TSMC Sees Continued Weakness, and EUV's Quandary (ASML)

TSMC sees further inventory correction, I see earnings disappointments. ASML has a quandary if the entire ecosystem is trying to use EUV.

Hello free subscribers! This is my customary earnings post about TSMC; if you enjoyed it, consider subscribing for coverage of most of the semiconductor universe, or better yet, share it if you found it helpful! On to the post.

TSMC Reports Earnings

TSMC reported earnings. They beat Q2 estimates, but importantly they guided down Q3 and FY 2023 estimates. The Q2 beat was widely expected regarding revenue, given that TSMC reports monthly revenue, but the Q3 guide was not. Here’s a quick summary of estimates versus actuals.

Revenue NT$480.84B ($15.68B) vs FactSet NT$479.22B

Gross margin 54.1% vs. FactSet 53.3% and prior guidance 52-54%

Taiwan Semiconductor guides Q3 revenue $16.7-17.5B vs FactSet's $17.41B

FY23 revenue (10%) y/y vs prior guidance low to mid-single digit % in US$

The midpoint of the guidance has the year-over-year decline decelerating, which I didn’t expect. Moreover, the -10% annual guide throws some water on the second-half recovery. Yes, the second half will be higher than the first, but the recovery is much more muted than historical. And what’s more, margins are looking worse for N3 than a typical node.

TSMC said that next quarter's gross margin will be ~52.5%, with N3 offsetting those margins by 200-300 bps. In Q4, it will be worse with a margin headwind of 300-400 bps.

We have just guided our third quarter gross margin to decline by 1.6 percentage point to 52.5% at the midpoint. Primarily as a higher level of capacity utilization rate, it is offset by 2 percentage points to 3 percentage points margin dilution from the initial ramp up of our 3 nanometer technology.

Looking ahead to the fourth quarter, we expect to continue a steep ramp up of our 3 nanometer to dilute our fourth quarter gross margin by about 3 percentage points to 4 percentage points. In 2023, our gross margin faces challenges from lower capacity utilization due to semiconductor cyclicality.

Semiconductor nodes are becoming harder to ramp. Unlike most new node ramps, N3 will not reach the corporate average in 7-8 quarters.

it's becoming more challenging for the leading nodes because of the process complexity increases a lot. It applies to N3. So it will be challenging for N3. We actually mentioned that at the beginning of last year already, it will be challenging that for N3 to reach the corporate leverage in the -- in 7 to 8 quarters time frame like before, yes. But however, part of it is really because of the higher corporate margin that we currently have.

TSMC blames the higher corporate gross margin, which is a good point. Gross margins have expanded meaningfully; even in this downturn, they exceed previous cycle highs.

But another alternate explanation is that TSMC 3nm is rumored to have bad yields, and the struggle to ramp those yields is putting meaningful pressure on margins. It’s widely rumored that Apple is not paying wafer but known-good-die pricing. That’s probably a headwind on gross margins as well.

Despite the fact that Apple is rumored to have secured 90 percent of TSMC’s 3nm chipsets for the A17 Bionic and M3, the yield rate still has a long way to go up from that 55 percent figure. Due to wafer production not delivering the best output, TSMC is said to be charging Apple for its good dies rather than standard wafer prices.

Speaking of Apple, let’s talk about the mix of revenue by end market this quarter because this has many interesting implications.

This is an interesting chart because we know a few things. HPC is down 5% QoQ, despite knowing that Nvidia is up 60% QoQ. Sure, there’s pricing in that, but it implies that everyone else in the HPC segment (AMD and AVGO) is doing horribly. Moreover, TSMC thinks CPUs will be cannibalized in the short term. This does not bode well for everyone selling products into the data center that isn’t Nvidia.

But in general, I think the -- trend of a big portion of data center processor will be AI processor is a sure thing. And will it cannibalize the data center processors? In the short term, when the CapEx of the cloud service providers are fixed, yes, it will. It is. But as for the long term, when their data service -- when the cloud services having the generative AI service revenue, I think they will increase the CapEx. That should be consistent with the long-term AI processor demand. And I mean the CapEx will increase because of the generative AI services. Anything more for you?

AI is still such a smaller part of the overall semiconductor industry. TSMC has it at 6% of revenue, growing at a 50% CAGR. That probably doesn’t include meaningful price increases, so that’s mostly driven by volume alone.

Today, server AI processor demand, which we define as CPUs, GPUs and AI accelerators that are performing training and inference functions accounts for approximately 6% of TSMC's total revenue. We forecasted this to grow at close to 50% CAGR in the next 5 years and increase to low teens percent of our revenue.

