2026 AI & Semiconductor Outlook

A wee bit late, and a bit different this year.

Happy New Year! Last year was incredible for semiconductors — and AI stocks in particular — so as tradition demands, here’s the annual outlook. Fair warning: outlooks are hard. Things change constantly, and my views will change with them.

But first, let’s see who actually won.

2025 Year Performance Review

Let’s ask ourselves who won this year, and the answers are a bit surprising.

If I had to put the stories of 2025 in semiconductors into a single cohesive narrative, it would be:

AI spending stepped down the stack. Memory and optics were the beneficiaries. The bottlenecks moved from GPUs to the things that feed and connect them.

Semicap finally participated. WFE was tepid, but the stocks ripped anyway. The market is pricing in what’s coming.

Automotive remains in purgatory. I thought it would bottom last year. I was wrong. Will it bottom this year? I’m done guessing.

This is the year the AI story got leverage. This remains my favorite topic, and I wrote about it in Capital Cycles and AI and referenced it in the railroads piece.

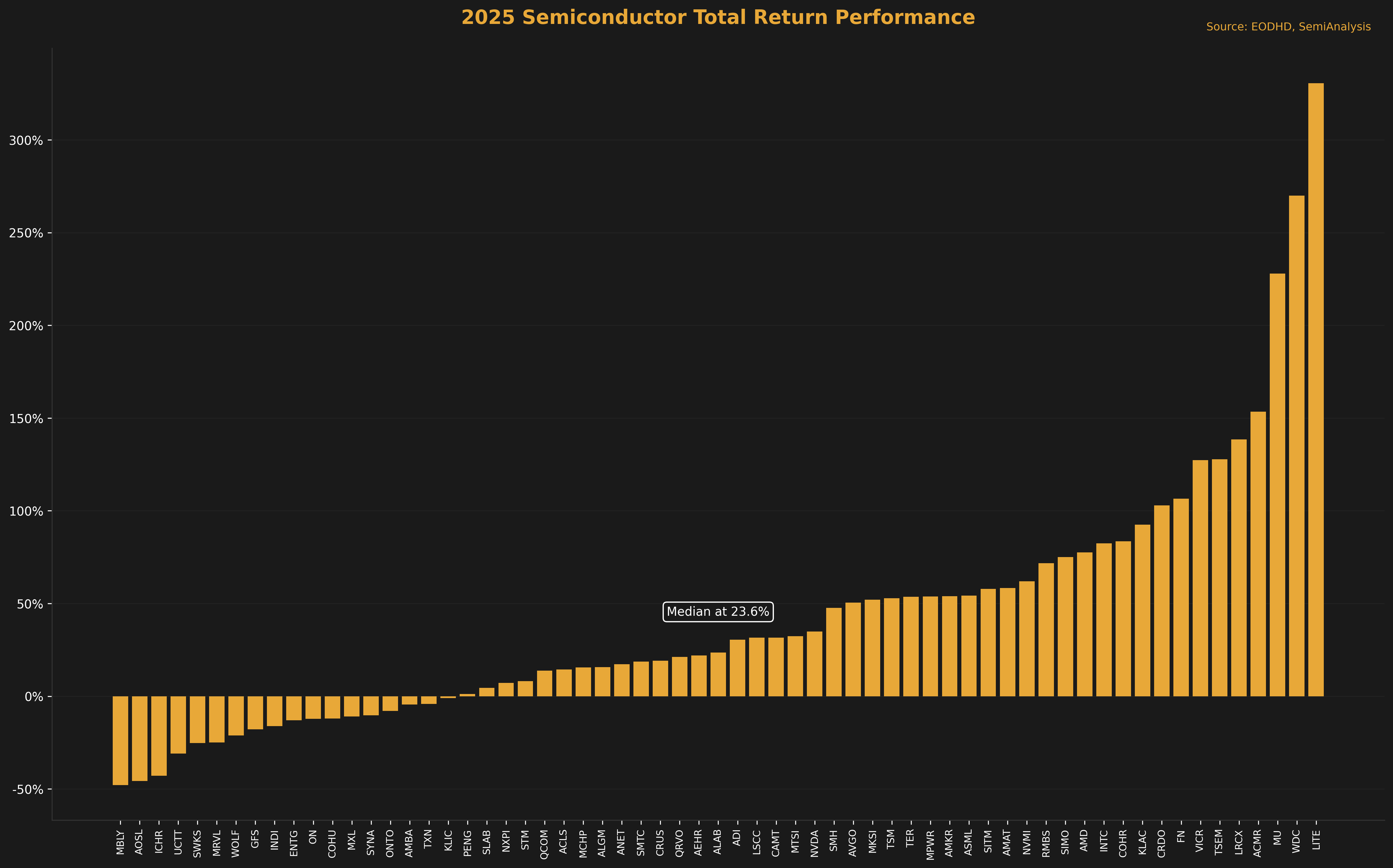

The chart below tells the story.

This year was clearly the year of memory and optics. I was pretty bullish on optics last year, and I think that definitely was the best prediction of them all so far. I also said that HBM would be really solid, and that definitely worked out.

I did, however, get really negative on everything related to the trade war and flipped out a bit too late. But at the end of the year, I am back to a believer, as I believe the most logical path is probably a bubble in the semiconductor / AI world.

2025 Predictions Scorecard

Before we continue into each big key theme, I did want to evaluate some of my “predictions”.

What Worked:

Optics “most bullish for 2025” — LITE +331%, FN +107%, TSEM +128%

HBM memory — MU +228%

AI returns moderate — NVDA +35% (vs +178% in 2024)

Intel pivot (Aug) — +75% from $21 to $37

Rambus (MRDIMM) — +72%

SiTime — +58%

MPWR — +54%

Lattice — +31%

What Didn’t:

AMD bear — +78% (ouch)

“Avoid NAND/HDD” — WDC +270% (missed a 3x)

Automotive bottom-fish — ON -12%, MBLY -48% (year 3 of pain)

Semicap “middle of road” — LRCX +139%, KLAC +93% (undercalled)

I’d say it was okay, but I definitely think I could do better. Anyway, let’s move on to this year’s themes, because I think they are noteworthy.

Memory and Optics

The bottlenecks became the winners. I was bullish on HBM last year, but I underestimated the knock-on effect: when HBM sells out, DRAM tightens. When DRAM tightens, prices rip.

People are buying DRAM for the price of a new PC; the price changes are catastrophic. I have never seen a line increase so rapidly and so sharply in semiconductor history. After the worst memory cycle, we are now in the strongest memory cycle in history. No surprise that a historic AI cycle would cause this. In optics, we are seeing a similar situation, with a complete shortage of EMLs, CW lasers, VSCELs, etc. It’s all backordered, and that’s for the massive 800g cycle. We are not even talking about the higher-performance 1.6T transceivers.

This is a perfect example of an expansion of the previous year’s historic Nvidia rise; it extends to suppliers. I think this will continue, but it’s difficult to replicate this result. I wouldn’t be surprised to see something similar to Nvidia’s performance this year, where returns moderate but are strong after a historic year.

Another signpost I have to consider is that NCNRs are ramping up in memory, and the last cycle occurred 9 months before the peak of the memory cycle. This time, however, I think it will be a much longer cycle, given the magnitude of AI.

