Micron and WFE

The uncertainty of the good, versus the knowable bad. WFE is going to be fine folks.

Micron Earnings

Just two weeks ago, I wrote about how I thought this was a mid-memory cycle. I mainly supported the memory companies if you didn’t read between the lines.

Fast-forward a week, and it seems that the calls for the end of memory were a bit premature.

I tweeted how everyone was short on this earnings result, and the outcome would always be the opposite. Here’s a little wisdom: markets are discounting and anxiety machines. Almost always, nothing is ever as bad as feared, and this was no exception.

Let’s talk about the results and what has changed.

Micron Technology reports Q4 EPS $1.18 ex-items vs FactSet $1.11

Reports Q4:

Revenue $7.75B vs FactSet $7.65B

Q1 Guidance:

Non-GAAP EPS $1.74 +/- $0.08 vs FactSet $1.52

Revenue $8.70B +/- $200M vs FactSet $8.27B

Non-GAAP gross margin 39.5% +/- 1.0% vs consensus 38.7%

Many expected a much worse guide than this, to $8 billion. The reasoning was driven mainly by falling DDR4 spot prices and overstocked inventory in Korea. Dylan tweeted that spot prices matter less than ever because many logic players purchase on contract and package with the die. That is one part of it. The other part is that many memory OEMs are dumping their DDR4 inventory as production shifts to DDR5. Investors focused on a backward-looking metric when the reality was that the results were good.

I think the reality is the market is going to freak out about things it can see well, which is DDR4 pricing (and a minority of the market now), and never believe the unknowable HBM demand will be fine. Furthermore, there’s been a persistent oversupply of HBM calls despite almost any sane bottoms-up build-up saying otherwise.

Let’s walk through specific callouts specifically focused on HBM.

HBM margins are accretive to DRAM margins even as DRAM margins have improved.

Even as our DRAM gross margins improved, our fiscal Q4 HBM gross margins were accretive to both company and DRAM gross margins indicative of our solid HBM yield ramp. We expect to achieve HBM market share commensurate with our overall DRAM market share sometime in calendar 2025.

Moreover, they expect it to be accretive for fiscal year 2025. The answer is yes, despite prices being locked in already. HBM is still a hot market, folks.

Now regarding your questions on gross margin being accretive, yes, we would expect our HBM business to be accretive for our fiscal year 2025. Beyond that, really not providing any further details. And yes, you are right that our volume and pricing for HBM is locked up for 2024 as well as for 2025 time frame, calendar year 2024 and calendar year 2025.

What’s more, HBM, on the calendar for 2025, is expected to be over 25 billion.

We expect the HBM TAM to grow from approximately $4 billion in calendar 2023 to over $25 billion in calendar 2025. As a percent of overall industry DRAM base, we expect HBM to grow from 1.5% in calendar 2023 to around 6% in calendar 2025.

That’s a crazy CAGR, and I wrote in my 2024 year-end outlook that I expected the 2024 estimate to be smashed. The “bull case” was 9 billion at the time, which looked like it would be extremely light.

If it continues to grow at this rate, HBM will be the second-largest market in memory before the decade's end! What a crazy growth story!

Let’s talk more about the Bit cannibalization thesis I outlined earlier this year.

Leading-edge supply is tight because industry in '22, '23 time frame with reductions in CapEx and CapEx-efficient industry-wide transitions to the newer technology nodes, the wafer capacity has come down from the peak levels in meaningful ways. So the lower wafer capacity compared to the peak of 2022, as well as the HBM 3:1 trade ratio, these are the ones that are overall keeping the industry in a tight supply. And tight supply, not just for HBM, but also for non-HBM part of the market.

There continues to be a solid supply-demand balance. What’s more, it looks like Micron is going to bite on the “New Era of NAND” thesis. In this presentation, WDC pleaded with the market to stop spending capacity on the NAND transition and lengthen the industry transition.

Here’s the public confirmation of WDC’s message: now it’s time for the rest of the industry to follow suit.

Given the significant reduction in the industry wafer capacity in NAND and the ongoing low NAND CapEx environment, we also expect a healthy industry supply-demand environment for NAND in calendar 2025. NAND technology transitions generally provide more growth in annualized bits per wafer compared to the NAND bit demand CAGR expectation of high teens. Consequently, we anticipate longer periods between industry technology transitions and moderating capital investment over time to align industry supply with demand. This can reduce both R&D expense growth and capital intensity in NAND over time, which can contribute to the improved financial health of the NAND industry.

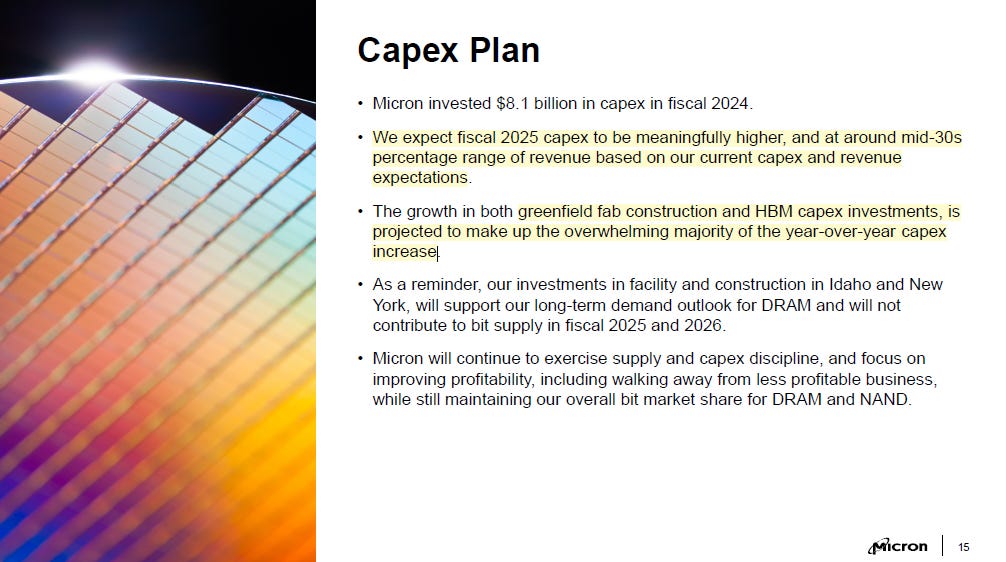

I think that’s good. WDC doesn’t want to spend on capex, and all DRAM players wish to spend on HBM. Despite that, this will all, in aggregate, be a meaningful step up in capex.

They gave their preliminary capex guide and expected it to be “meaningfully higher.” That implies more spending on shells than tools, which raises some interesting questions.

Doing the math implies about ~13.5 billion dollars of capex at today’s revenue expectations. That’s a new high in capex compared to fiscal year 2022 and should be a clearing event for memory WFE spending. Speaking of which, this brings me to my second and paywalled section: Semicap.