What is also interesting is that we look at DCE. What could be driving that revenue increase? If you look at the TSMC Annual report, the report includes TV, Voice AI control, and WiFi products in this segment. I think this is Apple’s VisionPro finally showing up in the value chain in a big way. Now notice that DCE is the smallest part of TSMC’s revenue, but it’s cool to see VisionPro in the wild.

Last, I want to call out Automotive briefly. Last quarter I called out the Automotive weakness, and fast forward a quarter, and we are still seeing quarter-on-quarter growth. That quickly became a consensus quick-twitch trade, and I think automotive looks like it will be the only area that isn’t about to disappoint the hell out of investors this quarter.

In the last quarterly conference, we said we expect fabless semiconductor inventory to rebalance to a healthier level exiting the third quarter. This statement continues to hold true. However, due to persistent weaker overall macroeconomic conditions, slower than expected demand recovery in China, and overall softer end market demand conditions, customers are more cautious and intend to further control their inventory into 4Q '23. Thus while we maintain our forecast for the 2023 semiconductor market, excluding memory, to decline mid-single digit year-over-year, we now expect the foundry industry to decline mid-teens and our full year 2023 revenue to decline around 10% in U.S. dollar term.

Part of this is China’s recovery is not taking off at all. The hope for the reopening has now led to fear. China’s economy seems bleak without much recovery in the future. And what’s more, is that Nvidia is one of the top customers at TSMC now, and knowing that they are growing meaningfully while all the other customers are not, implies that the average semiconductor company must be doing worse than mid-teens YoY revenue.

I cannot help but look at the entire semiconductor space and see disappointing prints. Revenue should be similar, but the fact that inventory cuts make me think that the market will be disappointed and unwilling to buy the third cut.

Let’s move on to semicap. Something I didn’t expect is that TSMC is cutting their capex guide to the low end. That’s bad for logic, which is supposed to be the perkiest part of wafer fab equipment spending.

We now expect our 2023 capital budget to be towards the lower end of our range of between $32 billion and $36 billion US dollars. Our depreciation expense is now expected to increase by mid-twenties percent We now expect our 2023 capital budget to be towards the lower end of our range of between $32 billion and $36 billion.

Part of that is fab pushouts, but part is that they think capex is normalizing. They had this period where Capex went from $10 billion a year to $30 billion, and in the future, this trend should moderate. If it cannot, this likely creates an unsustainable basis for their customers.

Randy, the push out of fabs does push out some part of the CapEx, but that doesn't affect a big part. For 2024, it's too early to talk about the overall CapEx. However, our CapEx, if you -- as we said before, every year, we spend the CapEx to capture the future growth opportunities. And in the past few years, our CapEx has risen very fast to capture the mega trend. And going forward, the next few years, when we start to harvest those investments, we believe that CapEx will begin to level off in terms of dollar amount. And that will lead to -- start to lower the capital intensity in the next several years.

I mean, for all the money they are making, TSMC is FCF negative this quarter. I understand it’s tough, but the pulling off capex makes sense.

Summary: The cycle doesn’t seem to be rebounding as fast as we’d hoped. Q4 will be okay, but Q3 looks like another rough quarter for everyone that isn’t Nvidia. I believe that tough results and outlooks are coming, as the Chinese recovery hasn’t materialized.

What’s more, for semicap, spending should moderate slightly, and the stocks should start to incorporate logic, not picking up quite as fast. According to everyone, 2024 looks like it will be a strong year, but the near term seems to be worse. The quarter ahead will disappoint the average semiconductor company as inventory headwinds eat into gross margins, the recovery continues to be pushed out, and AI only benefits a select few (Nvidia). Watch out.

ASML and the EUV Quandary

Now let’s talk about ASML’s earnings because there’s also much to unpack here. This was a meaningful beat and raise, yet shares are down on the outlook. In some ways, it’s tied to TSMC’s comments above. Here’s a summary of earnings.

ASML Holding reports Q2

EPS €4.93 vs consensus €4.63

raises FY Net sales growth guidance to +30% vs. prior guidance of +25%

Revenue €6.90B vs consensus €6.71B and guidance €6.5-7.0B

Gross Margin 51.3% vs. consensus 50.5% and guidance 50-51%

Guides Q3

Net sales between €6.5-7.0B vs consensus €6.49B

Gross margin of around 50% vs consensus 51.4%

A pretty meaningful beat and raise, both next quarter and for the year. So why the sluggish shares?

The question, as always, is a matter of sustainability. This quarter's big question is around the new Dutch export controls on ASML tools. Those new export restrictions come into effect on September 1, 2023.

It also doesn’t help when the entirety of the beat looks like Chinese DUV drove it. Check out the change year over year in Chinese sales as a percentage of revenue. It’s drastic.