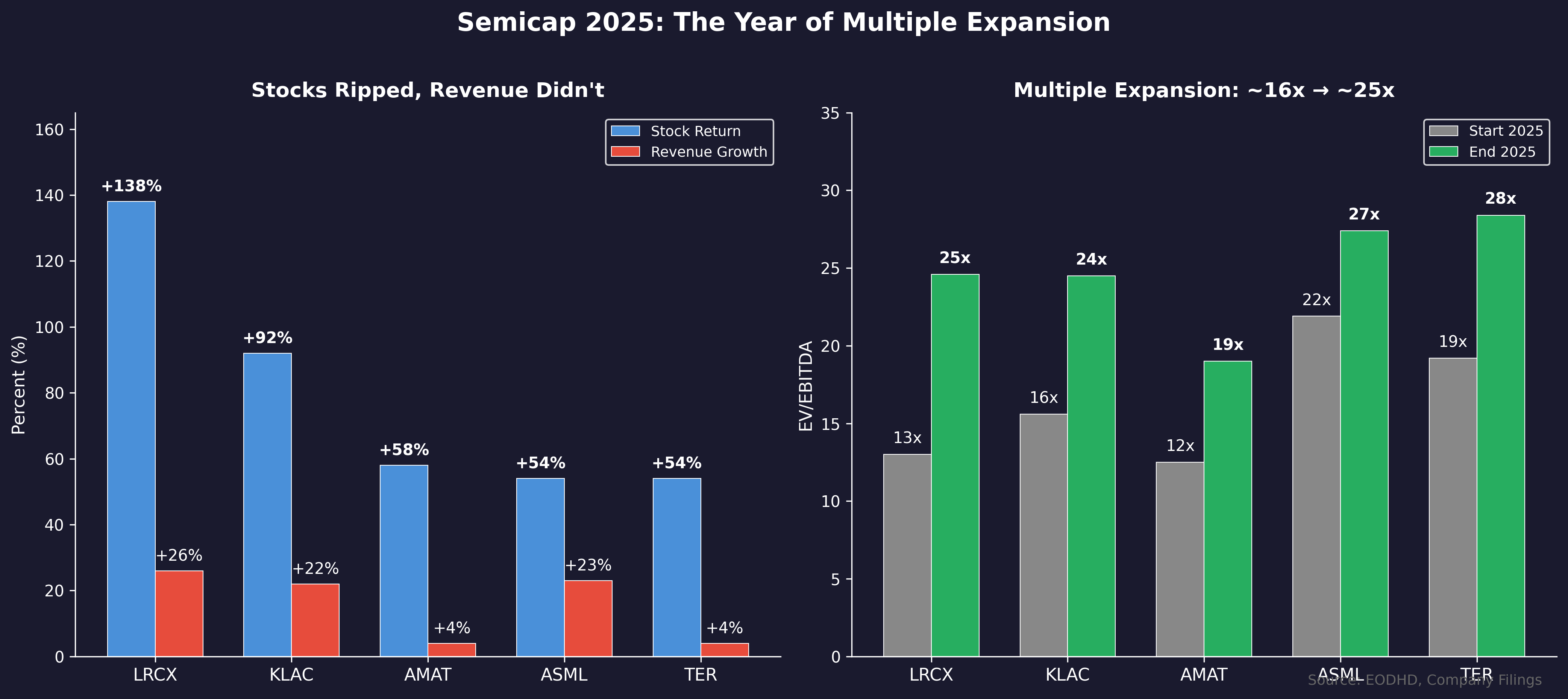

Semicap Equipment Roared on Modest Results

I recall that, once, semicap trading at 20x earnings was a hope, and now the average semicap company trades at 20x EBITDA. Discuss multiple expansion, but there have been quite a few commodity providers that have seen even worse on the data center side, so this is not surprising.

The surprising thing is that it’s not that semicap revenue grew rapidly this year; rather, multiples expanded, and forward estimates are rising. Now that’s because stocks trade on expectations, and given that logic is in a shortage, memory pricing is ripping, it’s pretty clear that 2027 and 2028 are going to be wild years for WFE.

I think the fundamental story for Semicap is just beginning, and I expect to see pretty massive beats in the coming quarters.

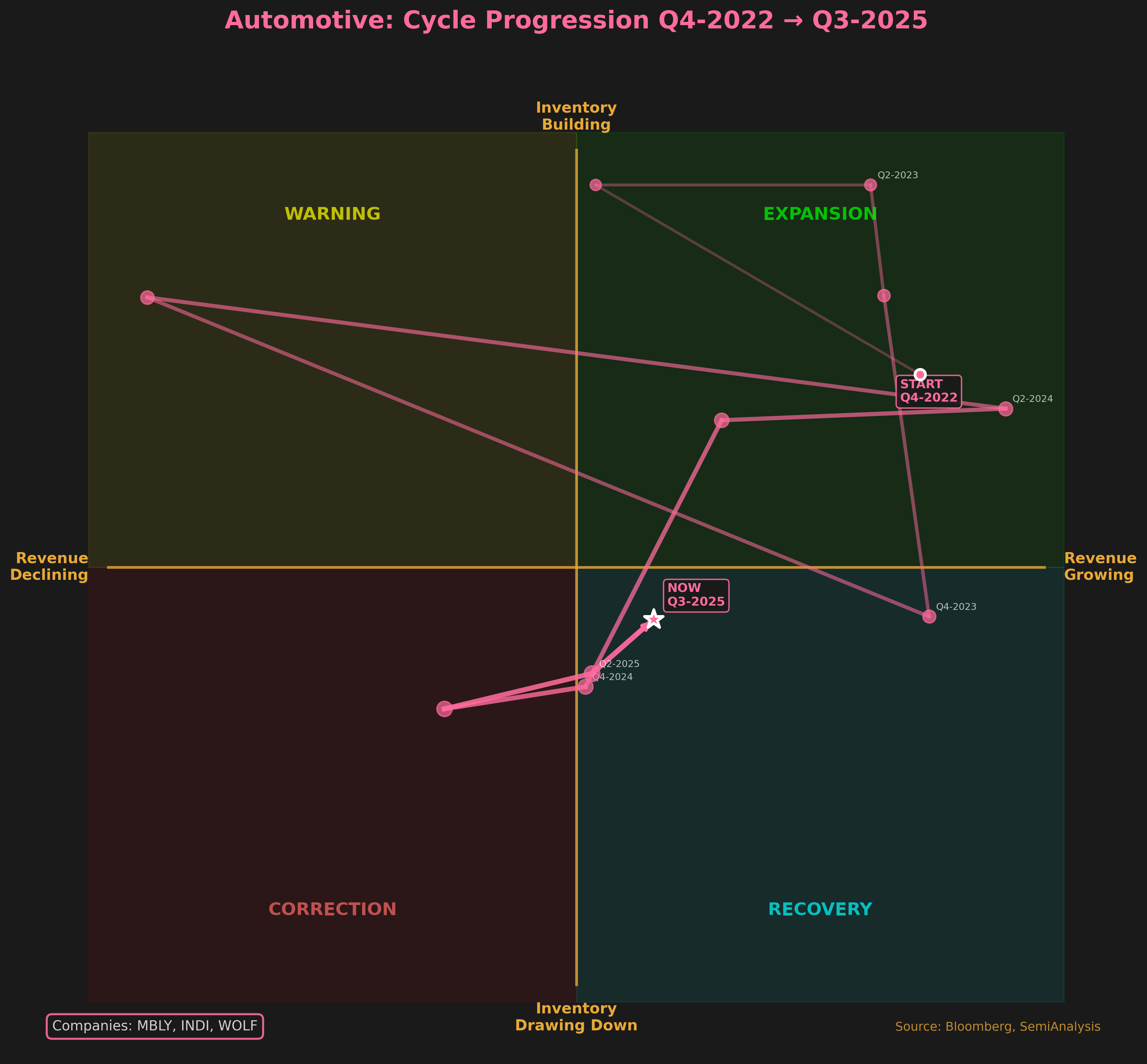

Automotive is in Death Valley

Last year, I tried to call the bottom in automotive. It never happened. One way to look at this is to track the historical inventory cycles of automotive and analog companies.

We didn’t experience the drastic correction observed in other markets, and we are now in the “recovery” quadrant despite a mild correction. The market has been and continues to expect weakness, and as much as I want to bottom call again, I mostly want to give up.

Maybe that means automotive and analog rips, but, man, it’s a tough market with the continued Chinese competition. If you asked me to put a gun to my head, I’m long. But I would have said that last year, and would be dead. So your mileage may vary. It’s troughed, but will it go up? Who knows!

AI Learned about Leverage

This is the year the AI story got leverage. I wrote about this in

and again in

In the second, I called the “alcohol” of this party, and I'm going to use this analogy in the future. Oracle is drinking the hardest, borrowing $100 billion over four years for the Stargate project.OpenAI has committed $300 billion to data center buildouts, while internal documents project $115 billion in cumulative cash burn through 2029, a period executives reportedly call “the valley of death.” There’s only way to party this hard, and it’s leverage.

Meanwhile, financing became a bit more circular this year. Nvidia takes equity stakes in GPU customers. Those customers buy more GPUs. The GPUs become collateral for debt facilities. The debt buys more GPUs. Nvidia’s revenue rises. Repeat.

None of this is illegal or actually even unusual for a capital cycle. But the bond market has begun asking questions that the equity market has not. CoreWeave’s credit default swap spreads widened sharply in late 2025, but in recent weeks have relaxed. This is now a key factor in this cycle. We will have a lot more to see this coming year, especially with a potential IPO. Supply is coming to the market to meet demand.

Anyways, it’s time for the broader semiconductor cycle.

