Intel's Mobileye Stub and Positioning

Semis are not that crowded & I take a crack at valuing Intel (model attached)

Before we talk about Intel’s Mobileye announcement - I wanted to highlight something I’ve noticed in the semiconductor space. It’s been no secret there has been a large de-grossing (moving gross leverage down) in the market. In particular, many SMID cap companies are experiencing bear-market-like drawdowns while the indices are relatively unscathed. Large caps are leading, meaning that if you don’t own FAMNG - you are feeling pain. An example of this dynamic is highlighted by Carter Braxton.

Positioning

Probably one of the hardest-hit places right now is SaaS - where a huge run since 2019 has kept this sector extremely popular among funds. Meanwhile, many hedge funds were looking to short anything and started to short semiconductors on DRAM price weakness and a single month of smartphone weakness in China.

As funds deleveraged, the crowded longs were sold and the crowded shorts were bought back. The results of the deleverage were drastic, and best summarized in this chart below comparing software to hardware returns YTD.

I want to caution you - this is not a sustainable trend. I usually don’t see a deleveraging and say “this is wonderful for my stocks!” - but rather take a step back and wonder if this is good at all. Usually, there’s some kind of snapback to the previous regime, and in my view, I think that Semiconductor stocks could have a bit of a cooling-off period here. Thursday’s relative performance seems to indicate that.

But the real value of the deleveraging is the litmus test for the crowdedness of the sector - and I’m happy to say with the exception of maybe Nvidia - semiconductors are anything but crowded. My biggest fear about semis is that the themes I write about are more crowded and appreciated than I thought - which in turn could make the forward results poor.

The positioning tells us that some investors still do not buy the secular story of semiconductors - and that’s great! The results should prove themselves, and when eventually Mr. Market falls in love with semiconductors, even the skeptics will be interested.