What’s more, amidst this pull forward of DUV revenue before the restrictions, there’s a bit of a demand pushout for EUV tools. That isn’t what investors want to see in the story.

In our EUV business, we have seen some shifts in demand timing. The majority of the shifts are due to fab readiness, with some elements of uncertainty around recovery. Deep UV demand still exceeds supply. While we have seen delays in deep UV demand from some customers, it has been compensated by strong demand for tools that mature and mid-critical nodes, particularly in China. The demand fill rate for our Chinese customers over the last 2 years was significantly less than 50%

Additionally, they are fast shipping the DUV tools, leading to higher revenue recognition this year, and making the 2024 year look a bit more dubious. EUV demand does not look as strong as initially anticipated. 2024 all of a sudden looks a bit more at risk. Bookings are frankly weak, and the 2024 backlog is starting to deplete.

Q2 net system bookings came in at EUR 4.5 billion, which is made up of EUR 1.6 billion for EUV bookings and EUR 2.9 billion for non-EUV bookings

They had some commentary on their end markets as well. Memory isn’t bottoming; logic might bottom, but who knows? The key X factor for demand is China, which is not looking well in terms of demand, but strategic demand for tools (Chinese domestic semiconductors) is really strong.

Also, one of the surprising answers was probably what I liked the most about the call. It’s time to throw some water on AI excitement. AI servers require more complicated chips, but people forget that each H100 server likely replaces 10s of high-end CPUs. That is a net shrinkage of the silicon area.

What’s more is that the current installed base is underutilized, meaning that it’s going to take a year or so for higher utilization leads to AI demand meaning new ASML litho purchases.

But I think we're at the beginning of this, you could say, AI high-power compute wave. So yes, you'll probably see some of that in 2024. But you have to remember that we have some capacity there, which is called the current underutilization. So yes, we will see some of that, but that will be taken up, the particular demand, by the installed base. Now -- and that will further accelerate. I'm pretty sure. But that will definitely mean that, that will be, you could say, the shift to customer by 2025. So I don't see that or don't particularly expect that, that will be a big driver for additional shipments in 2024, given the utilization situation that we see today.

For all the optimism for AI servers, it’s only 6% of TSMC’s revenue and not a big part of the whole pie in terms of million square inches of silicon. But I want to continue an interesting series of thoughts now I’ve had recently, and that is that EUV likely costs a bit too much.