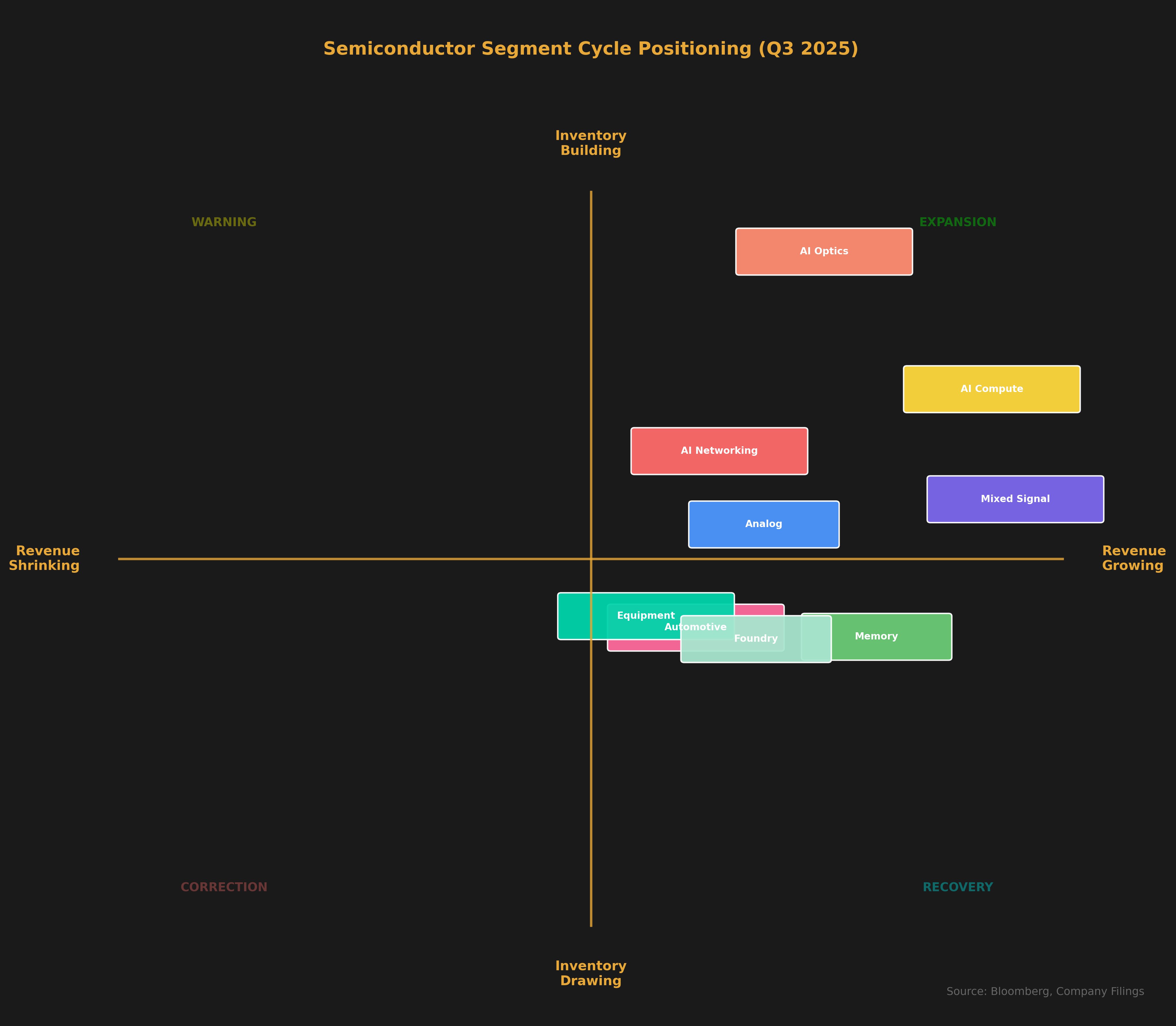

The Total Semiconductor Cycle

Let’s now turn to my favorite (and I think famous) chart about semiconductor cycle positioning. As you can tell, we are now in a huge upswing, and I believe almost every single company will make it out of the recovery cycle into the expansion cycle. The real question is, when will inventory growth outweigh revenue growth?

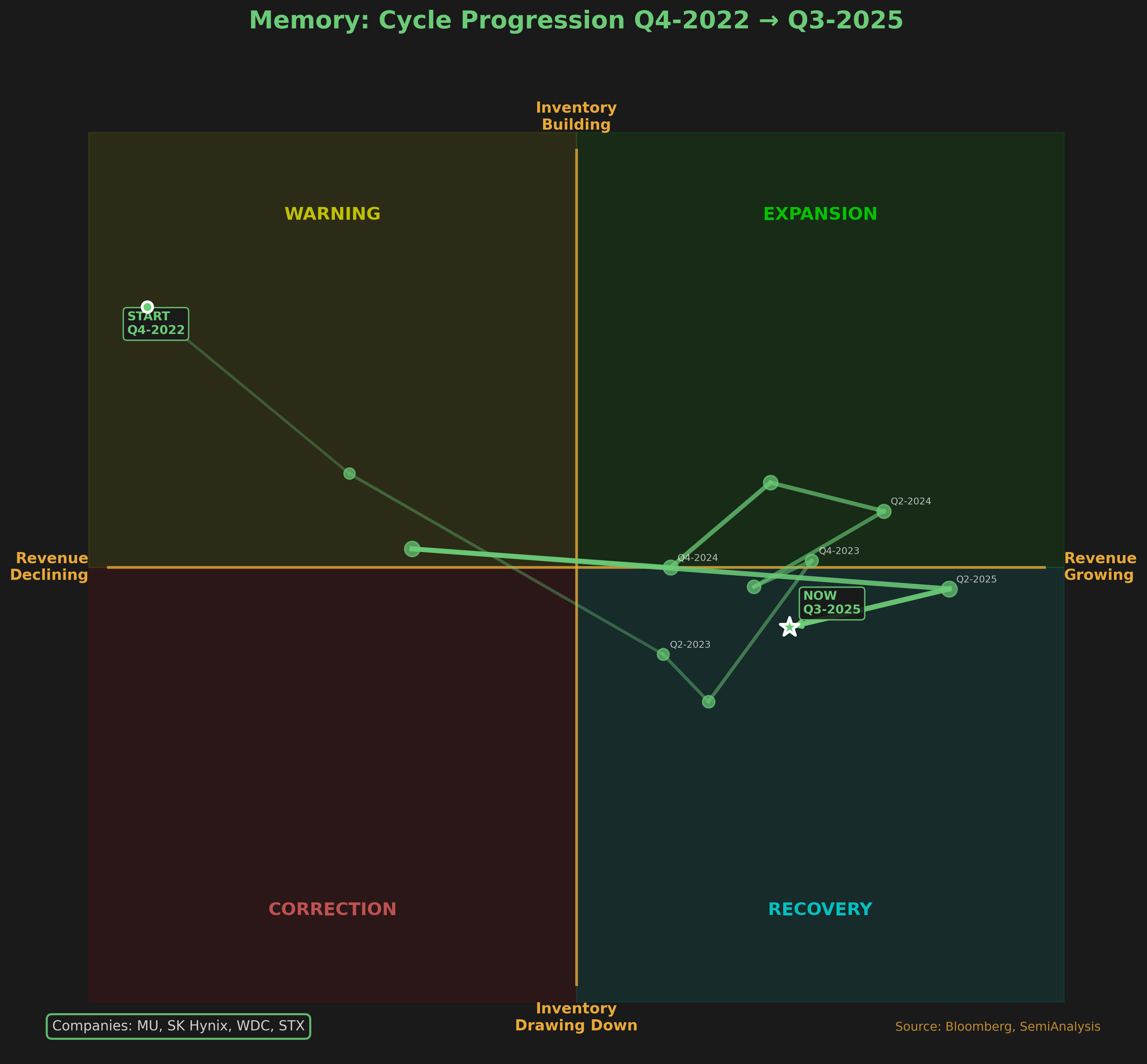

What’s also interesting is that Memory is still in the recovery cycle; we still aren’t even seeing inventory builds meaningfully. This is usually an “okay” time to own, but once meaningful inventory buildup begins, caution is warranted. Also, it’s surprising to see Automotive still in recovery, but not unexpected. It had previously spent the longest time in the expansion quadrant, as the 2020 cycle resulted in almost 4 years of consistent revenue growth.