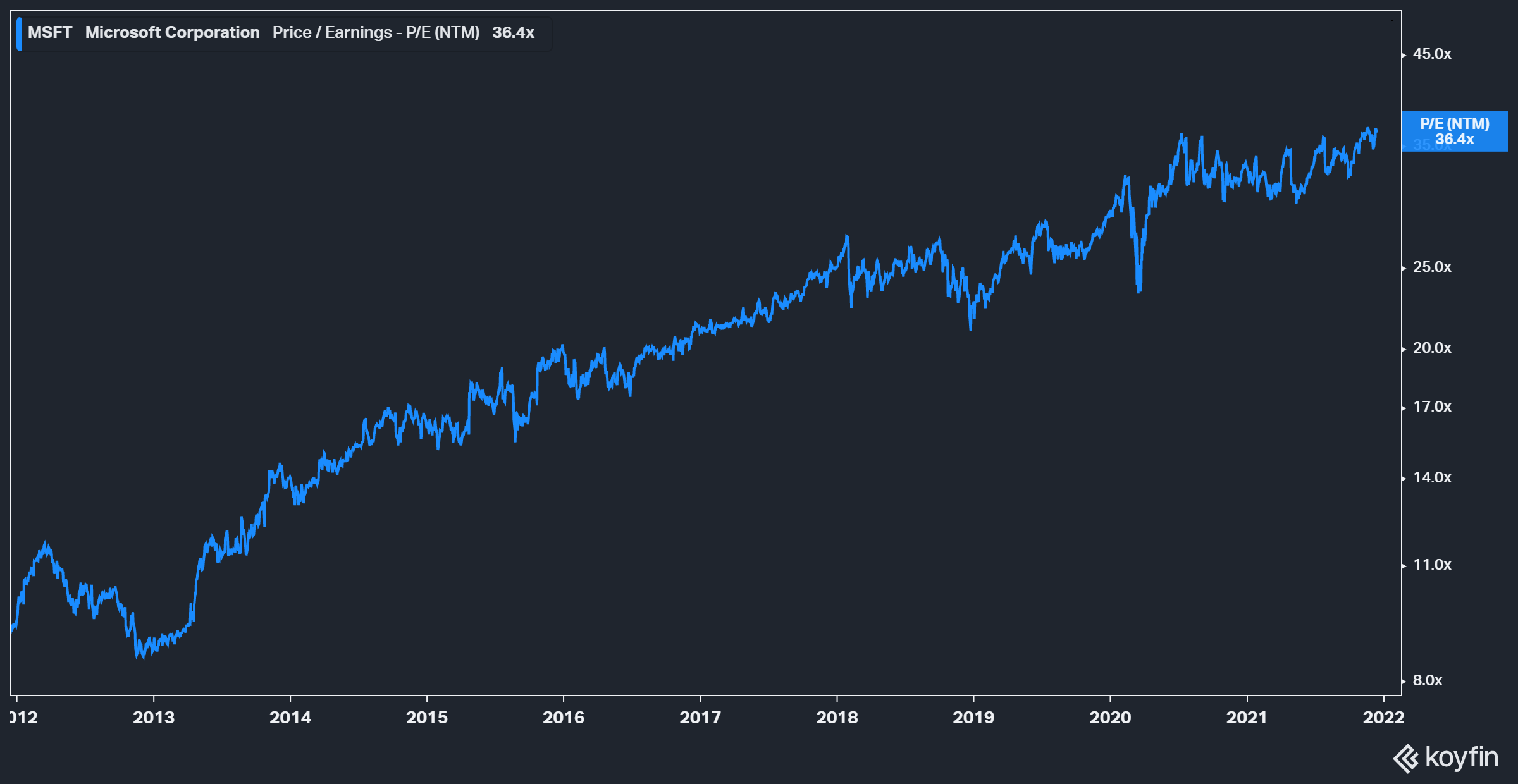

I liken it to the regime change that has happened in the last 5 years within software stocks - where software went from a relative loser industry with a bad reputation to the belle of the ball. Nothing better exemplifies this than the P/E of Microsoft.

I don’t think we will get something this drastic in semis broadly - and if we do it’s already happening in the highest fliers of the space like Nvidia. But I find that the cyclical to secular thesis is still compelling. The same investors who hated Salesforce for making no meaningful FCF in 2012 are buying the shares hand over first in 2021. It might take that long - but I believe that will eventually be the case for semicap.

Underlying these low multiples compared to the market is a financial model that works. These businesses have actually outperformed Microsoft with less modest multiple expansion - and obviously a bumpier ride. But if you believe that semis and semicap is a secular trend (I do), I think that investors will eventually appreciate these businesses for what they are - quasi-monopolies that are levered to the digitalization of our world.

A brief checkup on the positioning that they are under-owned in Long / Short TMT hedge funds means we have quite a while before they are loved. And that’s fine - the narrative comes after the results.

Intel Mobileye Stub

First I think it’s not very inspiring that Intel decided to do a public market equity stub of Mobileye. It’s reminiscent of VMWare, the former company that Pat Gelsinger led. The only difference here is that I would love to own Mobileye but would hate to own VMWare. So before dismissing the optically expensive $50 billion dollar headline - I want to dive a little deeper.

Part of the process of an IPO is the elusive media leak. Intel leaks an IPO price to the press to generate a headline and tries to measure the reaction. That’s where the $50 billion dollar number comes from, Intel themselves. That price is the first level of negotiation where Intel throws out a really high offer and sees if anyone will bite.

