2025 AI & Semiconductor Outlook

O3 and what's next. Marginal costs are coming for tech companies.

Last year, I called 2024 the year of AI’s adolescence, and that was quite a call. I “predicted” growing pains or a tremendous growth spurt, and the immense growth spurt happened all right. This last year was the year of AI through and through.

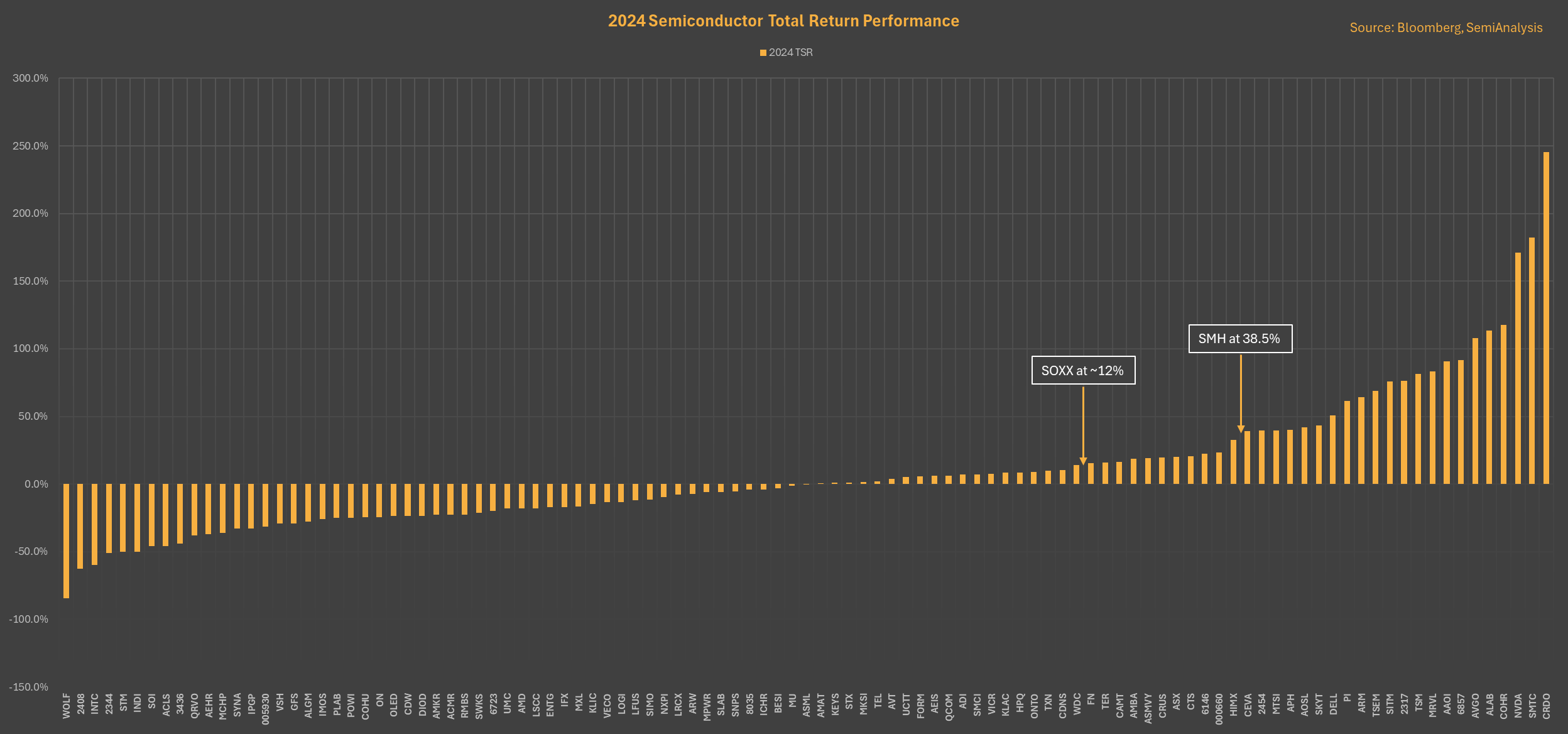

There’s a deep irony because anything related to AI had a phenomenal year while everything else languished. Surprisingly, SOXX underperformed the SPY, which seemed unheard of for the year that SOXX’s largest components ripped 100%+.

And that’s probably my favorite story from 2024. It was AI vs everything else. While Nvidia had almost a 200% increase this year, the median semiconductor company was down. That’s such a staggering divergence that it has to be one for the history books. When I did my 1997-9 dive, companies with horrible results still had share prices go up. But the breadth of results was unlike anything I’ve seen, and it primarily benefited the largest companies exclusively.

So, instead of discussing AI (which was good and is the primary subject of this newsletter), I want to discuss the lost year for everyone else in semiconductors. Then, I’ll bring it back to AI. Because if you look at this chart, this has almost been a widow-maker year for Automotive. Wolfspeed might (and should) go bankrupt.