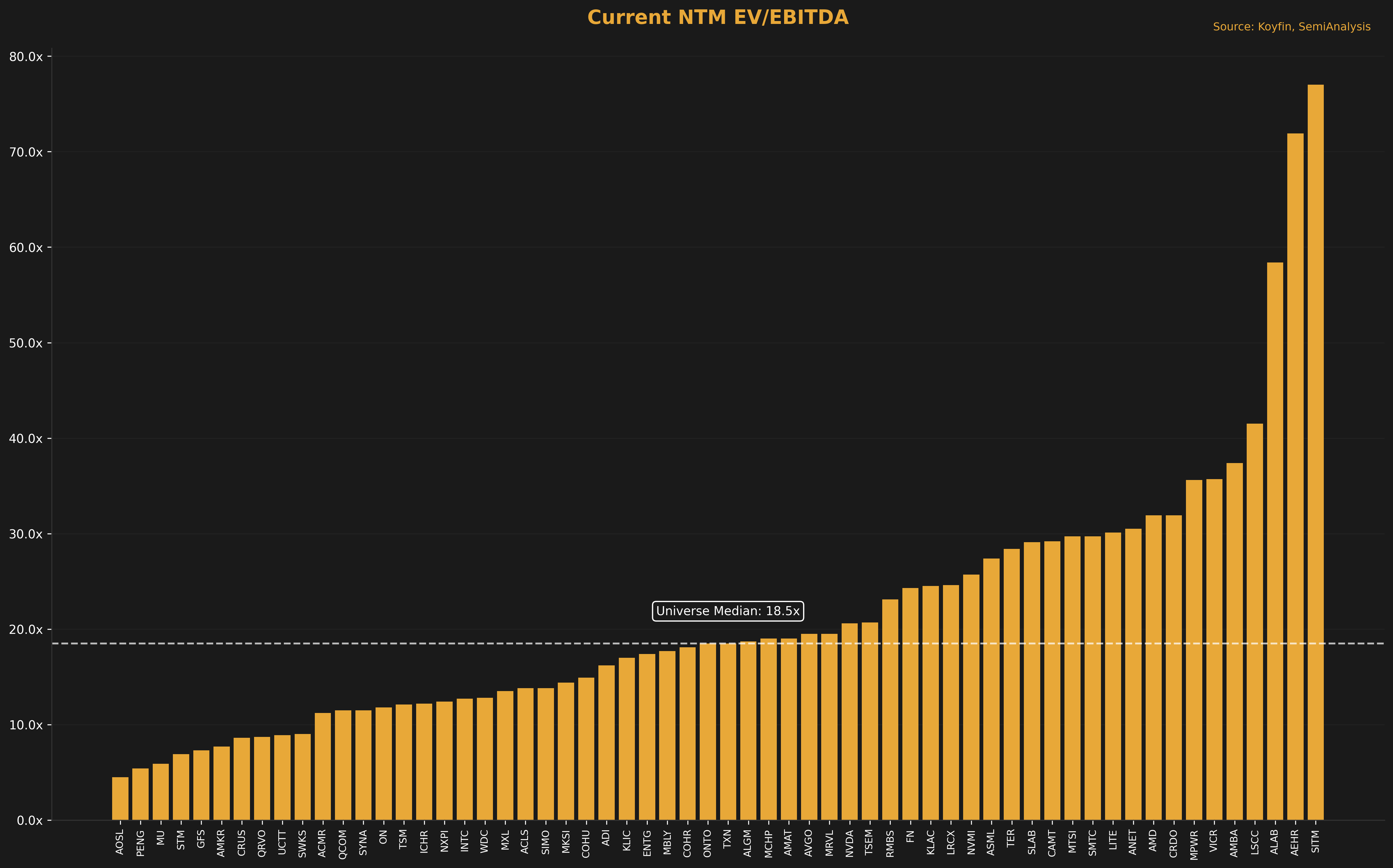

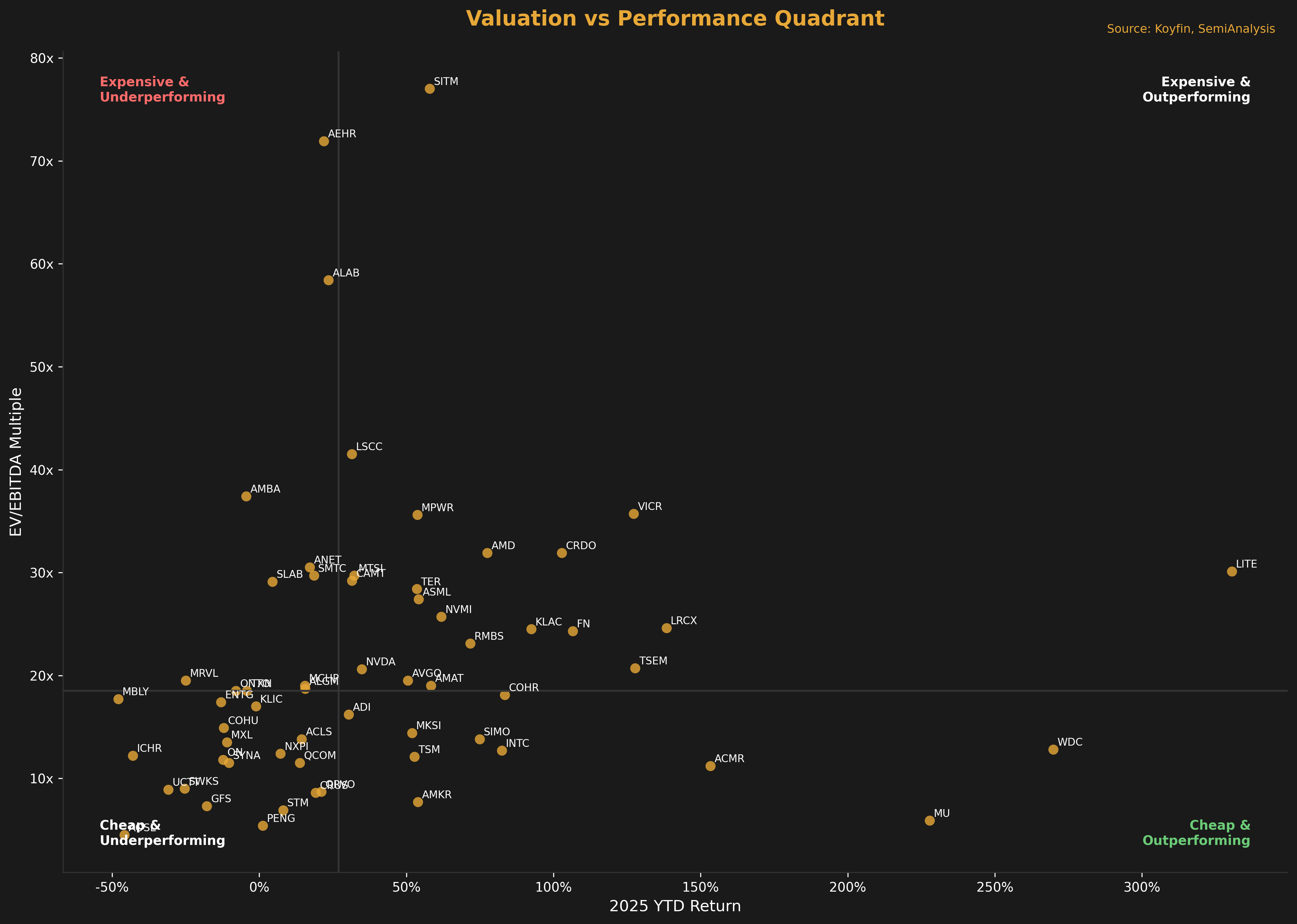

2025 Valuation and Valuation Changes

The median semiconductor company is not cheap. The most costly are SITM, AEHR, ALAB, and LSCC.

Some are during their cyclical troughs, so it makes sense. Still, the most exciting situation is when a company is trading at below-average valuation and high quality (looking at you, TSM, ENTG) or when it’s an excellent company trading at average multiples. That would be AVGO, NVDA, TSEM.