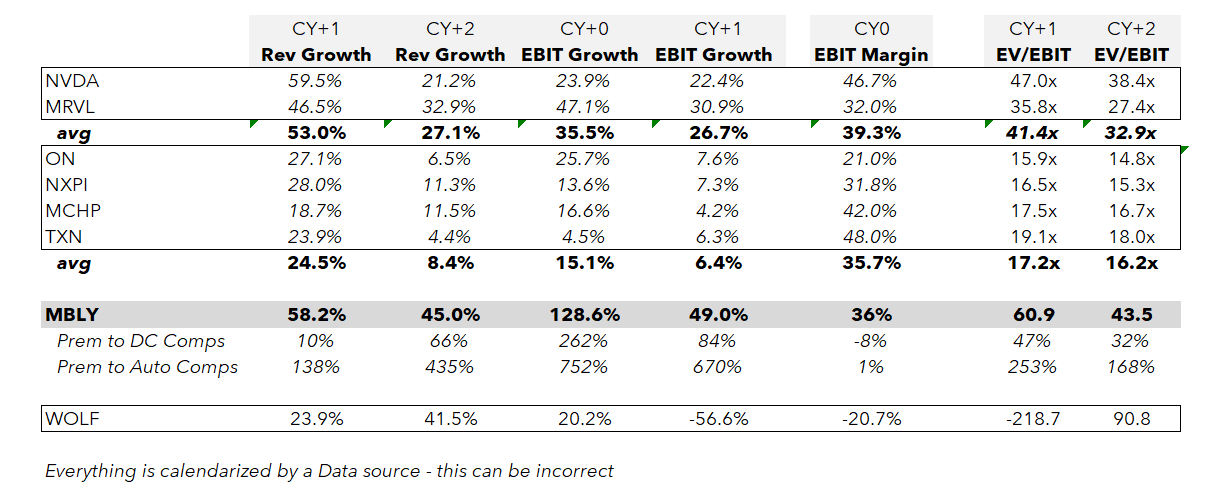

Intel is trying to gauge if investors and the public will take a $50 billion dollar Mobileye seriously, and at first blush, it seemed hefty. Even given my extremely bullish stance on automotive semiconductors (I talk a bit more about it here), that price seems insane. But I put my skepticism aside and made a simple comp sheet to see if Mobileye deserves the valuation.

That $50 billion dollar valuation seems possible! Mobileye would trade at a hefty premium to other automotive semiconductor stocks, but given they have 100% revenue exposure instead of 30-40% I believe that’s justified. And if we were to compare Mobileye to the likes of Nvidia and Marvell, its growth and margins would be a premium but automotive exposure is scarce. I can buy $50 billion. So what does that mean for the value of Intel as a whole?

My first reaction to the news was Intel ex-Mobileye should be cheap as hell, but the more I dug the less impressed I became. The big first problem is what exactly is the earnings power of Intel in 2022? I can say with confidence I believe that the street is still too high - I think they earn ~$3.20-3.40 a share and consensus is still at ~$3.74 a share. The problem is that the revenue guidance is completely gone in the near term and we are just left with a long-term guide, and even then we were given “above 50% margins” but no further detail. That’s a lot of uncertainty - and your belief in a growing data center or consumer group with just a bit of margin lift can swing numbers +/- 10%. What I’m trying to say is that in order to have a view on the standalone Intel being cheap or not - you have to have a strong view of their numbers. I don’t have that. I attached my quick and dirty model so you can input assumptions yourself.

My stab at the numbers put Intel at just around 10x 2022 EBIT - which is pretty worrying. Something I’ve noticed is that when a company is in freefall it always seems to stick to a round number in whatever multiple is easiest to grasp to. EBITDA is utterly unforecastable, and EPS is going to have a litany of adjustments. I think ~10x is not a coincidence.

In my experience, that round number is kind of worrying. I think of Stericycle - a company I refreshed the valuation on every 6 months from 2016 to 2019 and no matter what would happen the multiple would be at 11-12x EBITDA and EBITDA estimates, of course, were always too high. I think right now the direction of estimates is more important than multiple - and the 10x EBIT multiple doesn’t look that attractive to me.

Intel has traded for 10x EBIT in the past even without the Mobileye stake valued independently of Intel. Intel traded at 10x EBIT as recently as 2019 - and shares are essentially sideways since then.

I was hoping that Intel was either too cheap to pass (5-6x EBIT) but once again this is a hope trade. I still feel like it’s too early to catch the knife at Intel. I actually have become a lot more positive on the culture and execution but there is a lot of wood to chop, and I think when the signs that give you confidence in their turnaround do appear, you’ll maybe miss the first 20% but have more confidence to bet in size.

I think we are still in wait-and-see mode, and given how long it will take to ramp Intel Foundry Services, we have time to watch and wait. If you’re not satisfied with yourself - take a look at my attached model to tinker with the assumptions yourself. (Behind the paywall)

That’s all for this week folks. I will hopefully have a 2022 outlook for ya’ll next week. Hope everyone is staying safe during these weird times.

Hi Doug, the Discord invites you attached in a previous piece is invalid, could you provide again? Thanks.

Why are you saying semicap is underowned?