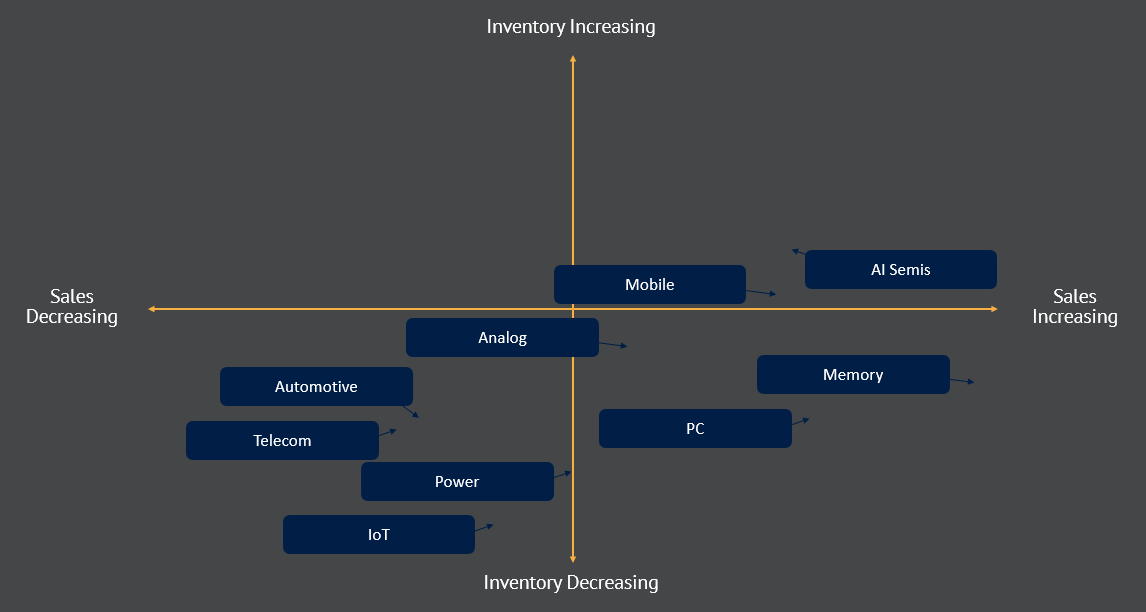

Automotive, Telecom, and Smartphones are in the Valley

Everywhere you look, that is not AI; Semiconductors are ironically not in a great place. TSMC is seeing strength in leading-edge AI, but the lagging edge is in a historic glut. I think it’s safe to say this piece is entirely wrong and depreciated now. Every lagging edge fab has too much capacity now.

Automotive, in particular, had a rough year. It was a relative darling in 2022, kept up with the market in 2023, and an absolute implosion in 2024.

If you zoom specifically into the mess, most of the most brutal hits were automotive, analog, and smartphones. These companies did well in last year’s runaway (60%!+) year but lagged this year. The ironic result is that the median Semiconductor company didn’t have a good but horrible year!

Ironically, I have long believed more dispersions in the semiconductor industries will exist. The different product lines will start going through various cycles, and this year is the perfect encapsulation.

Now, I want to mention that semiconductors are inherently cyclical. Historically, it has been a great idea to try to “buy low,” while Automotive has many reasons for concern, I find it among the most interesting segments right now. We could see the inverse - that AI does poorly, and automotive, power, IoT, and Telecom do particularly well next year.

Meanwhile, Memory, PC, and Mobile are somewhere in the middle. Yesterday’s laggards are likely tomorrow’s winners and vice versa. But enough about the niche semiconductors, let’s talk about the big story: AI.

AI is Not Stopping Yet

Nvidia had a fantastic year, which is unsurprising, as they continue to be the standard to which all other companies compare themselves. Their GB200 product is almost perfect for what’s coming. While Marvell and Broadcom had great years, they are not Nvidia yet.

I will admit. After two incredible years of the AI trade, I was worried that it would become long in the tooth at the end of the year. Ironically, one of the most bullish things possible happened at the end of the year: O3. While the world was focused on scaling laws, there are still many dimensions of improvement ahead of us, and O3 gave us a taste of the future.

I believe that there is no practical limit to the improvements of models other than economics, and I think that will be the real constraint in the future. It is reasonable that if we spent infinite dollars on a model, it would be improved. The problem is whether infinite dollars would make sense for a business.

That is going to be the key question for 2025. How do the economics of AI make this work? One of the core assumptions about the internet has just been broken. Marginal costs now exist again, meaning that most hyperscalers will become increasingly capital-intensive.