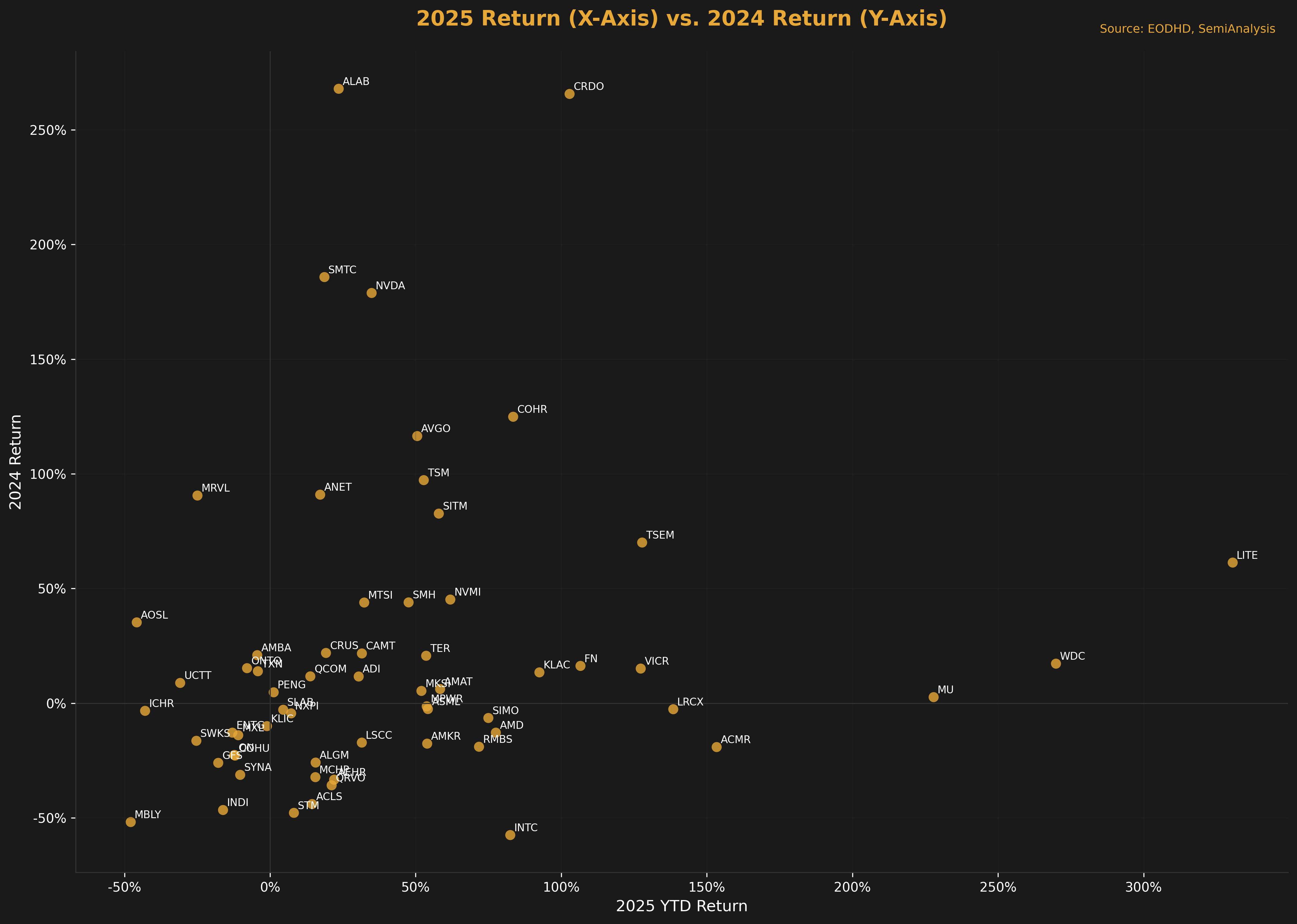

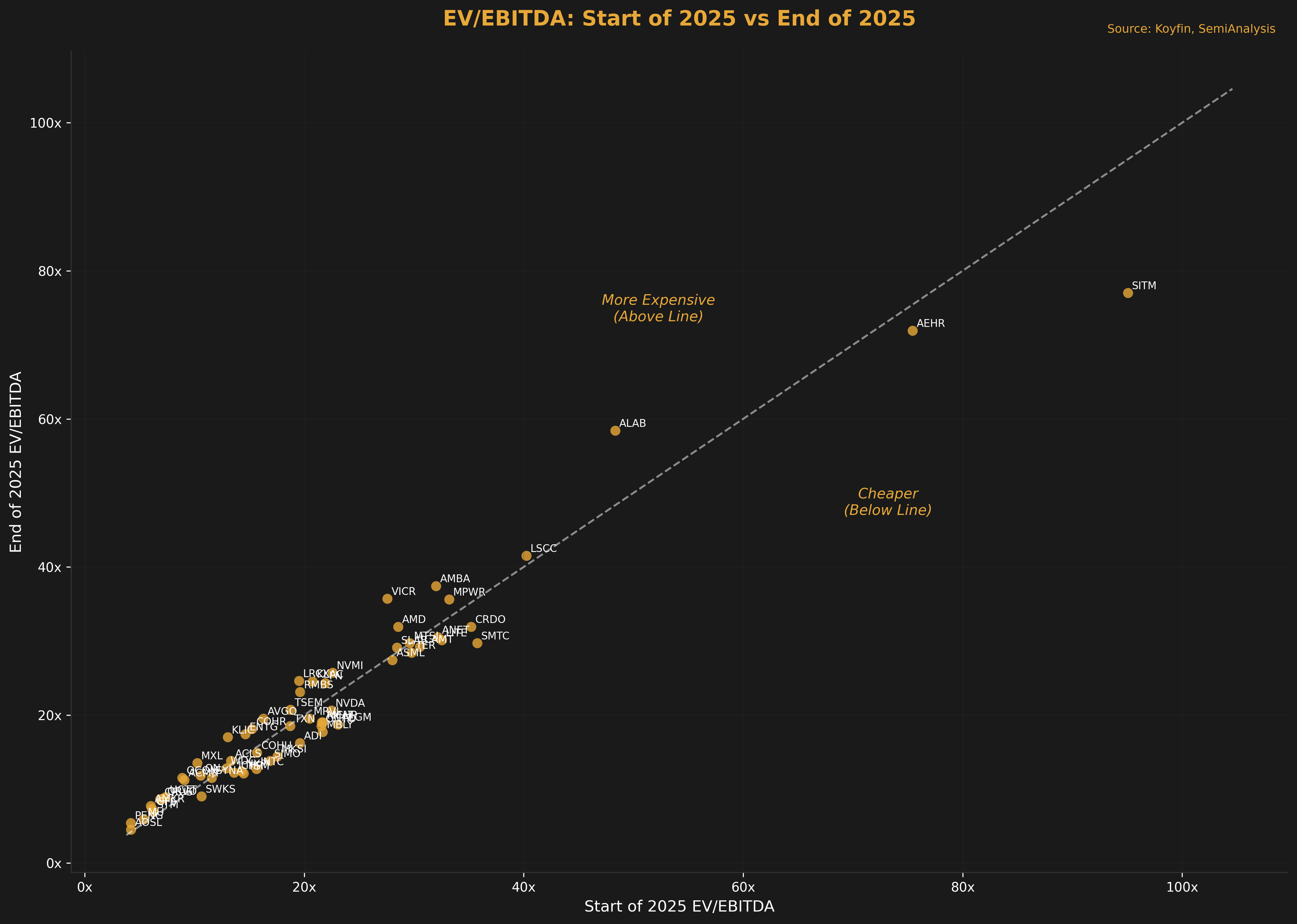

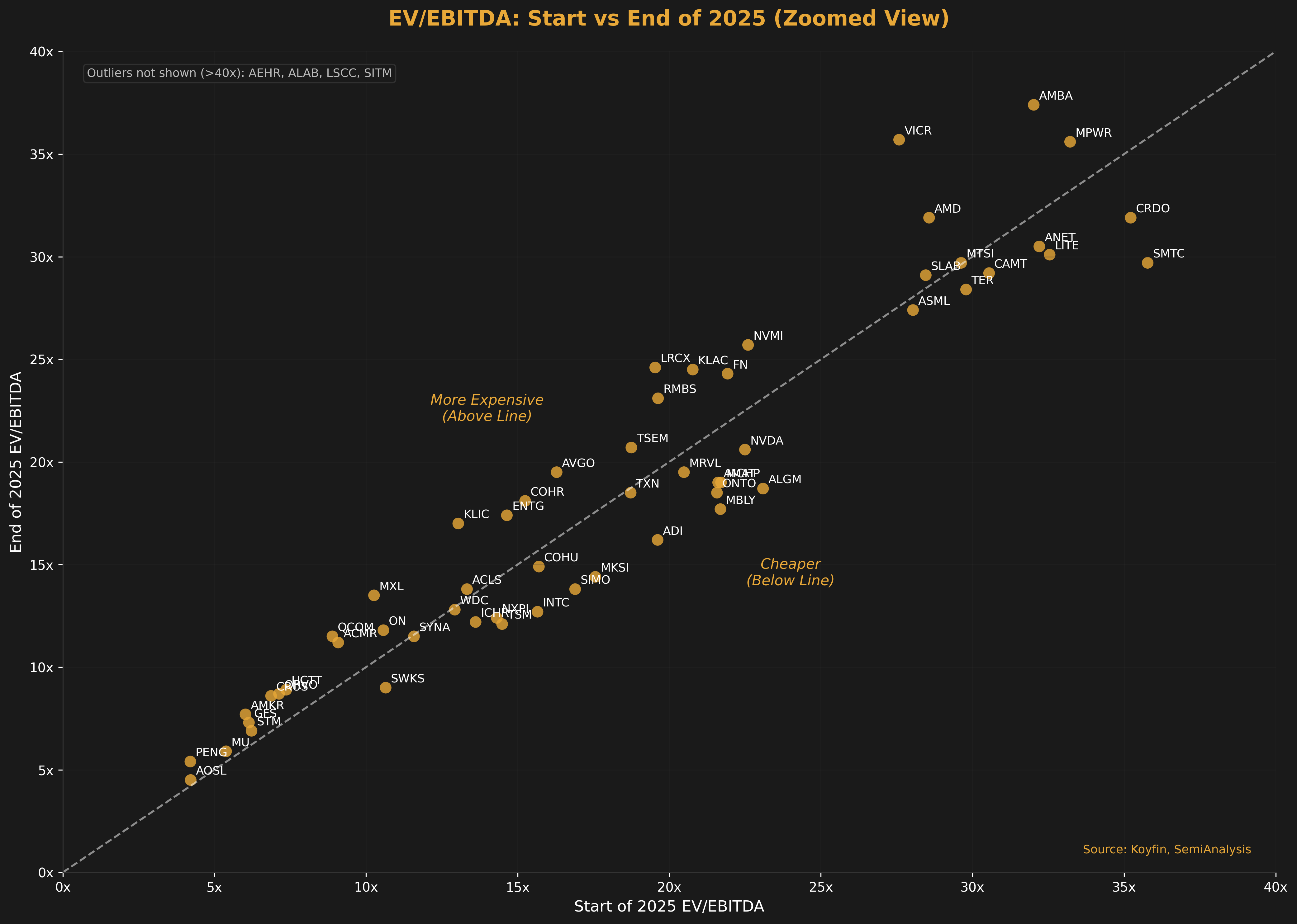

But another way to frame it is, did the company become more or less expensive? This is my graph to represent this. Now, the problem is the outliers here, so I did a zoom-in.

Pretty much it’s better to be below the line, not above. It’s not surprising that companies that are performing poorly are becoming more expensive (SWKS, COHU, etc.). Still, it is surprising to see companies that perform well become cheaper, namely LITE, CRDO, and SMTC. That is usually an interesting place to fish. Additionally, the observation that NVDA trades below the line is noteworthy, and as it assumes and retains the most prominent position in the market, multiple compressions are somewhat unsurprising.

It’s cool finally seeing ASML multiple compress, and it’s funny because it’s just in time for reacceleration.

Now, the final chart I love to do is the underperforming and outperforming chart considering valuation. Historically, you want to buy cheap underperformers, but companies that are underperforming this cycle often have a particular set of issues with them.