Reducing EUV Costs, or the EUV Quandary

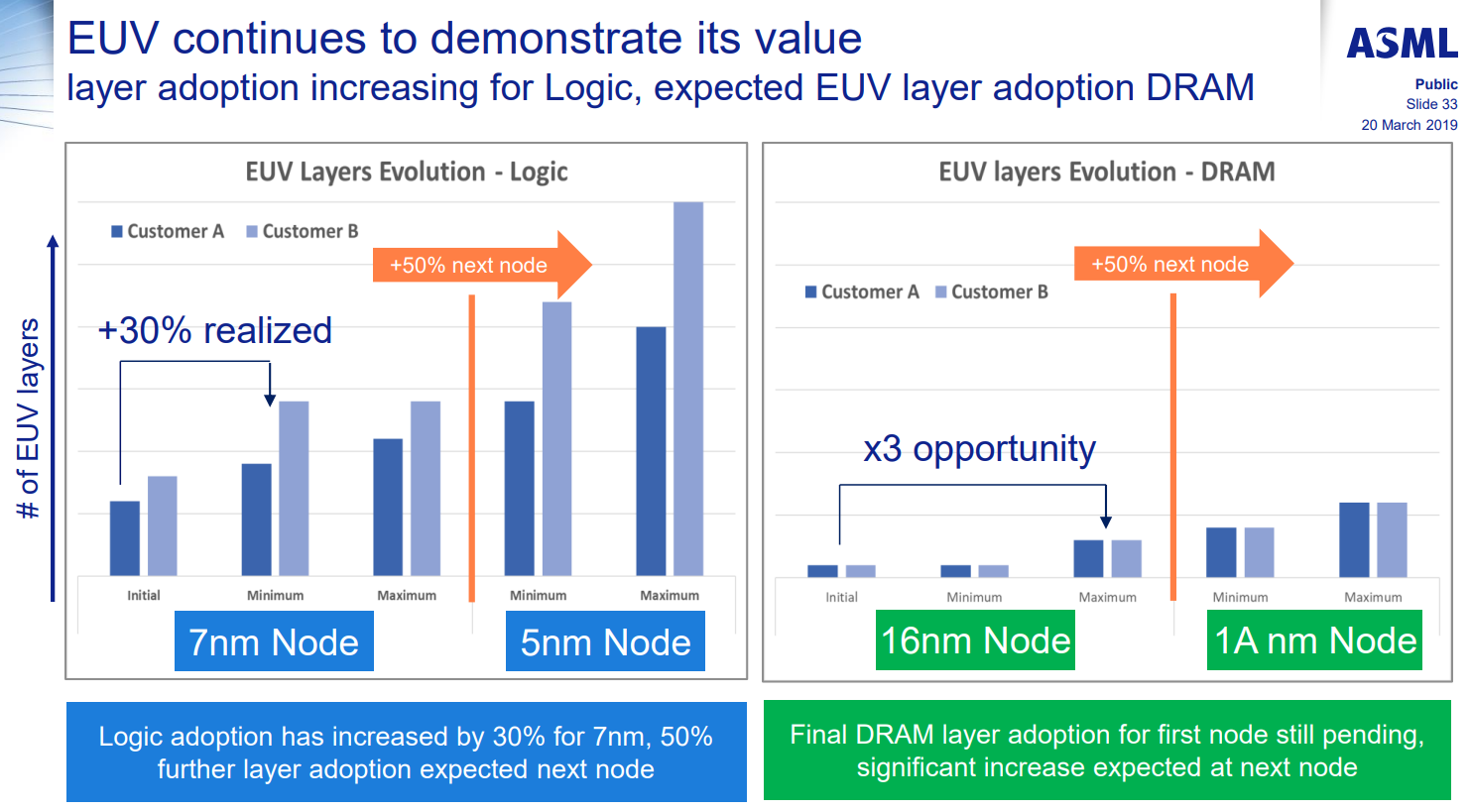

It’s no secret that capital intensity in semiconductors is increasing. The biggest jump in cost was primarily the insertion of EUV into the semiconductor manufacturing process. While I expect capital intensity per 100k WSPM (wafer starts per month) to increase, I expect it not to increase at the rate of EUV insertion. At Semicon, Tokyo Electron said they expect the shift to 2nm to be something like high single digits, but not as large as the recent increases.

The real reason for the increase is EUV. Notice the marked increase in EUV layers in 5nm from the graphic below. In the future, EUV insertion will decelerate. It just cannot continue at this rate of capital intensity.

The primary reason for this is it’s unsustainable. Most people acknowledge that the economic aspect of Moore’s Law is dead, but I don’t think increasing capital intensity by 15% per node will replace it. There has to be a bit of a shift. And the clearest path forward is finding a way to lower EUV layers.

It is no coincidence that the most exciting tool and process announcements are replacing EUV steps. This excellent writeup by SemiAnalysis on the Sculpta tool might as well be called “How to save money on your EUV bills.” In the past, it would be simply unfeasible to imagine a niche tool to reduce the step count of a single layer, yet here we are.

Or let’s take BSPDN, which I wrote up recently. One exciting benefit is that BSPDN can lower critical dimensions on the front side and lower EUV layers for the metal stack. That’s a process change that increases performance at a lower cost, and that’s all because it doesn’t use more EUV layers.

Put differently; I would be concerned when all your customers are excited about figuring out how to use less of your product in every single way. And what’s more, TSMC, the largest foundry and logic spender in the world, is saying we are trying to normalize our spending in the future.

For ASML, I would be a bit worried. EUV layers cannot go to infinity; the world cannot afford it. Thankfully, the multiple for the stock has come in a bit, but I would be worried. The biggest driver of ASML’s stock price has been multiple expansions as of late, and I would not expect that to continue. The peak of EUV intensity increases are behind us, and the declining 2024 EUV backlog should worry investors.

I’m worried about the entire space. I’ve written about Lam and ASML, and the stocks have massively outrun the fundamentals. It’s time for the stocks to take a breather. These are great businesses and will compound FCF per share at meaningful rates into the future. But share prices have pulled some of that forward, and I think it’s time to look around and realistically at the risks today. Be careful.

If you found this post valuable, please consider subscribing. I thought about not putting the ASML portion behind a paywall, which is the kind of quality of work I try to reserve for paying subscribers. But I think the world needs to know more about EUV layers and why intensity is peaking right now.

Thanks for reading today! Sorry to be such a downer, but it’s time to throw a little water into the space.

This also is going to be an exciting earnings season. I can feel it. I have some thoughts and will post about Alphawave and the knock-on effect of the TSMC quarter in a paid post soon. Until then!

awesome write-up! I thought it was odd that chips rallied so hard while MU sorta stayed flat. I'm not super technical but if the chip cycle was on this sharp trajectory back up again, one would think that MU would be going up with it. Maybe I'm reading into the reaction to Micron's report incorrectly, but I suspected that chips were getting ahead of themselves to a degree and were setting up for disappointments this quarter - hopefully I can get back into some of my favorites, soon!

Have you written anything on SMCI? Or if you haven't, have you seen any good write ups on it?