The era of aggregation theory is behind us, and AI is again making technology expensive. This relation of increased cost from increased consumption is anti-internet era thinking. And this will be the big problem that will be reckoned with this year. Hyperscaler’s business models are mainly underpinned by the marginal cost being zero. So, as long as you set up the infrastructure and fill an internet-scale product with users, you can make money.

This era will soon be over, and the future will be much weirder and more compute-intensive. Looking back on the 2010s, we will probably consider them a naive time in the long arc of technology. One of our fundamental assumptions about this period is unraveling. This will be the single most significant change in the technology landscape going forward.

Capital was cheap from ZIRP, and returns on some of that capital were near infinite. That era of technology is behind us, and the rise of AI means the rise of a new cost curve that none of the major technology companies have ever been in a paradigm that software improved with more capital instead of having extremely high fixed costs with zero marginal costs. Now, we have extremely high fixed costs and high marginal costs. This flips everything.

The economic implications are uncertain, but I have many thoughts on the capital cycle we are entering. I hope to write another follow-up piece on capital cycles soon.

2024 Overview

So, let’s move it back to stocks. Hilariously enough, it was a pretty crappy year for semiconductors if you didn’t own NVDA, CRDO, COHR, ALAB, AVGO, Advantest, MRVL, TSM, or ARM. There are a few smaller capitalization companies that I am missing from that list, but directionally, it’s the truth.

There’s a lot of pain under the surface. ASML, one of the last paradigm’s biggest winners, was flat, while Samsung and AMD were down 30 and 18 percent. The following 10 biggest companies, respectively, are TXN, QCOM, AMAT, ADI, MU, KLA, and INTC. Most of these companies were either up low double digits or down 60% in the case of Intel. That’s a staggering dispersion of outcomes in what has historically been an industry with tighter returns.

I think maybe this year that changes. I am not bold enough to call the end of the AI trade, but I believe this year will be the year of AI economics, and it’s unlikely for triple-digit returns to continue. Now, how I see this playing out is relative performance in line with the broader semiconductor space or market and not the eye-watering triple-digit year again.

One of my favorite visualizations is valuation compared to itself. Everything below the line got cheaper, while everything above got more expensive. The companies that cheapened that did well are likely opportunities, and that list looks like it’s semicap, AMD, MPWR, and Memory. I think that AMD is justified, but I find it amazing that SNPS, BESI, CDNS, MPWR have gotten cheaper.

Another way to look at this is this handy quadrant chart. The “best” names are in the bottom right, as they became less expensive while their estimates increased. For this last year, that’s SMCI, MU, STX, SK Hynix, PI, WDC, ONTO, ACMR, SNPS, AMAT, QCOM, Disco, Cand DNS, LRCX, CRDO, FN.

There are other ways to look at this. Companies with lowered estimates but longer-term improvements and moats are likely great fishing places. Meanwhile, companies with higher estimates that still do not account for improving fundamentals are also great places to look.

Overall, the entire space has become more expensive this year on average, driven by a few outliers that pushed the multiple higher. I’m always a lover of cheap out-of-favor names with some improving story, and that’s probably where I’d look in the future.

Anyway, let’s do a segment-by-segment overview of the markets and what I think the next year will hold. I’m going to paywall everything that is not AI.

AI Semiconductors (NVDA, AVGO, MRVL)

The current place in the semiconductor cycle is decidedly bullish. We are in a typical upswing of the AI semiconductor market. Inventory and Revenue are growing quarter on quarter. I have quite a few historical periods on here, and the type of growth we are seeing is consistent with the impressive periods of growth in the 2020-22 cycle, and the 16-18 cycle. The one thing I will note is that it’s probably time to watch inventory builds.

If you notice, Inventory is growing faster than revenue. Given that Nvidia is the majority dollar-weighted component of this basket, this makes sense for the coming Blackwell ramps.

The one thing that gives me pause is that spending this much time in the top right quadrant is infrequent. While I continue to believe in the AI ramps to come, especially the GB200, this has to warrant a bit of caution compared to the past. Results tend to stay in the top right quadrant for ~8 quarters, and we are 6 quarters into this current upswing.

While O3 makes me hyper-bullish on Nvidia, it seems likely that the best days of percentage growth are likely behind us. AI Semiconductors will likely remain strong, with results in the top right quadrant (expanding revenue and inventory). It’s been quite a strong cycle, but nothing lasts forever. While I see no clouds on the horizon, I am wary of history’s past lessons that semiconductors are indeed cyclical.

Any change in spending could turn the cycle, but all AI semiconductor companies seem to be in the perfect place. They will do well next year, just not as well as the past 2 years. These are Nvidia, Marvell, and Broadcom. While multiple has expanded, so have revenue estimates. Marvell, in particular, seems to have a huge opportunity, while Nvidia’s GB200 ramp is another opportunity for meaningful growth next year.

Please consider subscribing for more on Automotive, Memory, Mobile, Semicap, PC, and my “favorite ideas!”