Of the companies I see at the bottom, I think most of them are automotive, and that itself is a cycle call. Meanwhile, being cheap and outperforming is another interesting concept, and this is where memory will “shine” as EPS rises and multiple contracts are signed. Finally, it is expensive yet outperforms the competition. Nvidia and AVGO are truly incredible because they are decently priced, continue to outperform (marginally), and are “becoming the market”. Now, let’s step through each segment cycle.

Sector by Sector Overview

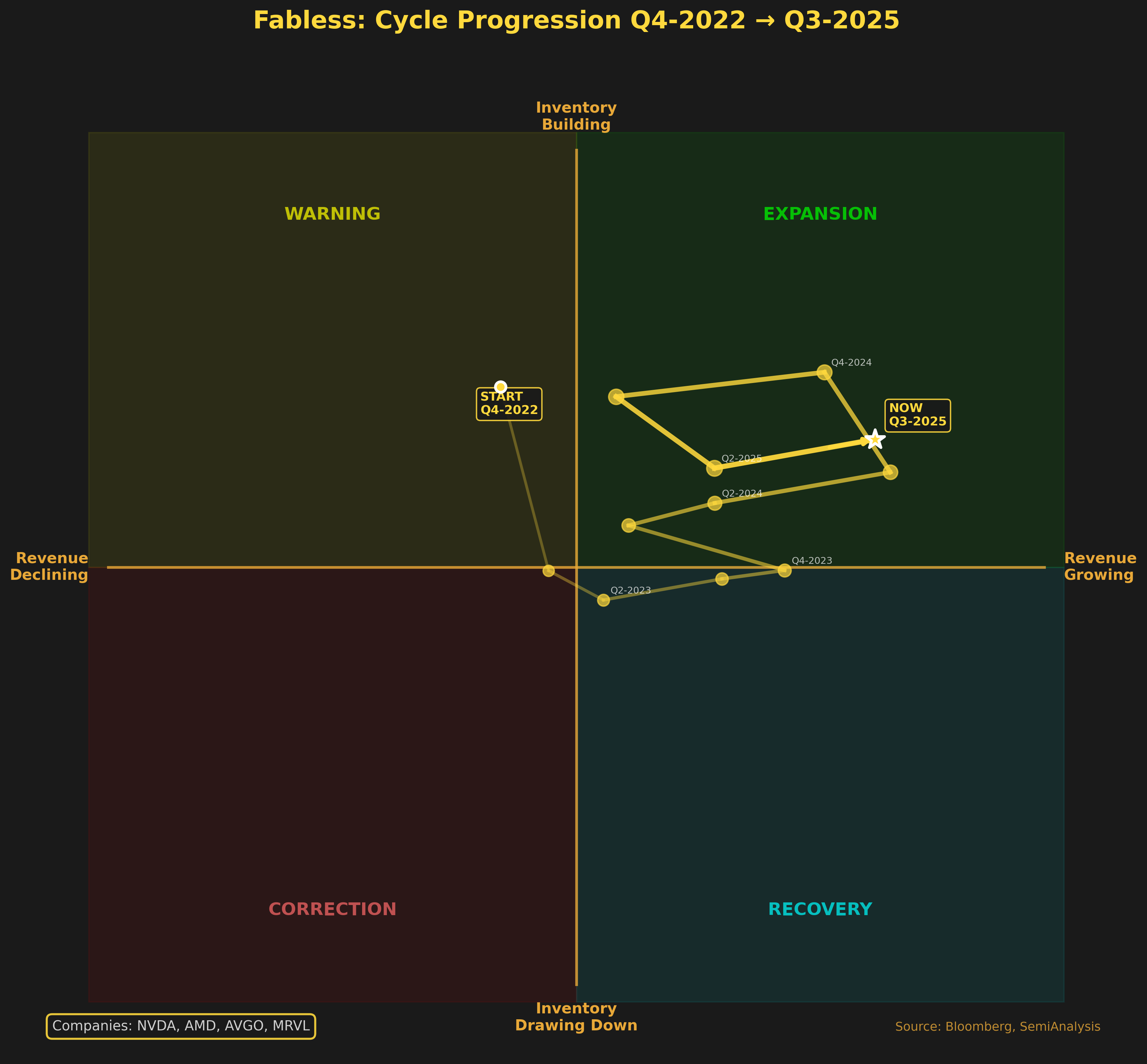

Now it’s time to walk through the sectors to review the inventory cycle of each. First and foremost, let’s do the most important segment, “fabless semiconductor” which really is just AI revenue now. Everyone expect AMD has meaningful amount of revenue exposure here, and you can argue it’s AMD’s “story”.

The interesting thing is that you can see the inventory cycle that occurred during the GB200 build-up partially resolve itself. While there was a point where inventory was growing faster than revenue, we are now back to a very expansionary market. This is likely to be a “fine” year for these companies, and I expect further outperformance (though probably not eye-watering). I’m still not a fan of Marvell, but at this point hell, even they deserve a bid.

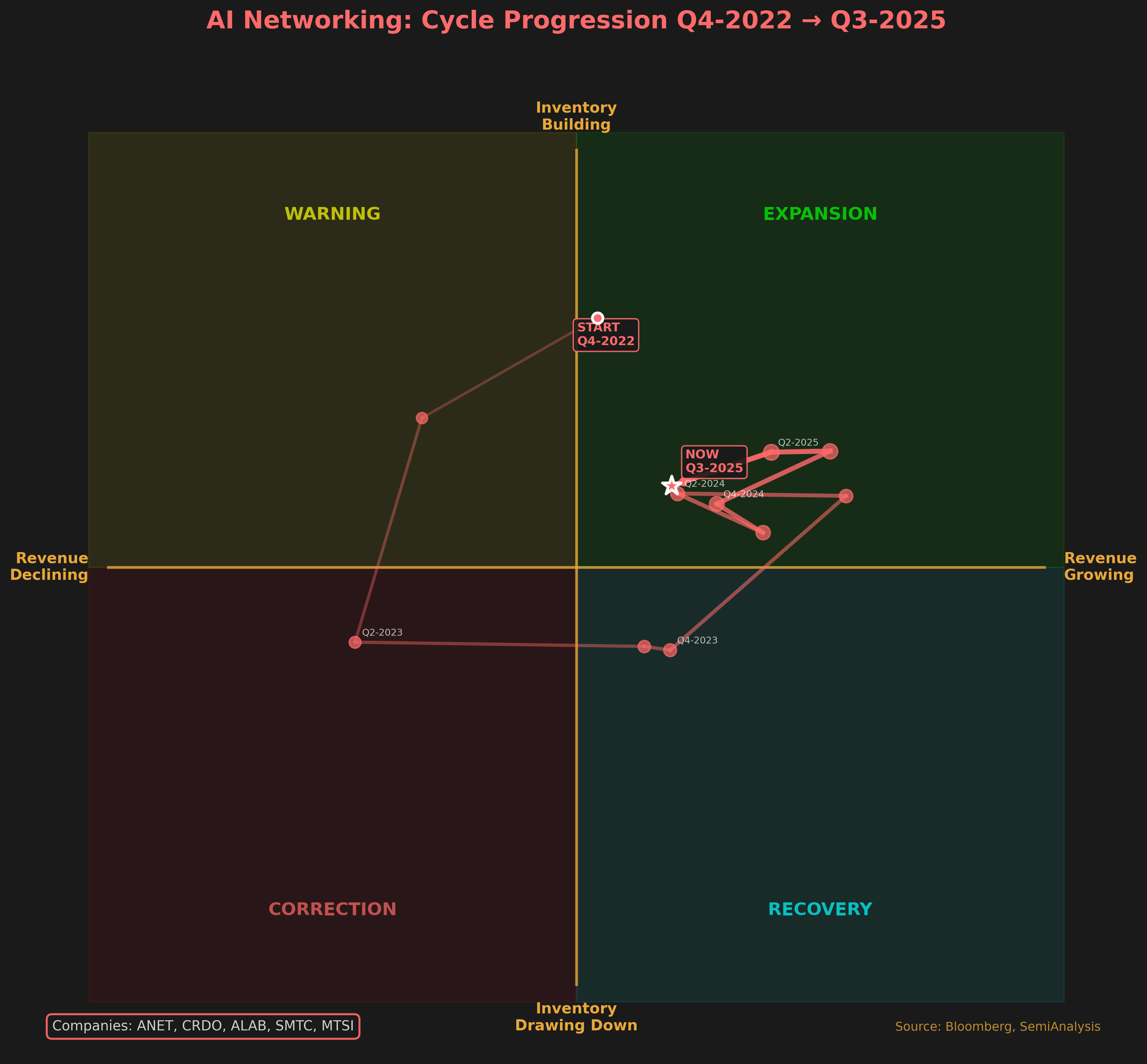

AI Networking

This is probably the bottleneck and will remain the bottleneck. I really like the setup of these companies, even after the prodigious run. Odds are we will see slightly moderated outperformance given how hard it ripped year to date, but I do like share gain stories like SMTC, which should gain share at TPU.

I expect another great year in AI networking, as hilariously enough, most of the 800G and 1.6T cycle is still ahead of us, not behind us.

