at high single digits, mostly because of this Chinese equipment splurge.

Next year, the baton will be passed to Memory, leading-edge logic, and the West. But I wouldn’t be surprised to see it much higher than historical levels. China remains critically reliant on the US to make their own semiconductors and will play nice to get what they want. The tension between the US and China will continue.

Let’s now shift our focus to stocks and the economy after discussing the big stories of the semiconductor market this year.

Overview of Stock Markets and the Economy

Stocks soared this year. Despite an uncertain broader macroeconomic environment2, inflation has slightly abated and the expected hard landing never happened. Rate increases that had a negative impact on the stock market last year are now expected to be offset by multiple rate cuts in the coming year. As a result, the level of uncertainty in the economy is decreasing.

This graph from Joseph Politano’s Apricitas’s yearly outlook tells it all.

Stocks like certainty. This year has been great for stocks because of that reason. The Nasdaq has had an especially strong performance, thanks to the Magnificent 7 - the big tech-based mega caps. These companies have been responsible for driving most of the market’s return this year.

One of the magnificent seven is Nvidia, which was the best-performing of the group and the semiconductor universe this year with an eye-watering ~240% return.

Although Nvidia accounted for ~35% of the semiconductor universe’s returns, it was not the only company that saw gains this year. On average semiconductor companies did better than the broad market. The distribution of returns for semiconductors and semicap this year is more positively skewed than in previous years.

Another way to look at annual returns is to add some context from last year. This is a two-year return graph, with the X-Axis being last year’s returns, and the Y-Axis this year’s returns.

Only two companies had positive returns in both years, Axcelis and Rambus. Rambus is a long-time favorite in the newsletter, so it’s nice to see them do so well.

Let’s take a look at the EV/EBITDA for the next twelve months. I used EBITDA to account for capital structures. Some companies like SiTime are expensive, while others like AMBA, SLAB, and WOLF are outright unprofitable. It’s a tough market in some corners of the semiconductor market still.

This year, I am introducing a new graph that compares the EV/EBITDA of a particular group of companies over a two-year period. On the graph, the X-axis represents the previous year, while the Y-axis shows the current year’s forward EV/EBITDA multiple. If a company is below the Y=X line, then its valuation has decreased, whereas if it is above the line, its valuation has increased.

This graphic depicts industry-wide multiple expansions or contractions. The companies with the biggest valuation increases were AMD, Nordic, BESI, MPWR, and the others clustered around them.

There are very few multiple contractions this year, with only Nvidia, MU, ALGM, and LSCC getting cheaper. Nvidia is one of the few companies that managed to outgrow their share price, with their fundamental results even stronger than price appreciation. That’s rare.

Valuation doesn’t account for the whole story. Companies may appear more expensive in the short term before their results accelerate, and the market often considers that.

Within my paid section, I provide a detailed analysis of each subsector and highlight a few individual companies. If you want to learn more about semiconductors, I would greatly appreciate your support. If not I wish you a fantastic 2024! Thank you for reading and please consider sharing this article.