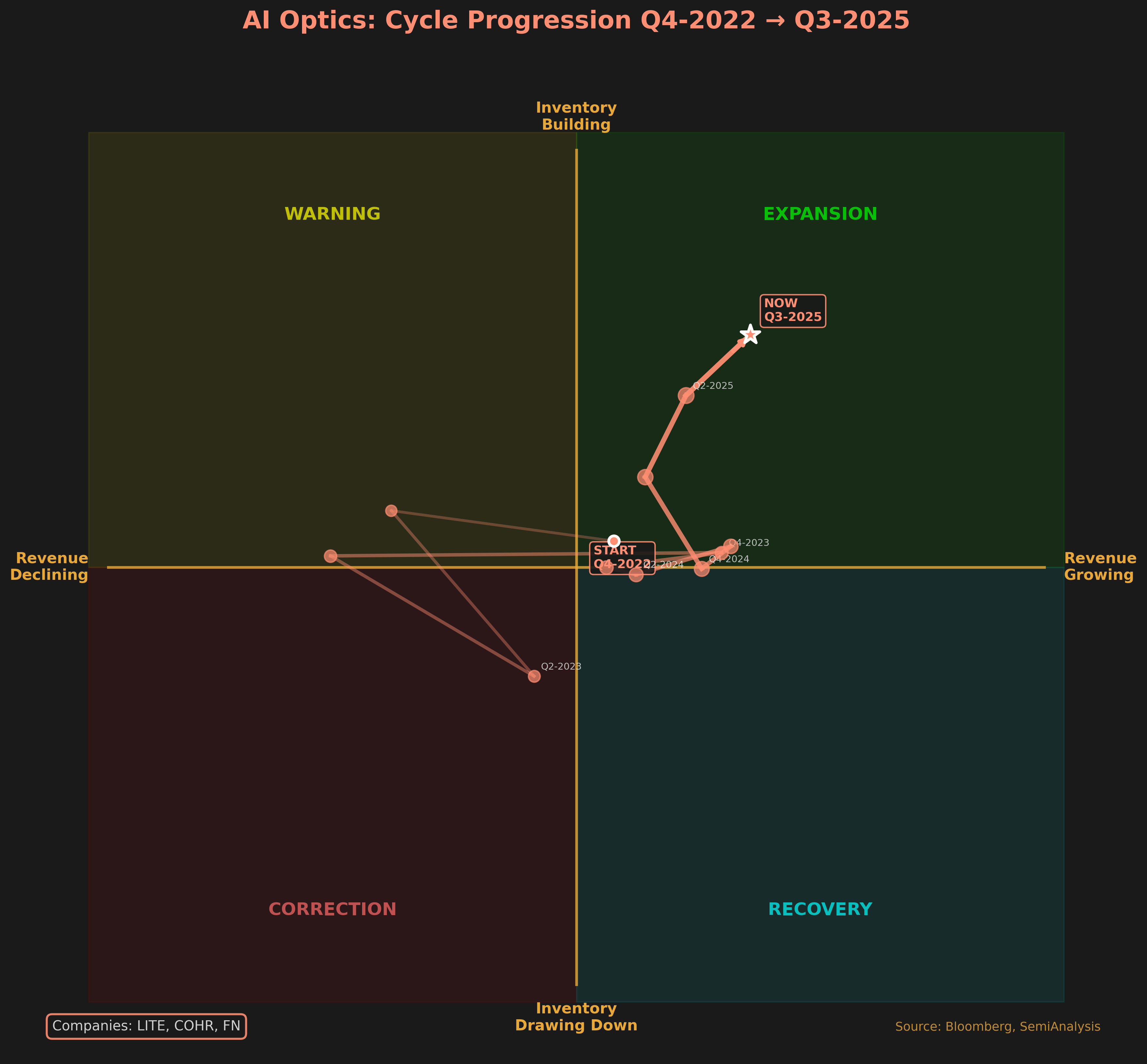

Meanwhile, I’ll have a separate call out for optics, which is probably the hottest segment right now. Another name not mentioned here is 5802 and AXTI, which are part of the InP and CW laser trade. These stocks are parabolic, but the demand seems unstoppable.

This is pretty much an industry on fire, and I think LITE is leading the way. I don’t really have much to say other than “wow look at them go”.

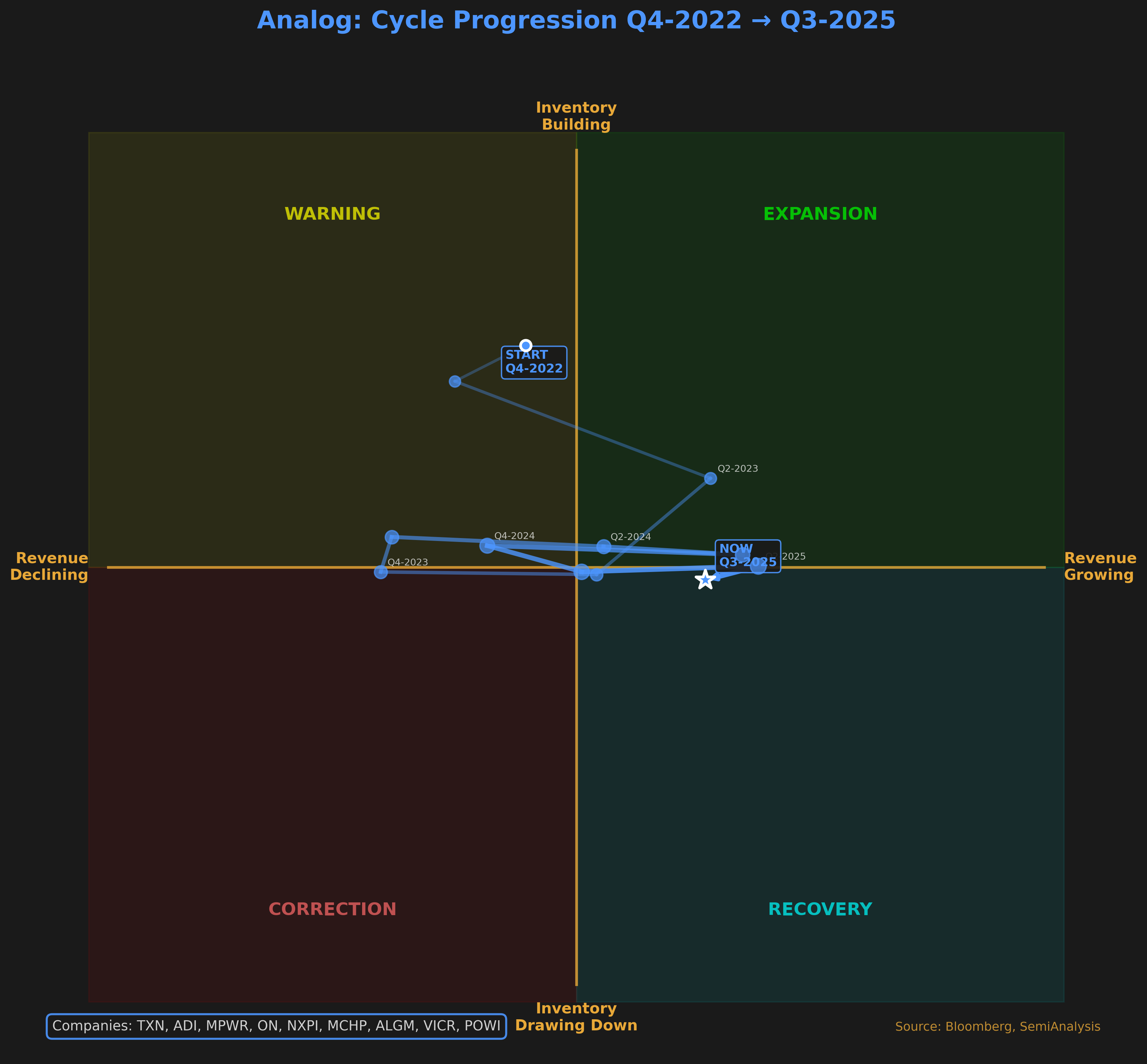

Analog / Automotive Cycle

Now this is where I think I will be spending some tokens to discuss. Look at 2022 and how the inventory cycle has continuious stayed high, despite even negative revenue. This is a chart that is showing the global buildup in inventory in 1 picture, and I think that because there never was the horrific blowup in inventory, there isn’t the parabolic rise today.

Now, the thing is, I think that will change on the margin. While MPWR, ON, ADI, TXN, NXPI, and IFX are mostly analog and power companies, I do believe that this time, surging demand for smaller parts of their businesses should pull those parts out of the trough.

The companies that might show (especially last year’s plunge) way better are the much smaller, pure-play companies. WOLF, INDI, MBLY have corrected sharply out of the trough, but still are burning through inventory. In aggregate, this is a healthy place to be.

Pretty much this is the single best setup in terms of inventory timing / the cycle. Maybe this is the year that it rallies finally, but I have been burned so many times before.

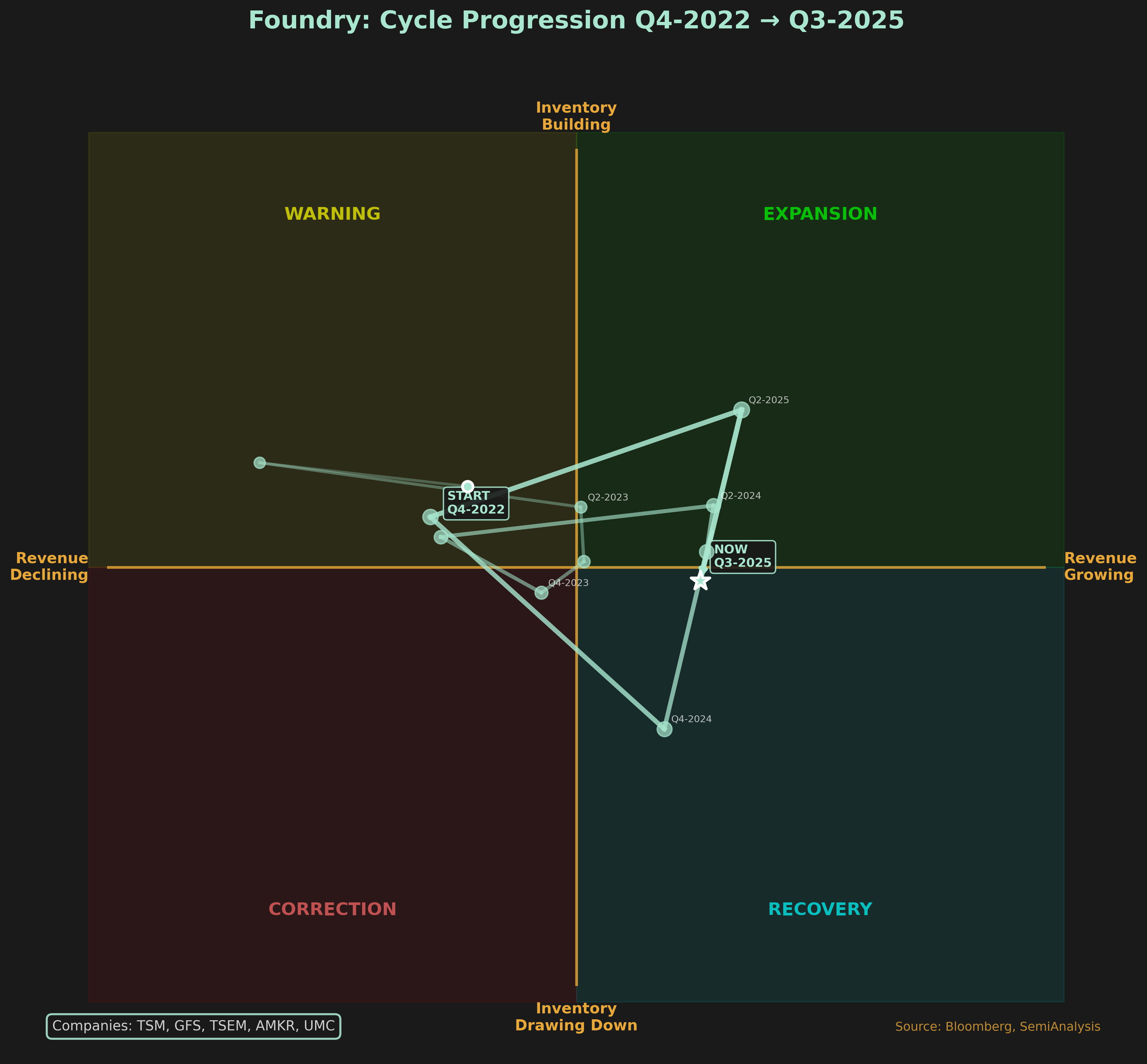

Foundry Cycle

This one, in my opinion, is somewhat imperfect. Inventory of wafers is rarely built to be busts in the way that semiconductors do, but I do think that the positioning of the foundry right now is very good.

I think there is a non-zero chance that foundry is the next bottleneck, as we know shortages in leading logic are happening at TSMC, which are overflowing to Intel and even Samsung. While AI is the story of the day, it is starting to completely fill the leading nodes at TSMC, with PC and smartphones going to other foundries as a gap fill. In some ways, this is like the HBM thesis, and Foundry is going to get the lift from AI selling out TSMC so completely.

Which brings me to my 5-second conversation on Semicap. I think that if the above is true (I believe it is), then the semicap stocks are about to have the strongest, most meaningful year in WFE history. Probably not a calendar 26 over 25, but something like 2H26 + 1H27 over 2H25 + 1H26. There’s clearly substantial demand, and we are starting to see pull-ins everywhere, including in China WFE.

Memory

We are still in the inventory burning phase, and likely will be for sometime to come. All of HBM is sold out, all of DRAM is sold out, spot is going to be probably be ripping on the back price increases / relaps.

I know that memory will have at least an incredible 6 months, if not 12. Who knows what stock prices do? This is where things get dangerous, but I believe it gets better fundamentally for some time yet. And that, of course, accrues to Semicap.

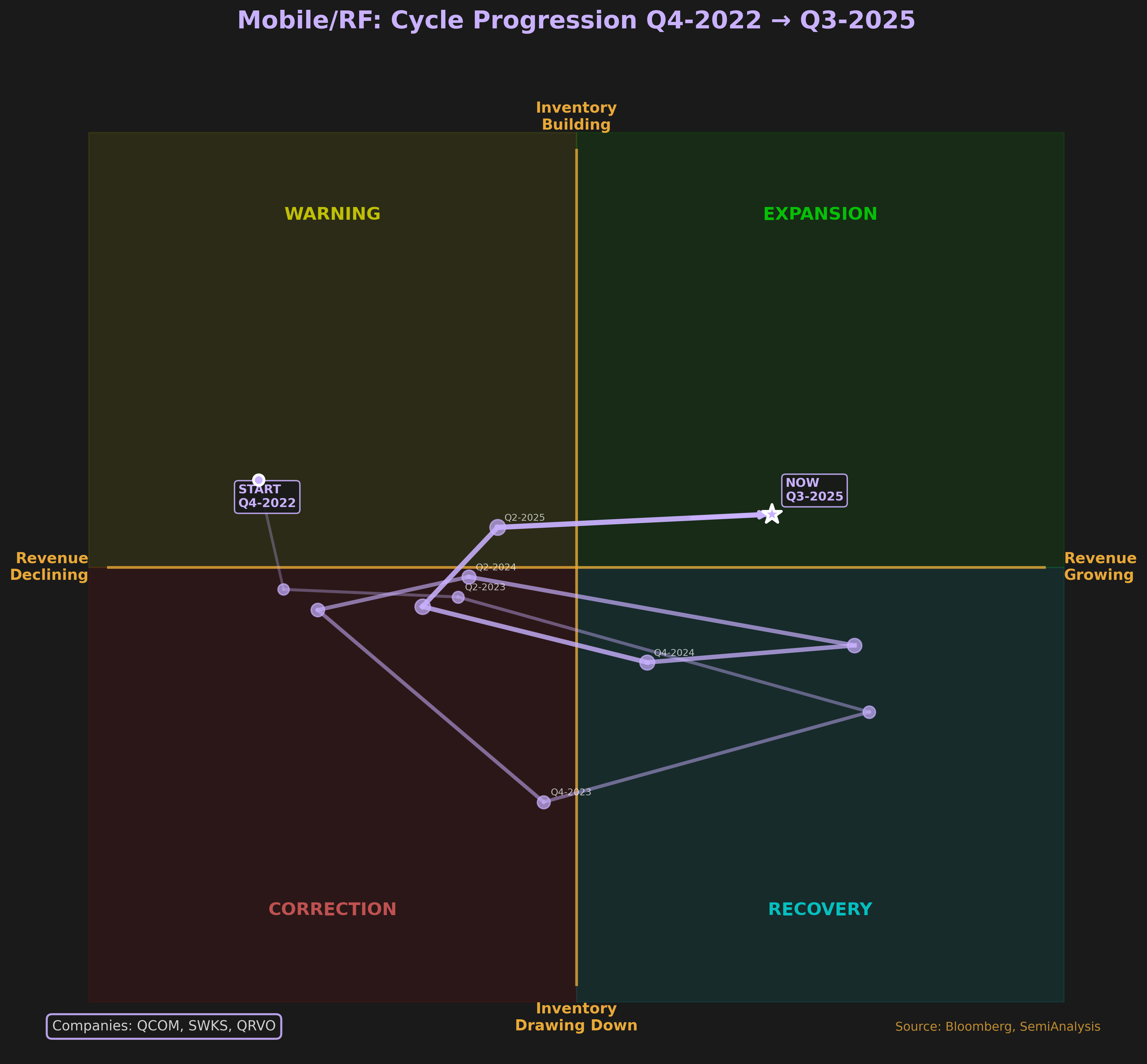

Mobile / RF

Inventory after multiple its so over and it’s so backs (you can see it in the chart) is finally so back. But now the real headwind is going to be memory pricing.

The consensus is that memory pricing is going to drive up phone prices so much that there’s really only one outcome: people buying fewer phones. I think that happens, and I think this is probably a lag to a certain extent. Inventory is cleaned up, but smartphones really are the new PC. It will likely be a decade of irrelevance before we care about phones again. This is, and will likely remain, the permanent funding shortfall.